Savvy grey presentation v3

26

SavvyGrey.com by ROC Insurance Services Medicare, Social Security, and Retirement

-

Upload

rickgmann -

Category

Healthcare

-

view

212 -

download

0

Transcript of Savvy grey presentation v3

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Medicare, Social Security,and Retirement

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

are the foundation of a successful retirement.

&Good health Financial

stability

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Medicare and Social Security will play a big role your retirement future.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

10,000 new Medicare subscribers per day

for 20 years

What the future holds:

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

78 Million Boomers retiring will overload Medicare

and Social Security

What the future holds:

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

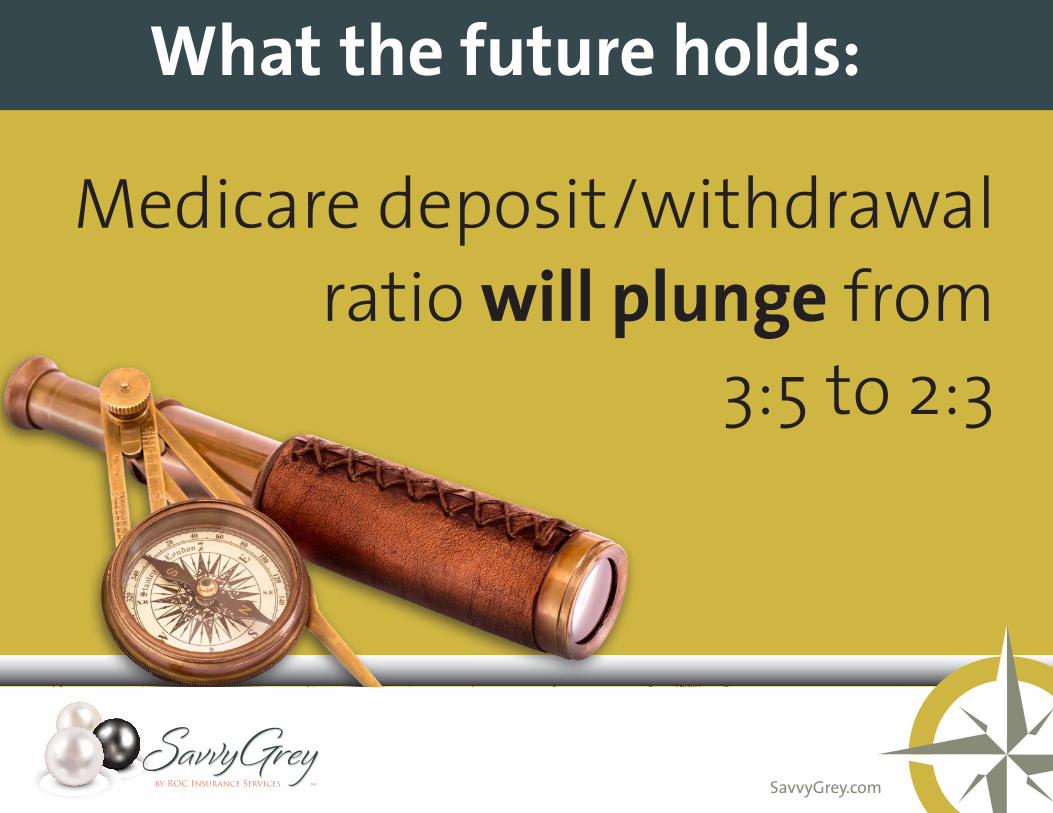

Medicare deposit/withdrawal ratio will plunge from

3:5 to 2:3

What the future holds:

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Reduced benefits and increased premiums

are expected

What the future holds:

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Healthcare will be 33% of your total expenditures

post-retirement

What the future holds:

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Boomers will bear financial responsibility for

aging parents (and unemployed children)

What the future holds:

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Medicare

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Medicare is

not free.

And the Affordable Care Act will not cover you after age 65.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

If you don’t enroll, you are likely to experience:• Late-enrollment penalties• Health care expenses that may not be covered• Private insurance options that may be limited

Enrolling in Medicare at 65 is extremely important.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Enrolling in the wrong program

means you could be paying too much and

not getting the coverage you need.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Social Security

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

You've contributed to it.

Prepare to claim it.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

It's an integral part of your income in planning

for retirement.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

It's the first big decision you will

face as you transition into

retirement.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Key factors:• Age• Desire to keep working,

even part-time• Marital status

(married, divorced, widowed, etc.)

Knowing how you

best qualify makes a big difference.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Calculating your benefit and when to claim to get

the maximum payout isn't obvious.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Knowing when and how to claim spousal benefits

will maximize payout as well.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Medicare and Social Security are complex programs. The wrong decision can have

serious financial consequences:fines, loss of benefits, and loss of income.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

You don't have to go it alone.

