Idiomas

Páginas

Jurídico

MODELO ECONOMICOPLURINACIONAL PRODUCTIVO

ESTADO PLURINACIONAL DE BOLIVIA

Análisis del Plan Nacional de Desarrollo 2010 Plan Nacional de Desarrollo 2010 -- 2015 2015 (a partir de datos del gobierno de Bolivia)

Elaboración exposición gráfica: Maria Lohman

Temas a tratar

Las 4 crisis del CAPITALISMO

Dos modelos económicos

Inversiones y marco legal

Cifras y datos

Datos importantes para el ANALISIS

El Plan Nacional de Desarrollo 2010-2015

MODELO ECONOMICOPLURINACIONAL PRODUCTIVO

Las 4 crisis del CAPITALISMOqCrisis financieraqCrisis climáticaqCrisis energéticaqCrisis alimenticia

Fuente: LUIS ALBERTO ARCE CATACORAMINISTER OF ECONOMY AND PUBLIC FINANCES

MODELO ECONOMICOPLURINACIONAL PRODUCTIVO

Dos modelos económicos

Fuente: LUIS ALBERTO ARCE CATACORAMINISTER OF ECONOMY AND PUBLIC FINANCES

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

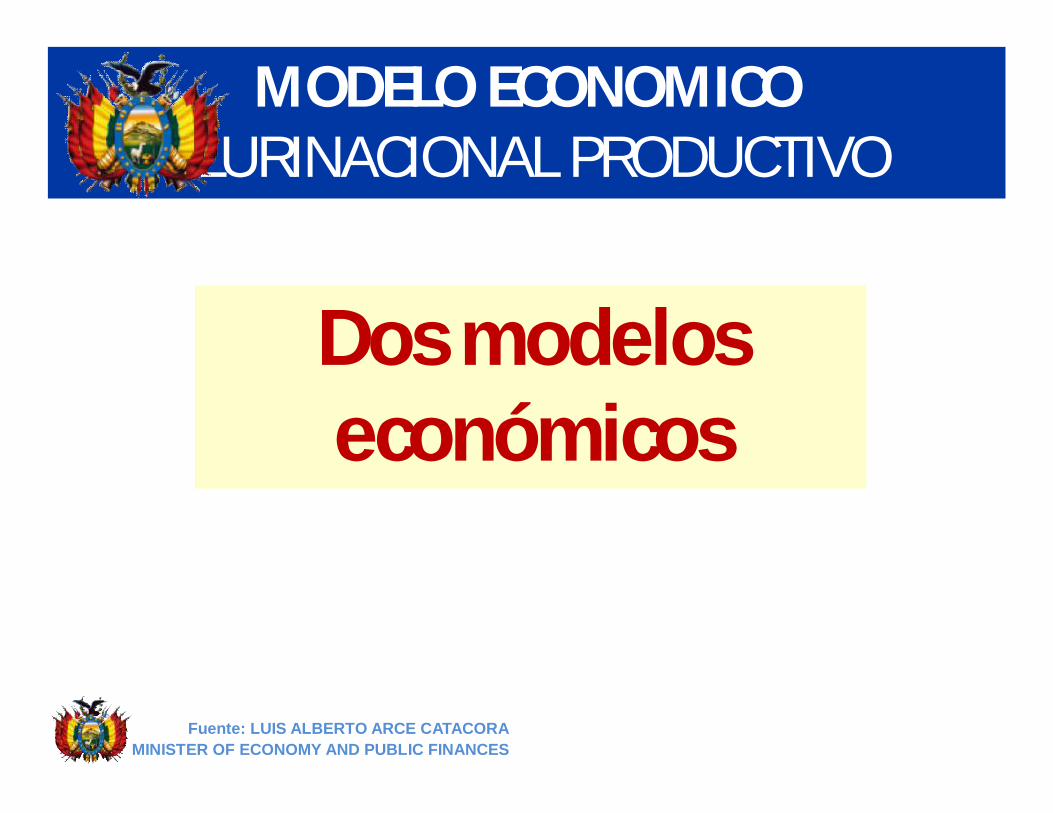

LIBRE MERCADO. The market is the mechanism for allocating resources

and the imbalance adjustor. Hypothesis: Efficient Market

EL ESTADO INTERVIENE to correct market failures (lack of redistribution

of wealth and transnational monopoly of strategic companies)

1. 1.

An isolated State. The market is a self-regulated mechanism of the

economic process

2. An active participation of the state in the economy. The state must

intervene in the economy through its seven facets: planner, entrepreneur,

investor, regulator, benefactor, developer, banker

2.

Privatization, the surplus is transferred abroad and without a

precautionary management policy of Natural Resources

Nationalization and control of strategic natural resources

3. 3.

A Primary Exporter DevelopmentPattern

4. A pattern of industrialization and productive development

4.

5

The Neoliberal Economic ModelThe Economic Social

Communitarian and Productive Model

El modelo económico neoliberal

El modelo económico social y comunitario

Preserving macroeconomic stability as a social asset y promueve el desarrollo

económico

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

High concentration of income, sectors excluded of society

5. Estado redistribuye5.

7. 7.Growth depends only on the external demand

Growth based on external and DEMANDA INTERNA

8. 8.Investment depends on external savings, boosting debt and fiscal

deficit

Generation of domestic resources for investment, superavit fiscal y baja en

la deuda

9. 9.Pobreza Stagnation, poverty, inequality of wealth and

opportunity

Development, redistribution and trabajo generation

Macroeconomic stability as an end in itself

10. 10.

Economy focused on private initiative 6. The State is the sponsor of a economía plural

6.

6

The Neoliberal Economic ModelThe Economic Social

Communitarian and Productive Model

El modelo económico neoliberal

El modelo económico social y comunitario

Fuente: Exposición de Alvaro García Linera nov. 2009 “REVOLUCIÓN DEMOCRÁTICA Y CULTURAL”

