Chapter 14: Money, Banks, and the Federal Reserve...

43

Chapter 14: Money, Banks, and the Federal Reserve System Yulei Luo SEF of HKU March 28, 2016

Transcript of Chapter 14: Money, Banks, and the Federal Reserve...

Chapter 14: Money, Banks, and the FederalReserve System

Yulei Luo

SEF of HKU

March 28, 2016

Learning Objectives

1. De�ne money and discuss its four functions.

2. Discuss the de�nitions of the money supply.

3. Explain how banks create money.

4. Discuss the three policy tools the central bank uses to managethe money supply.

5. Explain the quantity theory of money and use it to explainhow high rates of in�ation occur.

What Is Money and Why Do We Need It?

I Money: Economists consider money to be any asset thatpeople are generally willing to accept in exchange for goodsand services, or for payment of debts.

I Asset: Anything of value owned by a person or a �rm.I Suppose you were living before the invention of money. If youwanted to trade, you would have to barter, trading goods andservices directly for other goods and services.

I Shortcoming: requiring a double coincidence of wants. For abarter trade to take place bw. two people, each person mustwant what the other one has.

I Hence, the problem of BE provides an incentive to identify aproduct that most people will accept in exchange for whatthey have to trade.

I (Conti.) Eventually, societies started using commodity money.Commodity money: A good used as money; also has valueindependent of its use as money. E.g., silver, gold, anddeerskin.

I Historically, once a good became widely accepted as money,people who didn�t have an immediate use for it would bewilling to accept it.

I Trading G&S is much easier once money becomes available:people only need to sell what they have for money and thenuse the money to buy what they want.

I By making exchange easier, money allows people to specializeand become more productive while pursuing their comparativeadvantage.

The Functions of MoneyI Anything used as money� whether a deerskin, a seashell,cigarettes, or a dollar bill� should ful�ll the following fourfunctions:1. Medium of exchange (MOE): Money serves as a MOE whensellers are willing to accept it in exchange for G&S. Aneconomy is more e¢ cient when a single good is recognized asa MOE.

2. Unit of account: Instead of having to quote the price of asingle good in terms of many other goods, each good has asingle price. This function of money gives buyers and sellers aunit of account, a way of measuring value in terms of money.E.g., in U.S., every good has a price in terms of dollars.

3. Store of value: Money allows value to be stored easily: If youdo not use all your accumulated dollars to buy G&Ss today,you can hold the rest to use in the future. Note that money isnot the only store of value.

4. Standard of deferred payment (SDP): Money can serve as aSDP in borrowing and lending. Money can facilitate exchangeover time by providing a store of value and a standard ofdeferred payments.

What Can Serve as Money?

I Five criteria make a good suitable to use as a medium ofexchange:

1. The good must be acceptable to (that is, usable by) mostpeople.

2. It should be of standardized quality so that any two units areidentical.

3. It should be durable so that value is not lost by spoilage.4. It should be valuable relative to its weight so that amountslarge enough to be useful in trade can be easily transported.

5. The medium of exchange should be divisible because di¤erentgoods are valued di¤erently.

I Dollar bills meet all these criteria.

Commodity Money

I Commodity money (CM) meets the criteria for a medium ofexchange.

I But CM has a signi�cant problem: its value depends on itpurity. Unless traders trust each other completely, they neededto check the weight and purity of the metal at each trade.

I It is ine¢ cient to use commodity good (transportation costsand risk, etc.). To get around this problem, privateinstitutions or governments began to store gold and issuepaper certi�cates that could be redeemed for gold.

Fiat MoneyI It can be ine¢ cient for an economy to rely on only gold orother precious metals for its money supply.

I Money, such as paper currency, that is authorized by a centralbank or governmental body and that doesn�t have to beexchanged by the central bank for gold or some othercommodity money.

I Federal Reserve System: The central bank of the US. A U.S.dollar bill is actually a Federal Reserve Note, issued by the FR.