We're here to help.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

We provide depth of experience and full understanding of the complex Medicare and Social Security rules

to put your mind at ease.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

With a thorough review of your history we develop a solid plan that will maximize your benefits and minimize your costs.

Important Information

Scope of this Report

This report provides broad, general guidelines and strategies which may help you define your retirement income

needs. This report is provided for educational purposes only and you should not rely on it as the primary basis for

your insurance, investment, financial, retirement or tax planning decisions.

Assumptions of this Report

No serious health changes

The Healthcare cost inflation rates vary depending on the specific expense

Expense amounts shown for under age 65 assume 100% client responsibility for private health insurance

costs. Amounts for age 65 and older assume coverage by Medicare Parts A, B, D, and supplemental

insurance (MediGap).

The disease states are assumed to be separate and distinct for purposes of estimating healthcare costs.

The information presented in the Annual Investment and Healthcare Expense Summary is hypothetical and is

not intended to serve as a projection or prediction of the investment results of any specific investment.

Limitation of this Report

The algorithms used in developing this HealthView Report evaluate an individual's health and create health and

financial assumptions for future health and healthcare needs. The HealthView Report considers national health

standards, healthcare costs, medical coverage, healthcare inflation rates, progress in certain areas of medical

research, and actuarial data including medical, dental and pharmacy cost models. The estimated average annual

out-of-pocket medical expenses were developed in part using typical Commercial Preferred Provider Plans

("PPO") and Medicare plan designs (including pharmacy) for males and females. Neither HealthView Services, its

affiliates, agents, or representatives have verified or confirmed the accuracy of these guidelines, assumptions or

estimated costs. Annual costs are future values as of the year of attained age. Average Annual Costs are the

average annual future costs for the stated 5-year period. These are estimated costs, they are hypothetical in

nature, and are not guaranteed. Your actual medical costs will likely vary (sometimes significantly) from the

estimates in this report. Your current and future decisions and actions should not depend on, or be based solely

on, the results generated by this HealthView Report. It is important that you periodically monitor their retirement

income and expense strategy throughout retirement.

The HealthView Report is dependent upon the quality and accuracy of the data furnished by you or unaffiliated

third parties, including information about your health status as well as certain assumptions as to future inflation

rates and future healthcare costs.

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 9 of 9

Terms & Definitions

Health Conditions

Cancer — Also called malignancy, is characte

rized by an abnormal growth of cell

s. There are more than 100

types of cancer, including breast cancer, skin cancer, lung cancer, colon cancer, prostate cancer, and lymphoma.

Cancer symptoms vary widely based on the type of cancer.

Cardiovascular disease — A disease affecting the heart or bloo

d vessels. Some conditions that fall under the

umbrella of cardiovascular disease are aneurysm, angina, arrhythmia, cardiomyopathy, congenital cardiovascular

defects, congenital heart disease, congestive heart failure, heart attack, diseases of pulmonary circulation,

endocarditis, rheumatic fever, stroke, heart valve disease, diseases of the circulatory system.

High blood pressure — (Hypertension) Blood pressure rea

dings are measured in millimeters of mercury (mmHg)

and usually given as two numbers -- for example, 120 over 80 (written as 120/80 mmHg). One or both of these

numbers can be too high. The top number is your systolic pressure. It is considered high if it is over 140 most of

the time. It is considered normal if it is below 120 most of the time. The bottom number is your diastolic pressure.

It is considered high if it is over 90 most of the time. It is considered normal if it is below 80 most of the time.

High cholesterol — The presence of high levels of cho

lesterol in the blood. It is not a disease but a metabolic

derangement that can be secondary to many diseases and can contribute to many forms of disease, most notably

cardiovascular disease. Primarily caused by diet and family history high cholesterol is defined as a measurement

greater than 200 mg/dL. LDL cholesterol levels greater than 130 mg/dL and HDL cholesterol levels less than 60

mg/dL are considered high.

Type 2 diabetes — Formerly called non insulin depend

ent diabetes mellitus (NIDDM). Typ

e 2 Diabetes (or adult-

onset diabetes) is a disorder that is characterized by high blood glucose in the context of insulin resistance and

relative insulin deficiency.

Tobacco user — User of tobacco in any form (cigare

ttes, cigars, pipes, etc.) on a consis

tent basis within the last

5 years.

Medicare Terms

Medicare Part A —Hospital insurance that helps cover i

npatient care in hospitals, skilled nursing facility, hospice,

and some home healthcare. Most people eligible for Medicare do not pay a premium for Part A.

