Decide. Create. Share. - aarp.org · turales, empleo relacionado con sus raíces mexicanas. Cruz...

12

AARP.ORG/VIVA AARP VIVA 1 Decidir . Crear . Compartir. TOME EL CONTROL DE SU FUTURO ¿ESTÁ PREPARADA PARA EL FUTURO? Imagine sus días plenos de tran- quilidad y seguridad. Si es como la mayoría de las mujeres, seguro que presta más atención a su familia que a sus propios planes. Esta guía la ayudará a tra- zar un rumbo en cuatro áreas clave: finanzas, vivienda, temas legales y salud. Decide. Create. Share. TAKE CHARGE OF YOUR FUTURE ARE YOU PREPARED FOR THE FUTURE? Picture your days filled with peace of mind and security. But if you’re like most women, you probably pay more attention to your family than you do to your own long-term plans. This guide helps you plot a course in four critical areas: finance, home, legal and health. VIVA VIVA

Transcript of Decide. Create. Share. - aarp.org · turales, empleo relacionado con sus raíces mexicanas. Cruz...

AARP.ORG/VIVA AARPVIVA 1

Decidir. Crear. Compartir.tome el control de su futuro

¿estÁ PrePArAdA PArA el futuro? Imagine sus días plenos de tran-quilidad y seguridad. Si es como la mayoría de las mujeres, seguro que presta más atención a su familia que a sus propios planes. Esta guía la ayudará a tra-zar un rumbo en cuatro áreas clave: finanzas, vivienda, temas legales y salud.

Decide. Create. Share.tAke chArge of your future

Are you PrePAred for the future? Picture your days filled with peace of mind and security. But if you’re like most women, you probably pay more attention to your family than you do to your own long-term plans. This guide helps you plot a course in four critical areas: finance, home, legal and health.

VIVA

VIVA

2 AARPVIVA OTOÑO/FALL 2011

Decidir. Crear. Compartir.

M y husband, Frank, and I stood in our living room surveying the accumulation of 30 years of marriage, two children, careers, a house-hold of furnishings, books and souvenirs.

We’d just returned from emptying his parents’ house. I turned to him and vowed: “We won’t leave our children

to pick up after us.” Eight years earlier, Frank and his brother, Philip, had

guided their parents, Bill and Rose, through their long-term care plans. A lawyer prepared the documents, but the broth-ers were left with questions no one wants to ask their par-ents: Have you thought about the quality of the rest of your life? Do you have enough money to travel and enjoy other activities? Who should manage your finances? Who should make decisions on your behalf if you’re incapacitated? How much medical intervention are you willing to undergo?

Bill and Rose had two modest homes, a car and a savings account. They sold the house with steep stairs and renovat-ed the smaller one-level home. After their parents’ deaths, Frank and Philip had to decide what to do with the belong-ings collected over a 68-year marriage.

“Should we sell the stamp collection?” asked Frank as he leafed through a book.

M i marido Frank y yo nos paramos en nuestro living evaluando lo que acumulamos durante 30 años de matrimonio: dos hijos, carreras, una casa llena de muebles, libros y recuerdos.

Acabábamos de volver de vaciar la casa de sus padres.Me volví hacia él y juré: “No dejaremos nuestros asuntos a

cargo de nuestros hijos”.Hace ochos años, Frank y su hermano, Philip, guiaron a sus

padres, Bill y Rose, en la preparación de sus planes de cuida-do a largo plazo. Un abogado preparó los documentos, pero los hermanos se quedaron con las preguntas que nadie quiere hacerles a sus padres: ¿Han pensado en la calidad del resto de sus vidas? ¿Tienen suficiente dinero para viajar y disfru-tar de otras actividades? ¿Quién debería manejar sus finan-zas? ¿Quién tomará decisiones si quedan incapacitados? ¿Por cuánta intervención médica están dispuestos a pasar?

Bill y Rose tenían dos casas modestas, un coche y una cuen-ta de ahorros. Vendieron la casa con escaleras empinadas y renovaron la más pequeña de un solo nivel. Tras sus muertes, Frank y Philip tuvieron que decidir qué hacer con las perte-nencias coleccionadas durante un matrimonio de 68 años.

“¿Debemos vender la colección de estampillas?”, pregun-taba Frank mientras hojeaba un libro.

Esmeralda SantiagoAuTORA, cuando era puertorriqueña

En este ensayo, la exitosa escritora reflexiona sobre la jubilación y lo que implica.

Esmeralda SantiagoAuThOR, when i was puerto rican

In this essay, the best-selling author ponders questions on retirement and beyond.

Decide. Create. Share.

InTROducTIOn

InTROduccIón

AARP.ORG/dEcIdE AARPVIVA 3

“¿Qué hacemos con estos álbumes de fotos?”, se pregunta-ba mi cuñada, Anne.

Empaqué la cristalería y las figuras de porcelana para Good will. Como Bill y Rose, deseo estar rodeada de cosas que me traigan recuerdos y me hagan sentir bien.

