SITUACIÓN Y FUTURO DE LOS CÍTRICOS EN EL MERCADO...

50

SITUACIÓN Y FUTURO DE LOS CÍTRICOS EN EL MERCADO EUROPEO ABRIL 2019

Transcript of SITUACIÓN Y FUTURO DE LOS CÍTRICOS EN EL MERCADO...

SITUACIÓN Y FUTURO DE LOS CÍTRICOS EN EL MERCADO EUROPEO

A B R I L 2 0 1 9

F U N D A D O E N 1 9 3 1 M U R C I A , E S PA Ñ A

E M P R E S A FA M I L I A R D E 3 ª G E N E R A C I Ó N

5 0 PA Í S E S 1 , 3 0 0 M € FA C T U R A C I Ó N A N U A L

I N T E G R A C I Ó N E 2 E C O M P L E TA

A M P L I O P O R TA F O L I O C O N G R A N E X P E R I E N C I A E N C Í T R I C O S Y U VA D E M E S A

I M P U L S A D O P O R L A I N N O VA C I Ó N Y L A T E C N O L O G Í A

ÍNDICE:

- I M P O R TA N C I A D E L M E R C A D O E U R O P E O PA R A P E R Ú

- P R E S E N T E Y F U T U R O D E L C O N S U M O D E C Í T R I C O S E N E U R O PA

- T E N D E N C I A S D E L C O N S U M I D O R

- P E R S P E C T I VA D E L O S R E TA I L E R S E U R O P E O S

IMPORTANCIA DEL MERCADO EUROPEO PARA PERÚ

30,06734,819

46,180

64,172

46,738

68,202

78,083

89,24693,301

113,427115,122

127,788

166,615

188,275

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

TOTAL EXPORTACIÓN (TM) vs AÑO

E VO LU C I Ó N D E L A S E X P O RTA C I O N ES D E C Í T R I CO S D ES D E P E R Ú

280 4457,834 14,415 3,785

7,538 9,893 7,464 9,453 8,504 6,314 10,377 16,685

18,79618,745

21,652 21,397

28,80323,095

36,42539,652

47,06652,288

71,32175,127

91,121

113,651

132,316

10,49812,150

15,822 19,75318,204

21,82925,671

31,65127,937

29,205

25,45920,877

23,924 19,397

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

CÍTRICOS (TM) vs AÑO

Naranja Mandarina Tangelo Clementina Toronjas L. Sutil L. Tahiti

D ES G LO S E P O R C AT EG O R Í A D E L A S E X P O RTA C I O N ES P E R UA N A S

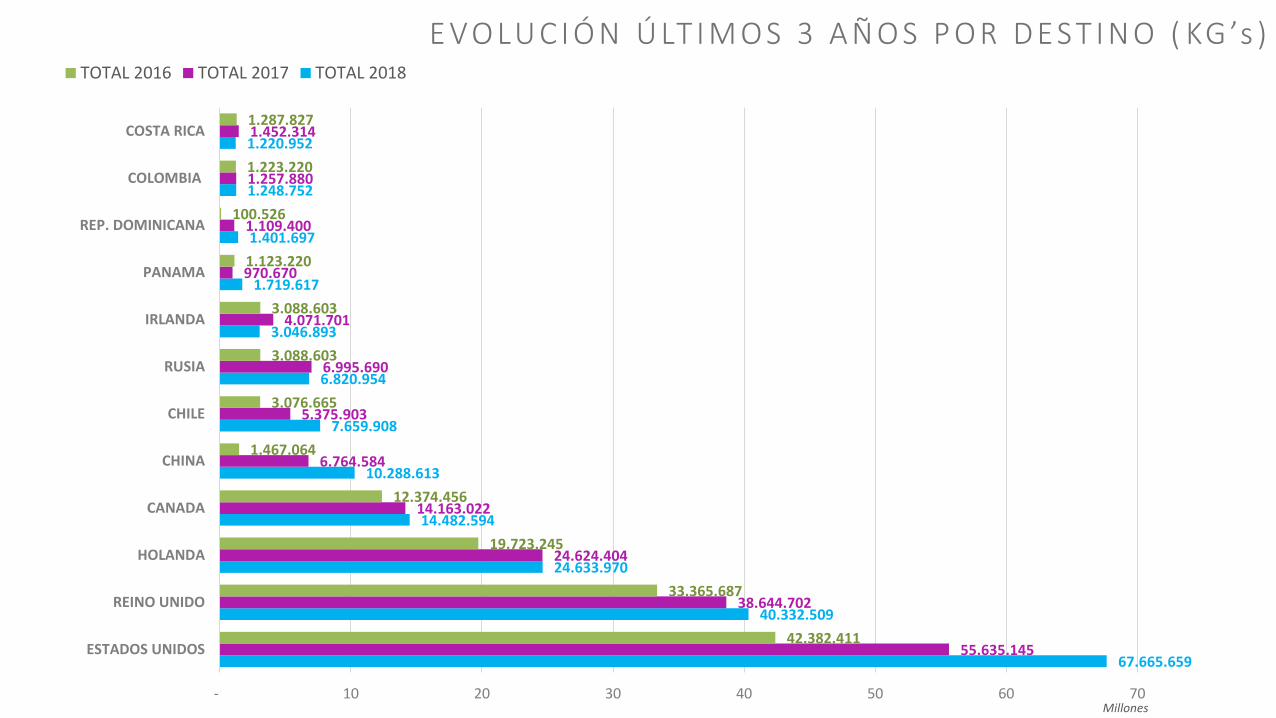

67.665.659

40.332.509

24.633.970

14.482.594

10.288.613

7.659.908

6.820.954

3.046.893

1.719.617

1.401.697

1.248.752

1.220.952

- 5 10 15 20 25 30 35 40 45 50 55 60 65 70

ESTADOS UNIDOS

REINO UNIDO

HOLANDA

CANADA

CHINA

CHILE

RUSIA

IRLANDA

PANAMA

REP. DOMINICANA

COLOMBIA

COSTA RICA

Millones Kg’s

TOTALES 2018

D ES G LO S E P O R PA Í S D E L A S E X P O RTA C I O N ES P E R UA N A S

-

5

10

15

20

25

30

35

40

45

50

M. Tempranas Clementina M. Tardías Tangelos Naranjas Toronjas L. Sutil L. Tahiti Limon

PAÍS POR ESPECIE 2018 (Kg)

ESTADOS UNIDOS REINO UNIDO HOLANDA CANADA CHINA CHILE RUSIA IRLANDAMillones (kg)