Medicare Part B — Helps cover medically necessary s

ervices like doctors’ services, outpa

tient care, some home

health services, some preventive care, and some medical services and equipment. Part B subscribers pay a

higher premium based on income.

Medicare Supplemental Insurance (MediGap) — Medicare Supplemental Insurance

policies fill in the gaps that

Medicare Parts A & B do not cover. This report assumes premiums for Medigap Plan C and uses the average

cost for this plan in the subscriber’s

state of residence.

Medicare Part D — Prescription drug coverage that is p

urchased through private insurance

companies who have

been approved by Medicare to sell drug coverage. Part D policy costs and coverage vary by insurer, state, and

plan. Part D subscribers pay a higher premium based on income.

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 8 of 9

Cost of Waiting

Action Plan

Sample

Here’s what steps you need to take

to get the most out of your Medica

re benefits.

Sign Up For Medicare

Sample needs to sign up for Medicare Part A (hospitalization coverage) in 2019 when he turns 65. You can enroll

in Medicare as early as 3 months before your 65th birthday. This can be done online at www.medicare.gov

Remember, if you are working for a company with < 20 employees, you must also sign up for Medicare Part B

(doctors and tests), because even though you may still have health coverage through your employer, Medicare will

become the “primary payor” and yo

ur health plan becomes a “secondar

y payor”.

And don’t forget to sign up for Part D

(prescription drugs). If your employe

r’s plan covers prescriptions, you do

n’t

need to do this until you stop workin

g and are no longer covered by you

r employer’s plan. You will purchase Part

D coverage through a private insurance company; you can start your search for the best plan at

https://www.medicare.gov/find-a-plan/questions/home.aspx

Cost of Waiting

$269,259

$373,260

$490,988

Toda

y Year

3 Year

5

0k

200k

400k

600k

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 7 of 9

Annual Investment and Healthcare Expense Summary

Allocated IncomeInvestment Accumulation & Expense Distribution

Year/AgePart B SS

Deduction*

AddtionalSS

Allocation

AdditionalAllocated

Income

AnnualHealthcareExpenses

AnnualShortfall

BeginningValue

HealthcarePayment Contributions

AssumedRate ofReturn

Return onInvestment

EndingValue

2014 (Age 60)$9,600

$269,2596.00% $18,106 $285,415

2015 (Age 61)$9,792

$285,4156.00% $19,062 $302,540

2016 (Age 62)$9,988

$302,5406.00% $20,102 $320,692

2017 (Age 63)$10,188

$320,6926.00% $21,203 $339,934

2018 (Age 64)$10,391

$339,9346.00% $22,370 $360,330

2019 (Age 65) $1,613 $9,793 $22,500 $6,872 $360,3306.00% $23,339 $381,950

2020 (Age 66) $1,702 $9,960 $22,500 $7,403 $381,9505.00% $20,521 $401,047

2021 (Age 67) $1,800 $10,127 $22,500 $7,967 $401,0475.00% $21,465 $421,099

2022 (Age 68) $1,926 $10,285 $22,500 $8,593 $421,0995.00% $22,457 $442,154

2023 (Age 69) $2,032 $10,457 $22,500 $9,233 $442,1545.00% $23,497 $464,262

2024 (Age 70) $2,144 $10,631 $22,500 $9,914 $464,2625.00% $24,588 $487,475

2025 (Age 71) $2,262 $10,806 $22,500 $10,641 $487,4755.00% $25,733 $511,849

2026 (Age 72) $2,386 $10,982 $22,500 $11,412 $511,8495.00% $26,935 $537,442

2027 (Age 73) $2,517 $11,160 $22,500 $12,240 $537,4425.00% $28,195 $564,314

2028 (Age 74) $2,656 $11,339 $22,500 $13,121 $564,3145.00% $29,517 $592,529

2029 (Age 75) $2,802 $11,519 $22,500 $14,057 $592,5295.00% $30,905 $622,156

2030 (Age 76) $2,956 $11,701 $22,500 $15,054 $622,1564.00% $25,889 $647,042

2031 (Age 77) $3,118 $11,883 $22,500 $16,117 $647,0424.00% $26,862 $672,924

2032 (Age 78) $3,290 $12,066 $22,500 $17,210 $672,9244.00% $27,874 $699,841

2033 (Age 79) $3,471 $12,250 $22,500 $18,375 $699,8414.00% $28,926 $727,834

2034 (Age 80) $3,662 $12,434 $22,500 $19,613 $727,8344.00% $30,019 $756,948

2035 (Age 81) $3,863 $12,619 $22,500 $20,759 $756,9484.00% $31,161 $787,225

2036 (Age 82) $4,076 $12,804 $22,500 $21,971 $787,2254.00% $32,348 $818,714

2037 (Age 83) $4,300 $12,988 $22,500 $311,152 ($271,364) $818,714 $271,3644.00% $22,066 $569,244

