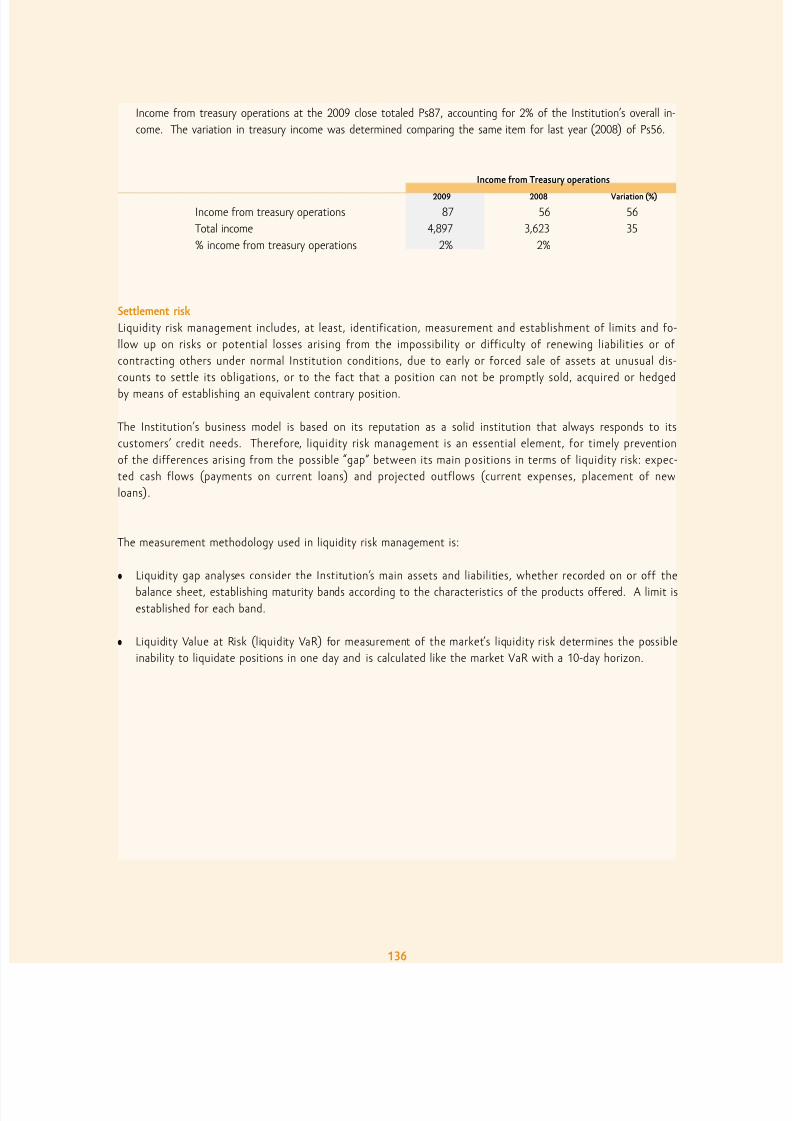

RSE - Reporte de Sustentabilidad de Compartamos Banco

146

STRENGTHS TO KEEP ON GROWING Annual and sustainable report 2009 SOCIAL, ECONOMIC A ND HUMAN VALUE

-

Upload

capacitarse-cursos-de-rse -

Category

Documents

-

view

225 -

download

0

Transcript of RSE - Reporte de Sustentabilidad de Compartamos Banco

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 1/146

STRENGTHS TO KEEPON GROWINGAnnual and sustainable report 2009

SOCIAL,ECONOMIC

AND HUMANVALUE

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 2/146

Business model

Aguascalientes 2

Baja California 5

Baja California Sur 2

Campeche 4

Chiapas 22

Chihuahua 5

Coahuila 13

Colima 3

Distrito Federal 9

Durango 5

Estado de México 26

Guanajuato 14

Guerrero 16

Hidalgo 6

Jalisco 11

Michoacán 13

Morelos 8

Nayarit 3

Nuevo León 13

Oaxaca 16

Puebla 22

Querétaro 3

Quintana Roo 6

San Luis Potosí 7

Sinaloa 6

Sonora 8

Tabasco 11

Tamaulipas 8

Tlaxcala 6

Veracruz 41

Yucatán 10

Zacatecas 1

325 Service Offices

in Mexico

Contents

2 Operative and financial

highlights

3 Results of the generation

of social, economic and

human value

4 Message from the

Chairman of the Board

of Directors

8 Social value

20 Economic value

36 Human value

60 Compartamos with

the Community

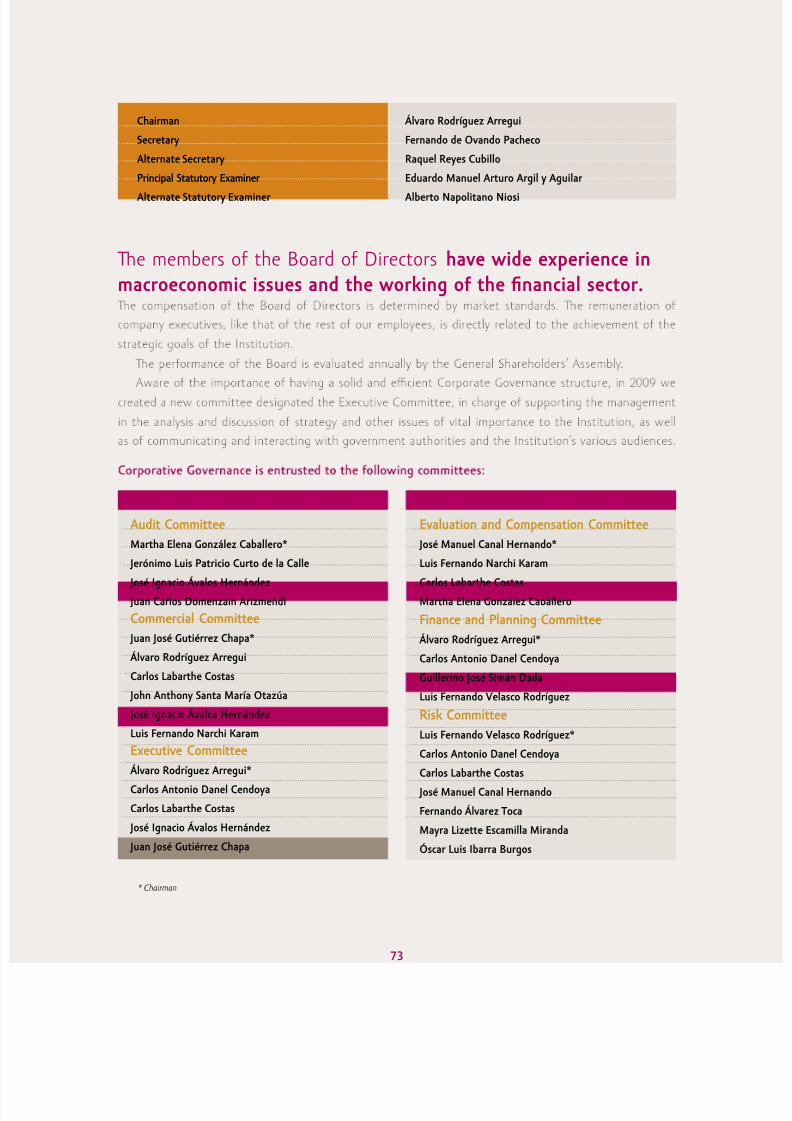

72 Corporate Governance

80 Honors and distinctions

83 GRI Index

89 Audited Financial Statements

Our infrastructure

Fund

ing

• Promotion • Group

form

ation

• S a v i n g s • C r e d i t a n a l y s i s • G r a n

t i n g o

f c r e d i t s

• Freq u

ent con

tact

with c

lients

• N e w c y c l e o

f t h e c r e d i t • S y

s t e m a t i z a t i o n • Week ly r

einbur

semen

t • Fin

ancial educati

M a r k e t R e s e a r c h

Produ

ct D

eve

lop me nt

R e c r u i t i ng and Training

F i na n c i a l S e r v i c e

s

Culture

Compartamos´ Philosophy

P r ofitability

T e a m w o r k

R e s p o n s i b i l i t y

Service

Passio

n

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 3/146

Sustainability Model

Sence of transcendence

Generation

Commongood

Social value

Humanvalue

Economic valueIntegral

development Opportunities

e sustainability model of Compartamos Banco incorporates our interest groups,determined through a process of impact evaluation and consultation with different

areas, taking into account the strategic guidelines of the institution. Our

sustainability model, which derives from our long-term vision, is based on

our values and is in harmony with our business model.

e HumanBeing

Sense of purpose and mystique, centered on the personCompartamos Philosophy

Passion Teamwork Profitability Service Responsibility

FuturegenerationsEmployees Suppliers Authorities Community Competitors InvestorsCivil organizationsClients

Education Family Health Environment Economic

development

Operatingand financial

results

How?

For whom?

Where?

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 4/146

Our mission

We are a bank that generates social, economic, and human

value. We are committed to people; we generate

opportunities for development within low-income segments

of the population. ese opportunities are based on

innovative and efficient, large scale business models and

on transcendental values which generate an internal and

external culture while building lasting relationships and

trust, therefore contributing to a better world.

Our visionWorking with self-accomplished individuals, to be the leading

microfinance bank, offering savings, credit and insurance

products, and extending the borders of the financial sector.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 5/146

Social value

Promoting development by providing access to financial services to the greatest number of

people in the shortest possible time.

Economic valueWe have created a profitable and strong institution in which private capital may participate,

making the industry more attractive for others to compete.

Human valueWe trust people, we trust in their word, their willingness to succeed and their ability

to develop their skil ls. is is why we promote means that offer clients and employees

the opportunity to become better people.

Mystique: e experience of our six institutional values:e person: We want to help individuals to be better persons. For this, we promote their

development according to an integrated model that considers all the dimensions of an

individual (physical, intellectual, social-family and professional).Service: We offer ourselves to others because we have an authentic interest in the

individual.

Responsibility: We comply with our duties with excellence and we assume the

consequences of our actions.

Passion: We love what we do.

Teamwork: We collaborate with others, making every effort to reach greater goals.

Profitability: We do more with less, being productive and efficient.

Our Ethics and Conduct Code

To live according to our philosophy is one of our principal concerns. In order to do so,we have an Ethics and Conduct Code whose central objective is “to share our ethical

values, defining the conduct to be followed by stockholders, members of the Board of

Directors, corporate secretaries, and employees.” We also have an Ethics and Conduct

Code for all of our suppliers, by which the chain of value is further reinforced.

e essential goal of Compartamos Banco is thegeneration of social, economic, and human value.