D ES G LO S E P O R ES P EC I E Y PA Í S D E L A S E X P O RTA C I O N ES P E R UA N A S

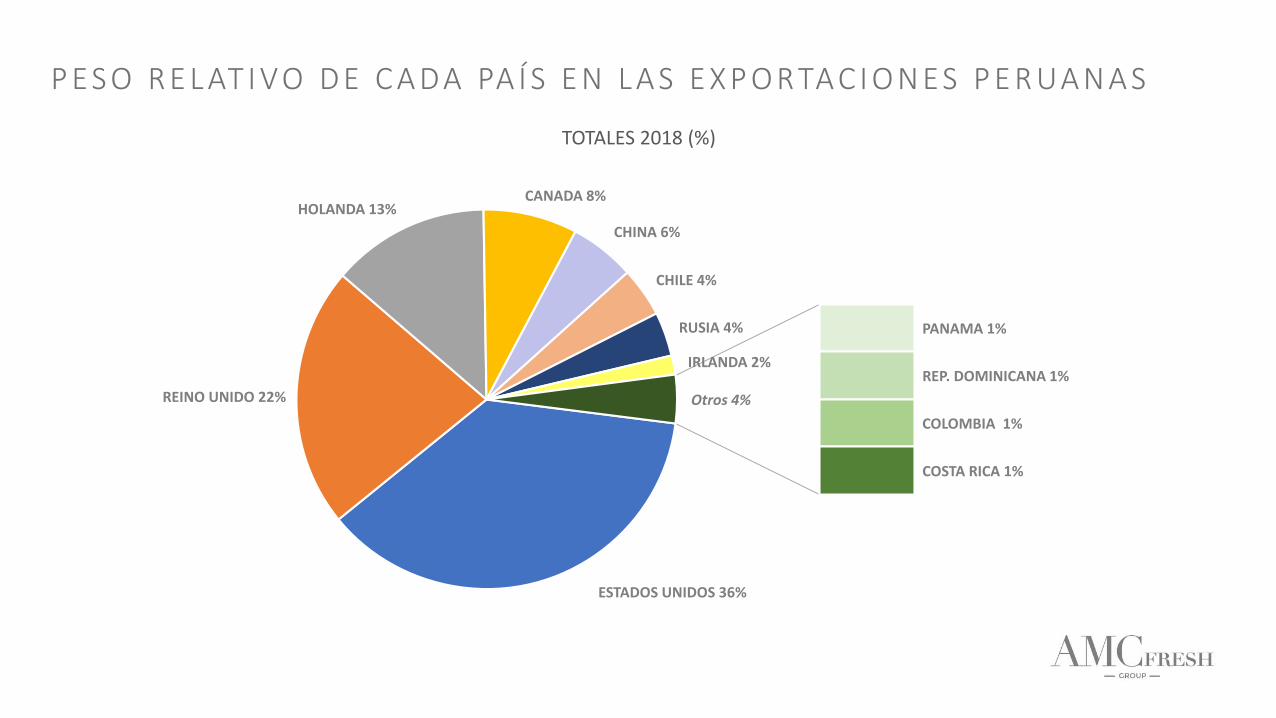

ESTADOS UNIDOS 36%

REINO UNIDO 22%

HOLANDA 13%CANADA 8%

CHINA 6%

CHILE 4%

RUSIA 4%

IRLANDA 2%

PANAMA 1%

REP. DOMINICANA 1%

COLOMBIA 1%

COSTA RICA 1%

Otros 4%

TOTALES 2018 (%)

P ES O R E L AT I VO D E C A DA PA Í S E N L A S E X P O RTA C I O N ES P E R UA N A S

67.665.659

40.332.509

24.633.970

14.482.594

10.288.613

7.659.908

6.820.954

3.046.893

1.719.617

1.401.697

1.248.752

1.220.952

55.635.145

38.644.702

24.624.404

14.163.022

6.764.584

5.375.903

6.995.690

4.071.701

970.670

1.109.400

1.257.880

1.452.314

42.382.411

33.365.687

19.723.245

12.374.456

1.467.064

3.076.665

3.088.603

3.088.603

1.123.220

100.526

1.223.220

1.287.827

- 10 20 30 40 50 60 70

ESTADOS UNIDOS

REINO UNIDO

HOLANDA

CANADA

CHINA

CHILE

RUSIA

IRLANDA

PANAMA

REP. DOMINICANA

COLOMBIA

COSTA RICA

Millones

TOTAL 2016 TOTAL 2017 TOTAL 2018

E VO LU C I Ó N Ú LT I M O S 3 A Ñ O S P O R D EST I N O ( KG ’s )

Millones (kg)