2038 (Age 84) $4,536 $13,173 $22,500 $324,040 ($283,831) $569,244 $283,8314.00% $11,598 $296,830

2039 (Age 85) $4,786 $13,357 $22,500 $337,472 ($296,830) $296,830 $296,8304.00% $191 $0

* Part B Medicare premium is automatically deducted from Social Security

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 6 of 9

Healthcare and Long-Term Care Funding Options

The income and investment contributions that you have designated to fund your healthcare and Long-term Care

costs are shown in the table below

Client Contribution Value Unfunded HC Costs

Total Healthcare and Long-term Care Expense

$1,213,218

From Future Income

Medicare Part B Deduction from Social Security $61,895 $61,895 $1,151,323

Additional Social Security$212,891 $230,900 $920,423

Pension

$0$0

$920,423

Other Income

$86,407 $116,671 $803,752

From Investments Using Rates Shown Below

Working In Retirement$0

$0$803,752

Other Investments$0

$0$803,752

You have chosen to fund your remaining Healthcare and Long-Term Care expense of $803,752 with a single

investment of $269,259 as shown below.

Selected Option For Unfunded Amount

Single Investment$269,259 $803,752 $0.00

RateAssumptionsPeriod Covered

% Rate of Return

Phase 1Through Age 2019 (Age 65)

6.00%

Phase 2Through Age 2029 (Age 75)

5.00%

Phase 3Through Rest of Life Expectancy

4.00%

Funding Sources

Unfunded

Sample Social Security

PensionInvestments

Part B

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 5 of 9

Long-term Care Options

Type of Care:Skilled Nursing

Region:NY - Rochester

Period:36 months

Assumed Inflation: 4.0%

Long Term Care Cost Summary

Today's cost: $116,800 per year.

Based on your options and planning horizon, costs are

projected below.

Projected long-term care costs

Year/AgeProjected Cost (Future Dollars) Projected Cost (Today's Dollars)

2037 (Age 83)$287,879

$145,866

2038 (Age 84)$299,394

$147,282

2039 (Age 85)$311,370

$148,712

Total$898,643

$441,860

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 4 of 9

Healthcare Expense Breakdown

The following chart illustrates the breakdown of projected healthcare expenses in retirement. Amounts are

expressed in future dollars.

Average Annual Healthcare Expenses per 5 Year Period

This chart shows your average estimated annual healthcare expenses for each 5-year period in retirement.

Amounts are expressed in future dollars.

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 3 of 9

YesNoNoNoNoNoYesYesYesNo

This is your personal retirement healthcare expense report, designed to estimate your health care expenses

throughout retirement. These calculations are the work of a coordinated team of professionals, including leading

physicians and actuaries utilizing proprietary health and lifestyle analytical tools.

Questionnaire

Below are your responses to the HealthView Questionnaire.Sample

Gender

Male

Age in 2014

60

Retirement

2019-2039Ages 65-85 (21 years)

Health & Lifestyle

High blood pressure:

High cholesterol:Type 2 diabetes:Cardiovascular disease:

Cancer:Tobacco user:Recent physical:2 hours exercise:Healthy diet:Family history:

State

NY

Income Level

Individual - $85,000 or less

Healthcare Expense Summary

Here is a summary of your projected healthcare expenses. Amounts are expressed in future dollars.

Sample

Premium Costs

Hospitals, Doctors, Tests

$61,895

Prescription Drugs

$32,191

Supplemental Insurance

$95,680

Dental Insurance

$18,167

Additional Costs

Hospitals, Doctors, Tests

not included

Prescription Drugs

$16,046

Hearing & Vision

$79,207

Dental

$11,389

Total Healthcare Costs

$314,575

Long-term Care

$898,643

Total Healthcare & Long-term Care Costs

$1,213,218

Your Personal Healthcare Expense Report

Prepared for Sample

by Rick Grossmann of ROC Insurance Services

Page 2 of 9

Healthcare Report

Prepared for Sample

By Rick Grossmann

Monday, May 19, 2014

Contact Number: 585-413-0483

Page 1 of 9

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

The SavvyGrey approach makes it easy to understand your options to

make the best choices so you can enjoy your retirement.

SavvyGrey.comby ROC Insurance Services

by ROC Insurance Services

Contact us today for an information overview:

Phone (585) 413-0483

Email [email protected]

Web www.SavvyGrey.com