I Federal Reserve currency is legal tender in the US, whichmeans the federal government requires that it be accepted inpayment of debts and requires that cash or checksdenominated in dollars be used in payment of taxes.

I HHs and �rms have con�dence that if they accept paperdollars in exchange for G&Ss, the dollars will not lose muchvalue during the time they hold them.

I Hong Kong Monetary Authority: The central bank of HongKong.

How Do We Measure Money Today?

I Economists have developed several di¤erent de�nitions of themoney supply (MS). Each de�nition includes a di¤erent groupof assets and is based on how liquid the assets are.

I The most narrow measure of money is cash. Broadermeasures include other assets that can be easily convertedinto cash, such as checking account or saving account.

I M1: The narrowest de�nition of the MS.I Currency: All the paper money and coins that are in circulation�meaning what is not held by banks or the government.

I The value of all checking account balances at banks.I The value of traveler�s checks. (ignore it in our discussion ofthe money supply as it is too small.)

I Checking account deposits (CAD) are used much more oftenthan currency to make payments. More than 80% of allexpenditures on G&S are made with checks rather than withcurrency.

I M2: A broader de�nition of the money supply: M1 plussavings account balances, small-denomination time deposits(such as CoD), balances in money market deposit accounts inbanks, and non-institutional money market fund shares.

I Small-denomination time deposits are similar to savingsaccounts, but the deposits are for a �xed period oftime� usually from six months to several years� andwithdrawals before that time are subject to a penalty.

I Money market mutual funds invest in very short-term bonds,such as U.S. Treasury bills.

I In the following discussion, we will use the M1 de�nition ofthe MS because it corresponds most closely to money as amedium of exchange.

I There are two key points about the MS to keep in mind:1. The money supply consists of both currency and checkingaccount deposits.

2. Because balances in checking account deposits are included inthe MS, banks play an important role in the process by whichthe MS increases and decreases.

13 of 54 © Pearson Education Limited 2015

U.S. Money Supply, July 2013

How much money is there in America? This is harder to answer than it first appears, because you have to decide what to count as “money”. M1 is the narrowest definition of the money supply: the sum of currency in circulation, checking account deposits in banks, and holdings of traveler’s checks.

There is a relatively large amount of U.S. currency, because people in other countries sometimes hold and use U.S. dollars instead of their own currency.

Measuring the money supply, July 2013

Figure 14.1

Presenter

Presentation Notes

The Federal Reserve uses two different measures of the money supply: M1 and M2. Panel (a) shows the assets in M1. Panel (b) shows M2, which includes the assets in M1, as well as money market mutual fund shares, small-denomination time deposits, and savings account deposits. Source: Board of Governors of the Federal Reserve System, “Federal Reserve Statistical Release, H.6,” July 14, 2013.

14 of 54 © Pearson Education Limited 2015

U.S. Money Supply, July 2013—continued

M2 is a broader definition of the money supply: it includes M1, plus savings account balances, small-denomination time deposits, balances in money market deposit accounts, and non-institutional money market fund shares.

Measuring the money supply, July 2013

Figure 14.1

17 of 54 © Pearson Education Limited 2015

Making the

Connection Are Bitcoins Money?

When we think of money, we typically think of currency issued by a government. • But currency is only a small part of the

money supply. Over the last decade or so, consumers have come to trust forms of e-money such as PayPal.

Bitcoins are a new form of e-money, owned not by a government or firm, but a product of a decentralized system of linked computers. • Bitcoins can be traded for other currencies on web sites. • Some web sites accept Bitcoins as a form of payment. Should Bitcoins be included in a measure of the money supply? • For now, they are not; if they grow popular, maybe they should be.

Two examples

I The De�nitions of M1 and M2. Suppose you decide towithdraw $2, 000 from your checking account and use themoney to buy a bank certi�cate of deposit (CoD). How thiswill a¤ect M1 and M2? Answers: Reduce M1 by $2000 butleaves M2 unchanged.

