Nuestro entorno económico (editorial) · Se rohibe la reproducción total o arcial del ontenido...

8

Perspectivas Año 25 Núm. 8 septiembre 2018 Estudios Técnicos, Inc. no necesariamente suscribe los puntos de vista de los artículos incorporados en la revista, uno de cuyos objetivos es, precisamente, presentar diversos acercamientos a temas de política pública. Perspectivas es una publicación de Estudios Técnicos, Inc. Se prohibe la reproducción total o parcial del contenido sin el consentimiento de los editores. Si le interesa recibir Perspectivas en formato electrónico comuníquese a través de [email protected] o a través del 787-751-1675. © 2018. Domenech 113 Hato Rey, Puerto Rico 00918-3501 • estudiostecnicos@estudios-tecnicos.com. Continúa en la página 2 Contenido Nuestro entorno económico (editorial)................................................................................................... 1 La participación laboral .............................................................................................................................................2 La economía global ...................................................................................................................................................... 4 The Drug Pricing Reform Effort .......................................................................................................................5 10 Years After (Not The Band) .......................................................................................................................... 6 Threatening retaliation over closer relations with China is misguided.............7 Por Los editores Nuestro entorno económico (editorial) E ste número de Perspectivas está dedicado mayormente a temas que no son directamente de Puerto Rico pero que nos impactan. Luego del huracán María hace un año, y como es de esperar, la atención se centró en la recuperación y reconstrucción del país. Pensamos que a un año del huracán era positivo traer ante los lectores de la revista, temas relacionados a nuestro entorno económico. En Estudios Técnicos, Inc. siempre hemos dado mucha importancia al contexto global y regional dentro del cual evoluciona nuestra economía, precisamente por ser una extraordinariamente abierta a las influencias de ese entorno. De ese interés han surgido varias iniciativas como fueron el primer estudio de la política de comercio exterior, el plan estratégico de comercio exterior, los estudios sobre la exportación de servicios y, en números previos de esta publicación, muchos trabajos relacionados al contexto externo. Se incluye una nota del Fondo Monetario Internacional sobre un tema que ha estado en el centro de la discusión sobre la economía en Puerto Rico, la tasa de participación laboral. En esta nota se mencionan tendencias globales que, en algunos casos, contrastan con lo ocurrido aquí pero que, sobre todo, nos ayudan a entender mejor las razones por las cuales esa tasa es tan baja en Puerto Rico. De la OECD se publican las perspectivas globales pues, aunque muchos se sienten cobijados por la sombrilla que es la economía norteamericana, no estamos aislados de lo que ocurre a nivel global. Se publican dos columnas de Douglas Holtz-Eakin, un conocido economista norteamericano quien fuera Director

Transcript of Nuestro entorno económico (editorial) · Se rohibe la reproducción total o arcial del ontenido...

Perspectivas Año 25Núm. 8

septiembre 2018

Estudios Técnicos, Inc. no necesariamente suscribe los puntos de vista de los artículos incorporados en la revista, uno de cuyos objetivos es, precisamente, presentar diversos acercamientos a temas de política pública.

Perspectivas es una publicación de Estudios Técnicos, Inc. Se prohibe la reproducción total o parcial del contenido sin el consentimiento de los editores. Si le interesa recibir Perspectivas en formato electrónico comuníquese a través de [email protected] o a través del 787-751-1675. © 2018. Domenech 113 Hato Rey, Puerto Rico 00918-3501 • [email protected].

Continúa en la página 2

ContenidoNuestro entorno económico (editorial) ...................................................................................................1La participación laboral .............................................................................................................................................2La economía global ...................................................................................................................................................... 4The Drug Pricing Reform Effort .......................................................................................................................510 Years After (Not The Band) ..........................................................................................................................6Threatening retaliation over closer relations with China is misguided.............7

Por Los editores

Nuestro entorno económico (editorial)

Este número de Perspectivas está dedicado mayormente a temas que no son directamente de Puerto Rico pero que nos impactan. Luego del huracán María hace un año, y

como es de esperar, la atención se centró en la recuperación y reconstrucción del país. Pensamos que a un año del huracán era positivo traer ante los lectores de la revista, temas relacionados a nuestro entorno económico. En Estudios Técnicos, Inc. siempre hemos dado mucha importancia al contexto global y regional dentro del cual evoluciona nuestra economía, precisamente por ser una extraordinariamente abierta a las influencias de ese entorno. De ese interés han surgido varias iniciativas como fueron el primer estudio de la política de comercio exterior, el plan estratégico de comercio exterior, los estudios sobre la exportación de servicios y, en números previos de esta publicación, muchos trabajos relacionados al contexto externo.