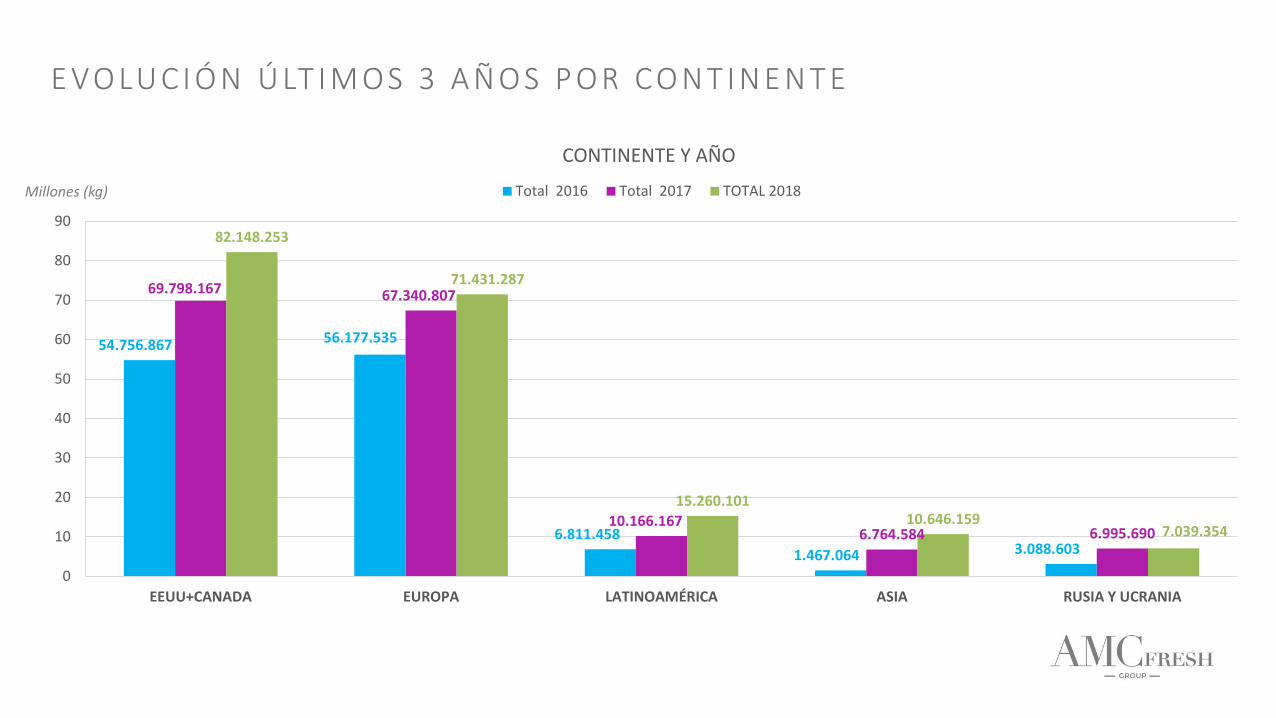

54.756.867 56.177.535

6.811.458

1.467.064 3.088.603

69.798.167 67.340.807

10.166.1676.764.584 6.995.690

82.148.253

71.431.287

15.260.10110.646.159

7.039.354

0

10

20

30

40

50

60

70

80

90

EEUU+CANADA EUROPA LATINOAMÉRICA ASIA RUSIA Y UCRANIA

CONTINENTE Y AÑO

Total 2016 Total 2017 TOTAL 2018

E VO LU C I Ó N Ú LT I M O S 3 A Ñ O S P O R CO N T I N E N T E

PRESENTE Y FUTURO DEL CONSUMO DE CÍTRICOS EN EUROPA

C R EC E N L A S I M P O RTAC I O N ES E U RO P EA S D E F R U TA S Y V E R D U R A S

11,4 MILLONES TM

+2,6% CAGR 2013-2018

E L CO N S U M O D E C Í T R I CO S E N E U RO PA A S C E N D I Ó A 1 1 , 4 M I L LO N ES T M E N 2 0 1 8

Source: USDA. Unión Europea-28

11,4

1,9

10,1

43,7

0,2

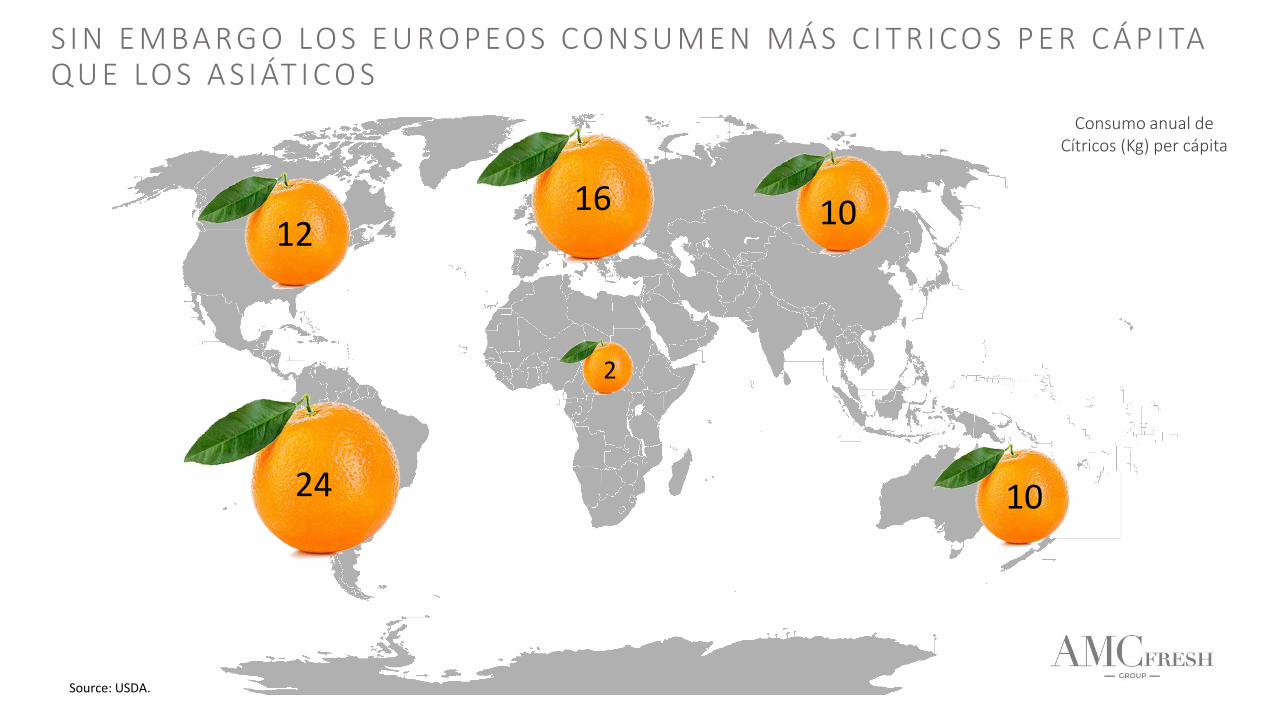

A S I A ES E L CO N T I N E N T E M Á S G R A N D E E N CO N S U M O D E C Í T R I CO S

Source: USDA.

4,2

MILLONES TM POR REGIÓN

S I N E M BA RG O LO S E U RO P EO S CO N S U M E N M Á S C I T R I CO S P E R C Á P I TA Q U E LO S A S I ÁT I CO S

Source: USDA.

Consumo anual de Cítricos (Kg) per cápita

12

2

24

10

10

16

+2,6% +3,2%

AMBOS CONTINENTES CRECEN A UN RITMO S IMILAR

CAGR 2013 -2018Consumo de Cítricos

Source: USDA.

+2,2%

¿QUÉ CATEGORÍA CONCENTRA MÁS VENTAS EN EUROPA?