I What About Credit Cards and Debit Cards? They are notincluded in the de�nitions of the money supply. When you buyG&S with a credit card, you are in e¤ect taking out a loanfrom the bank issuing the card. Only when you pay your billat the end of the moth from your checking account is thetransaction complete. With a debit card, the funds to makethe purchase are taken directly from your checking account.In either case, the cards themselves do not represent money.

Bank Balance SheetsI The key assets on a bank�s balance sheet are its reserves,loans, and holdings of securities, such as U.S. treasury bills.

I Reserves: Deposits that a bank keeps as cash in its vault or ondeposit with the Federal Reserve.

I Required reserves: Reserves that a bank is legally required tohold, based on its checking account deposits.

I Required reserve ratio: The minimum fraction of depositsbanks are required by law to keep as reserves.

I Excess reserves: Reserves that banks hold over and above thelegal requirement.

I Banks make consumer loans to households and commercialloans to businesses. A loan is an asset to a bank because itrepresents a promise by the person taking it out to makecertain speci�ed payments to the bank.

I Deposits include checking accounts, savings accounts, andcerti�cates of deposit, and are liabilities to banks because theyare owed to the households or �rms that have deposited thefunds.

I Fractional reserve banking system: A banking system in whichbanks keep less than 100% of deposits as reserves.

I Bank run A situation in which many depositors simultaneouslydecide to withdraw money from a bank.

I Bank panic A situation in which many banks experience runsat the same time.

I A central bank, like the Federal Reserve in the US, can helpstop a bank panic by acting as a lender of last resort. Inacting as a lender of last resort, a central bank makes loans tobanks that cannot borrow funds elsewhere.

20 of 54 © Pearson Education Limited 2015

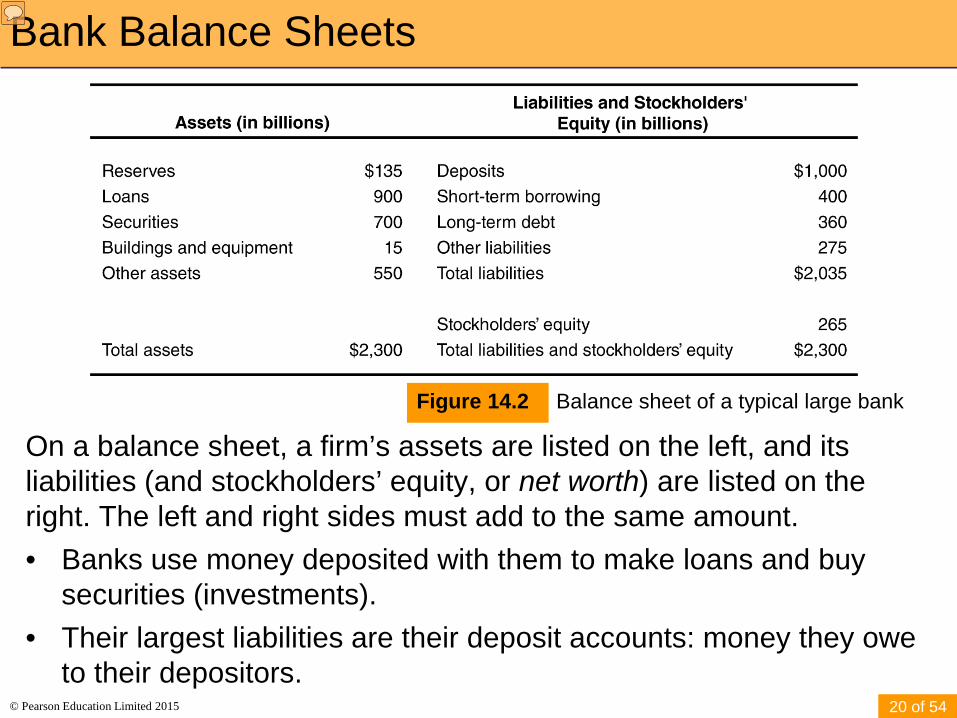

Bank Balance Sheets

On a balance sheet, a firm’s assets are listed on the left, and its liabilities (and stockholders’ equity, or net worth) are listed on the right. The left and right sides must add to the same amount. • Banks use money deposited with them to make loans and buy

securities (investments). • Their largest liabilities are their deposit accounts: money they owe

to their depositors.