1

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 6/146

Operative and nancial highlights

2

2007 2008 2009 Var 08/09 %

Service Oces 252 314 325 3.5%Employees 4,277 5,946 7,364 23.8%Clients 838,754 1,155,850 1,503,006 30.0%Loan portolio (millions o Mexican pesos) 4,186 5,733 7,645 33.4%Loan balance per client (Mexican pesos) 4,991 4,960 5,086 2.5%Non-perorming loans 1.4% 1.7% 2.4% 41.2% (Millions o Mexican pesos)Net operating income 2,824 3,623 4,897 35.2%Interest income 2,803 3,567 4,811 34.9%

Interest expenses 177 248 318 28.2%Net interest income 2,580 3,375 4,579 35.7%Net interest income ater provisions 2,510 3,290 4,297 30.6%Net operating revenue 2,466 3,247 4,257 31.5%Operating expenses 1,237 1,807 2,240 24.0%Net operating income 1,237 1,440 2,017 40.1%Net income 877 1,120 1,490 33.0% Operating margin

(Operating income/Average portolio) 33.8% 29.5% 30.2% 2.4%Net margin

(Net income/Average portolio) 24.1% 22.6% 22.3% -1.3%Operating margin on productive assets

(Operating income/Average productive assets) 29.6% 22.7% 24.0% 5.7%Net margin on productive assets

(Net income/Average productive assets) 21.1% 17.4% 17.7% 1.7% Asset otal assets (millions o Mexican pesos) 145 198 170 -14.1%otal loan portolio (millions o Mexican pesos) 4,186 5,733 7,645 33.4%Non-perorming loans (millions o Mexican pesos) 57 98 186 89.8%Cash 17.7% 27.2% 16.0% -41.2% Liabilitiesotal liabilities (millions o Mexican pesos) 2,818 5,274 5,187 -1.6%Liabilities with cost (millions o Mexican pesos) 2,608 4,944 4,697 -5.0%otal stockholder’s equity (millions o Mexican pesos) 2,285 2,856 4,061 42.2% Earnings per share/EPS (Mexican pesos) 2.1 2.6 3.5 33.6%

ROAA 20.8% 16.9% 17.1% 1.2%ROAE 47.5% 43.6% 43.1% -1.1% Book value per share (Mexican pesos) 5.3 6.7 9.5 41.8%Prices at the end o the year (Mexican pesos) 47.3 25.0 67.5 170.0% otal shares or calculation EPS and BVPS 427,836,876 427,836,876 427,836,876 0.0%

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 7/146

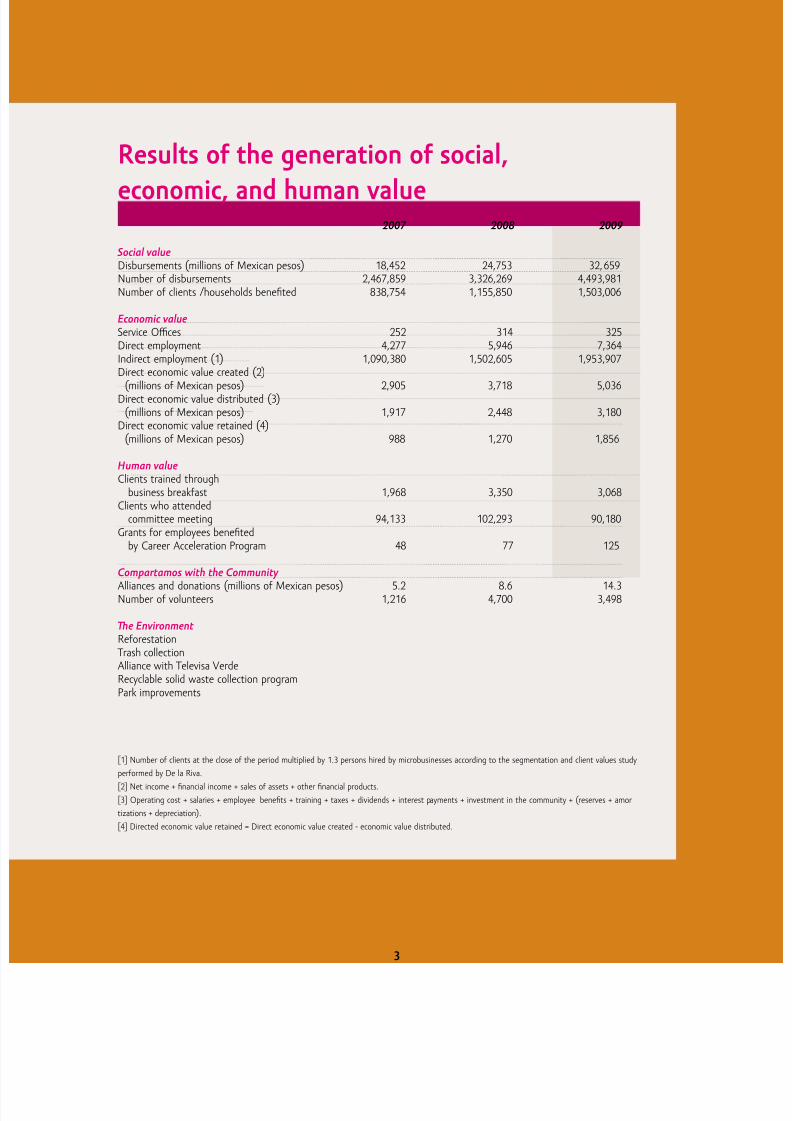

3

Results o the generation o social,

economic, and human value

2007 2008 2009

Social value Disbursements (millions o Mexican pesos) 18,452 24,753 32,659Number o disbursements 2,467,859 3,326,269 4,493,981Number o clients /households beneted 838,754 1,155,850 1,503,006 Economic value Service Oces 252 314 325Direct employment 4,277 5,946 7,364Indirect employment (1) 1,090,380 1,502,605 1,953,907Direct economic value created (2)

(millions o Mexican pesos) 2,905 3,718 5,036Direct economic value distributed (3)(millions o Mexican pesos) 1,917 2,448 3,180

Direct economic value retained (4)(millions o Mexican pesos) 988 1,270 1,856

Human valueClients trained through

business breakast 1,968 3,350 3,068Clients who attended

committee meeting 94,133 102,293 90,180Grants or employees beneted

by Career Acceleration Program 48 77 125

Compartamos with the Community Alliances and donations (millions o Mexican pesos) 5.2 8.6 14.3Number o volunteers 1,216 4,700 3,498 Te Environment Reorestationrash collectionAlliance with elevisa VerdeRecyclable solid waste collection programPark improvements

[1] Number o clients at the close o the period multiplied by 1.3 persons hired by microbusinesses according to the segmentation and client values study

perormed by De la Riva.[2] Net income + nancial income + sales o assets + other nancial products.

[3] Operating cost + salaries + employee benets + training + taxes + dividends + interest payments + investment in the community + (reserves + amor

tizations + depreciation).

[4] Directed economic value retained = Direct economic value created - economic value distributed.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 8/146

Mensaje del Presidente del

Consejo de Administracion

4

Message rom the

Chairman o the Board

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 9/146

Mensaje del Presidente del

Consejo de Administracion

5

results obtained with this product are a particular source o pride, encouraging us to increase our eorts

to oer our clients and their amilies an opportunity to improve their quality o lie.

We also ostered a culture o planning and oresight in our clients through our lie insurance pro-

ducts. Compartamos Banco is the largest microinsurer in the world, with 90.3% o our clients having

lie insurance as an added eature o their loan. Active policies at the end o 2009 numbered 1.9 million,

o which 1.4 million had been acquired or extended voluntarily in the course o the year.In spite o the diculties o the credit market in 2009, Compartamos Banco was able to increase

its nancing or uture growth, as well as to improve the terms and costs. Its primary objective was

to ensure unding through the diversication o its sources o nancing. An example o this was the

successul placement o Ps. 1,500 million o long-term debt bonds in domestic market (Certicados

Bursátiles). In line with our long-term strategy, our own capital base provides an important oundation

or growth, making Compartamos Banco one o the most solid banks in the Mexican Financial system.1

Te perormance o our shares was outstanding, as the share price o COMPAR O went rom Ps.

25.0 at the end o 2008 to Ps. 67.5 at the end o 2009, representing a yield o 170.2%, which com-

pared avorably with the 43.5% growth o the IPC, the main benchmark index o the Mexican Stock Exchange.

We remain committed to reaching the greatest number o people in the shortest possible time,

serving to the low income sectors o our society. An indicator that refects the prole o our clients is

the size o our average loan: Ps. 7,267, which represents 6.2% o GDP per capita.2 Tis percentage

compares with the standard averages o 25.5% o GDP and 17.8% o GDP in the Latin American and

Asian micronance industries, respectively.3

In 2009, we had the opportunityto demonstrate the strength and eciency o our business model.

1 Source: CNBV data rom December 2009.

2 Source: INEGI data rom December 2009.

3 Source: Micronance Inormation Exchange (MIX) data rom December 2008.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 10/146

6

Managing to achieve more with less, Compartamos Banco reduced its annual cost per client by

5.38%, rom Ps. 1,781 in 2008 to 1,685 in 2009. In comparison with the Latin American average o Ps.

2,488,4

this makes Compartamos Banco one o the most ecient micronance institution in the region.Maintaining excellent credit quality is one o the main goals o Compartamos Banco. Our employees

are given incentives to encourage successul collection and recovery o credits, so we have been able to

maintain our leadership in this area. Non-perorming loans represent only 2.4% o our total portolio,

up rom a year beore but still below the average o the Mexican banking. Te rise can be attributed

to a change in our product mix, with home improvement loans and business expansion loans (Crédito

Mejora tu Casa, Crédito Comerciante, and Crédito Crece tu Negocio) increasing their share within the

portolio as a whole. Tese products have a dierent risk prole rom that o Crédito Mujer, so their in-

creasing share in the total portolio can be expected to cause the percentage o non-perorming loans to

increase as well. We believe, nevertheless, that the growth o these products is in line with our strategy

o oering more and better products and services to our clients. At the same time, as part o our eortto maintain excellent credit quality, the process through which these higher-risk products are granted

has been restructured, and the tools designed to ensure that our clients avoid excessive debt loads have

been reinorced. Tanks to the larger number o clients and subsequent increase in revenues, but above

all thanks to our leadership in eciency, net income increased this year by 33.0% to Ps. 1,490.

In 2009 Compartamos Banco consolidated its position as one o the leading nancial institutions in

Mexico in terms o credit quality and nancial strength. Te bank’s perormance has been recognized

by the investment community, which has shown its condence by acquiring long-term debt issued by

Compartamos Banco and purchasing our shares. We will continue working with the ratings agencies to

ensure that one day Compartamos Banco enjoys the credit rating it deserves.In 2009 we sought to consolidate the quality o our client service through 325 service oces and

more than 9,000 convenience points where our clients can make their payments. It is a priority or Com-

partamos Banco to continue expanding this network and so acilitate transactions with our clients.