Se incluye una nota del Fondo Monetario Internacional sobre un tema que ha estado en el centro de la discusión sobre la economía en Puerto Rico, la tasa de participación laboral. En esta

nota se mencionan tendencias globales que, en algunos casos, contrastan con lo ocurrido aquí pero que, sobre todo, nos ayudan a entender mejor las razones por las cuales esa tasa es tan baja en Puerto Rico. De la OECD se publican las perspectivas globales pues, aunque muchos se sienten cobijados por la sombrilla que es la economía norteamericana, no estamos aislados de lo que ocurre a nivel global.

Se publican dos columnas de Douglas Holtz-Eakin, un conocido economista norteamericano quien fuera Director

Perspectivas septiembre 2018

2

Viene de la portada

del Congressional Budget Office y ha ocupado importantes posiciones en el Council of Foreign Relations y el Peterson Institute for International Economics, ambas entidades muy prestigiosas. Una de las columnas se relaciona con el financiamiento de los programas de salud, tema que es medular para nosotros, y la otra trata con la crisis financiera del 2008 y lo que ha ocurrido en los diez años posteriores. Esa crisis y sus consecuencias tuvieron un fuerte impacto negativo en Puerto Rico y por eso pensamos que era deseable publicar esta nota en Perspectivas.

Como en otras ocasiones, publicamos una columna de David Jessop, del Caribbean Council de Londres. Es la segunda sobre el tema de la creciente influencia de China en América Latina y el Caribe que se publica en Perspectivas. Este tema adquiere particular vigencia a la luz del reconocimiento de China por parte de varios países de la región y la reacción de la Administración Trump a estas acciones. La tendencia innegable es que China asumirá una importancia cada vez mayor en la región y que, en gran medida, las acciones de la Administración Trump contribuyen a que esto sea así.

La participación laboralBy Los editores

El tema de la participación laboral ha sido una constante en Puerto Rico desde hace muchos años por ser mucho más baja aquí que en otras jurisdicciones. El Fondo Monetario Internacional (FMI) en su World Economic Outlook de abril de 2018 incluye un extenso análisis del tema y como se manifiesta en las economías desarrolladas. En esta nota se presenta un resumen del análisis del FMI (p. 71 del World Economic Outlook de abril de 2018) traducido al español, y como se relaciona con la situación en Puerto Rico. De acuerdo al FMI la tasa de participación agregada se ha mantenido a niveles cercanos al 60% del 1985 al 2016, mientras que la de mujeres aumentó de 45% a 55% en el período. En todos los grupos, el nivel educativo es un factor que explica mucho de la tasa, ya que a mayor nivel mayor la tasa de participación. El informe del FMI es detallado y solamente se resumen los hallazgos principales a continuación.

El resumen del informe del FMI

El FMI señala que no obstante el envejecimiento de la población en prácticamente todos los países, las tasas de participación laboral reflejan tendencias muy distintas. Los números agregados esconden el hecho de que los diferentes grupos de trabajadores reflejan tendencias muy distintas: la participación ha mejorado en mujeres de edad productiva y, más recientemente, en personas de mayor edad. Se ha reducido entre los jóvenes y en hombres en la edad productiva, lo que el FMI llama “prime age”. Se le atribuye la reducción en la pasada década en la participación de hombres a la crisis financiera de los pasados años y al envejecimiento de la población. Sin embargo, la creciente participación de mujeres apunta a que hay otros factores que influyen en la tasa de participación.

