Aluminium Site Presentation 08

24

Aluminium Investor Presentation Australia Analysts Site Visit 29 October 2008

Transcript of Aluminium Site Presentation 08

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 1/24

Aluminium Investor Presentation

Australia Analysts Site Visit

29 October 2008

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 2/24

Slide 2

Disclaimer By viewing this presentation you agree to be bound by the following conditions.Certain statements in this presentation are forward-looking statements (including statements regardingcontribution synergies, future cost savings, the cost and timingof development projects, future productionvolumes, increases in production and infrastructure capacity, the identification of additional mineral Reserves andResources and project lives and, without limitation, other statements typically containing words such as "intends,""expects," "anticipates," "targets," plans," "estimates" and words of similar import.) These statements are basedon current expectations and beliefs and numerous assumptions regarding BHP Billiton's present and futurebusiness strategies and the environments in which BHP Billiton will operate in the future and such assumptions,expectations and beliefs may or may not prove to be correct and by their nature, are subject to a number of known and unknown risks and uncertainties that could cause actual results, performance and achievements todiffer materially.Save as required by law or the rules of the UK Listing Authority and the London Stock Exchange, the UKTakeover Panel, or the listing rules of ASX Limited, BHP Billiton undertakes no duty to update any forward-looking statements in this presentation.No statement concerning expected cost savings, revenue benefits (and resulting incremental EBITDA) and EPSaccretion in this presentation should be interpreted to mean that the future earnings per share of the enlargedBHP Billiton group for current and future financial years will necessarily match or exceed the historical or published earnings per share of BHP Billiton, and the actual estimated cost savings and revenue benefits (and

resulting EBITDA enhancement) may be materially greater or less than estimated.BHP Billiton results are reported under International Financial Reporting Standards (IFRS). References toUnderlying EBIT and Underlying EBITDA exclude any exceptional items. A reconciliation to profit fromoperations is contained within the profit announcementReferences in this presentation to “$” are to United States dollars unless otherwise specified.

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 3/24

Slide 3

Presenter introduction

Jon Dudas

President Aluminium CSG

Julius Matthys

COO Worsley Alumina

Markus Meurer VP Marketing Alumina

• 24 years resources experience

• 17 years at BHP Billiton

• 26 years resources experience

• 26 years at BHP Billiton

• 21 years resources experience

• 7 years at BHP Billiton

Warren McKenzieE&G Project Director • 35 years resources experience

• 1 year at BHP Billiton

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 4/24

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 5/24Slide 5

Aluminium investor presentation

Business overview – Operating performance – Significance to BHP Billiton portfolio – Comparison to peers – Key challenges for the industry

Aluminium and alumina commodity outlook – Global demand and China growth outlook – Global supply outlook – Cost curves – Input costs