Also, as part o our commitment to Mexico, we collaborate constantly with the regulators in buil-

ding together a avorable environment or the micronance industry in the country. We are working

constantly with them to make it possible or more o our clients to be served through banking corres-

pondents, creating a nationwide network where our clients can make payments easily and eciently,

signicantly reducing their transaction costs.

Consistent with our aim o creating human value, in 2009 we created 1,418 new jobs, bringing the total

number o our employees to 7,364. Some 250,000 people in the communities where we operate were bene-ted by dierent Compartamos Banco social programs, carried out by volunteers rom within team members

and our employees, with the enthusiastic participation o clients and other civil society organizations.

In 2009, we have put special emphasis on training in 2009, seeking to promote the integral develop-

ment o our employees and reinorce their ethics and values. We implemented programs to develop both

4 Source: Micronance Inormation Exchange (MIX) data rom December 2008, based on an exchange rate o Ps. 13.45 to the US dollar.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 11/146

7

proessional and interpersonal skills which contributed to their growth as individuals. As a result o these

eorts, we received several workplace distinctions in 2009.

In line with our philosophy o social responsibility as an economic agent, we channeled more thanPs. 13 million into education, economic development, environment, and social projects, or the benet o

individuals that live in the same communities as our employees and clients live. Also, thanks to the parti-

cipation o more than 2,200 employees, clients, and volunteers, and with the backing o local authorities,

public spaces were rehabilitated to promote recreation in 23 dierent communities. In line with this eorts,

I am happy to report that starting in 2010 Compartamos Banco is committed to channeling 2% o its net

earnings into social programs every year.

Our outlook or the year 2010 is positive, with an enormous market potential, highly trained and moti-

vated personnel, a solid balance sheet, diversied sources o unding, consolidated leadership, and –most

importantly– a great organizational mystique and a business model that ulls our sense o purpose: the

generation o social, economic, and human value.I would like to reiterate that this year’s excellent results were made possible by the passion, proessio-

nalism, and commitment o our employees, and my deepest recognition is extended to them. I would also

like to thank our shareholders and top management or their support during my term as Chairman o the

Board. My acknowledgement also to José Manuel Canal Hernando, who stepped down as Chairman in

2009. During his tenure and under his leadership, we dened the strategic direction under which we are

operating today with success. I consider Manolo a riend, mentor, and example to ollow, and I remain in

debt with him or his excellent leadership.

With Compartamos Banco prepared in all areas to achieve new goals, our uture is promising.

Álvaro Rodríguez Arregui

Chairman o the Board o Directors

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 12/146

SOCI

8

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 13/146

Promoting development by providing

access to nancial services to thegreatest number o people in theshortest possible time.

“Beore Compartamos Banco gave me the rst loan I did not have enough money

to buy equipment and sometimes I could not ll orders, but now I have doubledmy sales and much more customers have arrived. ”

Juan Millán Pérez Puebla

7.4%

89.4%

2.2%

9

VALUE

AL

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 14/146

10

We promote productive projects that translateinto higher incomes, more jobs, and a better

quality o lie or more than 1,503,006clients and their amilies all over Mexico.Since the ounding o Compartamos Banco,we have been ully committed to the socialdevelopment o Mexico.

> We granted working capital loans to 714,069new clients.

> Our average credit was Ps. 7,267.

> We granted 109,876 home improvement loans,beneting the quality o lie o our clients and their amilies.

> All o our Crédito Mujer clients have a lie in-

surance policy, granted ree o charge, includingloan remission in the event o decease. During

the year, 1,350,408 additional lie insurancepolicies were taken out.

4,493,981 disbursements in2009.

We served to more than86,000 people through our call center.

In 2009:

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 15/146

11

We care about every little detail o

the service and to extend the positiveimpact o our eorts at all levelso our customers’ lie.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 16/146

Growth and leadership o Crédito Mujer

12

1 C = Monthly amily income o between P$11,600 and P$34,999; D+ = Monthly amily income o between P$6,800 and P$11,599; D = Monthly amily income o between P$2,700 and P$6,799.

2 4Q09 gure rom a national employment survey perormed by the INEGI.

Who are our clients?

We generate development opportunities in

lower-income segments o the population.

> Almost all our clients all into the C, D+, and D1

segments o the population.

> 98% o them are women.

Contributing to the social, economic, and human development o

lower-income segments o the population, which oten have scant

access to nancial services, we directly and proactively promote the

integral development o Mexico.According to the INEGI, the Mexican statistics bureau, there are

20 million people in Mexico who are in a position to get a working

capital loan to start their own business. Based on gures provided by

Consulta-Mitosky, a market research rm aliated with the Asocia-

ción Mexicana de Agencias de Investigación de Mercados (AMAI),

Mexico has a population o approximately 64.7 million in the C, D+,

and D socio-economic levels. Tese are the segments at which our

products are aimed.

It is estimated that the potential market o Compartamos Bancoconsists o 13.2 million people2 who have a business and/or are in a

position to start one. Compartamos Banco currently serves 11% o

this number.

Trough our credits we help microentrepreneurs who work in di-

erent sectors o the economy, reducing our dependence on economic

cycles and crises.

Crédito Mujer (Women Credit) 7.4% Crédito Adicional (Additional Credit)

8.2 % Crédito Mejora tu Casa (Home Improvement Credit)

39.8 % One or more additional Lie Insurance modules

Clients who have:

11%

89%

35%36%

7% 11% 11%

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 17/146

13

How do they Invest? In 2009, Compartamos Banco granted 4,493,981 loans, to be channeled into productive projects, in a

total amount o Ps. 32,659 million. As o the end o 2009, 74.0% o our portolio corresponded to theproduct called Crédito Mujer, loans to women who have their own business or are engaged in some

economic activity. Tis product continues recording one o the lowest non-perorming loan ratios o the

sector 0.87%.

We make a constant eort to oer our clients an ever wider range o nancial products and services,

which address not only the need or economic assistance in starting up or expanding a business, but

which also improve quality o lie and oster a culture o savings and orward planning.

Our work methodology takes into account aspects o consumer protection such as transparency, di-

verse channels o communication, policies to prevent excessive debt load, decent collection practices, and

ethical behavior on the part o our employees.

North Center West South

Aguascalientes Distrito Federal Baja Caliornia Campeche

Chihuahua Edo. de México Baja Caliornia Sur Chiapas

Coahuila Guanajuato Colima Guerrero

Durango Hidalgo Jalisco Oaxaca

Nuevo León Morelos Michoacán Quintana Roo

San Luis Potosí Puebla Nayarit abasco

amaulipas Querétaro Sinaloa Veracruz

- laxcala Sonora Yucatán

- Zacatecas - -

236,407 412,713 185,964 667,922

15.7% 27.5% 12.4% 44.4%

Clients by zone

2007 2008 2009 Var. 09/08

Disbursed loans 2,467,859 3,326,269 4,493,981 35.1%

Loan balance per client Ps. 4,991 Ps. 4,960 Ps. 5,086 2.5%

Non-perorming loan ratio 1.4% 1.7% 2.4% 41.1%

15.7%

27.5%

12.4%

44.4%

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 18/146

14

3 Compartamos Banco insured its clients in 2009 through Seguros Banamex.

Products and services

Crédito Mujer (Women Credit)Our principal product, this credit is granted to women individually and

with solidary guarantees, the groups are rom 12 to 50 women. It has a

term o 16 weeks.

Crédito Adicional (Additional Credit)

Tis additional credit is granted to Crédito Mujer clients who require ur-

ther nancing or their businesses. Te terms o this credit is rom 4 to

11 weeks.

Seguro de Vida3 (Lie Insurance)

Our Crédito Mujer clients may increase their lie insurance benets by

purchasing additional modules o Seguro de Vida. Each additional module

extends by 19 weeks the period during which the policy remains in eect.

Crédito Mejora tu Casa (Home Improvement Credit)Tis credit is granted to Crédito Mujer clients who require nancing or

home improvements. Te term o this credit is rom 6 to 24 months.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 19/146

15

or irresponsible advertising. Tanks to this practice, in 2009 we received no legal or adminis-

trative sanctions or ailure to comply with air and responsible marketing regulations.

Likewise, eager to know our clients’ opinion o the general perormance o Comparta-mos Banco, we make ourselves available through a call center that allows them to express

their complaints and opinions. Te number is toll-ree and complaints are attended to within

an average o 72 hours.

Crédito Comerciante (Merchant Credit)Tis group credit, granted with a solidary guarantee, is granted to

groups rom 5 to 8 entrepreneurs (men and/or women). Te term o

this credit is rom 4 to 5 months.

Crédito Crece tu Negocio (Grow your Business Credit)

Tis credit consists o major nancing, with a personal or collateral guar-

antee, or those wishing to make a major investment in their business, in

order to purchase merchandise or xed assets. Te term o this credit is

rom 4 to 24 months.

Seguro de Vida Integral (Integral Lie Insurance)

Tis is a lie insurance policy which Crédito Crece tu Negocio and Crédito

Comerciante clients may acquire voluntarily to meet the immediate ex-

penses o a death in the amily, a terminal illness, or a permanent in-

capacity, including: medical or uneral expenses, business maintenance,

maintenance o children, etc.

Crédito de Emergencia (Emergency Credit)Tis individual credit, with a personal guarantee and minimal interest rate, is

granted to active Compartamos Banco’s clients who have lost their businesses

because o a natural disaster. Te credit conditions are adapted to the needs

o our clients on a case-by-case basis.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 20/146

16

Since 3 years ago, we recognize the

commitment, eort and wor o ourclients through the “Compartamos BancoMicroentrepreneur Award.”