3

Perspectivas septiembre 2018

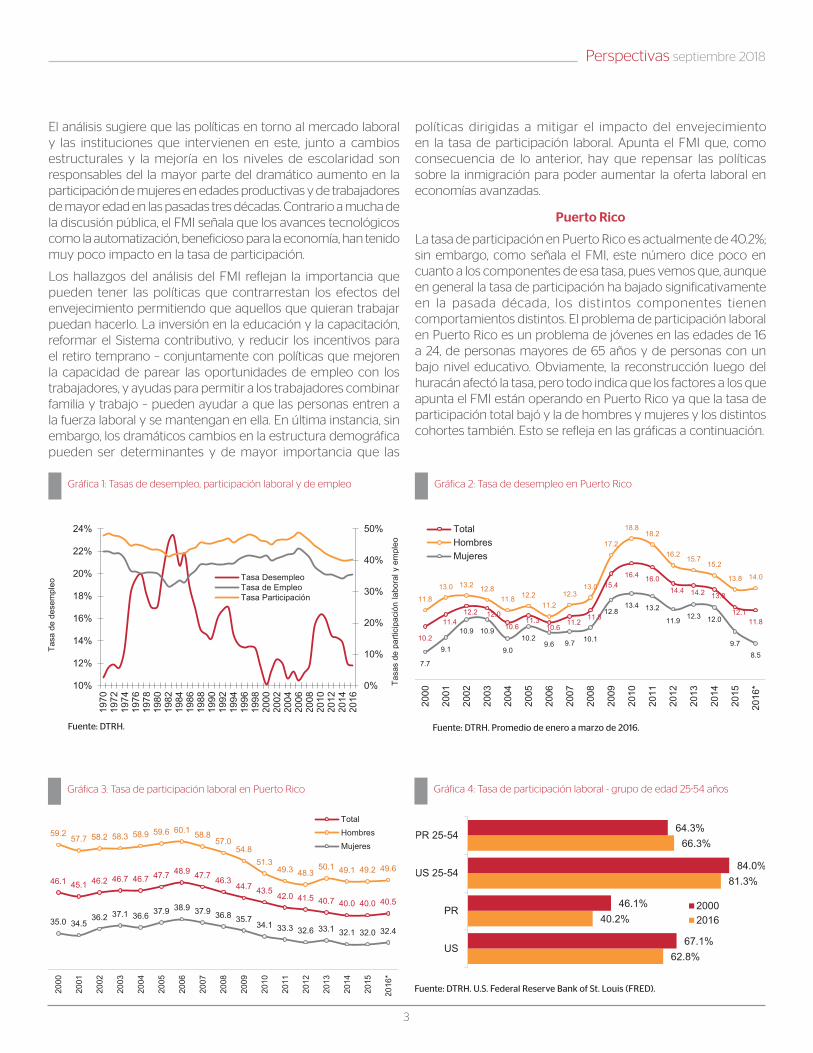

Gráfica 1: Tasas de desempleo, participación laboral y de empleo Gráfica 2: Tasa de desempleo en Puerto Rico

Gráfica 3: Tasa de participación laboral en Puerto Rico Gráfica 4: Tasa de participación laboral - grupo de edad 25-54 años

Fuente: DTRH. Fuente: DTRH. Promedio de enero a marzo de 2016.

Fuente: DTRH. U.S. Federal Reserve Bank of St. Louis (FRED).

El análisis sugiere que las políticas en torno al mercado laboral y las instituciones que intervienen en este, junto a cambios estructurales y la mejoría en los niveles de escolaridad son responsables del la mayor parte del dramático aumento en la participación de mujeres en edades productivas y de trabajadores de mayor edad en las pasadas tres décadas. Contrario a mucha de la discusión pública, el FMI señala que los avances tecnológicos como la automatización, beneficioso para la economía, han tenido muy poco impacto en la tasa de participación.

Los hallazgos del análisis del FMI reflejan la importancia que pueden tener las políticas que contrarrestan los efectos del envejecimiento permitiendo que aquellos que quieran trabajar puedan hacerlo. La inversión en la educación y la capacitación, reformar el Sistema contributivo, y reducir los incentivos para el retiro temprano – conjuntamente con políticas que mejoren la capacidad de parear las oportunidades de empleo con los trabajadores, y ayudas para permitir a los trabajadores combinar familia y trabajo – pueden ayudar a que las personas entren a la fuerza laboral y se mantengan en ella. En última instancia, sin embargo, los dramáticos cambios en la estructura demográfica pueden ser determinantes y de mayor importancia que las

políticas dirigidas a mitigar el impacto del envejecimiento en la tasa de participación laboral. Apunta el FMI que, como consecuencia de lo anterior, hay que repensar las políticas sobre la inmigración para poder aumentar la oferta laboral en economías avanzadas.