ETAPAS DEL NUEVO ESTADO•• REBELIONES

2000- 2005DEBILITAMIENTO DEL ESTADO NEOLIBERAL

• PROGRAMA DE GOBIERNO DE LOS MOVIMIENTOS SOCIALES2000-2005

• PROGRAMA DE GOBIERNO DE LOS MOVIMIENTOS SOCIALES2000-2005

CONSTRUCCIÓN DE UN BLOQUE SOCIAL DE PODER

• GOBIERNO DE LOS MOVIMIENTOS SOCIALES 2006 – 2009

• GOBIERNO DE LOS MOVIMIENTOS SOCIALES 2006 – 2009

VICTORIA ELECTORAL

• ASAMBLEA CONSTITUYENTE• ASAMBLEA CONSTITUYENTECONSTRUCCIÓN PACTADA DEL NUEVO ESTADO

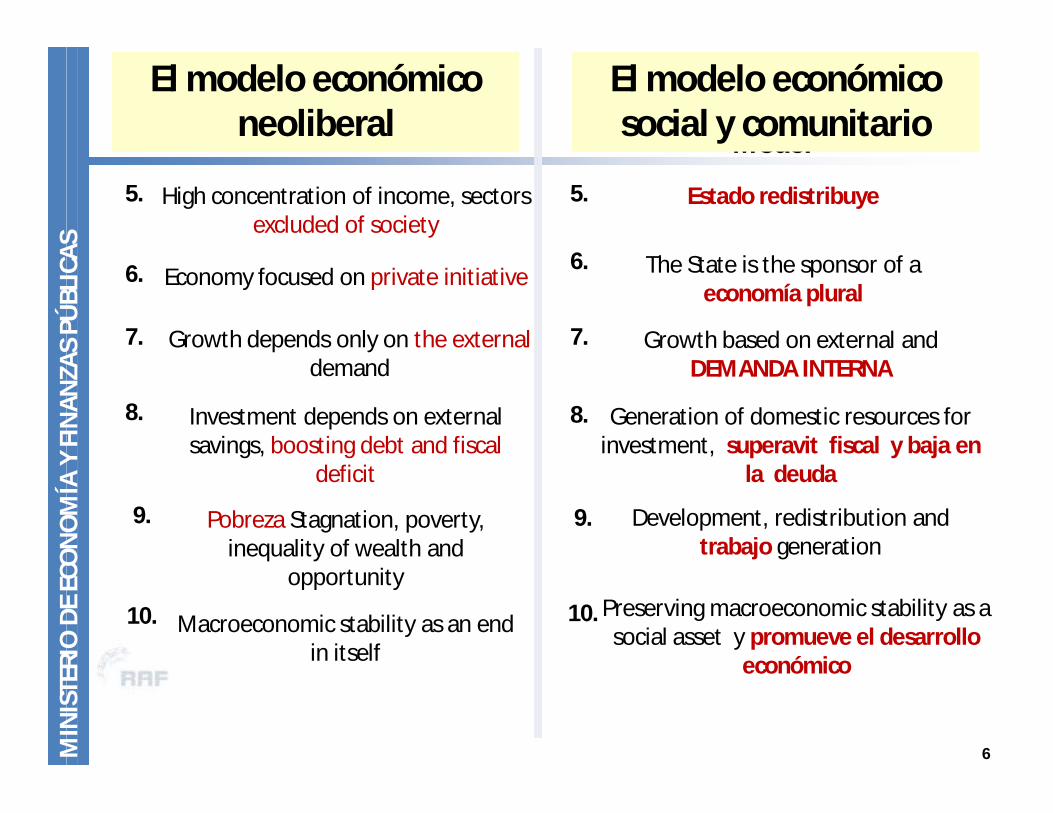

•• GUERRA ECONÓMICA 2007 – 2008• BOICOT A LA ASAMBLEA CONSTITUYENTE

2007 – 2008• GOLPE CÍVICO – PREFECTURAL 2008

CONTRA -REVOLUCIÓN

• REVOCATORIO 2008• FRACASO DEL GOLPE• CONGRESO CONSTITUYENTE 2008 • APROBACION DE LA NUEVA CPE

• REVOCATORIO 2008• FRACASO DEL GOLPE• CONGRESO CONSTITUYENTE 2008 • APROBACION DE LA NUEVA CPE

VICTORIA NACIONAL -POPULAR DEMOCRATICA

CONSOLIDACIÓN DEL ESTADO PLURINACIONAL 2009

2010 -1015

• DESARROLLAR EL ESTADO

PLURINACIONAL 2010 -1015

TAREA

Fuente: Exposición de Alvaro García Linera nov. 2009 “REVOLUCIÓN DEMOCRÁTICA Y CULTURAL”

Ø Nacionalización de las empresas públicasØ Estado productor y

conductor de la economía Ø Economía pluralØModernización de la

economía campesina, micro empresarial y comunalØ Apoyo a la empresa privada

productivaØ Economía globalizada

ECONOMIA SOCIAL Y

COMUNITARIA

NUEVA ECONOMIA

Fuente: Exposición de Alvaro García Linera nov. 2009 “REVOLUCIÓN DEMOCRÁTICA Y CULTURAL”

Sectores estratégicos,

generadores de GANANCIAS

Sectores quegeneran ingresos y

trabajo

• Hydrocarbons

• Mining

• Electricity

• Environmental Resources

• Industry, manufacturing and crafts

• Tourism

• Agricultural development

• Housing

• Trade, transport services, other services

Ganancias

ESTADO RETRIBUTIVO

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

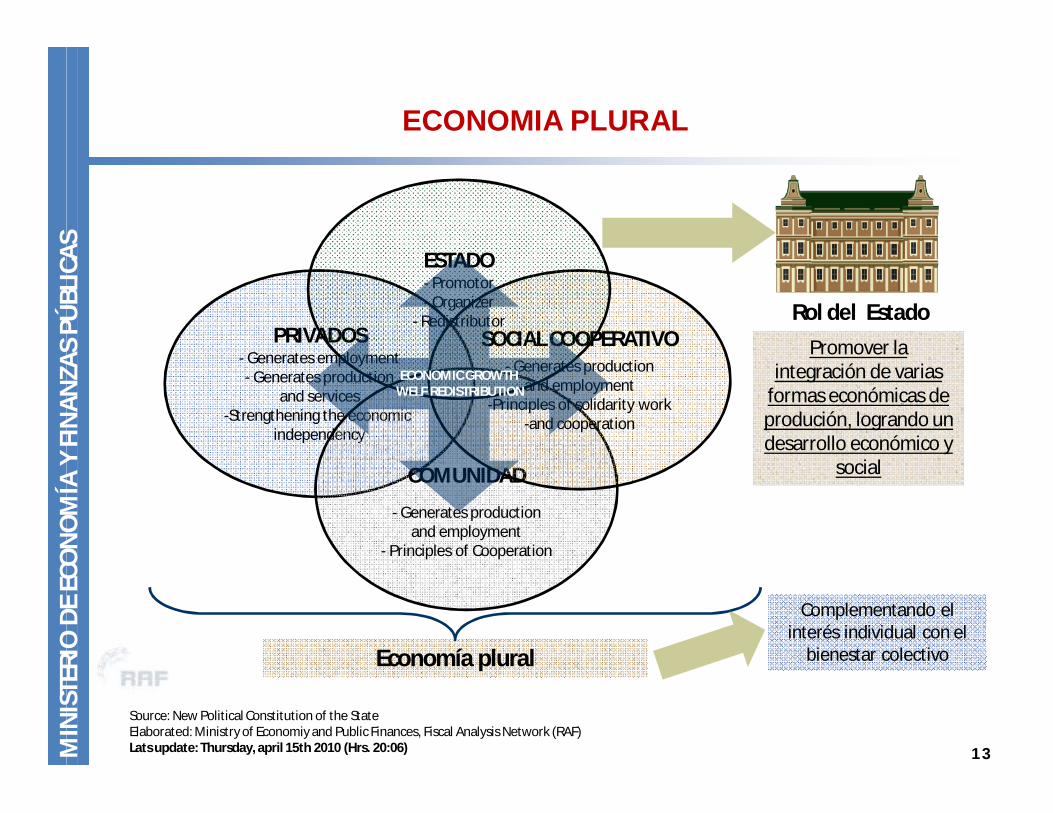

EL MODELO ECONOMICO SOCIAL, COMUNITARIO Y PRODUCTIVO

12

Source: New Political Constitution of the StateElaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Lats update: Thursday, april 15th 2010 (Hrs. 20:06)