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 21/146

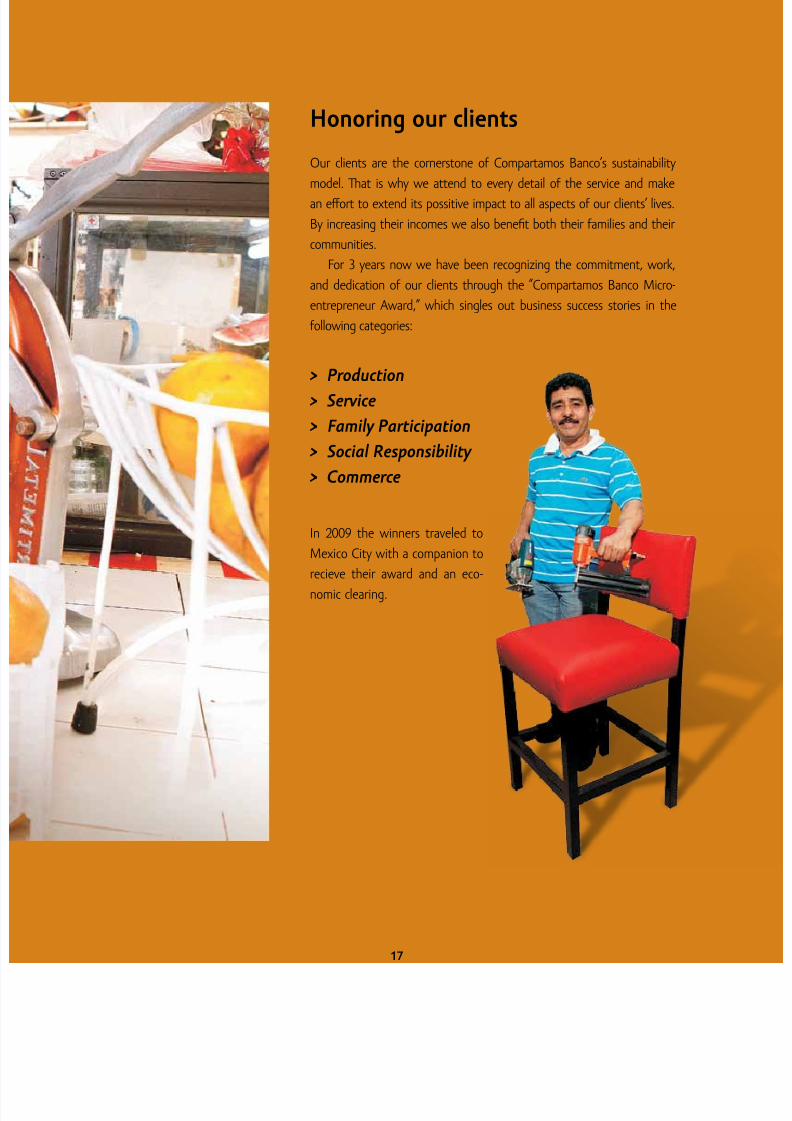

Honoring our clients

Our clients are the cornerstone o Compartamos Banco’s sustainability

model. Tat is why we attend to every detail o the service and make

an eort to extend its possitive impact to all aspects o our clients’ lives.

By increasing their incomes we also benet both their amilies and their

communities.

For 3 years now we have been recognizing the commitment, work,

and dedication o our clients through the “Compartamos Banco Micro-

entrepreneur Award,” which singles out business success stories in the

ollowing categories:

> Production

> Service

> Family Participation

> Social Responsibility

> Commerce

In 2009 the winners traveled to

Mexico City with a companion to

recieve their award and an eco-nomic clearing.

17

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 22/146

Compartamos Banco Microentrepreneur Award

Trough the “Compartamos Banco Microentrepreneur Award,” werecognize the eort o our clients in the categories o: Production,Service, Family Participation, Social Responsibility and Commerce.

Marlene obilla GarduzaCategory: ProductionState: abascoMain activity: Production o dierent kinds o traditional cheeses

“My husband learned how to make cheese and we began the business with just a tableand molds or the irst cheeses we made. he irst loans we received rom Comparta-mos Banco were invested in the purchase o raw materials; later we bought land or the cheese-making operation and all the equipment.

My plans include business training or mysel, training or my employees, opening

more stores, exporting, hiring more employees, taking my products to other sales points,purchasing machinery, and oering new products.

I would like to grow a little more. With God’s will, and i we keep working, I think we will.”

Víctor Casarrubias GarcíaCategory: ServiceState: Mexico City

Main activity: Swimming school, therapy, gymnasium, and multi-use hall.

“I learned to swim thanks to my uncle; I enrolled at the Olympic pool and began to take

courses that motivated me to become a swimming coach mysel.With my savings I ound a space and received help rom my amily and riends, until

I learned about Compartamos Banco I began with aquatic therapy or people with di-sabilities; now it is a swimming school, but we still give therapy.

My uture plans include opening a caeteria, training mysel and my employees, en-couraging their studies, and oering new services.

I love my business. I am proud o it and have made every eort to continue impro-ving, not only economically but also proessionally, in order to oer ever better service.”

18

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 23/146

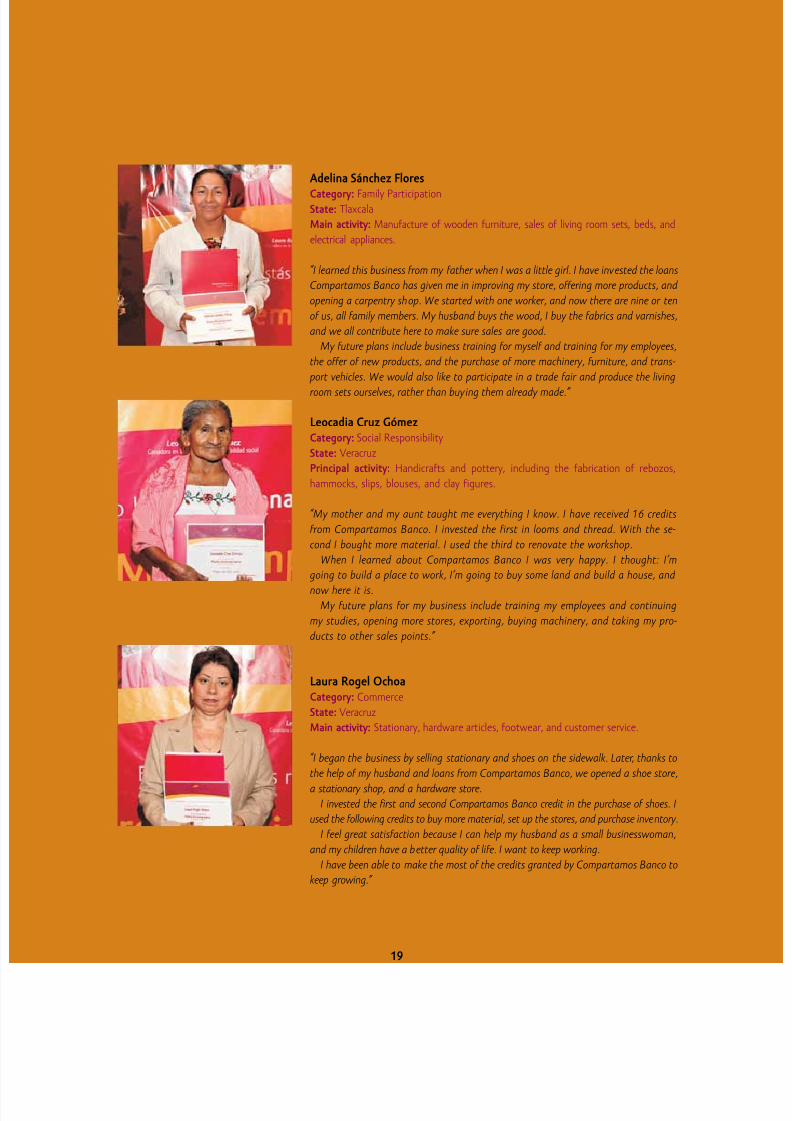

Adelina Sánchez Flores

Category: Family ParticipationState: laxcalaMain activity: Manuacture o wooden urniture, sales o living room sets, beds, and

electrical appliances.

“I learned this business rom my ather when I was a little girl. I have invested the loansCompartamos Banco has given me in improving my store, oering more products, and opening a carpentry shop. We started with one worker, and now there are nine or teno us, all amily members. My husband buys the wood, I buy the abrics and varnishes,and we all contribute here to make sure sales are good.

My uture plans include business training or mysel and training or my employees,the oer o new products, and the purchase o more machinery, urniture, and trans-port vehicles. We would also like to participate in a trade air and produce the living

room sets ourselves, rather than buying them already made.”

Leocadia Cruz GómezCategory: Social Responsibility

State: VeracruzPrincipal activity: Handicrats and pottery, including the abrication o rebozos,

hammocks, slips, blouses, and clay igures.

“My mother and my aunt taught me everything I know. I have received 16 creditsrom Compartamos Banco. I invested the irst in looms and thread. With the se-cond I bought more material. I used the third to renovate the workshop.

When I learned about Compartamos Banco I was very happy. I thought: I’m

going to build a place to work, I’m going to buy some land and build a house, and now here it is.My uture plans or my business include training my employees and continuing

my studies, opening more stores, exporting, buying machinery, and taking my pro-ducts to other sales points.”

Laura Rogel OchoaCategory: CommerceState: VeracruzMain activity: Stationary, hardware articles, ootwear, and customer service.

“I began the business by selling stationary and shoes on the sidewalk. Later, thanks to

the help o my husband and loans rom Compartamos Banco, we opened a shoe store,a stationary shop, and a hardware store.

I invested the irst and second Compartamos Banco credit in the purchase o shoes. Iused the ollowing credits to buy more material, set up the stores, and purchase inventory.

I eel great satisaction because I can help my husband as a small businesswoman,and my children have a better quality o lie. I want to keep working.

I have been able to make the most o the credits granted by Compartamos Banco tokeep growing.”

19

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 24/146

ECONWe have created a protable and strong

institution in which private capital mayparticipate, making the industry moreattractive or others to compete.

“Over 19 years, Compartamos Banco has distinguished itsel as a solidinstitution specialized in micronance.”

María Teresa ChaviraInvestor Relations

20

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 25/146

OMICVALUE

21

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 26/146

Te number o clients reached1,503,006, representing a growtho 30.0% over to 2008.

22

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 27/146

23

Our growth objectives, based on osteringthe development o micro-entrepreneurs

through nancing working capital,generated positive results in 2009.

> We granted 4,493,981 working capital loans.

> Our total loan portolio increased to Ps. 7,645million.

> We maintained excellent credit quality, with aNPL ratio o 2.4%.

> We issued - Ps. 1,500 million in long-term

debt, with a 3-year term.

> We ensured unding to nance growth in 2010.

> Net operating income in 2009 was Ps. 2,017 million, up by 40.1% over 2008.

We gained 347,156 new clients in 2009.

We opened 11 new oces, bringing the total to 325.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 28/146

Excellent potential market, a successulbusiness model, committed employees,and sucient resources to support operationsexplain our solid growth.

> Net income was Ps. 1,490 millions, repre-senting growth o 33.0%.

> EPS1 was Ps. 3.48, representing growth o 32.8%.

> Te perormance o our share was outstandingrepresenting a yield o 170.2% or the year, inMexican Pesos and in US dollars.