Balance sheet of a typical large bank Figure 14.2

Presenter

Presentation Notes

The items on a bank’s balance sheet of greatest economic importance are its reserves, loans, and deposits. Notice that the difference between the value of this bank’s total assets and its total liabilities is equal to its stockholders’ equity. As a consequence, the left side of the balance sheet always equals the right side. Note: Some entries have been combined to simplify the balance sheet.

21 of 54 © Pearson Education Limited 2015

Bank Balance Sheets

Reserves are deposits that a bank keeps as cash in its vault or on deposit with the Federal Reserve.

• Notice that the bank does not keep enough deposits on hand to cover all of its deposits. This is how the bank makes a profit: lending out or investing money deposited with it.

Balance sheet of a typical large bank Figure 14.2

23 of 54 © Pearson Education Limited 2015

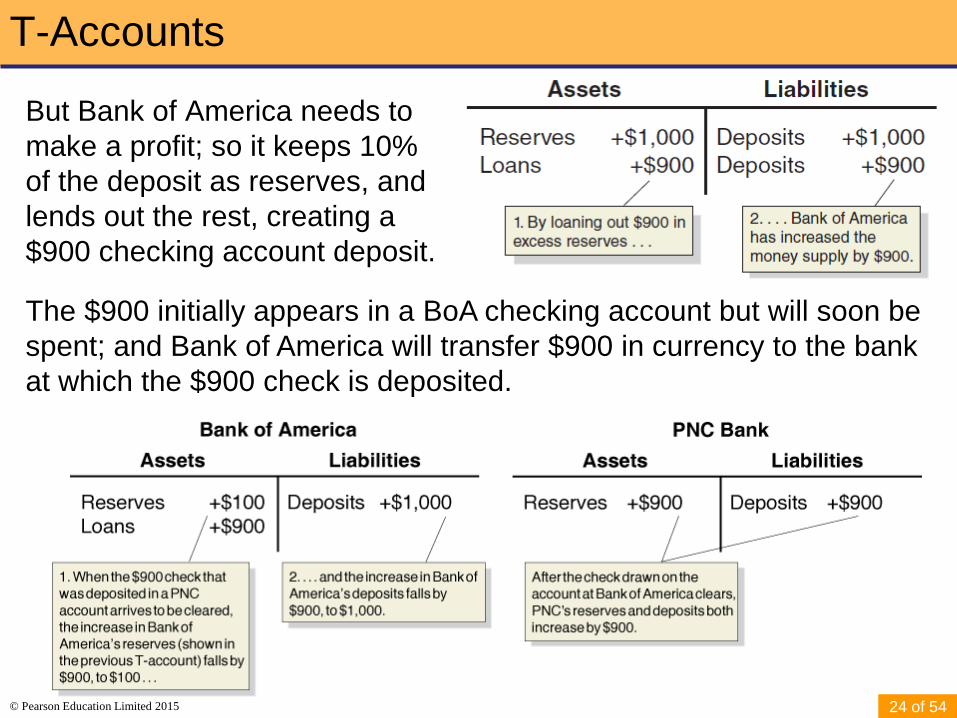

Money Creation at Bank of America

A T-account is a stripped-down version of a balance sheet, showing only how a transaction changes a bank’s balance sheet.

When you deposit $1,000 in currency at Bank of America, its reserves increase by $1,000 and so do its deposits:

The currency component of the money supply decreases by the $1,000, since that $1,000 is no longer in circulation; but the checking deposits component increases by $1,000. So there is no net change in the money supply—yet.