PRIVADOS- Generates employment- Generates production

and services-Strengthening the economic

independency

Promover la integración de varias

formas económicas de produción, logrando un desarrollo económico y

social

Economía plural

COMUNIDAD

- Generates productionand employment

- Principles of Cooperation

SOCIAL COOPERATIVO- Generates production

and employment-Principles of solidarity work

-and cooperation

ESTADO- Promotor- Organizer

- Redistributor

Complementando el interés individual con el

bienestar colectivo

Rol del Estado

ECONOMIC GROWTHWELF REDISTRIBUTION

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

ECONOMIA PLURAL

13

Source: New Political Constitution of the StateElaborated: Ministry of Economiy and Public Finances, Fiscal Analysis Network (RAF)Lats update: Thursday, april 15th 2010 (Hrs. 20:06)

MODELO ECONOMICOPLURINACIONAL PRODUCTIVO

Cifras y datos. Inversiones - Ingreso por Nacionalización Petróleo y

recaudación Minera – BONOS – crecimiento ingresos Municipios y Prefecturas – crecimiento de Reservas – disminución Deuda

Pública / Deuda interna baja– mayor ingreso tributario –mayores depósitos en la Banca – Saneamiento de Tierras –

Crecimiento PIB – Disminución inflación – Crecimiento exportación/importaciones- Balance comercial positivo –

Reducción Pobreza

Fuente: LUIS ALBERTO ARCE CATACORAMINISTER OF ECONOMY AND PUBLIC FINANCES

NACIONALIZACIÓN DE LAS GANANCIAS

312.444383.091

600.963 626.507 647.083 668.757 676.939 678.797 683.308 687.445

462.196

569.106

862.140

953.1891.020.295

1.084.701 1.112.205 1.139.913 1.167.780 1.195.759

774.640

952.197

1.463.103

1.579.696

1.667.378

1.753.4581.789.144 1.818.710 1.851.088 1.883.204

0

200.000

400.000

600.000

800.000

1.000.000

1.200.000

1.400.000

1.600.000

1.800.000

2.000.000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Estimación del número de hogares beneficiarios con bonos (Renta Dignidad, Juancito Pinto, Juana Azurduy)

Área Rural

Área Urbana

Total

Fuente: Estimaciones UDAPE

Bolivia: Domestic public debt of the TGN, 1993 – Marzo 2010 (p)(In percent of GDP)

(p) PreliminarySource: Ministry of Economy and Public Finances, DGCPElaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Last update: Monday, april 12 2010 (Hrs. 12:13) 22M

INIS

TERI

O D

E EC

ON

OM

ÍA Y

FIN

ANZA

S PÚ

BLIC

AS

Mar

13,814,8 13,9 13,8 13,3 13,7

16,4

26,724,8 24,7

23,123,7

31,231,2

18,9

25,3

27,5

30,1

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,019

93

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

DECLINING DEBT

SANEAMIENTO DE TIERRAS

9 AÑOS 1996 - 2005 SANEADO9,3

MILLONES DE HA

3 AÑOS 2006 - 2009 SANEADO 23,5 HA

TIPO DE PROPIEDAD

755 785

712

714

720 77

2 796

790

806 88

5 953

1.00

0

1.05

0

1.00

1

995

942

895

894 95

0

1.01

0

1.32

8

1.18

2

1.65

1

1.68

3

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

(p)

2006

(p)

2007

(p)

2008

(p)

2009

(p)

Bolivia: PIB per capita, 1986 - 2009 (p) (In USD)

Average 1986 - 2005 2005 (p) 2006 (p) 2007 (p) 2008 (p) 2009 (p)

871 1.010 1.182 1.328 1.651 1.683

27MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

(p) PreliminarySource: National Statistic Institute (INE)Elaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Last update: Tuesday, april 13 2010 (Hrs. 18:42)

Bolivia: Real GDP composition by economic activity2000 - 2009 (p)

(In millions of Bs.1990)

(p) PreliminarySource: National Statistic Institute (INE)Elaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Last update: Monday, april 19th 2010 (Hrs. 09:33) 28M

INIS

TERI

O D

E EC

ON

OM

ÍA Y

FIN

ANZA

S PÚ

BLIC

AS

17%

13%

11%

11%

9%

8%

7%5%3%2%

13%

3.699 3.798 3.807 3.952 4.173 4.298 4.646 4.929 5.110 5.355

3.178 3.288 3.303 3.591 3.599 3.779 3.940 3.920 4.022 4.170 3.140 3.146 3.047 2.946 2.903 2.913 3.070 3.263 3.415 3.557 2.385 2.457 2.563 2.662 2.770 2.851 2.963 3.066 3.190 3.368 2.024 2.075 2.141 2.214 2.290 2.373

2.459 2.559 2.657 2.829

1.891 1.902 1.943 1.991 2.069 2.133 2.215 2.338 2.450

2.570 2.648 2.760 3.006 3.165 3.474 3.652

3.725 3.846

4.004 3.955

2.100 1.720 1.054

22.356 22.733 23.298 23.929 24.928

26.030 27.279

28.524 30.278

31.294

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

2000 2001 2002 2003 2004 2005 2006(p) 2007(p) 2008(p) 2009(p)

Manufacturing Agriculture and livestock Financial service institutesTransport, storage and comun. Public administration services ComerceMining Hydrocarbons ConstructionElectricity, gas and water Others

10,66

21,51

16,5618,01

14,52

10,469,31

8,52

12,58

7,956,73

4,393,13 3,41

0,922,45

3,944,62 4,91 4,95

11,85

0,69

11,73

0,260,0

5,0

10,0

15,0

20,0

25,0

30,019

85

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

668.171

Mar

29MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

Source: National Statistic Institute (INE)Elaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Last update: Tuesday, april 13 2010 (Hrs. 18:42)

SHARP DECLINE IN INFLATION

Bolivia: Anual inflation rate, 1985 – March 2010(In percent)

12-M

onth

HOSPITALES

282

340

389

506

413

471

410

374

1.11

9

900604

616 738 89

2

743 93

2

870

926

2.59

9

2.28

0

535 65

9 755 1.