51%EUROPA ADORA

LAS NARANJAS

29%

16% 4%

NARANJAS MANDARINAS

LIMONES / LIMA POMELO

Source: USDA. Unión Europea-28

% Consumo anual (volumen) de cítricos en Europa

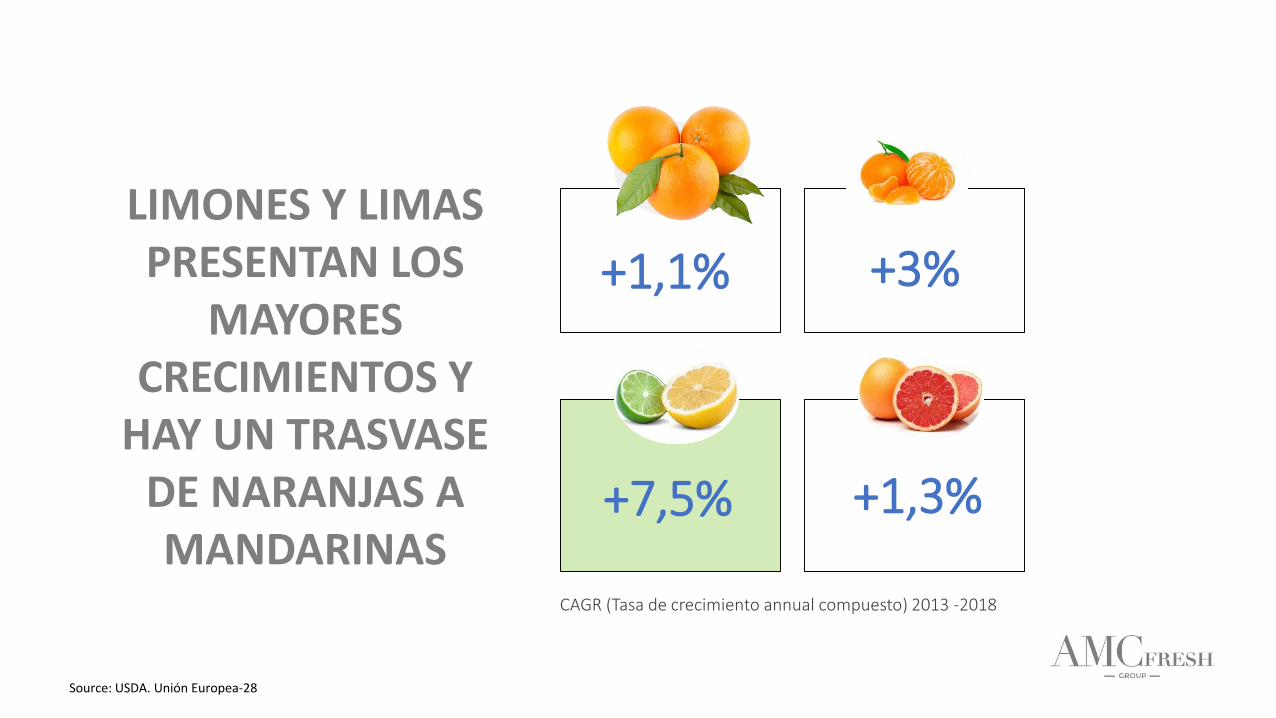

+1,1%

LIMONES Y LIMAS PRESENTAN LOS

MAYORES CRECIMIENTOS Y

HAY UN TRASVASE DE NARANJAS A MANDARINAS

+3%

+7,5% +1,3%

CAGR (Tasa de crecimiento annual compuesto) 2013 -2018

Source: USDA. Unión Europea-28

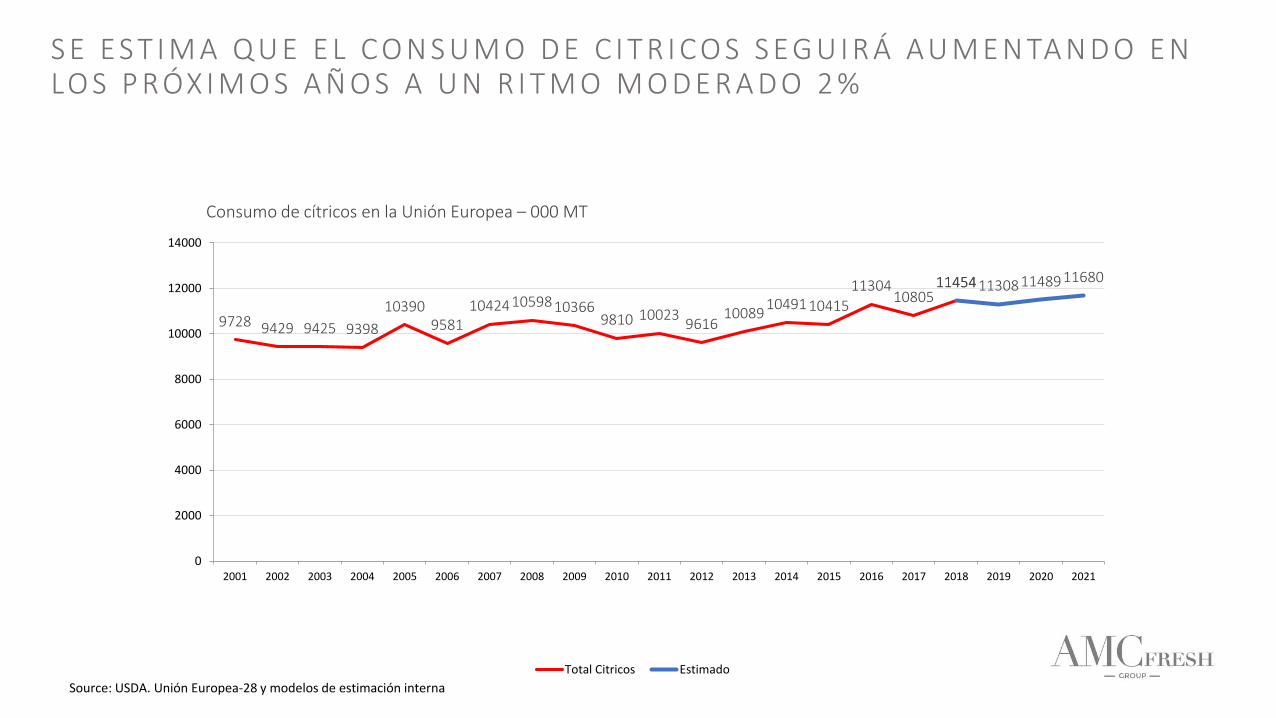

EVOLUCIÓN DE LAS CATEGORÍAS EN LA ÚLT IMA DÉCADA

Consumo de cítricos en la Unión Europea – 000 MT

Source: USDA. Unión Europea-28

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

European Union 9.581 10.424 10.598 10.366 9.810 10.023 9.616 10.089 10.491 10.415 11.304 10.805 11.454

Naranjas 5.060 5.772 5.869 5.717 5.324 5.536 5.382 5.549 5.333 5.407 5.950 5.735 5.874

Mandarinas 2.724 2.753 2.930 2.812 2.720 2.711 2.493 2.848 3.206 2.988 3.265 2.892 3.306

Limones / Limas 1.359 1.404 1.364 1.395 1.386 1.377 1.333 1.275 1.537 1.582 1.691 1.733 1.829

Pomelos 438 495 435 442 380 399 408 417 415 438 398 445 445

El consumo de limones y limas ha aumentado un 34% desde el 2008 y han pasado de suponer un 13% del consumo de cítricos hace 10 años a un 16% en la actualidad.

El consumo de mandarinas ha aumentado un 13% desde el 2008 y han pasado de suponer un 27% del consumo de cítricos hace 10 años a un 29% en la actualidad.

El consumo de naranjas es el más importante y se ha mantenido estable, pero ha perdido cuota frente a otras categorías (del 55% al 51% del consumo de cítricos).

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

EL CONSUMO DE L IMONES Y L IMA SE HA ACELERADO EN LOS ÚLT IMOS 5 AÑOS EN EUROPA

Consumo de cítricos en la Unión Europea – 000 MT y % variación vs año anterior

Source: USDA. Unión Europea-28

El crecimiento de su uso como ingrediente en “Fresh food” (mermeladas, bollería, dulces, ensaladas) y el auge del Gin&Tonic, agua con limón y otros cocktails ha aumentado su consumo en los últimos años

0

1000

2000

3000

4000

5000

6000

7000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

0

500

1000

1500

2000

2500

3000

3500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

+21% +3%+7% +2% +6%

+14%

9728 9429 9425 9398

103909581

1042410598103669810 10023

961610089

1049110415

1130410805

1145411454113081148911680

0

2000

4000

6000

8000

10000

12000

14000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Total Citricos Estimado

S E E S T I M A Q U E E L C O N S U M O D E C I T R I C O S S E G U I R Á AU M E N TA N D O E N LO S P RÓX I M O S A Ñ O S A U N R I T M O M O D E R A D O 2 %

Source: USDA. Unión Europea-28 y modelos de estimación interna

Consumo de cítricos en la Unión Europea – 000 MT

PERSPECTIVASA FUTURO POR

CATEGORÍA El consumo de naranjas frescasse mantiene estable y pierdecuota en favor de mandarinas

para uso “On the Go”

Source: USDA, MAPA, BMEL, FAS y análisis interno

Se prevee un aumento del consumo en línea con el auge de

la producción

Su tendencia positiva continuaráen los próximos años.

El consumo actual per cápita es 3 kg en la Unión Europea.