> In 2009, or the second year in a row,

Compartamos Banco’s Series “O” shares(COMPAR O) were listed on the Stock Market Index (IPC), the main benchmark stock index o the Mexican Stock Exchange.Tey were likewise ratied to be listed in 2010.

> Average client balance was Ps. 5,086.

> Te perormance o our shares was one o the5 best on the IPC.

We maintained our Standard & Poor’s and Fitch credit ratings o mx AA- y AA- (mex),respectively.

24

1Earnings per share, excluding shares repurchased.

We created 1,418 new jobs.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 29/146

25

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 30/146

26

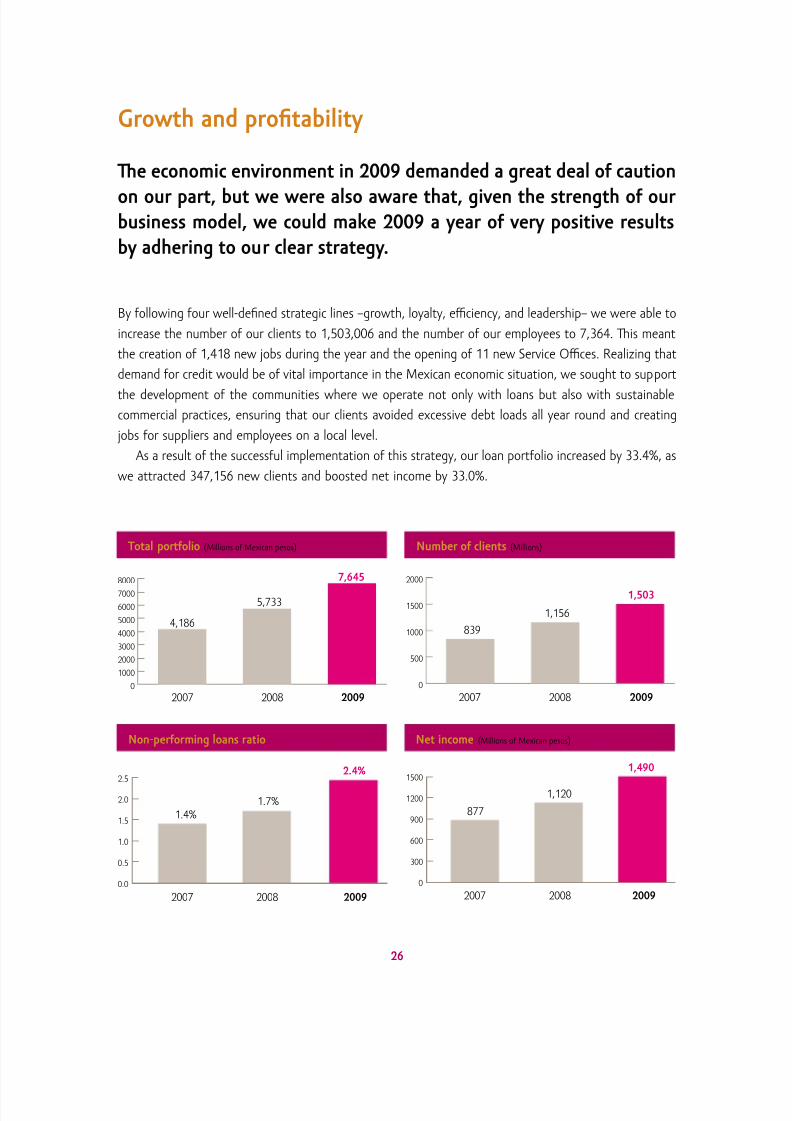

Growth and protability

Te economic environment in 2009 demanded a great deal o caution

on our part, but we were also aware that, given the strength o ourbusiness model, we could mae 2009 a year o very positive resultsby adhering to our clear strategy.

By ollowing our well-dened strategic lines –growth, loyalty, eciency, and leadership– we were able to

increase the number o our clients to 1,503,006 and the number o our employees to 7,364. Tis meant

the creation o 1,418 new jobs during the year and the opening o 11 new Service Oces. Realizing that

demand or credit would be o vital importance in the Mexican economic situation, we sought to support

the development o the communities where we operate not only with loans but also with sustainable

commercial practices, ensuring that our clients avoided excessive debt loads all year round and creating

jobs or suppliers and employees on a local level.

As a result o the successul implementation o this strategy, our loan portolio increased by 33.4%, as

we attracted 347,156 new clients and boosted net income by 33.0%.

otal portolio (Millions o Mexican pesos) Number o clients (Millions)

Non-perorming loans ratio Net income (Millions o Mexican pesos)

2007 2008 2009

4,186

5,733

7,645

0

1000

2000

3000

4000

5000

6000

7000

8000

2007 2008 2009

839

1,156

1,503

0

500

1000

1500

2000

0.0

0.5

1.0

1.5

2.0

2.5

2007 2008 2009

1.4%

1.7%

2.4%

2007 2008 2009

0

300

600

900

1200

1500

877

1,120

1,490

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 31/146

Eciency and unding

Eciency is a vital element in our strategy or creating a business model that is sustainable in the long term.

In 2009 we continued to work on the premise o bringing our products and services to the greatestnumber o people in the shortest possible time, and o oering incentives to our employees to save re-

sources. Tis translated into an eciency ratio2 o 25.8%.

At the same time, on a nancial level, in spite o the challenges o the local credit market, we were

able to ensure unding to support operations or the entire year. Tanks to our solid equity structure, we

had access to diverse sources o nancing and were the only micronance institution to participate in the

local debt market, issuing Ps. 1,500 millon in debt (Certicados Bursátiles Bancarios) with a 3-year term

at very avorable conditions. Tanks to this strategy o diversied unding, we have ensured the nancing

o our operations through 2010.

2Eciency Ratio = Operating Expenses / Operating Income * 100

27

GRI Economic Indicators Item 2007 2008 2009Millions o Mexican pesos

Direct economic value created 2,905 3,718 5,036

Distributed economic value 1,917 2,448 3,180

Retained economic value 988 1,270 1,856

Net Income 877 1,120 1,490

Item 2007 2008 2009

Number o clients 838,754 1,155,850 1,503,006

Net interest income (millions o Mexican pesos) 2,580 3,375 4,579

Operating eciency 29.3% 26.8% 25.8%

Net income (millions o Mexican pesos) 877 1,120 1,490

Net Interest income – Net income (millions o Mexican pesos)

Commercial DevelopmentEquity ban ban Multilateral L debt otal

Dec-08 36.69% 30.06% 29.02% 4.24% 0.00% 100.00%

Sep-09 43.12% 6.39% 28.25% 4.01% 18.23% 100.00%

Dec-09 45.84% 8.64% 24.37% 3.81% 17.33% 100.00%

4.24%

30.06%

29.02%

36.69% 43.12%45.84%

24.37%

8.64%3.81%

17.33%

28.25%

.39%

4.01%

Multilateral Comercial Bank

Dic-08

100

80

60

40

20

0Dic-09Sep-09

Development Bank Equity LT Debt

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 32/146

28

Notes on nancial statementsand stoc maret perormance

Tere was a sharp drop in economic activity in Mexico in 2009, with low investment, a steep decrease inormal employment, a generalized all in aggregate demand, and a consequent contraction o gross domestic

product. All o this was the result o the serious economic crisis in the countries with which Mexico maintains

its principal commercial relations, detonated by the collapse o important nancial institutions worldwide. Te

negative impact was also elt in the Mexican micronance sector.

In this dicult environment Compartamos Banco not only showed strong operating and nancial growth

but also improved its protability and eciency ratios. At the same time, it grew in terms o inrastructure and

number o clients, even as it maintained a non-perorming loans ratio that is below average in the Mexican

banking sector. All o this was possible thanks to the implementation o a proven business strategy, successul

in spite o the o dicult environment, the guiding elements o which are:

2009 was another record year or Compartamos Banco, as we accelerated growth and reined in costs,

thanks to our business model, the strength o our institution, and the ecient work o all those who

belong to it.In spite o the good results, we are watching closely the development o our market and the key

variables that will aect our perormance. One o these is unding, so in 2009 we ensured sucient

resources to support our operations by diversiying our sources o nancing. Tese ranged rom develop-

ment banks to commercial banks to the issue o Ps. 1,500 million in long-term debt, part o a program

which will allow the issue o an additional Ps. 4,500 million over the next 5 years.

Operating results

Net interest income

In 2009 net interest income ater provisions was Ps. 4,297 million, up 30.6% rom the Ps. 3,290 recorded in 2008.

Tis positive perormance refects an increase in interest income, which went rom Ps. 3,623 million in

2008 to Ps. 4,897 million in 2009, as the bank’s total loan portolio grew by 33.4%, derived rom 33.0%

growth in the number o clients.

Interest expenses in 2009 were Ps. 318 million, up by 28.2% rom the Ps. 248 million recorded in

2008, as available resources were increased to ensure unding and so maintain growth in a particularly

volatile environment.

Growth > Loyalty > Eciency > Leadership

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 33/146

29

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 34/146

Average cost o unding (interest expenses / average interest-bearing liabilities) dropped rom 8.5%

in 2008 to 7.0% in 2009, as a result o a generalized decrease in interest rates in the Mexican money

market.

In 2008 we changed the methodology or calculating loan-loss reserves in order to comply with the

National Banking and Securities Commission (CNBV) standards, so these provisions increased by Ps. 101million in 2009. Based on our policy to write-o loans that are 270 days past due, write-os in 2009 to-

taled Ps. 184 million, giving a write-o ratio (write-os / total loan portolio) o 2.4%, up rom the 1.6%

registered in 2008.

Te bank’s net interest margin (NIM = net interest income ater loan-loss reserves / average yielding

assets) in 2009 was 51.2%, up a notch rom the 51.1% recorded in 2008, in spite o higher leveraging,

the aorementioned increase in loan-loss reserves, a slight drop in active interest rates, derived rom a

pricing model which oers lower rates to clients with a good credit history.

Operating income

otal operating income in 2009 was Ps. 4,257 million, up by 31.1% rom the Ps. 3,247 million regis-

tered in 2008. Tis increase was due to strong growth in net interest income ater provisions and ee

income o Ps. 116 million, up by 63.4% over the previous year. Te latter increase was the result o

ees generated rom voluntary lie insurance products and ees charged to clients with past-due loans.

Tese revenues were oset, however, by Ps. 144 million in ee and commission expenses derived rom

third-party transactions.

Compartamos Banco has no exposure to oreign exchange risks or derivative instruments that might

aect operating results in the prevailing market volatility.