007

919

607

418

524

1.31

5

1.22

5

837

490

524

403

359 36

5

372

862 997 1.28

1

1.46

7 1.77

095

2

946

611

504

458

7039941.1301.1771.196

1.4341.657

1.926

2.4512.0982.020

1.7081.8321.6921.920

2.440

2.926

5.100

4.467

692 700

3.588

0

1.000

2.000

3.000

4.000

5.000

6.000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2009

2010

Capital goodsRaw materials and intermediate productConsumer goodsOthers

Bolivia: Imports by economic use or destiny (CUODE)1990 – 2009, Accumulated January – February 2009 - 2010 (p)

(In millions of USD)

-12%

42%

23%

20%

Average 1985 - 2005 2006 2007 2008 2009 (p)

1.415 2.926 3.588 5.100 4.467

31MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

Jan-Feb

1%

(p) PreliminarySource: National Statistic Institute (INE)Elaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Last update: Monday, april 5 2010 (Hrs. 11:02)

AMBULANCIAS

64,8 63,6 63,566,4

63,1 63,3 63,260,6 59,9 60,1 59,3 58,3

51,954,5

51,454,5 54,3 53,9 54,4

51,1 50,3 50,9 51,2 50,1

83,9

78,0

84,087,0

77,7 78,8 77,7 77,6 76,5 77,374,3 73,8

40,0

45,0

50,0

55,0

60,0

65,0

70,0

75,0

80,0

85,0

90,0

1996 1997 1999 2000 2001 2002 2003-2004

2005 2006 2007 2008(e)

2009(e)

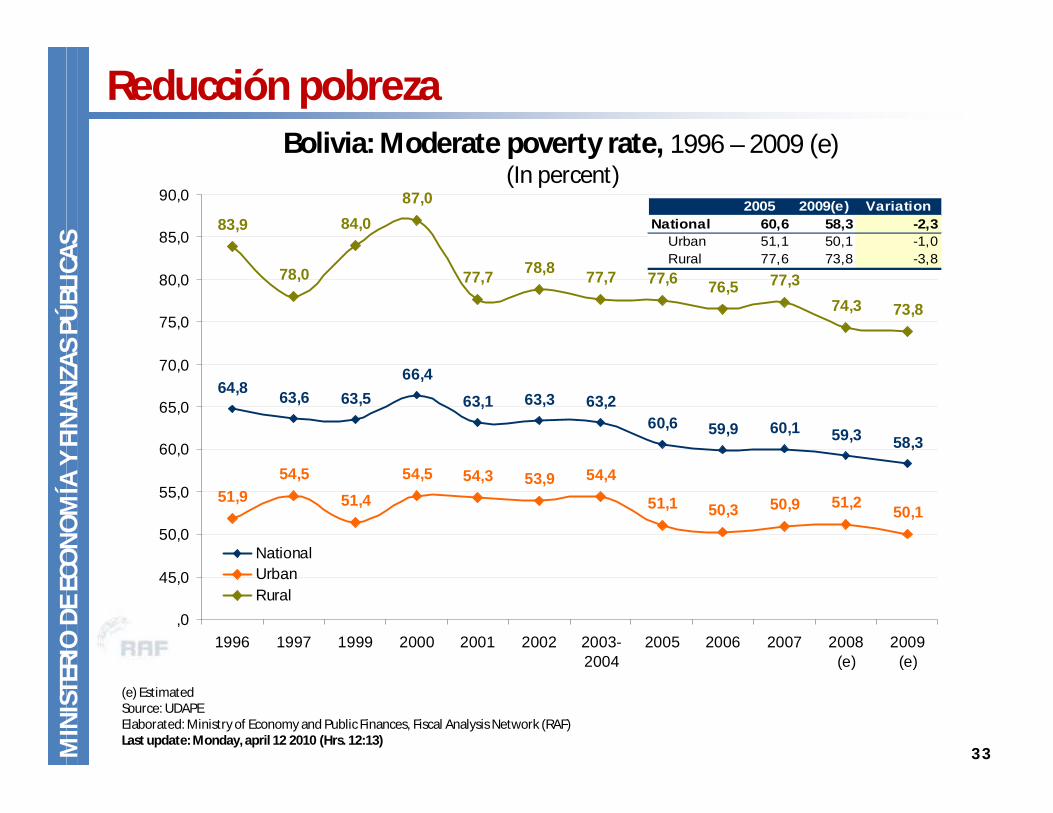

NationalUrbanRural

Bolivia: Moderate poverty rate, 1996 – 2009 (e)(In percent)

2005 2009(e) VariationNational 60,6 58,3 -2,3

Urban 51,1 50,1 -1,0Rural 77,6 73,8 -3,8

33MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS

Reducción pobreza

(e) EstimatedSource: UDAPEElaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Last update: Monday, april 12 2010 (Hrs. 12:13)

MODELO ECONOMICOPLURINACIONAL PRODUCTIVO

El Plan Nacional de Desarrollo 2010-2015

Fuente: LUIS ALBERTO ARCE CATACORAMINISTER OF ECONOMY AND PUBLIC FINANCES

BOLIVIA PRODUCTIVA

La Bolivia Productiva garantizará el desarrollo económico del país, continuandocon la transformación de la matriz productiva con capacidadde generar ahorro e inversión, empleo estable e ingresos y produccióndestinada al mercado interno y luego al externo.

Esta visión permitirá establecer un nuevo patrón de desarrollo –culminandola trayectoria histórica del patrón primario exportador vigente en el país–, ingresando a una nueva era de industrialización y generaciónde valor agregado.

En este sentido, se avanzará de un modelo donde solamente se hangenerado y creado condiciones para el desarrollo de algunas regionesdel país hacia otro modelo donde la prioridad es la generación equilibrada de capacidades productivas en el conjunto de territorios y regiones de Bolivia, logrando al mismo tiempo una articulación entre procesos dedesarrollo urbano y rural.

BOLIVIA PRODUCTIVAUno de los más importantes desafíos de esta transición es el hecho de que se debe avanzar en la creación de un escenario de equidad en lo que se refiere a la redistribución de la riqueza generada en las actividades productivas.

Este nuevo modelo económico está plasmado en la Nueva Constitución Política del Estado y en el Plan Nacional de Desarrollo presentado durante el Gobierno del MAS-IPSP.