Puerto Rico

La tasa de participación en Puerto Rico es actualmente de 40.2%; sin embargo, como señala el FMI, este número dice poco en cuanto a los componentes de esa tasa, pues vemos que, aunque en general la tasa de participación ha bajado significativamente en la pasada década, los distintos componentes tienen comportamientos distintos. El problema de participación laboral en Puerto Rico es un problema de jóvenes en las edades de 16 a 24, de personas mayores de 65 años y de personas con un bajo nivel educativo. Obviamente, la reconstrucción luego del huracán afectó la tasa, pero todo indica que los factores a los que apunta el FMI están operando en Puerto Rico ya que la tasa de participación total bajó y la de hombres y mujeres y los distintos cohortes también. Esto se refleja en las gráficas a continuación.

Perspectivas septiembre 2018

4

Tabla 1: Real GDP growthYear-on-year, %. Arrows indicate the change in growth rate from previous year

La economía globalPor Los Editores

La Organización de Cooperación Económica y Desarrollo (OCED) publicó su más reciente proyección de la economía global en mayo de este año y la publicación (OECD Economic Outlook, May, 2018) contiene temas que resultan de mucho interés, más allá de lo que proyecta con respecto al crecimiento económico. Es bueno mencionar que la OCED reúne a las economías desarrolladas del mundo y sus informes son una importante fuente de inteligencia económica.

Las proyecciones para el 2018 y 2019 de la OCED reflejan una economía global que crecerá a ritmos muy saludables en estos dos años, pero con ritmos muy diversos entre países, como queda claro en la tabla 1.

Lo más notable es que tanto China como India tuvieron los crecimientos más altos e, inclusive, India por encima de China por alrededor de un punto porcentual anual. En el Informe se hace un análisis de lo que cada región y país contribuye al crecimiento del PNB real global y esos dos países contribuyen con cerca del 50% del total. Aunque era evidente que el centro de gravedad de la economía global se movía en dirección de Asia, estos números lo confirman más allá de toda duda. Del Informe también surge que los seis países de América Latina incluidos – Argentina, Brasil, Chile, Colombia, Costa Rica y México – todos tendrán economías relativamente robustas con crecimientos de entre 2.0% (Brasil) a 3.7% (Costa Rica).

Si bien los próximos dos años reflejan un panorama positivo, la OCED hace la advertencia de que esto puede cambiar más adelante. Los riesgos que se identifican son los siguientes:

• Un aumento importante en el precio del petróleo debido a la volatilidad geo-política

• Aumentos en las tasas de interés

• Tensiones en el comercio internacional

• Volatilidad financiera

Un dato interesante del Informe que parece sustentar la tesis de Pickety en cuanto al crecimiento del capital y la remuneración a la mano de obra es que el valor de los mercados de acciones aumentará en cerca de un 50% entre el 2014 y el 2018 (“global stock market capitalization”). Un aumento sustancialmente superior al de los salarios.

El informe contiene recomendaciones para estimular el crecimiento sostenido en las economías de sus miembros que incluyen reducir las contribuciones a personas asalariadas de ingresos bajos, enfatizar en contribuciones sobre la propiedad, aumentar los beneficios a familias de ingresos bajos, reducir las barreras de entrada para profesionales, mejorar la infraestructura digital y varias otras.

El Informe está disponible en la página web de la OCED.

5

Perspectivas septiembre 2018

By Douglas Holtz-Eakin

The Drug Pricing Reform Effort

Yesterday marked 100 days since President Trump announced his drug pricing blueprint, the basic goal of which is to “lower prices” somehow. How successful has it been?

In thinking about this question, it is useful to remind oneself that drug production and distribution is largely market-based, and the lesson of the market framework is that prices fall only if there is an increase in supply, a decrease in demand, or a reduction in taxes and other overhead-like costs. Broadly speaking, there is little interest in decreasing the demand for drugs per se, so most of the focus is on increasing supply.

Regarding supply, the Department of Health and Human Services (HHS) will quickly point out that in the past 100 days the Food and Drug Administration (FDA): approved a record number of generic drugs in July; approved the first generic drug under a pathway designed to fight price gouging; launched a working group on how safe, short-term importation of certain medically necessary drugs could address price spikes; and announced an FDA Biosimilar Action Plan to spur competition among expensive biologic drugs. To be honest, the last two of those are merely announcements — no action yet — and the impact of the second is limited, but the focus is on increasing supply.