De regreso a nuestro hogar, recorrí la casa, eligiendo qué guardar, qué regalar y a quién. Mientras trabajo, intento res-ponder las preguntas de Frank y Philip. A medida que enve-jezco, ¿podré seguir utilizando las escaleras hasta la oficina donde escribo? ¿He guardado suficiente dinero para no tener que ser una carga financiera para Frank o para mis hijos?

En un cajón, encuentro mi testamento, escrito a mano y lamentablemente desactualizado. ¿Cómo pude ignorar este documento fundamental? Debería haber actuado mejor.

Mañana dejaré una bolsa llena de ropa en el Ejército de Salvación, y cajas con libros y CDs para la venta de libros de la biblioteca. En la semana, me reuniré con un abogado y un planificador financiero. Estos primeros pasos ayudarán a ali-viar a mis hijos y me guiarán a mi futura independencia. Me produce bienestar este conocimiento y la capacidad de tomar decisiones conscientes que determinarán el resto de mi vida.

En los siguientes perfiles, cuatro mujeres cuentan sus histo-rias y expertos ofrecen sus consejos.

“What do we do with these photo albums?” wondered my sister-in-law Anne.

I packed up the glass and porcelain figurines for Goodwill. Like Bill and Rose, I want to be surrounded by the things that trigger memories and bring me comfort.

Back at home I go through the house, choosing what to keep, what to give away and to whom. While I work, I try to answer Frank’s and Philip’s questions. As I age, will I be able to manage the stairs to my office, where I write? Have I set aside enough money so that I won’t be a financial liability to Frank or my kids?

Inside a drawer I find my will, handwritten and woefully out of date. How could I ignore this crucial document?

Tomorrow I’ll drop off a bag full of clothes at the Salvation Army and boxes with books and CDs for the library book sale. Later this week, I’ll meet with the lawyer and a finan-cial planner.

These first steps will help unburden my children and lead to my future independence. There’s comfort in that knowl-edge, and in the ability to make conscious choices that will determine the rest of my life.

In the profiles that follow, four women tell their stories, and experts offer their advice.

“

”“”

No deja- remos nuestros asuntos a cargo de nuestros hijos.

We won’t leave our children to pick up after us.

ILLusTRATIOns by Jon VAlk PhOTOGRAPhy by DAVe lAuRiDsen

4 AARPVIVA OTOÑO/FALL 2011

Mary Cruz, 56 chuLA VIsTA, cA

Tiene dinero para gastos básicos, pero ¿tendrá sufi-ciente para viajar?

Mary Cruz, 56chuLA VIsTA, cA

She’s got enough money for the basics, but will she have enough to travel?

M ary Cruz didn’t worry about retirement un-til 10 years ago when she divorced, at age 46. Prior to that, her ex-husband had done the financial planning for both of them.

“It never occurred to me that I might be single when I was older,” she says.

She’ll have a pension, Social Security and a 401(k) when she retires from the Sharp Chula Vista Medical Center, where she’s program manager for community and multicultural re-lations, a job that relates to the Mexican side of her family.

She expects her retirement income will cover the basics but wants money to travel and do things with her family. She knows her financial situation is better than most working single women, but she still worries. When she divorced, she took the middle-of-the-road approach to investing: neither conservative nor risky. Back then, retirement was 20 years away. Now she wonders if she should take a second look at her investments. Are they enough?

“It’s time for me to start taking care of myself financially,” she says.

She’d like to have a clearer plan, especially for investing the proceeds of her 401(k) account after she retires. “Should I manage it all myself?”

M ary Cruz no se preocupó por la jubilación hasta hace 10 años, cuando se divorció a los 46. Anteriormente, su exmarido había hecho la planificación financiera para ambos.

“Nunca se me había ocurrido que podría estar soltera cuando llegara a ser mayor”, afirma.

Ella tendrá una pensión, el Seguro Social y un plan 401(k) al jubilarse del Sharp Chula Vista Medical Center, donde es gerente del programa de relaciones comunitarias y multicul-turales, empleo relacionado con sus raíces mexicanas.

Cruz espera que sus ingresos de jubilación cubran los gas-tos básicos, pero quiere viajar y hacer cosas con la familia.

Sabe que su situación financiera es mejor que la de la ma-yoría de las mujeres solteras que trabajan, pero aún así, se preocupa. Cuando se divorció, tomó por la vía del medio al abordar el tema de las inversiones: no muy conservador, pero tampoco muy riesgoso. En ese momento, le faltaban 20 años para jubilarse. Ahora, se pregunta si debería revisar sus inver-siones, que se han ido acumulando, pero ¿serán suficientes?

“Es hora de comenzar a cuidarme financieramente”, dice.Le gustaría tener un plan más claro, especialmente para

invertir los ingresos de su cuenta 401(k) después de que se jubile. “¿Debería administrar todo por mi cuenta?”.

Decidir. Crear. Compartir.

Decide. Create. Share.