El consumo de pomelos permanecerá estable en los

próximos años, siendo la categoría de menor consumo

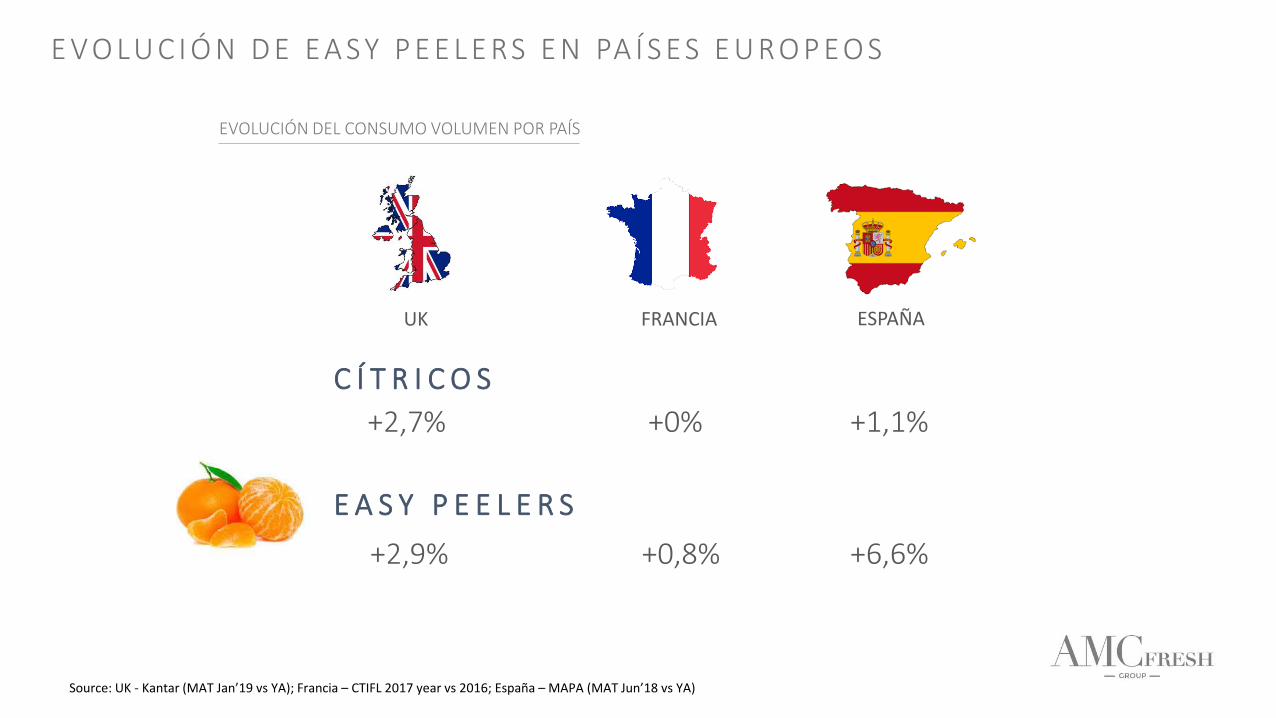

E V O LU C I Ó N D E E A S Y P E E L E RS E N PA Í S E S E U RO P EO S

C Í T R I C O S

+2,7%

E A S Y P E E L E R S

+2,9%

Source: UK - Kantar (MAT Jan’19 vs YA); Francia – CTIFL 2017 year vs 2016; España – MAPA (MAT Jun’18 vs YA)

EVOLUCIÓN DEL CONSUMO VOLUMEN POR PAÍS

+0%

+0,8%

UK FRANCIA

+1,1%

+6,6%

ESPAÑA

UK- CONSUMO DE CITRICOS (Millones kg)

LO S E U RO P EO S S O N D I F E R E N T E S E N E L C O N S U M O.

Mientras que el mercado inglés consume cítricos todo el año, en otros países del sur la demanda en verano es baja debido a la competencia de las frutas de temporada.

En España se sustituye el consumo de mandarinas por melón y sandía durante el verano.

Source: Kantar Panel para UK ( de Oct 2017 a Sep 2018) y Datos del MAPA para España (de Abr 2017 a Marzo 2018)

227

469

29

320

Mandarinas

Naranjas

H.Norte (Oct-Mar) H.Sur (Abr-Sep)

ESPAÑA- CONSUMO DE CITRICOS (Millones kg)

56

8

59

10

Limón

Pomelo

ESPAÑA- CONSUMO DE CITRICOS (Miles kg)

139

47

96

45

Mandarinas /Satsumas

Naranjas

H.Norte (Oct-Mar) H.Sur (Abr-Sep)

30

12

30

13

Limón /Lima

Pomelo

UK - CONSUMO DE CITRICOS (Miles kg)

TENDENCIAS DEL CONSUMIDOR

TO P 5 – T E N D E N C I A S D E L C O N S U M I D O R

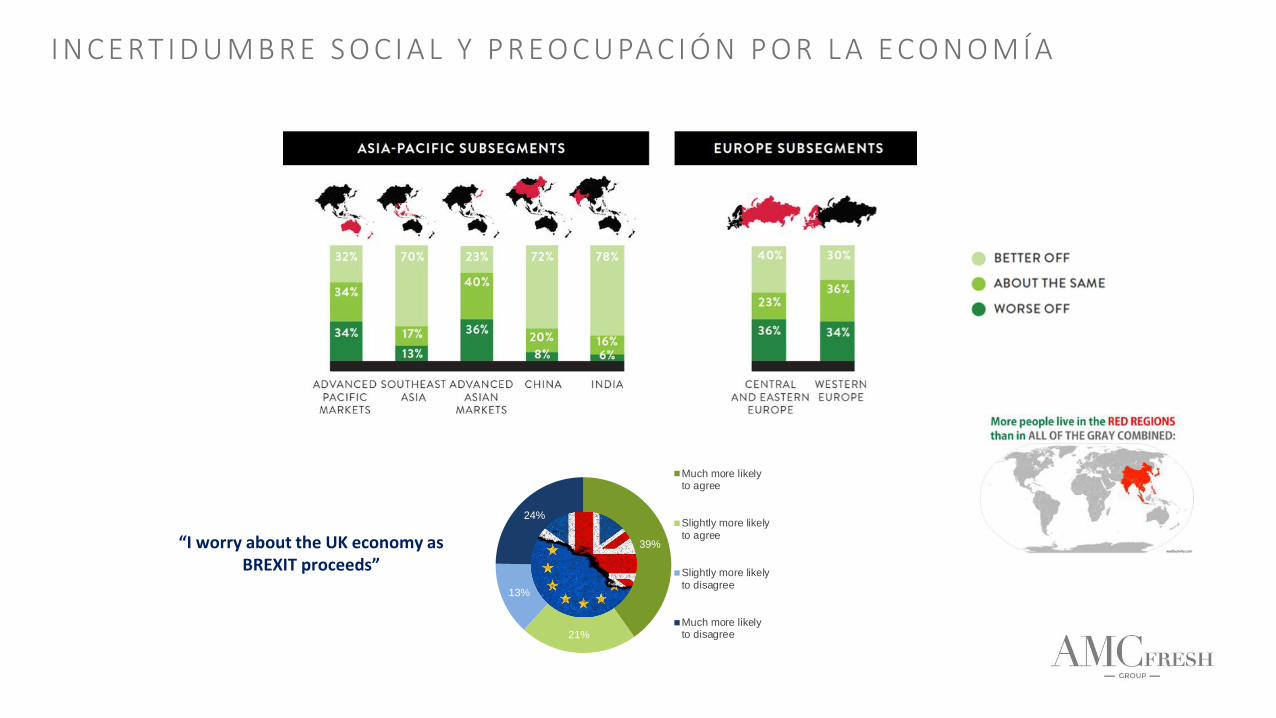

39%

21%

13%

24%

Much more likelyto agree

Slightly more likelyto agree

Slightly more likelyto disagree

Much more likelyto disagree

“I worry about the UK economy as BREXIT proceeds”