Operating resultsOperating income was Ps. 2,017 million in 2009, up by 40.0% rom the Ps. 1,440 million registered

in 2008. Operating expenses increased by 24.0%, rom Ps. 1,807 million in 2008 to Ps. 2,240 million

in 2009, owing mainly to an 3.5% increase in installed capacity, as 11 new oces brought the total

number to 325. Te number o employees increased by 1,418 to a total o 7,364. Nevertheless, in a

refection o the bank’s ever greater eciency and protability, the increase in operating expenses was

less than growth in client base, total loan portolio, and interest income.

Payroll accounted rom the greater part o operating expenses, representing 57.5% o the total.

Other important expenses were derived rom marketing and advertising, increasing by 3.7% to Ps.

94 million.

In line with new CNBV regulations, employee prot sharing, which amounted to Ps. 53 million

in 2009, is registered as an operating expense. Even when this is taken into account, the bank’s e-

ciency ratio dropped rom 54.8% in 2008 to 52.6% in 2009, demonstrating its strong operating

eciency. Excluding the eect o prot-sharing expenses, the eciency ratio improved considerably

rom 54.8% in 2008 to 51.4% in 2009.

30

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 35/146

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 36/146

32

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 37/146

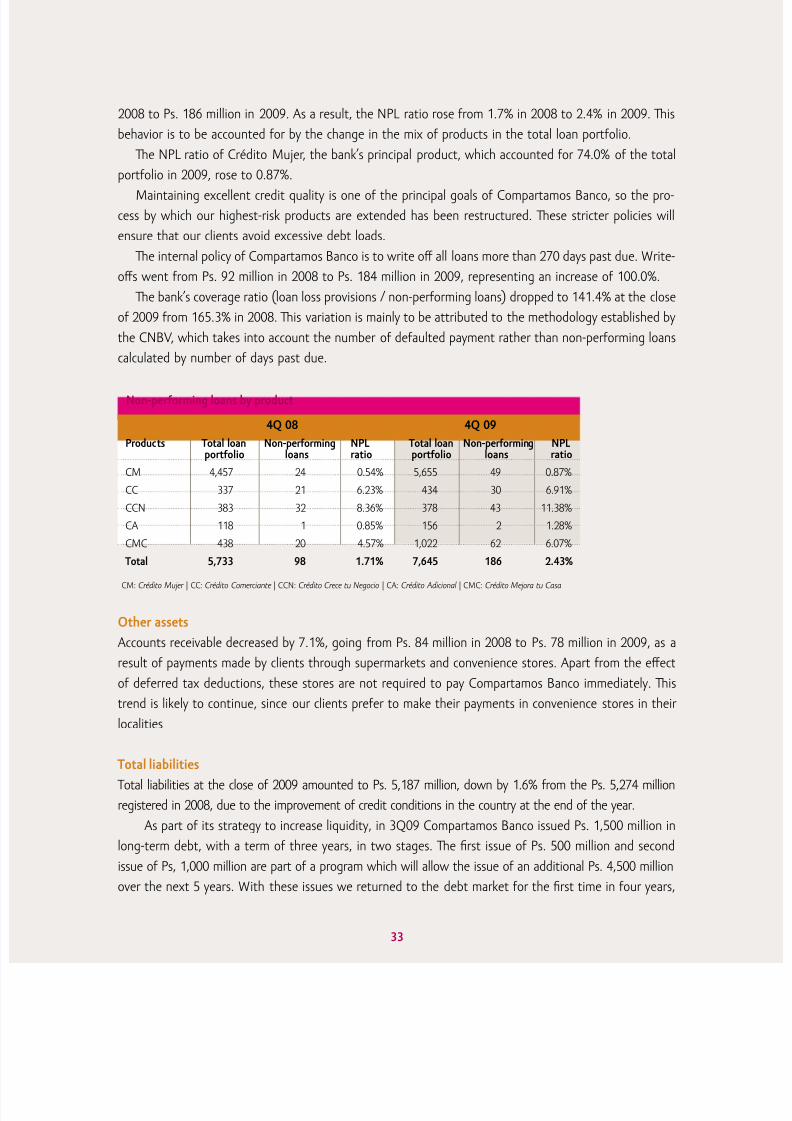

2008 to Ps. 186 million in 2009. As a result, the NPL ratio rose rom 1.7% in 2008 to 2.4% in 2009. Tis

behavior is to be accounted or by the change in the mix o products in the total loan portolio.

Te NPL ratio o Crédito Mujer, the bank’s principal product, which accounted or 74.0% o the total

portolio in 2009, rose to 0.87%.

Maintaining excellent credit quality is one o the principal goals o Compartamos Banco, so the pro-cess by which our highest-risk products are extended has been restructured. Tese stricter policies will

ensure that our clients avoid excessive debt loads.

Te internal policy o Compartamos Banco is to write o all loans more than 270 days past due. Write-

os went rom Ps. 92 million in 2008 to Ps. 184 million in 2009, representing an increase o 100.0%.

Te bank’s coverage ratio (loan loss provisions / non-perorming loans) dropped to 141.4% at the close

o 2009 rom 165.3% in 2008. Tis variation is mainly to be attributed to the methodology established by

the CNBV, which takes into account the number o deaulted payment rather than non-perorming loans

calculated by number o days past due.

Other assets

Accounts receivable decreased by 7.1%, going rom Ps. 84 million in 2008 to Ps. 78 million in 2009, as a

result o payments made by clients through supermarkets and convenience stores. Apart rom the eect

o deerred tax deductions, these stores are not required to pay Compartamos Banco immediately. Tis

trend is likely to continue, since our clients preer to make their payments in convenience stores in their

localities

otal liabilities

otal liabilities at the close o 2009 amounted to Ps. 5,187 million, down by 1.6% rom the Ps. 5,274 million

registered in 2008, due to the improvement o credit conditions in the country at the end o the year.

As part o its strategy to increase liquidity, in 3Q09 Compartamos Banco issued Ps. 1,500 million in

long-term debt, with a term o three years, in two stages. Te rst issue o Ps. 500 million and second

issue o Ps, 1,000 million are part o a program which will allow the issue o an additional Ps. 4,500 million

over the next 5 years. With these issues we returned to the debt market or the rst time in our years,

33

Non-perorming loans by product

4Q 08 4Q 09Products otal loan Non-perorming NPL otal loan Non-perorming NPL

portolio loans ratio portolio loans ratio

CM 4,457 24 0.54% 5,655 49 0.87%

CC 337 21 6.23% 434 30 6.91%

CCN 383 32 8.36% 378 43 11.38%

CA 118 1 0.85% 156 2 1.28%

CMC 438 20 4.57% 1,022 62 6.07%

otal 5,733 98 1.71% 7,645 186 2.43%

CM: Crédito Mujer | CC: Crédito Comerciante | CCN: Crédito Crece tu Negocio | CA: Crédito Adicional | CMC: Crédito Mejora tu Casa

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 38/146

34

diversiying our sources o unding, reducing the concentration o debt with commercial banks, and

increasing the term o our debt.

Compartamos Banco’s sources o unding consist o:

1. A solid capital base: 43.9% o total assets were unded with equity in 2009, compared to 35.1%

in 2008. Te bank’s ROAE in 2009 was 43.1%.2. Short-term bank obligations: the advantage o having a banking license is the ability to issue

deposit certicates on the local market. At the close o 2009 Compartamos Banco had issued Ps.

300 million in short-term bank obligations.

3. Long-term debt: the issue o Ps. 1,500 million in long-term debt is part o a program which allows

the issue o an additional Ps. 4,500 million over the next 5 years.

4. Lines o credit with banks and other institutions: Compartamos Banco has credit lines with several

commercial banks and development banks, as well as other nancial institutions.

Compartamos Banco’s liabilities are entirely denominated in pesos, reeing it rom exposure to

oreign exchange fuctuations.

otal shareholders’ equity

otal shareholders’ equity at the close o 2009 was Ps. 4,061 million, an increase o Ps. 1,205 million, or

42.2%, over the Ps. 2,856 million recorded at the close o 2008. Te ratio o equity to assets was 43.9%.

Compartamos Banco’s solid capital base has three main objectives:

1. o maintain a solid base;

2. o reduce nancing costs;

3. o ensure unding or continued growth.

In 2009, a total o 185,400 shares were repurchased, in the amount o Ps. 4.12 million representing

0.59% o the approved amount o Ps. 700 million.

Ratios and perormance indicators

ROAE/ROAA

Return on average equity (ROAE) at the close o 2009 was 43.1%, compared to 43.6% at the close o

2008. Te 33.0% increase in net income partly accounts or this rise. Return on average assets (ROAA)

was 17.1% in 2009, compared to 16.9% in 2008.

Eciency

Te eciency ratio (operating expenses / net operating income) at the close o 2009 was 52.6%, down

rom 55.7% in 2008. Tis ratio alls within the bank’s expectations, in spite o the increase in operating

expenses derived rom the new regulation that requires employee prot sharing to be registered as an

operating expense. Tis amount o Ps. 53 million was ormerly reported under Other Expenses. Excluding

this eect, the bank’s eciency ratio would stand at 51.4%.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 39/146

Stoc maret perormance

In 2009 Compartamos Banco showed an excellent recovery on the stock markets due mainly to strong

operating results, in combination with good expectations or growth in 2010. Te perormance o the

bank’s shares was one o the ve best on the IPC, yielding 170.2% or shareholders during the year.

Tanks to this recovery, the bank’s shares went rom 35th to 26th place in the listing o most tradedshares, an encouraging indicator that refects the excellent results o Compartamos Banco.

35

Stoc maret perormance 2008 2009 Var. %

Prices (Mexican pesos) 24.59 58.99 139.92

Value (millions o Mexican pesos) 5,584.69 7,957.82 42.49

Volume (millions o Mexican pesos) 161 208 29.19

Number o transactions 32,800 74,075 125.84

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 40/146

HUM

36

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 41/146

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 42/146

At Compartamos Banco we know that theeconomic development o our clients must go

hand by hand with their integral development.We believe in people, in their honesty and capacity or transormation.

> We created 1,418 new positions.

> A 24% increase in the size o our sta.

> 100% o our employees certied in our Ethicsand Conduct Code.

Our employees numbered 7,364 at the end o 2009.

873 courses aimed at the development o our employees.

38

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 43/146

105 business worshops and289 committee meetings or our clients.

39

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 44/146

40

Te programs developed in 2009 were:

Business workshops

In 2009 we held 105 business workshops (two workshops per week),

devoted to subjects such as nancial education, business administra-

tion, and values. Clearly and directly, with examples rom everyday

lie, we seek to clariy our clients’ doubts and uncertainties. Various

credit and savings products are also presented in these workshops.

Committee meetings1

In 2009 we also held 288 committee meetings, attended by CréditoMujer clients, at which subjects such as sel-esteem and nancial edu-

cation were dealt with. Tis represents more than 5 committee meetings

per week, clearly demonstrating the interest o our clients and the

decided commitment o Compartamos Banco to their development.