Entonces, el propósito principal de nuestro Nuevo Modelo NacionalProductivo, basado en la Economía Plural, es crear las condiciones paragarantizar un incremento en la producción de los recursos naturales renovables y no renovables con el propósito de garantizar un mayor crecimiento económico del país pero con mayores ingresos, empleos y con mayor equidad social y económica, de tal modo que se lleve a cabo, porprimera vez en la historia del país, un proceso de redistribución de losingresos que resultan del desarrollo de las actividades productivas.

5 pilares► Expansión del Rol del Estado.

► Desarrollo productivo con valor agregado de los recursos naturalesy sustentabilidad ambiental.

► Participación activa de las economías (pública, privada, comunitariay cooperativa) en el aparato productivo.

► Producción para satisfacer el mercado interno y luego la exportación.

► Redistribución equitativa de de la riqueza y excedentes y reducciónde las desigualdades.

MODELO ECONOMICOPLURINACIONAL PRODUCTIVO

Plan de Inversiones2010-2015

Fuente: LUIS ALBERTO ARCE CATACORAMINISTER OF ECONOMY AND PUBLIC FINANCES

PROYECCION de INVERSIONES PROGRAMA 2010 - 2015

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

40

Este documento se encuentra sólo en versión inglés. Algunos títulos y subtitulos fueron traducidos al castellano

INVERSIONES PRIORITARIAS M

INIS

TER

IO D

E EC

ON

OM

ÍA Y

FIN

ANZA

S PÚ

BLI

CAS

41

Cuadro: Elaboración: Somos Sur (p) PreliminarySource: Ministry of Development PlanningElaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Last update: Monday, april 19th 2010 (Hrs. 10:35)

0

1000

2000

3000

4000

5000

6000

7000

8000Minería 7294

Hidrocarburos 7048Energía eléctrica 6585

Transporte 5597Produción industrial 931

Vivienda 680Comunicación -satelite 460

Agua y saneamiento básico 386Telecomunicación 306

Educación 280Desarrollo Rural 256

Erradicación de pobreza 251Represas e irrigación 91

Turismo 69Salud 68

Seguridad ciudadana 58Plan compatriota 43

Ciencias y tecnología 40Otros 2392

Achacachi

Vinto

Bermejo

El Alto

Caracollo

San Buenaventura

San JoséMisicuni

Cbba.Corocoro

Huanuni Zinc

Litio

Gran Chaco

Rositas

Santa Cruz El Mutún

Rio Grande

Cachuela Esperanza

El Bala

Miguillas

Villa Tunari

Challapata

Carrasco

MineríaLitio – Uyuni (I)Hierro – Mutún (I)Zinc – Potosí, Oruro (PreI)Huanuni (I)Fundación Vinto (I)Complejo Corocoro (F)

Industrialización de HidrocarburosRefineríaSanta Cruz y Cochabamba (PreI)

Amoníaco/Urea: Cochabamba (PreI)

Planta de Separación:Rio Grande (Santa Cruz) y Tarija (PreI)

Casas pre-fabricadas: Caracollo (I)

Gas to liquids, GTL: Gran Chaco (San Alberto, Sábalo, Margarita) (PreI)

Plantas de energía hidroeléctricaPara EXPORTACION: Cachuela Esperanza, El Bala y Rositas (PreI)Mercado interno: Miguillas, Misicuniy San José (PreI)

CARTONBOL (O)

LACTEOSBOL (O)PAPELBOL (O)

Empresas públicas

ECEBOL (I)

Empresa forestal Boliviana (EFB) (PreI)Empresa Boliviana de almendra (F)

AZUCARBOL (I)

Ingenio azucarero S. Buenaventura (PreI)

Estudios de pre-inversión (PreI)

Inversión (I)

Operación (O)

PRIORIDAD: INDUSTRIALIZAR HIDROCARBUROS, MINERIA, ENERGIA y otros

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

42

Area potencial de petróleo Area tradicionalExploración de PetróleoExploitación de petróleoNuevas áreas de exploraciónMadidi, Chepite, ChispaniAguaragüe , Camatindi norte y sur, San Telmo

Producción7 pozos en Margarita y Huacaya (Repsol)2 Pozos verticales aditionales- Incahuasi (E&P)Planta San AlbertoCampos al Norte

El desafío de la INDUSTRIALIZACIONM

INIS

TER

IO D

E EC

ON

OM

ÍA Y

FIN

ANZA

S PÚ

BLI

CAS

43

Sector HIDROCARBURIFERO Exploración y producción

RefineríaSanta Cruz, Cochabamba

IndustrializaciónAmoníaco/Urea: Cochabamba Provincia Gran Chaco (Campo San AlbertoSábalo, Margarita (GTL))

Plantas de separaciónSanta Cruz, Tarija

Refinería e industrialización

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

44

INVERSIONES EN HIDROCARBUROS (en mill. de dólares)

El desafío de la INDUSTRIALIZACIÓN

Projects Investment amount (e)

HIDROCARBUROS 7,048

- Hydrocarbon exploration 852- Hydrocarbon exploitation 648- Separation GLP Plant 450- Converting the energy matrix - natural gas distribution system

748

- Hydrocarbons industrialization 1,410- Hydrocarbons transportation 2,093- Hydrocarbons storage 62- Hydrocarbons refinement 715- Oil houses construction (YPFB - PEQUINVEN)

70

- Hydrocarbons Research and Technological Innovation Centre (CITH) 1

Complejo hidrometalúrgico Coro-Coro Inversión (50.000 TM cobre/año)

Fundición AUSMELT VINTO

Refinería nueva de Huanuni (3.000 TON/día)

Plantas hidrometalúrgicas de Zinc (Oruro / Potosí)

Hierro → El Mutún

Planta piloto de Carbonato de Litio (40 MT/día)

Producción de Carbonato de Litio a gran escala (400.000 MT/año)

Cloruro de Litio/ Litio Metal

Industria de baterías de Litio

Industria de automóviles eléctricos

Minería

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

45

El desafío de la INDUSTRIALIZACIÓN

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

46

INDUSTRIALIZACIÓN DEL LITIO“SALAR DE UYUNI”

FASES DEL PROYECTO DE LITIO1. Instalación de la Planta Piloto de Carbonatio

de Litio2. Producción a gran escala de carbonato de

litio3. Elaboración industrial de baterías de alta

tecnología en base al metal de litio

DESCRIPCIÓN DEL PROYECTODe acuerdo a The United States Geological Surveylas reservas del litio en Bolivia son de 5,4 millones de toneladas.

Entre los países con mayor demanda de litio están: Estados Unidos, China, Inglaterra, Alemania y Japón. El precio de este metal fluctúa alrededor de $ 4.300 por tonelada.