24 of 54 © Pearson Education Limited 2015

T-Accounts

But Bank of America needs to make a profit; so it keeps 10% of the deposit as reserves, and lends out the rest, creating a $900 checking account deposit.

The $900 initially appears in a BoA checking account but will soon be spent; and Bank of America will transfer $900 in currency to the bank at which the $900 check is deposited.

25 of 54 © Pearson Education Limited 2015

When Will it End?

Each “round”, the additional checking account deposits get smaller and smaller.

• Every round, 10% of the deposits are kept as reserves. This allows us to tell by how much the checking deposits will eventually increase: the $1,000 in currency will become the 10% required reserves for all of the checking deposits, so a total of $10,000 in checking deposits can be created. Bank Increase In Checking Account Deposits Bank of America $1,000 PNC + 900 (= 0.9 × $1,000) Third Bank + 810 (= 0.9 × $900) Fourth Bank + 729 (= 0.9 × $810)

• + • • + • • + •

Total change in checking account deposits = $10,000

26 of 54 © Pearson Education Limited 2015

Simple Deposit Multiplier

An alternative way to find out how much money the original $1,000 in currency will create is to add up all of the checking account deposits.

$1,000 + [0.9 × $1,000] + [(0.9 × 0.9) × $1,000] + [(0.9 × 0.9 × 0.9) × $1,000] + …

= $1,000 + [0.9 × $1,000] + [0.92 × $1,000] + [0.93 × $1,000] + …

= $1,000 (1 + 0.9 + 0.92 + 0.93 + …)

The expression in the parentheses can be rewritten as:

9.011− 10.0

1= 10=

So the total increase in deposits is $1,000(10) = $10,000.

• The “10” here is the simple deposit multiplier: the ratio of the amount of deposits created by banks to the amount of new reserves.

27 of 54 © Pearson Education Limited 2015

General Form for the Simple Deposit Multiplier

In general, we can write the simple deposit multiplier as:

RR1multiplierdeposit Simple =

So with a 10% required reserve ratio (RR), the simple deposit multiplier is 10.

• With a 20% required reserve ratio, the simple deposit multiplier is 5.

Then:

RR1 reservesbank in Changedepositsaccount checkingin Change ×=

For example, $100,000 in new deposit, with a 10% required reserve ratio, results in:

10.01 000,100$depositsaccount checkingin Change ×=

000,000,1$10 000,100$ =×=

28 of 54 © Pearson Education Limited 2015

Real-World Deposit Multiplier

With a 10% required reserve ratio, the simple deposit multiplier tells us that a currency deposit will be multiplied 10 times. • But in reality, we do not observe this: currency deposits only end

up being multiplied about 2.5 times, during “normal” periods. Why this difference? • Banks may not lend out as much as we predict, either because

they want to keep excess reserves, or they cannot find credit-worthy borrowers.

• Consumers keep some currency out of the bank; that currency cannot be used as required reserves.

Note: during the recession of 2007-2009, research suggests that the real-world multiplier fell to close to 1.

How the Federal Reserve Manages the Money Supply?

I Monetary policy: The actions the Federal Reserve takes tomanage the money supply (MS) and interest rates to pursueeconomic objectives.

I To manage the MS, the Fed uses three monetary policy tools:

1. Open market operations2. Discount policy3. Reserve requirements

34 of 54 © Pearson Education Limited 2015

The Federal Reserve System

In 1913, Congress divided the country into 12 Federal Reserve districts, each of which provides services to banks in the district. But the real power of the Fed lies in Washington, DC, with the Board of Governors. • In 2013, the chair of the Board of Governors was Ben Bernanke.

The Federal Reserve system Figure 14.3

Presenter

Presentation Notes

The United States is divided into 12 Federal Reserve districts, each of which has a Federal Reserve Bank. The real power within the Federal Reserve System, however, lies in Washington, DC, with the Board of Governors, which consists of 7 members appointed by the president. The 12-member Federal Open Market Committee carries out monetary policy. Source: Board of Governors of the Federal Reserve System.