AARP.ORG/dEcIdE AARPVIVA 5

PROFILEs by mAuReen west

FInAncE

FInAnzAs

RESOURCES

AArP retirement calculator: A tool to help you plan your financial future so you can retire when—and how—you want to. aarp.org/retirement

calculator national Association of

Personal financial Advisors: Con-sumer tips and tools and a directory of fee-only financial advisors. 847-483-5400 napfa.org/consumer

WIser (Women’s Institute for A secure retirement): Information on preparing for retirement, includ-ing materials on Social Security, pensions, saving and investing. Offers specific information on widowhood and divorce. Some information is available in Spanish. 202-393-5452, wiserwomen.org

Consejo experto

Expert advice

RECURSOS

calculadora para la jubilación de AArP: Una calculadora para ayudar-lo a planificar su futuro financiero y jubilarse cuando y como lo desee. aarp.org/retirementcalculator

national Association of Person-al financial Advisors: Consejos para consumidores, herramientas y un directorio de consultores finan-cieros que cobran por sus servicios. 847-483-5400, napfa.org/consumer

WIser (Women’s Institute for A secure retirement): Informa-ción sobre cómo prepararse para la jubilación, incluído material sobre el Seguro Social, pensiones, ahorro e inversiones. Cierta información está disponible en español. 202-393-5452, wiserwomen.org

PAblo bIAnchIPlanificador financiero certificado Filadelfia, PA

Pablo Bianchi dice que Mary debe sobreponerse a la inercia y desarrollar un plan de jubilación, a partir de ahora. Debería revisar el plan de inversiones que estableció hace una década.

“Lo último que uno querría es despertar a los 78 años, quedarse sin bienes y tener que volver a tra-bajar”, afirma Bianchi. “La plani-ficación financiera no es algo que uno hace una vez y se olvida”.

Bianchi sugiere juntar las fuen-tes de ingreso de su jubilación, y calcular cuánto tendrá y cuánto

necesitará. De haber un déficit, de-berá tomar decisiones duras. Según Bianchi: arme un presupuesto ajus-tado; haga inversiones que poten-cialmente generarán más ganancias sabiendo que añaden riesgos a su cartera; jubílese más tarde o consi-dere trabajar a tiempo parcial cuan-do sea mayor.

Bianchi aconseja que conver-se con dos o tres planificadores financieros certificados. Ubique a alguien que la escuche y se pre-ocupe por ayudarla. Sin embargo, advierte, “huya si alguien comienza a hablarle de hacer transacciones de inmediato”. Contrate a alguien que le haga un plan, no que le venda productos.

PAblo bIAnchI Certified Financial PlannerPhiladelphia, PA

Pablo Bianchi says Mary must overcome the inertia of her situation and actively develop a retirement plan—starting now. She should be-gin by tweaking the investment plan she set up a decade ago.

“The last thing you want to do is to wake up at age 78, running out of assets and needing to go back to work,” Bianchi says. “Financial planning is not something you do once and forget.”

He suggests she pull together her sources of retirement income and estimate the money she’ll have and

how much she’ll need. If there’s a shortfall, she has to make some tough choices now, Bianchi says: Get on a tight budget; take on some investments that potentially will produce higher returns, knowing that they will add risk to your port-folio; retire later or plan on working part-time when she's older.

He suggests she interview two or three certified financial plan-ners. Find a planner who will lis-ten to what she wants to do in her later years, and care about help-ing her. But, he says, “Run away if someone starts talking about do-ing transactions right away.” Hire someone to set up your plan—not to sell you products.

6 AARPVIVA OTOÑO/FALL 2011

Marta Miranda, 57LOuIsVILLE, Ky

¿Puede la casa de sus sue-ños —en el trópico, junto a amigos— volverse realidad?

Marta Miranda, 57LOuIsVILLE, Ky

Can her dream house—in the tropics, living with friends—become a reality?

S ingle for the past five years, Marta Miranda says her retirement dream is to find a house to share with her closest long-term male and fe-male friends, perhaps near a beach in Florida,

in southern Italy or even in affordable Cuba—her family’s homeland—if that becomes politically feasible.

“Three to five people would be ideal, people I love and want to celebrate life with,” says Miranda, president/CEO of the nonprofit Center for Women and Families in Louisville, Kentucky. She imagines a common living room and kitchen with separate bathrooms, bedrooms and perhaps porches. Maybe individual cabanas and a common single-story house.

“I love my private space, but ultimately we’re going to need each other,” she says. “I want a tropical area because snow will be hard on our bones!”

Miranda is close to her family and friends, so the dream house will need to have a guest room. Eventually, they’ll need a room for live-in help.

“If you end up in a retirement community, you are going to end up with strangers,” she says. “That’s not my idea of fun.”

She’s a planner and wonders what to do to make the dream a reality. A few of her good friends are already interested, and they have a wealth of ideas. But where do they start?