I N C E RT I D U M B R E S O C I A L Y P R EO C U PA C I Ó N P O R L A E C O N O M Í A

ETIQUETAS – FREE FROM

Los consumidores buscan etiquetas claras y quitar todos aquellosingredientes innecesarios (Conservantes, colorantes…)

Hay un auge de las categorías Free-From: las categorías sin lactosa y sin gluten crecen por encima del total mercado

TRANSPARENCIA

El origen de los productos, su trazabilidad y la historia que hay detrás de ellos se ha convertido en un factor importante en las decisiones de compra

PLANT- BASED

El número de productos plant-based ha aumentado su presencia en losRetailers, provocado por el aumento de la preocupación por la salud

PURO Y NATURAL

Los consumidores buscan productos naturales y puros, cada vez más. Estaes la principal motivación por la que compran producto orgánico o ecológico, que a su vez se asocial con un producto más sano y sabroso.

ON THE GO

Sin tiempo para nada, todos aquellosproductos que nos ahorren tiempo y ademásestén ligados al concepto salud evolucionanfavorablemente (Fruta cortada, berries….)

EXPERIENCIAS ÚNICAS

Los consumidores buscan productosdiferenciados que les permitan vivir experienciasúnicas. Y están dispuestos a pagar por ello un precio más alto.

M Á X I M O I N T E R É S E N C O N S U M I R P RO D U C TO S S A LU DA B L E S

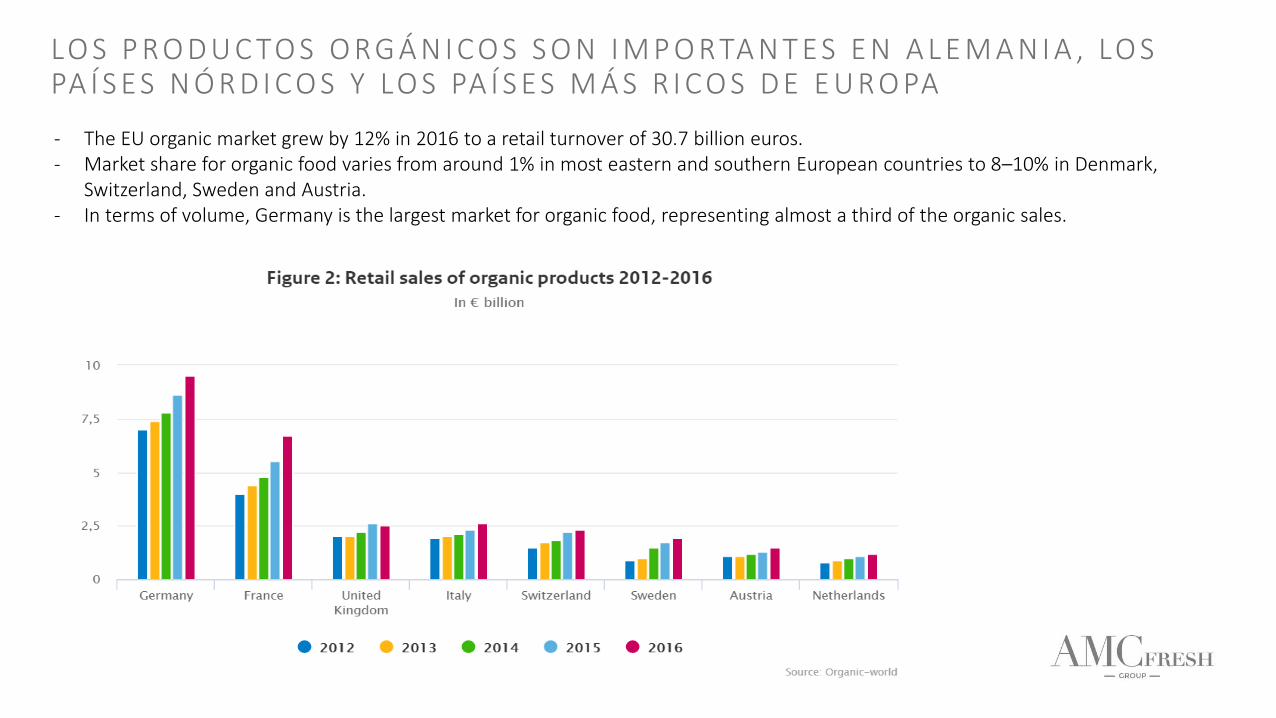

LO S P RO D U C TO S O RG Á N I C O S S O N I M P O RTA N T E S E N A L E M A N I A , LO S PA Í S E S N Ó R D I C O S Y LO S PA Í S E S M Á S R I C O S D E E U RO PA

- The EU organic market grew by 12% in 2016 to a retail turnover of 30.7 billion euros.- Market share for organic food varies from around 1% in most eastern and southern European countries to 8–10% in Denmark,

Switzerland, Sweden and Austria. - In terms of volume, Germany is the largest market for organic food, representing almost a third of the organic sales.

© IGD 2018 Page 32Source: ShopperVista, Feb’18-Apr’18. Base: 1,193 British supermarket and hypermarket shoppers

64%

47%

38%36%

26%

17%

57%

37% 36%

29%

44%

10%

It was more convenient It has a good choice ofproducts

It was quicker and easier It has good quality products It helps me to save money It is more enjoyable to shop

RAZONES PARA LA ELECCIÓN DE TIENDA

Supermarkets and hypermarkets All grocery stores

R E D E F I N I C I Ó N D E L VA LO R

P R EO C U PA C I Ó N C R E C I E N T E P O R LO S O C I A L Y E L M E D I O A M B I E N T E

61% 59%50% 47% 45% 43%

30% 28% 26%

% consumers who have ever purchased these products / services on line

No puedo comprobar frescura No puedo ver la calidad No puedo tocar el producto, olerlo…

Off line

4,9%

On line

18,4%

Global forecast growth CAGR (2017-2022)