Te magazine “Avancemos hacia el éxito”

Tis publication, distributed ree to the majority o our clients, oers

valuable content that is accessible and easily readable. Trough this

way we share success stories and articles on nancial education,

105 business workshops.

289 committee meetings.

Development or our clients

At Compartamos Banco we know that the economic development o our clients must go hand in hand

with personal development on other levels. Tis is the only way to achieve integral wellbeing. Te person

is the beginning and end o Compartamos Banco, which is why we oer opportunities to complement

our clients’ growth as persons. In 2009 more than 93,000 clients were benetted by business workshops

and committee meetings. In addition to the benets reaped by our clients, these activities strengthened

three undamental aspects o our strategy: leadership, loyalty, and growth.

As part o our eorts to support and develop our clients, we have implemented workshops and com-

mittee meetings, and we have published a magazine “Avancemos hacia el éxito” and disseminate our

values. Tis important work is perormed by highly trained personnel with wide experience in the eld. In

2009 we distributed 2,604,600 among our clients.

About 84% o the clients who attendedbusiness workshops in 2009 renewedtheir loan.1In Crédito Mujer, committees are ormed by the president, the secretary and the treasurer o the group, chosen by the integrants.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 45/146

amily, and values, as well as recipes and other subjects o general

interest. Tis eort is inspired by our philosophy o ostering the

integral development o our clients, employees, and the communities

where we operate.

Our eorts to maintain close links with our clients by means o

active communication through various activities and events, as well

as successul advertising campaigns, have produced positive results.

Compartamos Banco’s positioning as a brand in the “MicronanceBanking” segment went rom 32% in 2008 to 70% in 20092 and

shows, part o the achievement.

Children’s drawing contest

In July 2009 we held the rst children’s drawing contest or the ami-

lies o our employees, called “Compartamos Banco and My Family.”

More than 600 drawings were submitted and 10 winners were chosen

rom dierent parts o the country. Tey traveled to Mexico City

accompanied by relatives to receive their awards and enjoyed a day

o un at a amous amusement park.

Breakast or Champions

It is very important or Compartamos Banco to oer our clients

additional benets in appreciation o their preerence and trust. In

November 2009, 150 clients were invited to participate, with a com-

panion, in an exclusive event with the Mexican soccer teams Chivas

o Guadalajara, Rayados o Monterrey and Cruz Azul. Participants at-

tended a team practice and then an autograph session at the teams

acility. Te lucky ones were selected rom among 1,900 stories, re-counting how, through their own eorts and a Compartamos Banco

credit, they have set up a business in the league o champions.

2,604,600 copies o the “Avancemos hacia el éxito“ magazine.

10 winning drawings.

About 86% o the clients who attendedcommittee meetings in 2009 renewed

their loan.

150 clients participate with the Ch ivas o Guadalajara, Rayados o Monterrey and Cruz Azul soccer teams.

41

2 Source: Brand racking 2009

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 46/146

In 2009 we created

1,418 new positions.

42

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 47/146

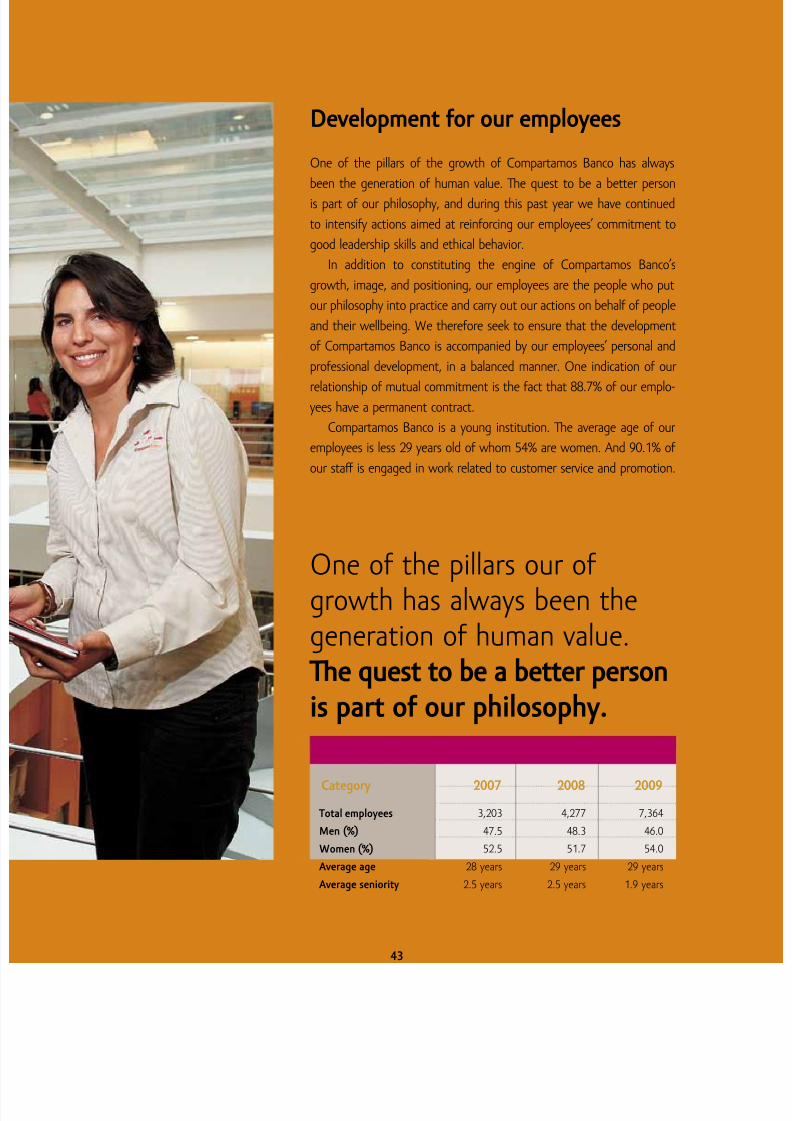

Development or our employees

One o the pillars o the growth o Compartamos Banco has always

been the generation o human value. Te quest to be a better person

is part o our philosophy, and during this past year we have continued

to intensiy actions aimed at reinorcing our employees’ commitment to

good leadership skills and ethical behavior.

In addition to constituting the engine o Compartamos Banco’s

growth, image, and positioning, our employees are the people who put

our philosophy into practice and carry out our actions on behal o people

and their wellbeing. We thereore seek to ensure that the development

o Compartamos Banco is accompanied by our employees’ personal and

proessional development, in a balanced manner. One indication o our

relationship o mutual commitment is the act that 88.7% o our emplo-yees have a permanent contract.

Compartamos Banco is a young institution. Te average age o our

employees is less 29 years old o whom 54% are women. And 90.1% o

our sta is engaged in work related to customer service and promotion.

otal employees 3,203 4,277 7,364

Men (%) 47.5 48.3 46.0

Women (%) 52.5 51.7 54.0

Average age 28 years 29 years 29 years

Average seniority 2.5 years 2.5 years 1.9 years

Category 2007 2008 2009

One o the pillars our ogrowth has always been thegeneration o human value.Te quest to be a better personis part o our philosophy.

43

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 48/146

44

Ocers 15 0.2 17 0.2

Sub ocers 28 0.5 32 0.4

Managers 64 1.1 81 1.1

Administrative 382 6.4 445 6.1

otal main oce personnel 489 8.2 575 7.8

Managers 315 5.3 325 4.4

Sub managers 2 0.0 57 0.8

Administrative assistants 336 5.5 502 6.8

Systems administrators 325 5.6 335 4.5

Consultants 615 10.3 559 7.6

Loan ocers coordinators 125 2.1 129 1.8

Crédito Mujer coordinators 574 9.7 676 9.2

Loan ocers 2,751 46.3 3,565 48.4

Specialized loan ocers 285 4.8 485 6.6

otal sales personnel 5,328 89.6 6,633 90.1

Regional managers 34 0.6 43 0.6

Recruiting and selection coordinators 8 0.1 7 0.1

Regional recruiters 34 0.6 38 0.5

Lawyers/Regional intermediaries 53 0.9 68 0.9

otal regional personnel 129 2.2 156 2.1

otal Compartamos personnel 5,946 100 7,364 100

Employees with a collective contract 5,336 89.7 6,533 88.7

Personnel by position Number Percentage Number Percentage2008 2008 2009 2009

Leader Formation Program

One o the most important events in the personal eld and thereore refected in improving workplace,

was the creation o the leadership department. In keeping with our philosophy, strategy goals and de-

centralized labor scheme, this area ocuses primarily on the design and delivery o programs to develop

leadership, both personal and proessional o employees.

Pyxis is the leadership brand o Compartamos Banco, at the same time encompasses our Comparta-

mos Banco leadership program. Developed 100% at home, by people who know the operation, business

strategy and micronance in the world, so we can meet the needs in the areas o personal developmentand transormation o our employees.

As a rst practice, the Leadership raining Program was provided to 116 ocers and managers at head-

quarters “Seas”3 , our target group are those people with high impact and infuence inside and outside

Compartamos Banco, subsequently the leadership culture move to other levels.

One important actor in achieving a healthy work environment is the design o selection processes

suited not only to the needs o the position but also in empathy with the values and mystique o

3 SeaS means service to branches and it is Compartamos Banco headquarters.

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 49/146

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 50/146

46

“Jengibre” Seeks to monitor and increase awareness among middle management 35.9% turnover

in order to hold on to the best employees, drawing up a specic plan ocused

on areas o opportunity or reducing turnover.

Human ormation Aimed at ostering the personal development o employees through 1,580 sessions given

workshops on subjects such as responsibility, teamwork, loyalty.

INNOVA Encourages employees to propose initiatives that contribute to improving 2 initiatives

project processes, working methods, and new products.

Balanced Flexible Fridays, physical conditioning through the use o our gymnasium 345 employees

lie practices and psychological support through the Employee Attention Program (PAC). served by PAC

Perormance Evaluation takes into account the achievement o goals in accord with 100% o the

evaluation institutional objectives. employees evaluatedPromotion Selects employees with high potential and ollows up their perormance with 1,142 promotions

planning a view to considering them or promotion. 3,344 ascents

Career acceleration Promotes employees’ proessional development through scholarships or 125 scholarships

ull nancing. granted

Compensation Competitive salaries, with greater benets than required by Mexican -

labor legislation, as well as monthly incentives and perormance bonuses.

Employee Employees with more than one year’s seniority can purchase shares o 99 employees

share-purchasing Compartamos Banco in any amount ranging rom Ps. 2,500 to the equivalent

o hal a month’s participated salary (every six months). Tis program seeks

to give access to the stock market to those who work day by day

in achieving the objectives o Compartamos Banco.