But there have been lots (and lots) of other initiatives as well. Why? Digging a bit deeper reveals that not all drugs are the same. There are brand-name drugs protected by patents, and generic drugs that compete with those whose patent has expired. Among the patented drugs, certainly there are some that are therapeutically unique. In short, there are lots of situations where little can be done to increase supply, but there may be room for negotiating a better price on the few that are on the market and available for use.

For example, the Center for Medicare and Medicaid Services (CMS) took action to provide Medicare Advantage (MA) plans greater flexibility in their benefit design and coverage of certain medicines. MA plans will now be able to impose step therapy requirements as a way to manage utilization of physician-administered drugs (that is, not outpatient drugs taken at home) covered under the Medicare Part B benefit. It is hoped that this expanded authority will enable insurers to promote the use of higher-value medicines and better negotiate discounts for drugs. (In a managed care setting, “step therapy” is an approach to prescription drugs where a patient begins treatment for a medical condition with the most cost-effective drug therapy and progresses to other more costly or risky therapies only if necessary.)

Specifically, CMS rescinded a memo from September 2012 that stated MA plans were not allowed to impose additional requirements (such as step therapy) that would hinder access to Part B drugs or services. Additionally, MA prescription drug plans will have new authority to cross-manage Part B and Part D drugs by allowing drugs covered under one benefit to be the first step of a treatment plan before allowing use of a drug covered by the other benefit. Any step therapy requirement must be coupled with drug-management and care-coordination services, and at least half of the savings generated from reduced drug costs must be shared with the beneficiary. These requirements are intended to encourage patient participation, which is essential to realizing better health management and medication adherence.

The other way to reduce prices of drugs is to reduce the explicit and implicit taxes on them. Congress made things a bit worse in this regard recently by increasing the fraction of Medicare Part D costs that must be paid by pharmaceutical firms — a tax in disguise. (See the discussion in Tara O’Neill Hayes’ reform piece.) Among the most important of the implicit taxes is the 340B Drug Pricing Program (340B). Under the 340B program, manufacturers must provide discounts to eligible health care providers for covered outpatient drugs. There was no guarantee that those providers were passing along any of the discounts to the low-income patients they were intended to benefit, and the lost revenue from the discount has to be made up elsewhere (the implicit tax), so CMS introduced reforms in 2017. In the past 100 days, CMS extended this policy to 340B drugs provided at off-campus hospitals sites, while also reforming the calculation of the average sales price (ASP) for biosimilars.

The final lever that the government could pull is essentially shifting part of the price onto someone else. That might not make drugs cheaper for the health care system as a whole, but it could relieve some of the burden on, for example, consumers. CMS has instituted a wide range of proposals to reduce the out-of-pocket portion paid by consumers.

Nobody should have expected a 100-day miracle in drug pricing — the economics are simply too daunting. But by continuing to pursue policies of increased supply, stronger negotiations, and fewer explicit and implicit taxes, the administration can make additional progress.

Note:

Douglas Holtz-Eakin is the President of the American Action Forum. Read more: https://www.americanactionforum.org/experts/douglas-holtz-eakin/#ixzz5PNhxvS6U

Perspectivas septiembre 2018

6

10 Years After (Not The Band)By Douglas Holtz-Eakin

This week marks 10 years since the full fury of the financial crisis and raises the obvious question as to whether policymakers have absorbed the lessons of the crisis and are prepared to prevent a recurrence.

No.

They haven’t, at least in the United States, because they continue to frame this as a U.S.-specific regulatory failure. That is wrong. As we put it in my dissent on the Financial Crisis Inquiry Commission (FCIC), “We also reject as too simplistic the hypothesis that too little regulation caused the crisis, as well as its opposite, that too much regulation caused the crisis. We question this metric for determining the effectiveness of regulation. The amount of financial regulation should reflect the need to address particular failures in the financial system. For example, high-risk, nontraditional mortgage lending by nonbank lenders flourished in the states and did tremendous damage in an ineffectively regulated environment, contributing to the financial crisis. Poorly designed government housing policies distorted market outcomes and contributed to the creation of unsound mortgages as well. Countrywide’s irresponsible lending and AIG’s failure were in part attributable to ineffective regulation and supervision, while Fannie Mae and Freddie Mac’s failures were the result of policymakers using the power of government to blend public purpose with private gains and then socializing the losses. Both the ‘too little government’ and ‘too much government’ approaches are too broad-brush to explain the crisis.”