Base de Reserva Mundial de Litio(1), 2007

(In millions of tons)Lithium reserve

% Percent

Bolivia 5,4 49,1Chile 3,0 27,3China 1,1 10,0Brazil 0,9 8,3United States 0,4 3,7Canada 0,4 3,3Australia 0,3 2,4Zimbawe 0,0 0,2World total (rounded) 11,0 100,0

(1) That part of an identified reosurce that meets specified minimium physical and chemical criteria related to current mining and production practices, including those for grade, quality, thickness, and depht.Source: United States Geological Survey, Mineral Commodity Summaries 2007

INVERSIÓN MINERA(En millones de dólares)

EL RETO DE LA INDUSTRIALIZACIÓN

Projects Investment amount (e)

MINING 7.294

- Lithium industrialization - Salar de Uyuni (Potosí) - basic chemicals 2.500

- Two zinc's hidrometallurgical plants (Oruro - Potosi) 500

- Sulfuric acid production plant installation 120- Ausmelt furnace installation (Metallurgy company Vinto - Oruro) 20

- Metal Recovery Karachipampa (Potosí) 140Mecanization program's of statal mining- Elaboration of geological maps 40- Mechanization of statal mining 115- Mutun exploitation (50% not concessioned) 3.645- Corocoro Kores (Foreign direct investment) 214

PRODUCTION 300

Lithium Battery Plants- Lithium batteries production industrial plant 300

Minería

PROYECTOS PARA EXPORTACIÓN

PROYECTOS HIDROELÉCTRICOS(En millones de dólares)

PROYECTOS PARA EL CONSUMO INTERNO

Cachuela Esperanza

El Bala

Rositas

Miguillas

Misicuni San José

Energía

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

47

Installed power

(MW)

Revenue / year (e)

Misicuni (Cochabamba) 80 10San José (Chapare) 120 25Miguillas (Inquisivi, La Paz) 250 95

Installed power

(MW)

Revenue / year (e)

Cachuela Esperanza (Beni) 800 359Rositas (Río Grande,Santa Cruz) 400 146El Bala (North La Paz) 1600 619

EL RETO DE LA INDUSTRIALIZACIÓN

PROYECTOS PARA EXPORTACIÓN

PROYECTOS PARA EL CONSUMO INTERNO

Cachuela Esperanza

El Bala

Rositas

Miguillas

Misicuni San José

Energía

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

48

INVERSIÓN EN ENERGÍA ELÉCTRICA(En millones de dólares)

EL RETO DE LA INDUSTRIALIZACIÓN

Projects Investment amount (e)

ELECTRICAL ENERGY 6.585

- Cachuela Esperanza (Beni) hydroelectrical construction 2.500

- Rositas (Rio Grande, Santa Cruz) hydroelectrical construction 640

- El Bala (North La Paz) hydroelectrical construction 2.400

- Miguilla (Inquisivi, La Paz) central hydroelectrical construction 375

- Laguna Colorada (Potosí) geothermal plant construction 350

- San José (Cochabamaba) hydroelectrical construction 195

- Wind energy generation 125

Carreteras existentes

Perú

Brazil

Puerto Ustariz

Yacuiba

GuayaramerínCobija

La Paz

Villazon ParaguayChile

S. I. Moxos

Villa Tunari

Programa de gobierno

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS Carreteras interconectadas

INTEGRACIÓN CAMINERA

49

INVERSIÓN EN CONSTRUCCIÓN DE CAMINOS(En millones de dólares)

Chile

Projects Investment amount (e)

ROADS AND BRIDGES 1,637

Corridor I: East - West (Bolivia, Brasil and Chile)- San Matías - Concepción (paving) 292

Corridor III: West - North - Yucumo - San Borja 24 - Guayaramerín - San Javier 18 - Guayaramerín - San Javier 285 - Porvenir - El Choro 162

Paved roads- Guayanamerin - Cachuela Esperanza road (Pando) 20- Uyuni - Hito LX road (Potosí) 153- San Juan - Laguna Colorada road (Potosí) 117- Pando paved road, connecting to Brazil 250- Puerto Ustarez - Rodonia (Brasil) and other roads (Beni) 163

Strategic bridge for regional integration: 6.160 m 154

CORREDORES VIALES

Corredor 1. Este – Oeste (Bolivia, Brasil y Chile) 910 Km

Corredor 2. Norte – Sud (Puerto Ustáriz - Yacuiba) 128 Km

Corredor 3. Oeste – Norte (La Paz-Riberalta-Guayaramerín-Cobija) 1.617 Km

Corredor 4. Oeste – Sud (La Paz -Bermejo-Villazón) 329 Km

Corredor 5. Este – Oeste (Central-Sud) (Chile, Bolivia y Paraguay) 209 Km

Carreteras existentes

Programa de gobierno

Villa Tunari – San Ignacio de Moxos295 Km

Perú

Brazil

ParaguayChile

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

50

Carreteras integradas

INTEGRACIÓN CAMINERA

Red Ferrocarrilera Oriental(Existente)

Programa de gobiernoRed Ferrocarrilera del Oeste(Zona de interconexión)