E l sueño de Marta Miranda, soltera desde hace cin-co años, es encontrar una casa para compartir con amigos, quizás cerca de una playa en Florida, en el sur de Italia o en la asequible Cuba —la patria de

su familia— de volverse políticamente viable.“Tres o cuatro personas sería lo ideal; personas a las que

quiero y con las que deseo celebrar la vida”, afirma Miranda, presidenta y directora de la organización sin fines de lucro Centro para Mujeres y Familias de Louisville, Kentucky. Ella imagina una sala y cocina en común, con cuartos de baño y dormitorios separados y, tal vez, terrazas. Quizás, cabañas individuales alrededor de una casa de una sola planta.

“Amo mi privacidad, pero a la larga vamos a necesitarnos”, señala. “Quiero una zona tropical ya que la nieve será dura para nuestros huesos”.

Miranda es apegada a su familia y amigos, por lo que la casa soñada deberá tener un cuarto de invitados. Eventual-mente, requerirán una habitación para quien los atienda.

“Si optas por una comunidad para jubilados, terminarás con desconocidos”, dice. “Esa no es mi idea de pasarla bien”.

Miranda es una planificadora y se pregunta cómo conver-tir el sueño en realidad. Algunos de sus amigos ya están inte-resados, y tienen muchas ideas. ¿Por dónde empezar?

Decidir. Crear. Compartir.

Decide. Create. Share.

AARP.ORG/dEcIdE AARPVIVA 7hOmE And cOmmunITy

cAsA y cOmunIdAd

RECURSOS

AArP home design: Listas de verificación, videos, fotos y artículos para ayudarle a orientar su decisión sobre cómo hacer su hogar más seguro y acogedor. aarp.org/homedesign

cohousing Association of the united states: Información sobre comunidades de viviendas compar-tidas y cómo crear una. Incluye ma-terial sobre viviendas compartidas y comunidades universitarias para jubilados. 812-618-2646, cohousing.org

eldercare locator: Servicio públi-co de la Administración de Asuntos sobre la Vejez de EE.UU. con informa-ción para adultos mayores. Incluye reparaciones para el hogar, opciones de vivienda y asistencia legal. 800-677-1116, n4a.org/enespanol

RESOURCES

AArP home design: Checklists, videos, photos and stories that can help guide your decisions about how to make your home more safe and comfortable. aarp.org/homedesign

cohousing Association of the united states: Information on finding cohousing communities or creating your own. Incudes materials on senior cohousing and on univer-sity-based retirement communities. 812-618-2646, cohousing.org

eldercare locator: A public ser-vice of the U.S. Administration on Aging connecting you to resources for older adults and their families. Includes home repair, housing op-tions and legal assistance. 800-677-1116,

www.eldercare.gov

tIm cIsnerosCisneros Design Studio ArquitectosHouston, TX

Tim Cisneros ha diseñado vi-viendas compartidas para jubila-dos. Según él, Miranda y sus amigos deberían pensar en qué los hace sentir cómodos, y ver si las piezas del rompecabezas encajan.

“Va más allá de la arquitectura”, señala, “hay asuntos psicológicos y, a veces, legales”. Limitarse a tres o cinco personas es bueno. “Con un número impar, no habrá empates en las votaciones. Sin embargo, tres po-dría ser más manejable que cinco”.

Cisneros sugiere crear un arreglo

parecido a una sociedad, una com-pañía de responsabilidad limitada (o LLC, por sus siglas en inglés), o algo similar, y fijar reglas para evi-tar conflictos si se necesita renovar, o si alguien se va de la casa y hay que decidir si será o no reemplaza-do. (Hay libros y una asociación de viviendas compartidas y conferen-cias sobre el tema).

Cisneros está de acuerdo en que habrá oportunidades de jubilarse en Cuba, cuando este país lo permi-ta, aunque cuánto tiempo demore es incierto.

Para comenzar, Cisneros reco-mienda que el núcleo del grupo escriba sus deseos, y estudie las lec-ciones que otros ya aprendieron.

Consejo experto

tIm cIsnerosCisneros Design Studio, ArchitectsHouston, TX

Tim Cisneros has designed sev-eral shared retirement houses. Miranda and her friends, he says, should think about what makes them comfortable, and then see if all the puzzle pieces fit together.

“It goes beyond architecture,” Cisneros says. “There are psycho-logical and sometimes legal issues.”

Limiting it to three to five peo-ple is good: “With an odd number, you won’t have deadlocked votes. Three, however, might be more manageable than five.”

He suggests setting the arrange-ment up as an LLC (limited liabil-ity company) or something similar, and laying out rules to avoid con-flicts when renovations are needed, or if someone leaves and decisions must be made to bring in another person—or not. (There are books and a cohousing association and conferences to help with that.)

Cisneros thinks that there will be retirement opportunities in Cuba when it opens, though the timing is uncertain.

To begin, he recommends the core group of dreamers put down their individual desires on paper and study the cohousing lessons learned by others.

Expert advice

8 AARPVIVA OTOÑO/FALL 2011

Mary Ann Kellam, 56cOPPELL, TX

Sabe que un testamento —con el cual cuenta— no es suficiente. Pero ¿qué más necesita?

Mary Ann Kellam, 56cOPPELL, TX

She knows a will—which she has—isn’t enough. But what else does she need?