Family Day Te employees had the opportunity to share with their amilies the pride o Participation central oce:

working in Compartamos Banco. (Headquarters and Services Oces). 153 employees, 132 guests,

At the headquarters two conereces were held to refect and give practical advice and 117 children. 317

to built healthy and long lasting relationships at work and amily. Service Ocers participated.

Ethical criteria Workshop adapts to dierent positions, lawyer, recruiters, leader, moderators, etc. 378 participants

worshops Te main purpose: the way to work, discovering attitudes according to

Compartamos Philosophy that help them in their daily administration,

become aware o their work as a coordinators; to make daily decisions

having as a guide the Ethics and Conduct Code.

Círculo Peces o motivate the volunteer participation o our employees, we created 742 volunteers

“Círculo Peces”, integrated by dierent programs such as human ormation

program, induction, volunteers, nancial education and reporters.

Círculo Peces is a employees’ club agents o change that guide, encourage

and promote the Sense o purpose and Mystic to their co-workers

and community.

Personal developmentProgram Description Results

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 51/146

In 2009 we continued with major programs

ocused on the development o sillsamong our employees, within work place,personal and ethical.

47

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 52/146

Permanent training is one o the most

signicant aspects o Compartamos Bancoand a actor that explains its solid growth.

48

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 53/146

raining

raining is consistent with our principles and is an indispensable ele-

ment in achieving our goals, which involve the continual development

o people and o the Institution.

Tis is why we have invested Ps. 23 million in the proessional de-

velopment o our employees, using the most up-to-date online tools,

such as e-learning, virtual classrooms, and video tutorials, as well as

conventional courses and eld work.

Depending on our particular training needs, we use various me-

thodologies –both our own and those o others– in a process o

continual improvement. We have training centers at our main oces

and at other points around Mexico, where we strike alliances with

suppliers, ensuring wider coverage and lower costs.Te Compartamos Banco training program includes a large num-

ber o areas and specializations: induction into the company and

its products, sales workshops, systems practices, administrative skills,

administration processes, management procedures, etc. Tese help to

give our employees both the technical competence and the rame o

mind necessary to carrying out the tasks entrusted to them.

We use dierent methodologies,both third party and own, in a processo continuous improvement.

More than Ps.23 million invested in training.

We have training center in dierent cities o the country.

InductionAll new employees receive an induction course. Its aim is or new employees to understand and adopt the

organizational culture o Compartamos Banco, to master the basic skills with which to perorm their work,

and to learn what is expected o them.

Tis induction course constitutes their rst encounter with the Compartamos Philosophy, which they will

experience in their daily activities through their ellow workers and the way the organization conducts itsel.

49

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 54/146

Ethics and Conduct Code

Since its ounding, Compartamos Banco has worked rom a clear ethical vision, whereby social, economic,

and human value are generated. Tat is why it is o vital importance or all o our employees, and especially

new ones, to be certied in our Ethics and Conduct Code. Tis translates into a commitment to live by our

philosophy and our standards o conduct. All o our employees rearm their ethical commitment annually.

> 3,493 new employees certied in the Ethics and Conduct Code.

> 100% o the employees recertied annually in the Ethics and Conduct Code.

> 140 complaints attended.

Our Ethics and Conduct Code is a guide to dening our objectives, determining the strategies and ac-

tions required to achieving them, and to decision-making in general. Our vigorous Code does not shy

away rom any aspect o ethical conduct in situations such as confict o interest, inormation handling,

interpersonal relations, human rights, corruption, harassment, use o assets and services, custody o the

Compartamos brand, and work environment.

Ethical conduct brings great benets to Compartamos Banco, to the communities where we operate,

and to our other key publics, by ostering trust, improving work environments, encouraging mutuallybenecial relations, and reinorcing loyalty and good understanding. It is essential to have the means to

detect, prevent, and remedy actions contrary to our Ethics and Conduct Code, so our employees have ree

and entirely condential channels through which to submit complaints, including email, a toll-ree number,

and prepaid mail service. Our Honor Commission is responsible or ollowing up the complaints, listening

to the parties involved, ruling on the case, and imposing penalties i necessary.

Te annual review and continuous circulation o our Ethics and Conduct Code is vital to Compartamos

Banco, and is supervised by top management and the Honor Commission.

Since its ounding, Compartamos Banco hasworked rom a clear ethical vision in order togenerate social, economic and human value.

50

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 55/146

Wor environment

An excellent work environment is the result o who we are and what we do. Since its beginnings, Com-

partamos Banco has ocused on people, seeking to provide a air, participative, respectul, sae, stimula-

ting, and human work environment. Tis is the rst step in ensuring that our employees eel motivated,

satised, and happy to work in a company with policies, programs, and activities ocused on improving

the quality o their working lives rom a balanced and integral perspective.

Integration with employees is intensive, involving a monthly meeting in every work center (a total

o 12 integration meetings per year), as well as participation by all employees in annual encounters to

reinorce the Compartamos Philosophy, ollow up on objectives and strategies, recognize outstanding

perormance, and promote communication and general integration.

In order to keep abreast o the work environment, surveys are conducted among all employees to

gather perceptions and suggestions, which are then translated into actions that solve problems or imple-

ment improvements. Te results o the last survey were very positive, showing a clear trend toward

Annual meetings are organized to reinorcethe Compartamos Philosophy and 100%o the employees participate.

51

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 56/146

52

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 57/146

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 58/146

Financial Education

For Compartamos Banco it is essential that the public in general andour clients in particular have access to better nancial education, sothat they are able to mae the best decisions and tae uller advantageo dierent nancial services, yielding benets both or themselves andtheir communities. Financial education is thereore an important parto our social responsibility.

Financial education has become a vital issue in various sectors o Mexico. In recentyears national and international conerences and congresses have been organized

to discuss the strategies that need to be implemented in this area, especially in the

context o the economic situation we are going through.

For Compartamos Banco this is nothing new. Our business model, based on per-

sonal and direct contact with our clients, has allowed us to:

> Foster a culture o savings and orward planning through

our services.

> Promote an awareness o how much debt can saely beassumed, in order to avoid excessive debt load.

> Ofer useul inormation to those wishing to comparedierent nancial products and services.

In 2009, our nancial education activities were designedto go beyond our business model, developing channels o communication adapted to our dierent publics, such asthe entrepreneur worshop, videos, audios and fyers.

54

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 59/146

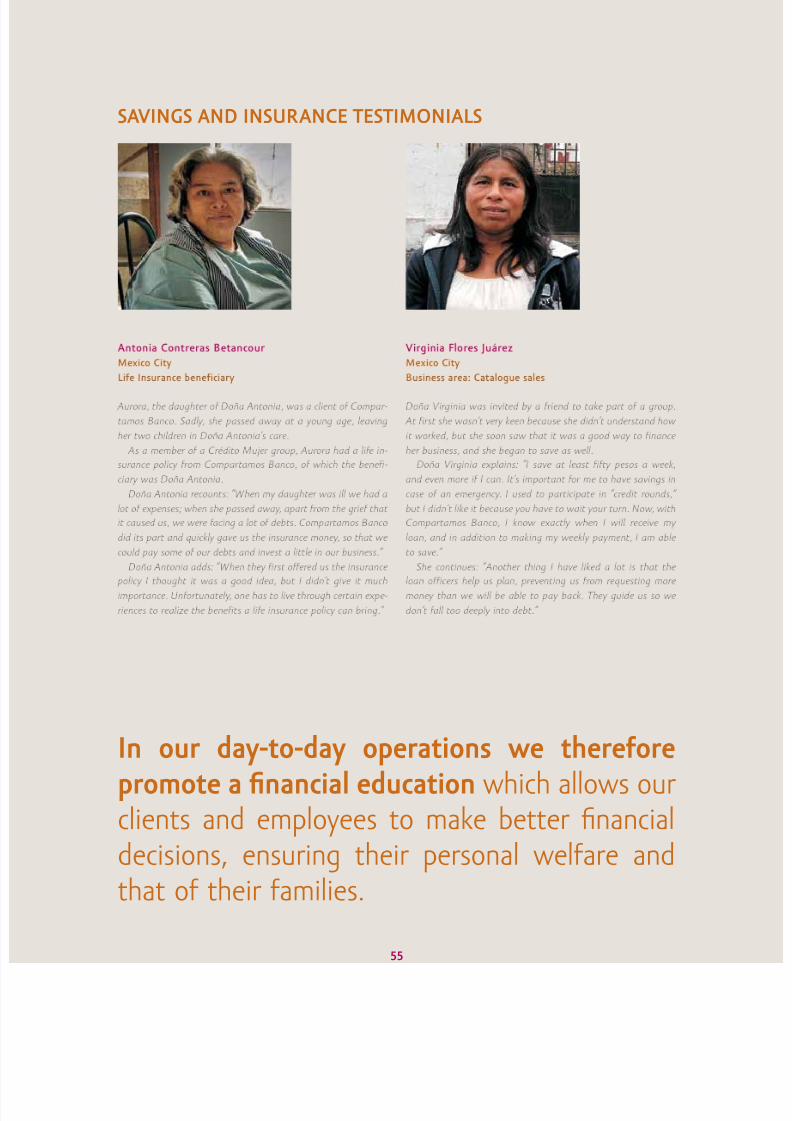

SAVINGS AND INSURANCE ESIMONIALS

In our day-to-day operations we thereorepromote a nancial education which allows ourclients and employees to make better nancialdecisions, ensuring their personal welare andthat o their amilies.

55

8/7/2019 RSE - Reporte de Sustentabilidad de Compartamos Banco

http://slidepdf.com/reader/full/rse-reporte-de-sustentabilidad-de-compartamos-banco 60/146

EMPLOYEES

> We train all o our employees through an e-learning Micronance

Course.

> We deal with issues such as excessive indebtedness, saving, budgeting, and credit in our magazine Compartips and through Regional Encounters.

> We have prepared a Financial Education section in our Intranet that

deals with subjects such as nancial administration, indebtedness,

savings calculations, and trivia.

José Antonio Varela FigueroaOice manager, Compostela Service Oice

“It was exciting to hear what the clients said; they were grateul or the attention and patience, since many o them were not very good with numbers. he most important thing is what they carry within: a positivemental attitude to accomplish what they propose, the care o their loan, the care rom Compartamos Banco,and the conidence in themselves.”

EMPLOYEE INSRUCORS OF HE ENREPRENEUR WORkSHOPS ESIMONIALS

helma Sarahí Lazcano RodríguezAdministrative assistant, Zacatelco Service Oice

“Most o the people who took the course were Compartamos Banco employees. At irst it was discouragingnot to have people rom outside, but when I saw my ellow workers’ interest I became enthusiastic, because