1. Nielsen- the quest for convenience report 2018; Future opportunities in FMCG Ecommerce 2018

S I E M P R E C O N E C TA D O S , AU G E D E L C O M E RC I O O N L I N E P E RO …

PERSPECTIVA DE LOS RETAILERS EUROPEOS

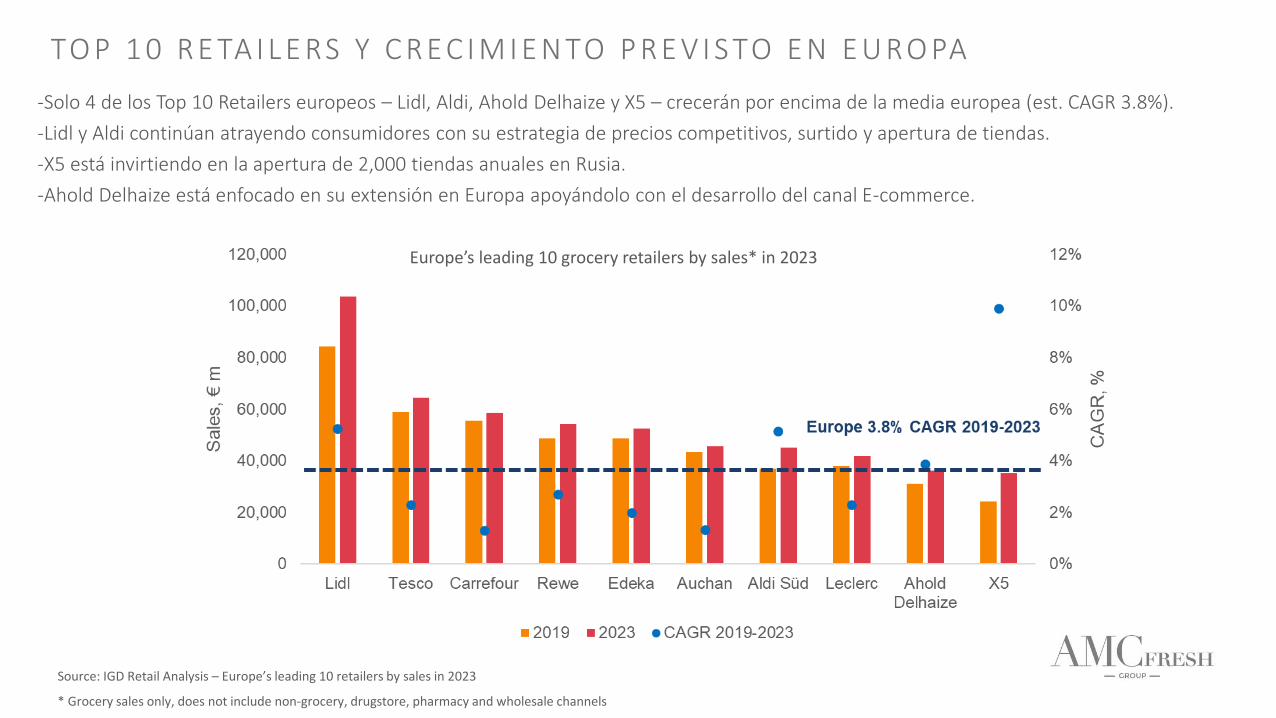

TO P 1 0 R E TA I L E RS Y C R E C I M I E N TO P R E V I S TO E N E U RO PA

Source: IGD Retail Analysis – Europe’s leading 10 retailers by sales in 2023

* Grocery sales only, does not include non-grocery, drugstore, pharmacy and wholesale channels

-Solo 4 de los Top 10 Retailers europeos – Lidl, Aldi, Ahold Delhaize y X5 – crecerán por encima de la media europea (est. CAGR 3.8%).

-Lidl y Aldi continúan atrayendo consumidores con su estrategia de precios competitivos, surtido y apertura de tiendas.

-X5 está invirtiendo en la apertura de 2,000 tiendas anuales en Rusia.

-Ahold Delhaize está enfocado en su extensión en Europa apoyándolo con el desarrollo del canal E-commerce.

Europe’s leading 10 grocery retailers by sales* in 2023

C U OTA D E M E RC A D O D E LO S P R I N C I PA L E S R E TA I L E RS E U RO P EO S

27,8%25,5%

20,2%

21%15,2%

18,1% 17,5%

15,2%

16,2%

24,3%

El Retailer #1 en cada país supera el 20% de cuota de mercado en valor en FMCG.

Cada país es liderado por un retailer diferente.

Source: Kantar, IRI, GKF. 2018 Year value sales, except for Germany 2017

Tesco launches more value brands and drives lower prices

Sainsbury’s makes £150m investment in price

¿ C Ó M O R E S P O N D E N L A S C A D E N A S A L A S T E N D E N C I A S ?

P R E O C U PA C I Ó N P O R L A E C O N O M Í A – P R E C I O S B A J O S …

¿ C Ó M O R E S P O N D E N L A S C A D E N A S A L A S T E N D E N C I A S ?

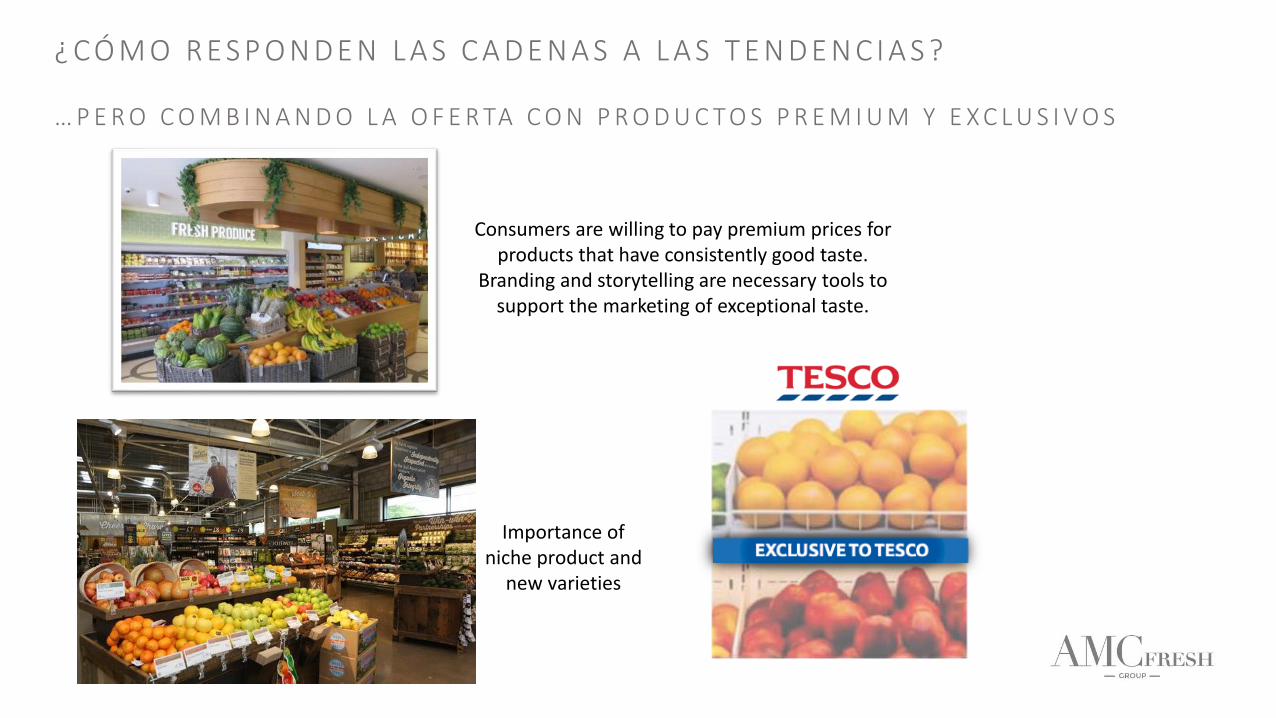

… P E R O C O M B I N A N D O L A O F E R TA C O N P R O D U C T O S P R E M I U M Y E X C L U S I V O S

Consumers are willing to pay premium prices for products that have consistently good taste.