F inancial planner Mary Ann Kellam has her finan-cial house in order for retirement, but her expe-rience with her father’s and mother’s last days have her wondering if the same can be said for

her own legal planning.With her five sisters, she helped her mother in her strug-

gle with Alzheimer’s disease. Their father died more sud-denly at age 89. The family, of Spanish ancestry, is close, but Kellam learned during that time that a simple last will and testament is hardly enough.

She takes care of her health and her mind—she solves crossword puzzles and makes jewelry to keep sharp. She’s completed a will and wants to prepare an advance directive for medical decisions.

Perhaps, like those who choose their clothes in the morning thinking they might be seen later in an emergen-cy room, she’d like the comfort of knowing all her legal i’s are fully dotted. She’d like a list of documents that will make it easier toward the end, not only on herself but on her husband and only son.

Her five sisters say they would help in her old age, but there’s an 18-year span among them, with four sisters who are older and only one younger.

L a planificadora financiera Mary Ann Kellam tiene sus asuntos financieros en orden para cuando se jubile, pero la experiencia vivida durante los últi-mos días de su padre y madre la hace preguntarse

si se podrá decir lo mismo de su propia planificación legal.Con sus cinco hermanas, ayudó a su mamá a luchar contra

la enfermedad de Alzheimer. Su padre murió de forma más repentina a los 89 años. La familia, de ancestros españoles, es unida, pero en ese tiempo aprendió que una simple declara-ción de los últimos deseos y un testamento no son suficientes.

Kellam cuida de su salud y de su mente —resuelve cruci-gramas y hace joyería para mantener la agudeza mental—. Ha completado un testamento y desea preparar directivas anticipadas para decisiones médicas. Tal vez, como aquellos que eligen la ropa en la mañana pensando que más tarde po-drían ser vistos en una sala de emergencias, le gustaría tener la tranquilidad de saber que todos sus documentos legales están en orden. Quisiera contar con una lista de documentos que hagan las cosas más fáciles hacia el final, no sólo para ella, sino también para su marido y para su único hijo.

Sus cinco hermanas dicen que la ayudarán en la vejez, pero hay una diferencia de 18 años entre ellas, y sólo una de las hermanas es más joven.

Decidir. Crear. Compartir.

Decide. Create. Share.

AARP.ORG/dEcIdE AARPVIVA 9LEGAL

LEGALEs

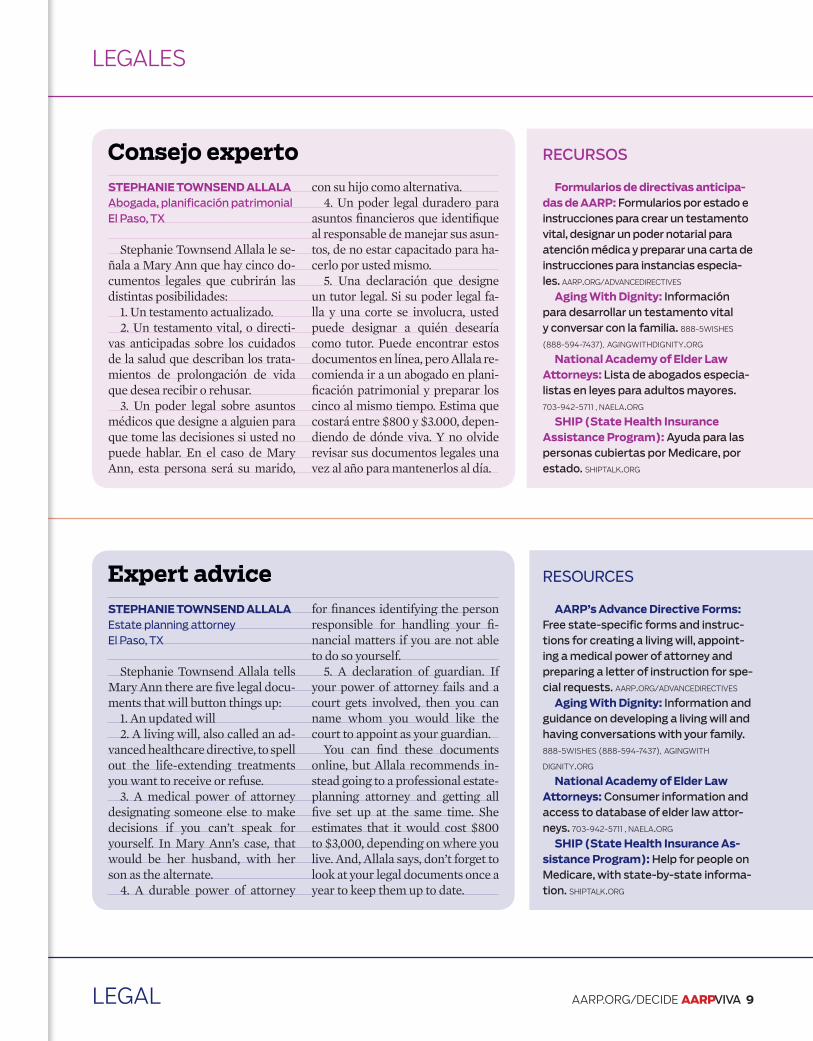

RECURSOS

formularios de directivas anticipa-das de AArP: Formularios por estado e instrucciones para crear un testamento vital, designar un poder notarial para atención médica y preparar una carta de instrucciones para instancias especia-les. aarp.org/advancedirectives