Ayquile

Warnes

Vía férrea propuestaPrograma de gobierno

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

51

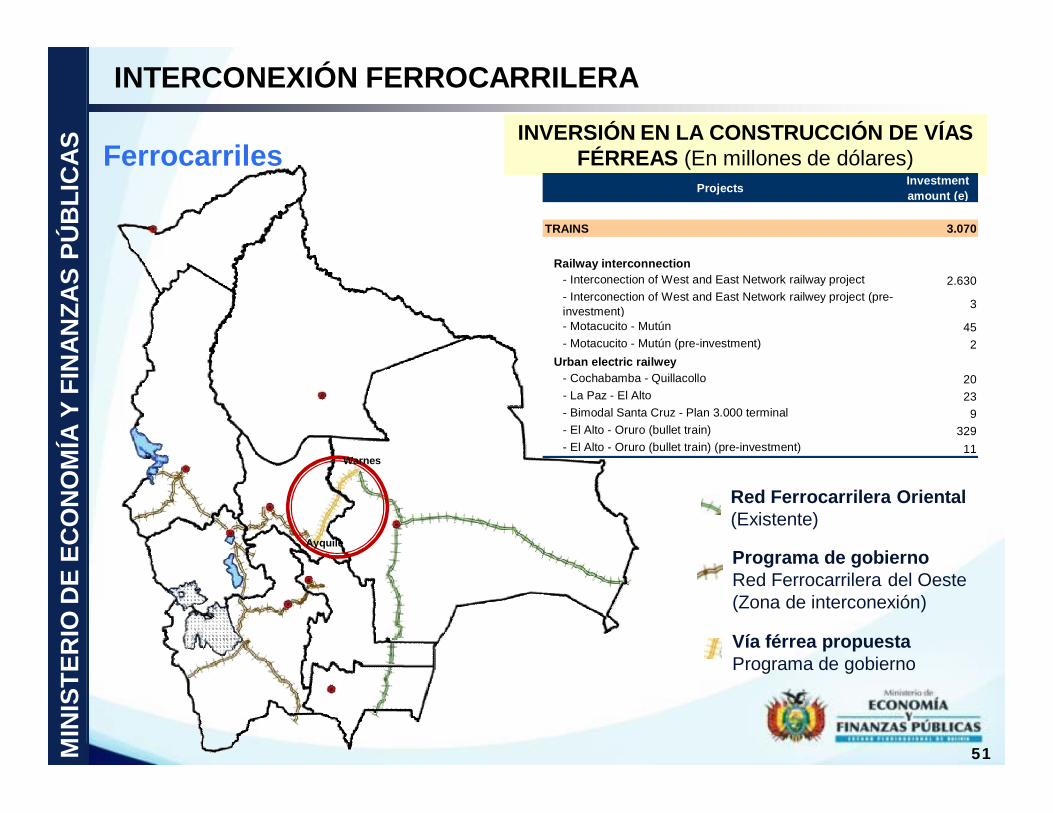

Ferrocarriles

INTERCONEXIÓN FERROCARRILERA

INVERSIÓN EN LA CONSTRUCCIÓN DE VÍAS FÉRREAS (En millones de dólares)

Projects Investment amount (e)

TRAINS 3.070

Railway interconnection- Interconection of West and East Network railway project 2.630- Interconection of West and East Network railwey project (pre-investment) 3

- Motacucito - Mutún 45- Motacucito - Mutún (pre-investment) 2

Urban electric railwey- Cochabamba - Quillacollo 20- La Paz - El Alto 23- Bimodal Santa Cruz - Plan 3.000 terminal 9- El Alto - Oruro (bullet train) 329- El Alto - Oruro (bullet train) (pre-investment) 11

Carretera pavimentada (ESM, JSB y ABC)Puerto Suárez – Mutún – Puerto Busch

Vía férrea Puerto Suárez – Mutún – Puerto Busch

Vía fluvial Mutún – Río Paraguay (Dionisio Foianini)

Vía FluvialMutún – Puerto Busch: 110 KmPuerto Busch – Puerto Nueva Palmira: 2.000 KmTOTAL: 2.110 Km aprox.

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚB

LIC

AS

52

Vía fluvial Mutún – Puerto Busch

BOLIVIA: CONECTADA AL ATLÁNTICO

VÍA FLUVIAL MUTÚN – PUERTO BUSCHMonto de inversión (e):USD 450 millions

MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y FI

NAN

ZAS

PÚB

LIC

AS

TRIGO (Hectáreas)

Producción potencial de trigo

DESARROLLO RURAL

53

INVERSIÓN EN DESARROLLO RURAL Y SEGURIDAD ALIMENTARIA

(En millones de dólares)Projects Investment

amount (e)

RURAL DEVELOPMENT 256

Secure agricultural production- Inorganic fertilizers production 6- Universal Agricultural Insurance 60- III National Agricultural Census 14

Food fair price- National Food Security Plan 10- National wheat production program 8- EMAPA 9- Greenhouses 21- Promote agricultural production capacities for food security program (INIAF) 31

- Milk production and beef encourage program 7Agroecological production

- Organic fertilizers production 7- CRIAR (Rural Food Initiatives Creation) consolidation

30

- EMPODERAR (Rural Development self managed organized enterprise) consolidation

10

- Ecological production national programme 7Early warning to agricultural sector (Risk management)

3

- Rural contingency national plan (Agriculture component) for risk management

5

- SUSTENTAR, Sustainable forestry program 7- Sugar cane production - San Buenaventura 21

MODELO ECONOMICOPLURINACIONAL PRODUCTIVO

Datos importantes para el ANALISS

Fuente: LUIS ALBERTO ARCE CATACORAMINISTER OF ECONOMY AND PUBLIC FINANCES

Elaborated: Ministry of Economy and Public Finances, Fiscal Analysis Network (RAF)Lats update: Tuesday, april 13 2010 (Hrs. 19:18)

Reconocimiento internacional …International Organisms

55MIN

ISTE

RIO

DE

ECO

NO

MÍA

Y F

INAN

ZAS

PÚBL

ICAS FMI: “Regional Economic Outlook: Western Hemisphere"

presentation in Bolivia, and Article IV Consultation. The IMF described as prudent and wise the economic policy implemented in the country, for the fiscal stimulus applied in the crisis period

October, 2009

October 2009 and February 2010

November, 2009

December, 2009

BID: Emphasizes the positive growth in 2009, and the least impact of the crisis in the country, in relation to Latin America and the Caribbean

World Bank: Emphasizes the "appropriate macroeconomic management, and achieving the highest growth rate among countries in Latin America”

CEPAL: Positioned to Bolivia as the fastest growing economy in 2009 and among the principals in 2010

Datos importantes para el ANALISIS del Plan Nacional de Desarrollo 2010-2015

Cinco actividades económicas amenazan las áreas protegidas en el país:

•Hidrocarburos •Caminos - ferroviarios•Madereras •Hidroeléctricas•Mineras

Fuente: Centro de Ecología y Pueblos Andinos (CEPA)

Datos importantes para el ANALISIS del Plan Nacional de Desarrollo 2010-2015

“Precio del estaño rebasó barrera de los 10 dólares la libra fina”

Datos importantes para el ANALISIS del Plan Nacional de Desarrollo 2010-2015

“La onza troyade oro alcanzó los 1300 dólares, lo que permite adelantar el incremento de exportaciones”.director de Minería, Freddy Beltrán

Auge MineroPrecios de los minerales pone optimistas a procesadores de minerales. Fides Potosí, el 20/09/2010

Mediante una licitación nacional e internacional arrancará en noviembre la venta de 20.000 millones de toneladas de minerales acumulados. (A. García Linera – sept. 2010)

Del 2011-2013 se comenzará a vender materia prima de minerales extraída con la nueva maquinaria en grandes cantidades, de 80 a 120.000 y 300.000 toneladas año. (A. García Linera – sept. 2010)

La plata fue el mayor aportante a los ingresos de los departamentos productores de minerales. Subió su precio a 20,91 dólares la onza troy

“La minería está pasando por su mejor

momento, debido a los altos precios de los

minerales en el mercado

internacional, especialmente del

estaño, oro y otros”.

Una cifra cercana a los US$ 50 millones invertirá minera Hochschild Miningen su plan de exploración de 2011, el cual prevé el desarrollo de nuevos proyectos.