Branding and storytelling are necessary tools to support the marketing of exceptional taste.

Importance of niche product and

new varieties

Nuevas misionesde compra

Influencers y sponsorship

Fomentaralimentossaludables

Conectar con losniños

¿ C Ó M O R E S P O N D E N L A S C A D E N A S A L A S T E N D E N C I A S ?

S A L U D Y B I E N E S TA R

Conectar con los niños

Los retailers europeos fomentan hábitossaludables en los niños. Un númerocreciente de retailers en Europa ofrecenfruta gratis a los niños en las tiendas.Tesco, Morrison, M&S en UK; Lidl enBélgica y Holanda; Albert Heijn’s enAlemania….

Tesco lanzó ‘Free fruit for kids’ en Julio 2016 y actualmentetienen activa la campaña enmás de 800 tiendas

Albert Heijn’s en Bélgica y Alemania

Lidl en Bélgica y HolandaKroger en USA

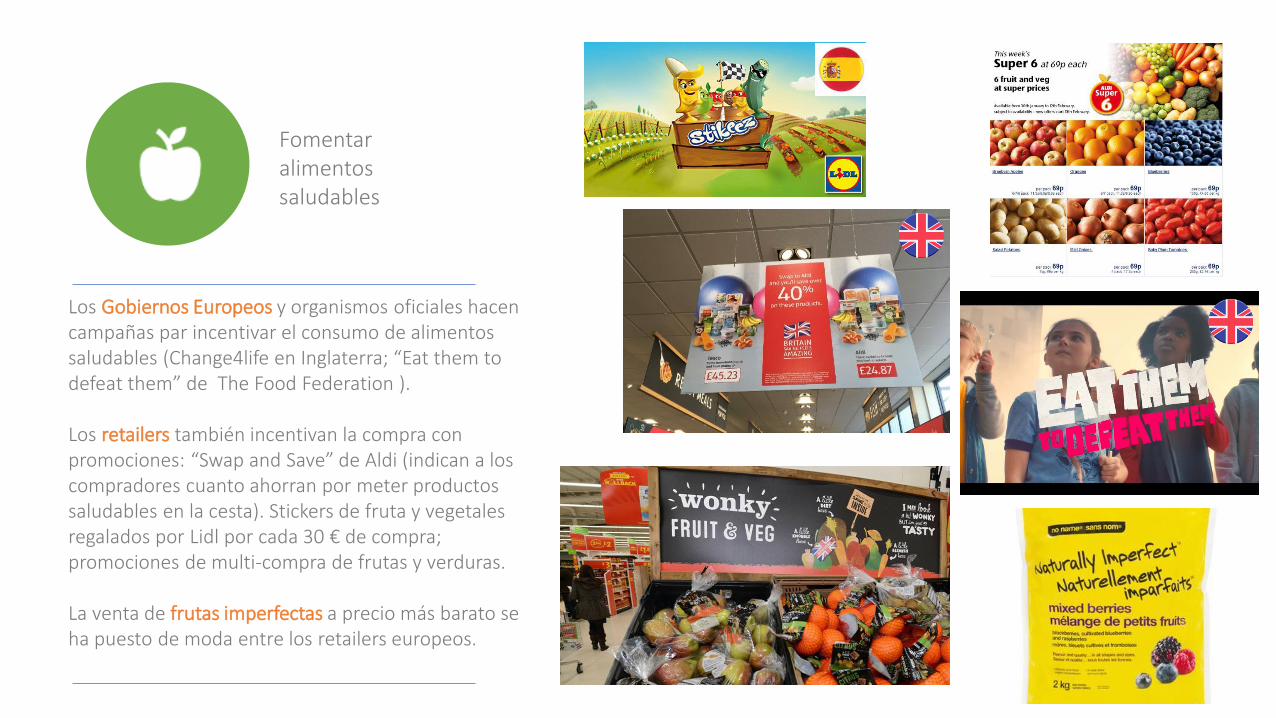

Fomentar alimentos saludables

Los Gobiernos Europeos y organismos oficiales hacen campañas par incentivar el consumo de alimentos saludables (Change4life en Inglaterra; “Eat them to defeat them” de The Food Federation ).

Los retailers también incentivan la compra con promociones: “Swap and Save” de Aldi (indican a los compradores cuanto ahorran por meter productos saludables en la cesta). Stickers de fruta y vegetales regalados por Lidl por cada 30 € de compra; promociones de multi-compra de frutas y verduras.

La venta de frutas imperfectas a precio más barato se ha puesto de moda entre los retailers europeos.

Influencers y sponsorship

Los retailers europeos hacen uso de famosos e influencers para sus campañas de consumo de frutas y verdurasy patrocinan equipos nacionales de deporte

Lidl patrocina la Liga de Balonmano de Dinamarca

Rema 1000 patrocina la Liga de Balonmano de Noruega

Nuevas misiones de compra

Los retailers europeos se enfocan en las misiones de compra de salud.

ICA ofrece a sus clientescuidados primarios a travésde su clínica “Min Doctor”

Lidl lanzó el año pasado enFinlandia una tienda on line,

enfocada en superfoods, vitaminas y suplementos

alimenticios.

@

¿ C Ó M O R E S P O N D E N L A S C A D E N A S A L A S T E N D E N C I A S ?

S O S T E N I B I L I D A D Y H A C E R L O C O R R E C T O

CERTIFICACIONES, FOOD SAFETY, GLOBAL GAP, ETI…HUELLA DE CARBONO, HUELLA HÍDRICA…

@

¿ C Ó M O R E S P O N D E N L A S C A D E N A S A L A S T E N D E N C I A S ?

A U G E D E L C O M E R C I O O N L I N E

¿ C Ó M O R E S P O N D E N L A S C A D E N A S A L A S T E N D E N C I A S ?

I N T E R A C C I Ó N C O N E L C L I E N T E Y C O M U N I C A C I Ó N

© IGD 2018 Page 48

FOOD-TO

-GO(11%)

Source: IGD Research

Help me save time

Ocado’s new meal list function allows shoppers to create ingredients’ lists for

their favourite meals

Help me be healthier

Asda is working with Foodmaestro to offer

personalised filtering for allergens, intolerances,

diets and lifestyles

Help me try new things

Unilever’s Recipedia is a voice activated Amazon

Alexa, helps shoppers look for recipes, specific

ingredients or to meet dietary / nutritional needs

Help me make the right choices

Co-op development to show shoppers the journey

of fresh produce from source to shelf

¿ C Ó M O R E S P O N D E N L A S C A D E N A S A L A S T E N D E N C I A S ?

A S I S T E N T E S P E R S O N A L E S I N T E L I G E N T E S

GRACIAS

CONTACTO:

DAV I D. A L B A @ A M C F R E S H G RO U P I N N O VAT I O N .C O M