35 of 54 © Pearson Education Limited 2015

The Federal Reserve System—continued

The Fed is also responsible for managing the money supply.

The Federal Open Market Committee (FOMC) conducts America’s monetary policy: the actions the Federal Reserve takes to manage the money supply and interest rates to pursue macroeconomic policy objectives.

The Federal Reserve system Figure 14.3

Open Market Operations

I Federal Open Market Committee (FOMC) The FederalReserve committee responsible for OMOs and managing theMS in the U.S.. It meets eight times per year to discussmonetary policy.

I Open market operations: The buying and selling of Treasurysecurities by the Federal Reserve in order to control the MS.Note that the US treasury borrows money by selling bills,note, and bonds.

I To increase (decrease) MS, the FOMC directs the tradingdesk, located in the New York Fed, to buy (sell) US treasurysecurities from the public. When the sellers (buyers) deposit(withdraw) the funds in (from) their banks, the reserve ofbanks will rise (decline). This will start the process ofincreasing (decreasing) loans and checking account depositsthat increases (decrease) MS.

I (Conti.) Three reasons why the Fed conducts MP principallythrough OMO:

1. The Fed initiate OMO, it completely controls their volume.2. The Fed can make both large and small OMO.3. The Fed can implement its OMO quickly.

I The main way the Fed increases the MS is not by printingmore paper money but buying Treasury securities.

37 of 54 © Pearson Education Limited 2015

Open Market Operations in Action

The Fed has three monetary policy tools at its disposal:

Open market operations (most common)

Suppose the Fed engages in an open market purchase of $10 million.

• The banking system’s T-account reflects an increase in reserves, and a corresponding decrease in assets due to its debt to the Fed.

• The banking system’s reserves are liabilities for the Fed, but it gains assets equal to the debt owed to it by the banking system.

Discount Policy

I Discount loans Loans the Federal Reserve makes to banks.I Discount rate The interest rate the Federal Reserve chargeson discount loans.

I When a bank receives a loan from the Fed, its reservesincrease by the amount of the loan. By lowering the DR, theFed can encourage banks to take additional loans and therebyincrease their reserves. As a result, MS will increase.

I Note that in practice, this policy is used to help banks thatexperience temporary problems with deposit withdrawals,rather than to use them to increase or decrease MS.

I In response to the bank failures that were occurring at theonset of the Great Depression, Congress established theFederal Deposit Insurance Corporation (FDIC) in 1934 toinsure deposits in most banks up to a limit, which is currently$250,000 per deposit.

Reserve Requirements

I When the Fed reduces the RR ratio, it converts requiredreserves into excess reserves.

I This policy is not conducted frequently because frequentadjustments would be disruptive and costly for banks.

Putting It All Together: Decisions of the Nonbank Public,Banks, and the Fed

I The nonbank public and banks also a¤ect MS in practice.The public decide how much money to deposit in banks andbanks decide how much to reserve and how to loan out.

I The Fed sta¤ monitors information on banks�reserves anddeposits every week, and the Fed can respond quickly to shiftsin behavior by depositors or banks. It can therefore steer theMS close to the desired level.

39 of 54 © Pearson Education Limited 2015

The Rise and Effects of the Shadow Banking System

The banks we have been discussing so far are commercial banks, whose primary role is to accept funds from depositors and make loans to borrowers.

In the last 20 years, two important developments have occurred in the financial system:

1. Banks have begun to resell many of their loans rather than keep them until they are paid off.

2. Financial firms other than commercial banks have become sources of credit to businesses.

40 of 54 © Pearson Education Limited 2015

Securitization Comes to Banking

A security is a financial asset—such as a stock or a bond—that can be bought and sold in a financial market. • Traditionally, when a bank made a loan like a residential mortgage

loan, it would “keep” the loan and collect payments until the loan was paid off.

In the 1970s, secondary markets developed for securitized loans, allowing them to be traded, much like stocks and bonds. Securitization: The process of transforming loans or other financial assets into securities.