Datos importantes para el ANALISIS del Plan Nacional de Desarrollo 2010-2015

Empresas estatales y privadas de España, Estados Unidos, Brasil, Francia, Rusia, China, Japón, Corea del Sur, Finlandia y Canadá han expresado al Gobierno de Evo Morales su interés en desarrollar proyectos mineros en Bolivia (La Prensa 21 de sept. 2010)

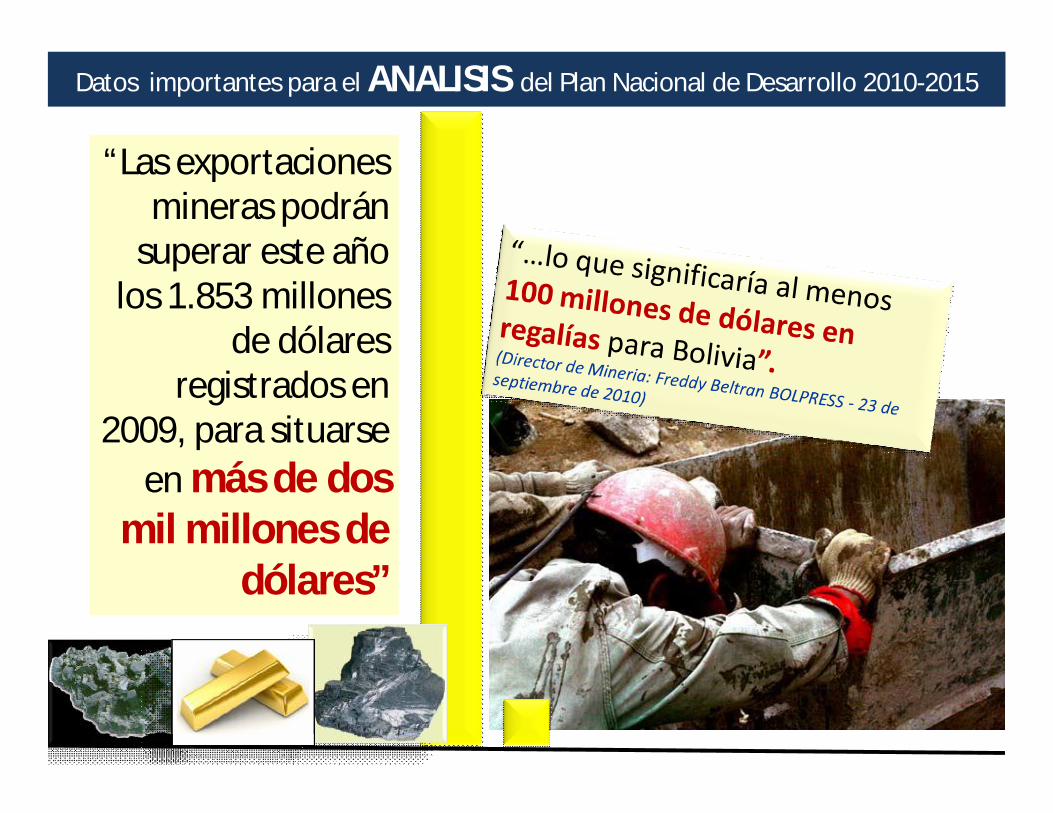

Datos importantes para el ANALISIS del Plan Nacional de Desarrollo 2010-2015

“Las exportaciones mineras podrán

superar este año los 1.853 millones

de dólares registrados en

2009, para situarse en más de dos

mil millones de dólares”

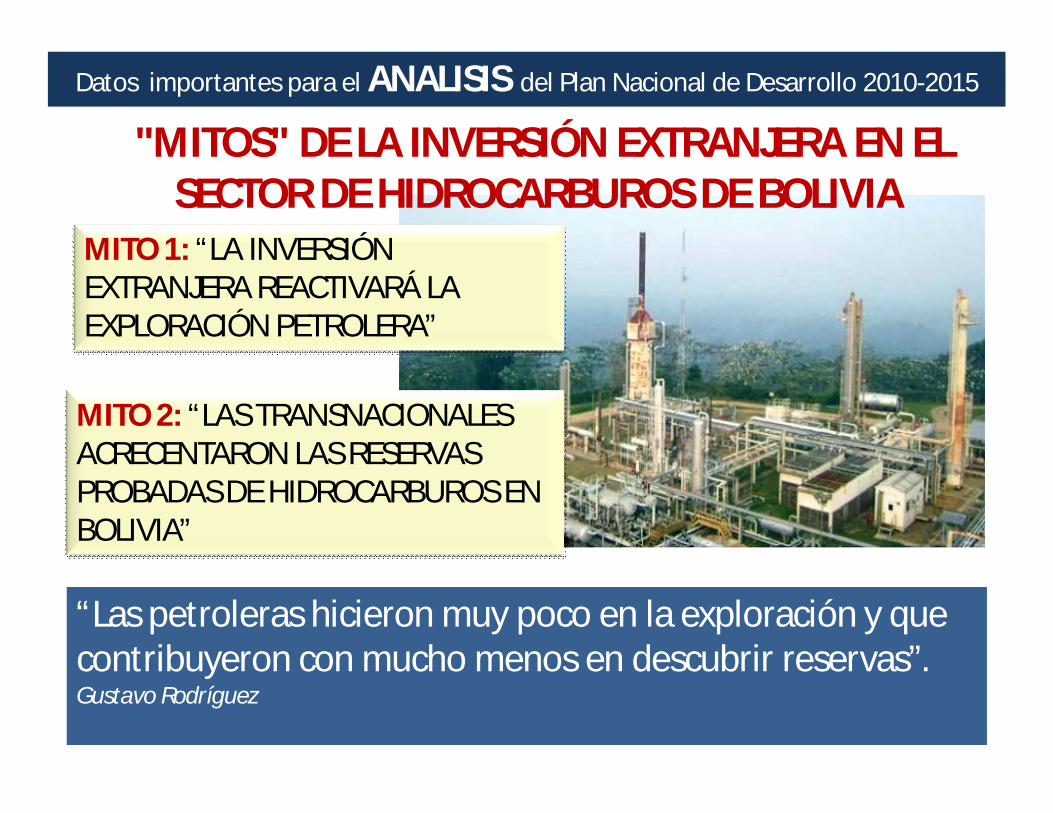

Datos importantes para el ANALISIS del Plan Nacional de Desarrollo 2010-2015

"MITOS" DE LA INVERSIÓN EXTRANJERA EN EL SECTOR DE HIDROCARBUROS DE BOLIVIA

MITO 1: “LA INVERSIÓN EXTRANJERA REACTIVARÁ LA EXPLORACIÓN PETROLERA”

MITO 2: “LAS TRANSNACIONALES ACRECENTARON LAS RESERVAS PROBADAS DE HIDROCARBUROS EN BOLIVIA”

“Las petroleras hicieron muy poco en la exploración y que contribuyeron con mucho menos en descubrir reservas”.Gustavo Rodríguez

Top Related