Even more important, the financial crisis was global. Again, “There were housing bubbles in the United Kingdom, Spain, Australia, France and Ireland, some more pronounced than in the United States. Some nations with housing bubbles relied little on American-style mortgage securitization. A good explanation of the U.S. housing bubble should also take into account its parallels in other nations. This leads us to explanations broader than just U.S. housing policy, regulation, or supervision. It also tells us that while failures in U.S. securitization markets may be an essential cause, we must look for other things that went wrong as well.”

But the one thing that continues to resonate is the role of real estate, commercial and residential. As The Economist succinctly put it, “The precise shape of the next financial crisis is unclear—otherwise it would surely be avoided. But, in one way or another, it is likely to involve property. Rich-world governments have never properly reconciled a desire to boost home ownership with the need to avoid dangerous booms in household credit, as in the mid-2000s.”

That is the key. Policymakers across the globe continue to push home ownership, minimizing down payments, subsidizing interest costs, and looking shocked when the financially unprepared are

unable to maintain their financial commitments. In the United States these terrible instincts are codified in the form of taxpayer-back subsidies to borrowing to own homes. (Think about it, why is it good public policy to force someone to go in debt to get help?) The poster children for this stance are Fannie Mae and Freddie Mac, whose public policy purpose was to keep low the 30-year fixed rate mortgage interest and use some of their earnings as off-budget slush funds to promote “affordable housing.” The only catch was that Fannie and Freddie got to pocket all the earnings in the good times, and the taxpayer held them harmless when the inevitable downturn transpired.

It is depressing, but nothing has changed, as evidence by a recent House Financial Services Committee hearing, “A Failure to Act: How a Decade without GSE Reform Has Once Again Put Taxpayers at Risk.” Former Acting Director of the Federal Housing Finance Authority Ed DeMarco summarized the state of play nicely, saying “Today’s ten-year anniversary of the failures and conservatorships of Fannie Mae and Freddie Mac is not a cause for celebration. What happened ten years ago to Fannie Mae and Freddie Mac had been forecast by some but denied as a possibility by many. Yet, Fannie Mae and Freddie Mac did fail, and taxpayers were forced to take on extraordinary financial risks bailing them out. Moreover, the fundamental challenge posed by their failure remains today…”

As more evidence of the bipartisan bad instincts of policymakers, check out this giveaway.

The short version is that real estate risk is systemic risk and we will never cure the large risks in the financial system as long as we treat them as a financial problem. They are not. They are a policy problem—a policy problem manifested by inappropriate housing subsidies and an unwillingness to expect people to be financially ready to own a home before they actually own a home.

Note:

Douglas Holtz-Eakin is the President of the American Action Forum. Read more: https://www.americanactionforum.org/experts/douglas-holtz-eakin/#ixzz5PNhxvS6U

7

Perspectivas septiembre 2018

Continúa en la página 8

Two weeks ago, El Salvador recognised China, breaking off its long-standing relationship with Taiwan. In so doing it followed recent decisions by Panama and the Dominican Republic to do the same.

What, however, was different this time around was the response from the Trump Administration.

The language was unequivocal. A statement from the White House said that the decision was of ‘grave concern’. Washington would, it observed, now revaluate its relationship with El Salvador and counter Chinese ‘political interference in the Western Hemisphere’. It added that the Government of El Salvador’s decision affected ‘the economic health and security of the entire Americas region’.

The statement coincided with US media reports that the Florida Senator, Marco Rubio, had discussed with Donald Trump ending US aid to the country and an earlier assertion by the US Ambassador, Jean Manes, that China might seek to transform the country’s commercial port of La Union into a military base.

What the strength of language in the White House statement suggested is that after decades of relative disinterest in China’s engagement in the Latin American and Caribbean region, the US has decided that it will now actively oppose China’s presence in the hemisphere.

Threatening retaliation over closer relations with China is misguided

By David Jessop

For the Caribbean - where now only Belize, St Kitts, St Vincent, St Lucia and Haiti recognise Taiwan – this and the language now being used by Washington suggests the need to consider how the region should respond to the increasingly fractious super power politics surrounding relations between China and the US.