Aging With dignity: Información para desarrollar un testamento vital y conversar con la familia. 888-5wishes

(888-594-7437), agingwithdignity.org

national Academy of elder law Attorneys: Lista de abogados especia-listas en leyes para adultos mayores. 703-942-5711 , naela.org

shIP (state health Insurance Assistance Program): Ayuda para las personas cubiertas por Medicare, por estado. shiptalk.org

stePhAnIe toWnsend AllAlA Abogada, planificación patrimonial El Paso, TX

Stephanie Townsend Allala le se-ñala a Mary Ann que hay cinco do-cumentos legales que cubrirán las distintas posibilidades:

1. Un testamento actualizado.2. Un testamento vital, o directi-

vas anticipadas sobre los cuidados de la salud que describan los trata-mientos de prolongación de vida que desea recibir o rehusar.

3. Un poder legal sobre asuntos médicos que designe a alguien para que tome las decisiones si usted no puede hablar. En el caso de Mary Ann, esta persona será su marido,

con su hijo como alternativa. 4. Un poder legal duradero para

asuntos financieros que identifique al responsable de manejar sus asun-tos, de no estar capacitado para ha-cerlo por usted mismo.

5. Una declaración que designe un tutor legal. Si su poder legal fa-lla y una corte se involucra, usted puede designar a quién desearía como tutor. Puede encontrar estos documentos en línea, pero Allala re-comienda ir a un abogado en plani-ficación patrimonial y preparar los cinco al mismo tiempo. Estima que costará entre $800 y $3.000, depen-diendo de dónde viva. Y no olvide revisar sus documentos legales una vez al año para mantenerlos al día.

rESourCES

AArP’s Advance directive forms: Free state-specific forms and instruc-tions for creating a living will, appoint-ing a medical power of attorney and preparing a letter of instruction for spe-cial requests. aarp.org/advancedirectives

Aging With dignity: Information and guidance on developing a living will and having conversations with your family. 888-5wishes (888-594-7437), agingwith

dignity.org

national Academy of elder law Attorneys: Consumer information and access to database of elder law attor-neys. 703-942-5711 , naela.org

shIP (state health Insurance As-sistance Program): Help for people on Medicare, with state-by-state informa-tion. shiptalk.org

stePhAnIe toWnsend AllAlAEstate planning attorneyEl Paso, TX

Stephanie Townsend Allala tells Mary Ann there are five legal docu-ments that will button things up:

1. An updated will2. A living will, also called an ad-

vanced healthcare directive, to spell out the life-extending treatments you want to receive or refuse.

3. A medical power of attorney designating someone else to make decisions if you can’t speak for yourself. In Mary Ann’s case, that would be her husband, with her son as the alternate.

4. A durable power of attorney

for finances identifying the person responsible for handling your fi-nancial matters if you are not able to do so yourself.

5. A declaration of guardian. If your power of attorney fails and a court gets involved, then you can name whom you would like the court to appoint as your guardian.

You can find these documents online, but Allala recommends in-stead going to a professional estate-planning attorney and getting all five set up at the same time. She estimates that it would cost $800 to $3,000, depending on where you live. And, Allala says, don’t forget to look at your legal documents once a year to keep them up to date.

Consejo experto

Expert advice

10 AARPVIVA OTOÑO/FALL 2011

I rma Almirall-Padamsee, the retired director of multi-cultural affairs at the Samuel Johnson School of Grad-uate Management at Cornell University, spends 40 hours a month volunteering with cancer patients. She

talks with new patients and identifies those who need bud-dies. She’s in charge of a boutique that offers cancer patients free bras, wigs and prostheses. Puerto Rican by ancestry and fluent in Spanish, Almirall-Padamsee also translates a health column for one of the doctors.

Those experiences have made her careful about her own health. She takes care of her asthma, high blood pressure and cholesterol through medications and diet. She sees her doctors regularly. She even keeps in her purse a list of the prescriptions that she takes.

Six years ago, Almirall-Padamsee and her husband bought long-term care insurance because their two grown children live far away and the couple doesn’t want to live in a nursing home. The policy gives them some comfort, but she worries she is not seeing the whole post-65 picture.

She wonders: Will she transition from Cornell’s insurance to Medicare? Will she need supplemental insurance? How does their long-term care insurance fit into the scheme? And what other types of insurance should they have in place?