The process of securitization Figure 14.4

(a) Securitizing a loan (b) The flow of payments on a securitized loan

Presenter

Presentation Notes

Panel (a) shows how in the securitization process banks grant loans to households and bundle the loans into securities that are then sold to investors. Panel (b) shows that banks collect payments on the original loans and, after taking a fee, send the payments to the investors who bought the securities.

41 of 54 © Pearson Education Limited 2015

The Shadow Banking System

The 1990s and 2000s brought increasing important of non-bank financial firms, including:

• Investment banks: banks that do not typically accept deposits from or make loans to households; they provide investment advice, and engage also engage in creating and trading securities such as mortgage-backed securities.

• Money market mutual funds: funds that sell shares to investors and use the money to buy short-term Treasury bills and commercial paper (loans to corporations).

• Hedge funds: funds that raise money from wealthy investors and make “sophisticated” (often non-standard) investments.

By raising funds from investors and providing them directly or indirectly to firms and households, these firms have become a “shadow banking system”.

45 of 54 © Pearson Education Limited 2015

How Does the Money Supply Affect Prices?

Beginning in the 16th century, Spain sent gold and silver from Mexico and Peru back to Europe.

• These metals were minted into coins, increasing the money supply.

Prices in Europe rose steadily during those years.

• This helped people to make the connection between the amount of money in circulation and the price level.

46 of 54 © Pearson Education Limited 2015

Connecting Money and Prices: The Quantity Equation

In the early 20th century, Irving Fisher formalized the relationship between money and prices as the quantity equation:

𝑀𝑀 × 𝑉𝑉 = 𝑃𝑃 × 𝑌𝑌

Money supply real output

velocity of moneyprice level

Velocity of money: the average number of times each dollar in the money supply is used to purchase goods and services included in GDP.

Rewriting this equation by dividing through by M, we obtain:

𝑉𝑉 = 𝑃𝑃 × 𝑌𝑌𝑀𝑀

47 of 54 © Pearson Education Limited 2015

Calculating the Velocity of Money

Measuring: • The money supply (M) with M1, • The price level (P) with the GDP deflator, and • The level of real output (Y) with real GDP, We obtain the following value for velocity (V): We can always calculate V. But will we always get the same answer? The quantity theory of money asserts that, subject to measurement error, we will: Quantity theory of money: A theory about the connection between money and prices that assumes that the velocity of money is constant.

48 of 54 © Pearson Education Limited 2015

The Quantity Theory Explanation of Inflation

When variables are multiplied together in an equation, we can form the same equation with their growth ratesaddedtogether.

So the quantity equation:

𝑀𝑀 × 𝑉𝑉 = 𝑃𝑃 × 𝑌𝑌

generates: Growth rate of the money supply + Growth rate of velocity

= Growth rate of the price level or the inflation rate+ Growth rate of real output

Rearranging this to make the inflation rate the subject, and assuming that the velocity of money is constant, we obtain: Inflation rate = Growth rate of the money supply − Growth rate of real output

49 of 54 © Pearson Education Limited 2015

The Inflation Rate According to the Quantity Theory

Inflation rate = Growth rate of the money supply − Growth rate of real output

This equation provides the following predictions:

1. If the money supply grows faster than real GDP, there will be inflation.

2. If the money supply grows slower than real GDP, there will be deflation (a decline in the price level).

3. If the money supply grows at the same rate as real GDP, there will be neither inflation nor deflation: the price level will be stable.

Is velocity truly constant from year to year? The answer is no.

• But the quantity theory of money can still provide insight:

• In the long run, inflation results from the money supply growing at a faster rate than real GDP.