Speaking last October in Beijing, President Xi could not have been clearer about China’s future role in the world. Then he told members of China’s Communist Party “it is time for us to take centre stage in the world and to make a greater contribution to humankind” and to offer a “new choice for the developing world”. This suggests, Venezuela apart, that the most taxing future foreign policy challenge the Caribbean and its neighbours will face is how to balance the quixotic nature of the present administration in Washington, with the significance of China’s accelerating global role.

While the US is still the Caribbean’s principle economic partner, recent studies have shown that within three decades a vastly more populous China will have far outstripped the US economy, enabling it to control around 30 per cent of the global economy though the unique economic model it is now constructing.

What seems not to be well understood in Washington is that this means that the region’s choice is not ideological. Instead it has welcomed China’s statements that it has no interest in imposing its model on the nations it works with, but rather is seeking through

Perspectivas septiembre 2018

8

Puede acceder las ediciones anteriores de Perspectivas escaneando el código desde su dispositivo móvil o a través de la siguiente dirección: http://www.estudiostecnicos.com/es/publicaciones/perspectivas.html32a ñ o s

Síguenos enEstudios Técnicos, Inc.

Viene de la página 7

investment, trade and other forms of linkage a ‘win-win’ approach, that is respectful of national interests.

In the Caribbean, this translates into a policy that is bringing billions of dollars in investment in infrastructure, new enterprises and multiple forms of development assistance. This was reflected in the outcome of January’s Second China-Community of Latin American and Caribbean States (CELAC) Ministerial Forum. There an agreed ten-page action plan went far beyond trade and development to advance initiatives that will provide support for the development of modern transport, telecommunications and IT infrastructure as a part of China’s Belt and Road project, and a deeper political and security relationship.

Unlike the US, which is busy trying to re-shore economic activity to make ‘America great again’, Beijing’s strategic approach revolves around a belief that overdependence on the west in trade is dangerous and that by enhancing co-operation with the non-western world all developing economies and many developed economies can grow, enabling its economic and political rise.

No one should be under any illusion about what this means or the ultimate outcome: by peaceful means China is advancing its desire to lead the world economy in a manner that ensures its continuing wealth, power and security. It aims to do so in ways that will change global relationships and thinking and will diminish the US’s role in the world.

Nothing better illustrates this and the ways in which China is causing even powerful nations to adapt than a section of a recent speech made by the French President, Emanuel Macron, to his country’s Ambassadors. “China”, he said “has posed one of the

most important geopolitical concepts of recent decades with its new silk routes. We cannot pretend that it does not exist. We must not give in to any guilty or short-term fascination: it is a vision of globalisation which has the stabilising virtues of certain regions, but which is hegemonic”.

Speaking to me recently one Caribbean Foreign Minister told me recently in relation to the US, that the region must determine where mutual interest lies. While there are positive relationships on security and investment, the region has to be clear about its sovereignty, the minister noted.

The Minister concerned added: “when it comes to China we have pointed out that they are investing and offering new opportunity. The US cannot expect to have influence without similar levels of engagement. The relationship with Washington has become more transactional, but we have shared values and global outlook. The influence of the US would be greater with greater investment”.

If the US does not want to see China playing a central role in future Caribbean development, threatening hemispheric nations is the wrong approach.

By framing China’s growing influence in the hemisphere in terms of security, considering cutting in response what little US aid remains, and stressing its hegemony in the hemisphere, the Trump administration seems intent on fighting a war that was lost long ago.

Washington needs to recognise that now is the time to develop in-depth complimentary programmes based on shared values. That is to say, for the Caribbean, the US should consider creating a new development model that addresses practically the impact of climate change on the region. This model should provide funding or tax incentives to US business to help renovate critical infrastructure and encourage productive investment and give support to multilateral programmes that address economic fragility.

Notas:

1. David Jessop is a consultant to the Caribbean Council and can be contacted at [email protected] Previous columns can be found at www.caribbean-council.org.

![ontenido Unidad [Flujo de informacion y omunicación online]](https://static.fdocuments.ec/doc/165x107/62c20a2c23e5db504f5f74dd/ontenido-unidad-flujo-de-informacion-y-omunicacin-online.jpg)

![ontenido Unidad [Protección de hardware y software]](https://static.fdocuments.ec/doc/165x107/62e86f8eac132257860d942b/ontenido-unidad-proteccin-de-hardware-y-software.jpg)