I rma Almirall-Padamsee, directora jubilada de asuntos multiculturales de la Samuel Johnson School of Gra-duate Management de Cornell University, pasa 40 ho-ras al mes realizando trabajo voluntario con pacientes

con cáncer. Habla con los pacientes nuevos e identifica a los que necesitan compañía. Está a cargo de la boutique que ofre-ce a los pacientes sostenes, pelucas y prótesis gratis. Al ser de familia puertorriqueña y hablar español fluido, también tra-duce una columna de salud para uno de los médicos.

Esas experiencias la han hecho más cuidadosa con respec-to a su propia salud. Se cuida del asma, de la presión arterial elevada y del colesterol, con medicamentos y dieta. Consulta a sus médicos con regularidad. Incluso, lleva en su cartera una lista de los medicamentos que toma.

Hace seis años, Almirall-Padamsee y su marido compraron un seguro de cuidados a largo plazo ya que no desean vivir en un hogar de cuidados especiales y sus dos hijos adultos viven lejos. La póliza les brinda cierta seguridad, pero ella se pre-ocupa de no estar viendo el panorama completo de su vida después de los 65. ¿Hará la transición del seguro de Cornell a Medicare? ¿Necesitará un seguro complementario? ¿Cómo se acoplará su seguro de cuidados a largo plazo a su realidad? Y ¿qué otro seguro deberían tener disponible?

Irma Almirall-Padamsee, 61IThAcA, ny

Cuatro años hasta que pueda ingresar en Medicare. ¿Debería hacerlo? ¿Qué más necesita?

Irma Almirall-Padamsee, 61IThAcA, ny

Four years until she can go on Medicare. Should she? What else does she need?

Decidir. Crear. Compartir.

Decide. Create. Share.

AARP.ORG/dEcIdE AARPVIVA 11hEALTh

sALud

RECURSOS

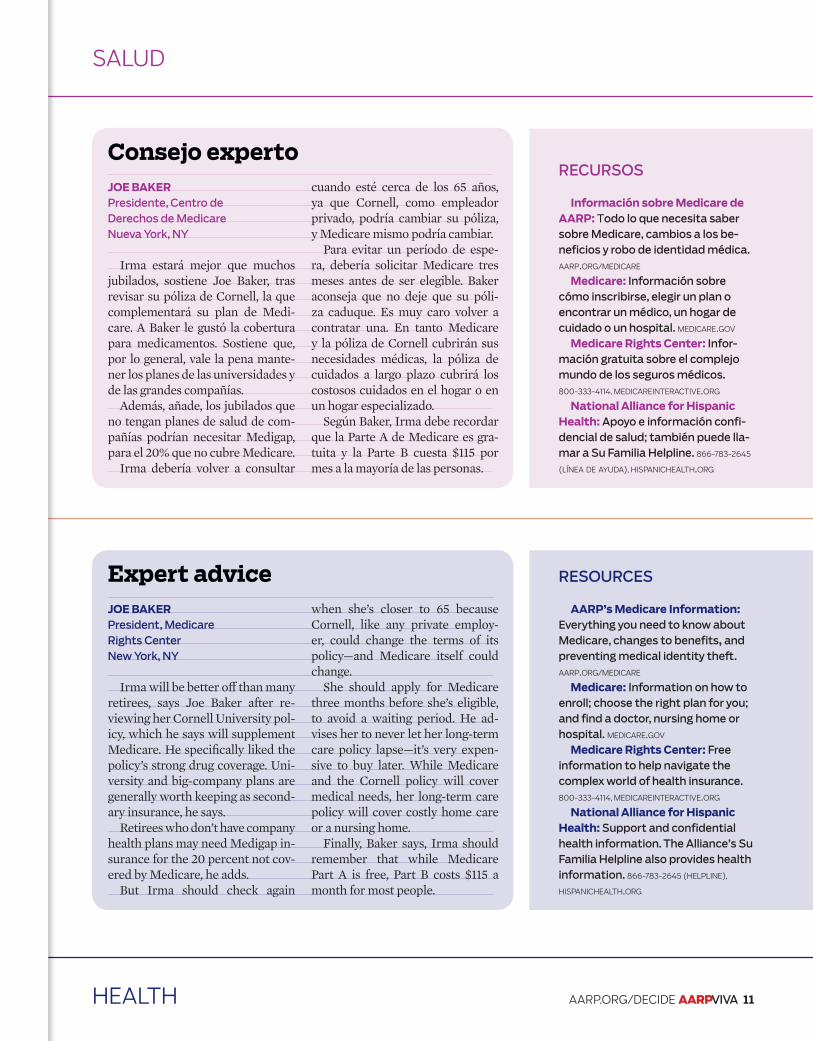

Información sobre medicare de AArP: Todo lo que necesita saber sobre Medicare, cambios a los be-neficios y robo de identidad médica. aarp.org/medicare

medicare: Información sobre cómo inscribirse, elegir un plan o encontrar un médico, un hogar de cuidado o un hospital. medicare.gov

medicare rights center: Infor-mación gratuita sobre el complejo mundo de los seguros médicos. 800-333-4114, medicareinteractive.org

national Alliance for hispanic health: Apoyo e información confi-dencial de salud; también puede lla-mar a Su Familia Helpline. 866-783-2645

(línea de ayuda), hispanichealth.org

Joe bAkerPresidente, Centro de Derechos de MedicareNueva York, NY

Irma estará mejor que muchos jubilados, sostiene Joe Baker, tras revisar su póliza de Cornell, la que complementará su plan de Medi-care. A Baker le gustó la cobertura para medicamentos. Sostiene que, por lo general, vale la pena mante-ner los planes de las universidades y de las grandes compañías.