50 of 54 © Pearson Education Limited 2015

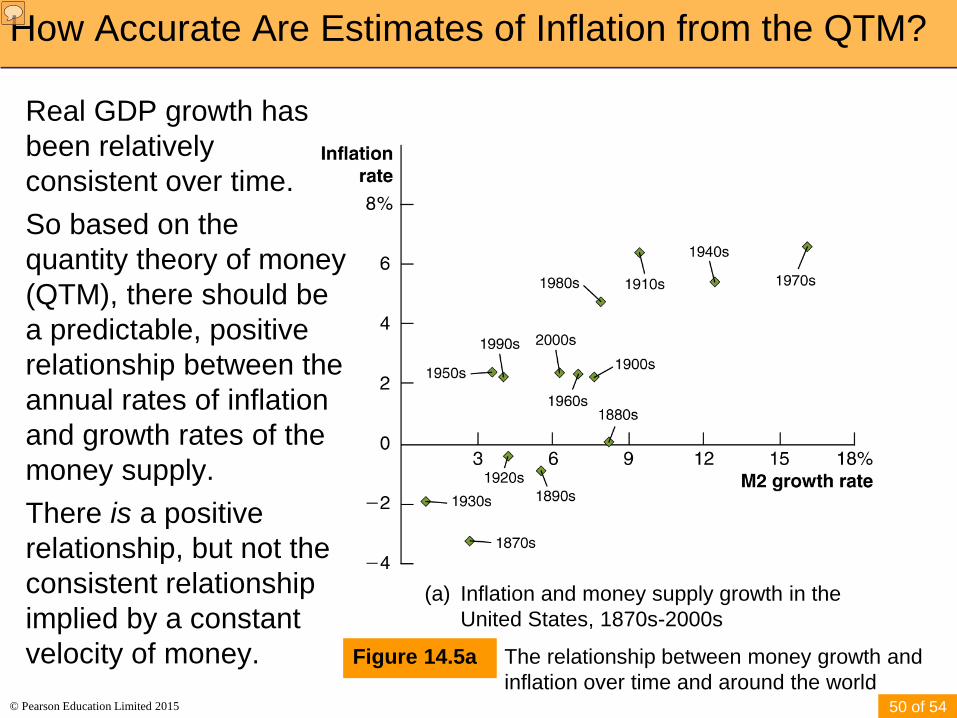

How Accurate Are Estimates of Inflation from the QTM?

Real GDP growth has been relatively consistent over time. So based on the quantity theory of money (QTM), there should be a predictable, positive relationship between the annual rates of inflation and growth rates of the money supply. There is a positive relationship, but not the consistent relationship implied by a constant velocity of money. The relationship between money growth and

inflation over time and around the world Figure 14.5a

(a) Inflation and money supply growth in the United States, 1870s-2000s

Presenter

Presentation Notes

Panel (a) shows that, by and large, the rate of inflation in the United States has been highest during the decades in which the money supply has increased most rapidly, and the rate of inflation has been lowest during the decades in which the money supply has increased least rapidly. Panel (b) shows the relationship between money supply growth and inflation for 56 countries between 1995 and 2011. There is not an exact relationship between money supply growth and inflation, but countries such as Bulgaria, Turkey, and Ukraine that had high rates of money supply growth had high inflation rates, and countries such as the United States and Japan had low rates of money supply growth and low inflation rates. Sources: Panel (a): For the 1870s to the 1960s, Milton Friedman and Anna J. Schwartz, Monetary Trends in the United States and United Kingdom: Their Relation to Income, Prices, and Interest Rates, 1867–1975, Chicago: University of Chicago Press, 1982, Table 4.8; and for the 1970s to the 2000s, Federal Reserve Board of Governors and U.S. Bureau of Economic Analysis; Panel (b): International Monetary Fund, International Monetary Statistics.

51 of 54 © Pearson Education Limited 2015

Accuracy of the QTM—continued

We see a similar story when we compare average rates of inflation and growth rates of the money supply across different countries.

Although the relationship is not entirely predictable, countries with higher growth in the money supply do have higher rates of inflation.

The relationship between money growth and inflation over time and around the world

Figure 14.5b

(b) Inflation and money supply growth in 56 countries, 1995-2011