Además, añade, los jubilados que no tengan planes de salud de com-pañías podrían necesitar Medigap, para el 20% que no cubre Medicare.

Irma debería volver a consultar

cuando esté cerca de los 65 años, ya que Cornell, como empleador privado, podría cambiar su póliza, y Medicare mismo podría cambiar.

Para evitar un período de espe-ra, debería solicitar Medicare tres meses antes de ser elegible. Baker aconseja que no deje que su póli-za caduque. Es muy caro volver a contratar una. En tanto Medicare y la póliza de Cornell cubrirán sus necesidades médicas, la póliza de cuidados a largo plazo cubrirá los costosos cuidados en el hogar o en un hogar especializado.

Según Baker, Irma debe recordar que la Parte A de Medicare es gra-tuita y la Parte B cuesta $115 por mes a la mayoría de las personas.

RESOURCES

AArP’s medicare Information: Everything you need to know about Medicare, changes to benefits, and preventing medical identity theft. aarp.org/medicare

medicare: Information on how to enroll; choose the right plan for you; and find a doctor, nursing home or hospital. medicare.gov

medicare rights center: Free information to help navigate the complex world of health insurance. 800-333-4114, medicareinteractive.org

national Alliance for hispanic health: Support and confidential health information. The Alliance’s Su Familia Helpline also provides health information. 866-783-2645 (helpline),

hispanichealth.org

Joe bAker President, Medicare Rights CenterNew York, NY

Irma will be better off than many retirees, says Joe Baker after re-viewing her Cornell University pol-icy, which he says will supplement Medicare. He specifically liked the policy’s strong drug coverage. Uni-versity and big-company plans are generally worth keeping as second-ary insurance, he says.

Retirees who don’t have company health plans may need Medigap in-surance for the 20 percent not cov-ered by Medicare, he adds.

But Irma should check again

when she’s closer to 65 because Cornell, like any private employ-er, could change the terms of its policy—and Medicare itself could change.

She should apply for Medicare three months before she’s eligible, to avoid a waiting period. He ad-vises her to never let her long-term care policy lapse—it’s very expen-sive to buy later. While Medicare and the Cornell policy will cover medical needs, her long-term care policy will cover costly home care or a nursing home.

Finally, Baker says, Irma should remember that while Medicare Part A is free, Part B costs $115 a month for most people.

Consejo experto

Expert advice

chEcKLIsT

LIsTA dE VERIFIcAcIón

HomeConsider whether you want to stay in your home, move in with family or be in an assisted-living situation.If staying at home, assess current living conditions, taking into account stairs, doorways and other possible obstacles.Consider location. Is your home or chosen community near family, transportation, doctors and a supermarket?

Healthreview health, Medicare and long-term care insurance policies for gaps in coverage.When eligible, sign up for Medicare and any applicable parts (for example, Part D). Keep up with payments on your long-term care policy. It’s very expensive to buy later.

FinanceCalculate retirement financial needs.review and organize current savings, 401(k), pension and other retirement accounts.Develop financial plan. If possible, work with a professional financial planner.

LegalCreate a will or trust.Complete an advance directive, or “living will.”Create medical and durable powers of attorney.

ViviendaPiense si desea permanecer en su hogar, mudarse con familiares u optar por una situación de vida asistida.Si se queda en su hogar, evalúe sus condiciones de vida, considerando escaleras, entradas y otros posibles obstáculos.Piense en la ubicación: ¿Está su hogar cerca de la familia, servicios de transporte, médicos y un supermercado?

Saludrevise las pólizas de sus seguros de salud, Medicare y de cuidados a largo plazo, por si hay brechas en las coberturas. Cuando sea elegible, inscríbase en Medicare y las partes para las que sea elegible (por ejemplo, la Parte D).No deje que su póliza a largo plazo caduque. Es muy caro volver a contratar una.

FinanzasCalcule las necesidades financieras de su jubilación.revise y organice los ahorros actuales, plan 401(k), pensión y otras cuentas de jubilación.Desarrolle un plan financiero. Si es posible, trabaje con un planificador financiero profesional.

Aspectos legalesPrepare un testamento o un fideicomiso.Complete directivas anticipadas o un testamento vital.Firme poderes legales y duraderos con respecto a temas médicos.

© 2011 por AARP. All rights reserved. d19572

for additional resources and information, visitaarp.org/decide

© 2011 por AARP. Todos los derechos reservados. d19572

Para más recursos e información, visiteaarp.org/decide

Decidir. Crear. Compartir.

Decide. Create. Share.