Future growth options

Key messages

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 6/24Slide 6

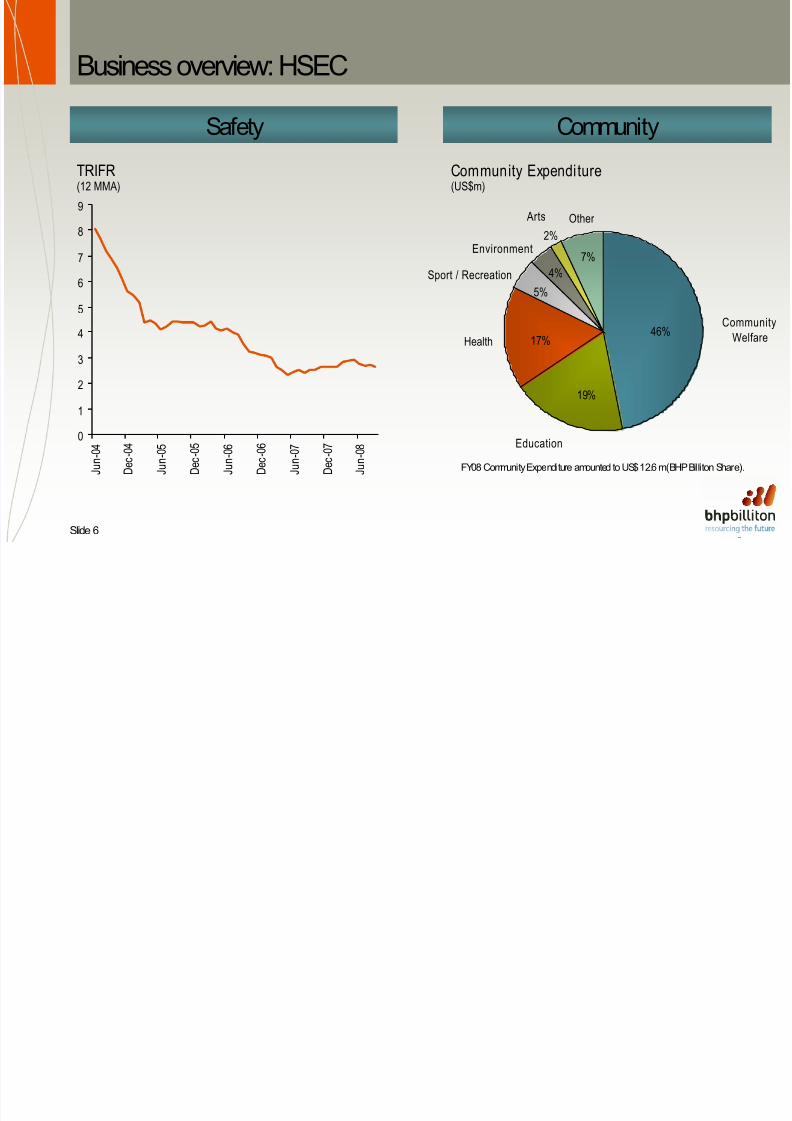

Business overview: HSEC

Safety Community

FY08 Community Expenditure amounted to US$ 12.6 m(BHP Billiton Share).

TRIFR(12 MMA)

Community Expenditure(US$m)

7%

2%

4%

5%

17%

19%

46%Communi

Welfare

Education

Health

Other

Sport / Recreation

Environment

Arts

0

1

2

3

4

5

6

7

8

9

J u n - 0

4

D e c - 0

4

J u n - 0

5

D e c - 0

5

J u n - 0

6

D e c - 0

6

J u n - 0

7

D e c - 0

7

J u n - 0

8

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 7/24Slide 7

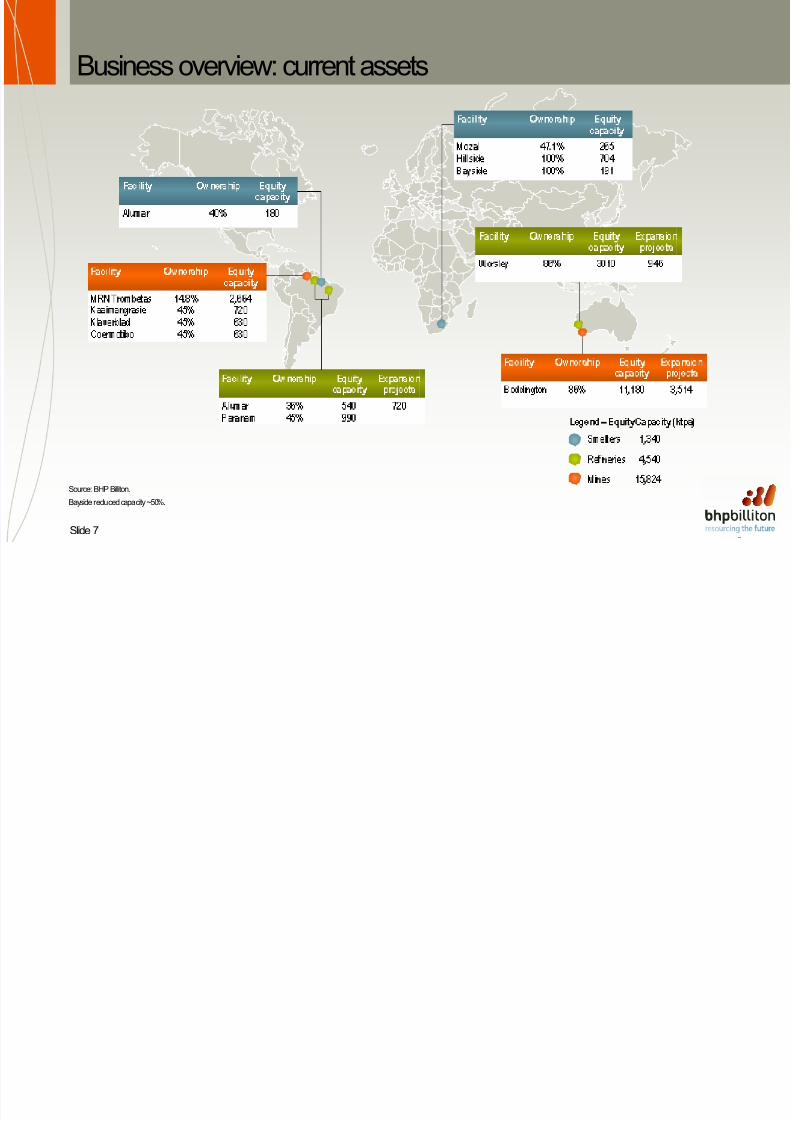

Business overview: current assets

Source: BHP Billiton.

Bayside reduced capacity ~50%.

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 8/24Slide 8

0

10

20

30

40

50

20 04 2005 2006 2 007 200 8

Peers BHP Billiton

Business overview: operating performance

• Record alumina production

• South African power situation will continue toimpact metal production• Worsley E&G approved

-21.11,8561,465 Aluminium EBIT

% Change20072008Year ended June (US$m)

Source: BHP Billiton and companies’ annual and half year reports Excludes Third Party Trading* Peers include AWAC, Chalco and the aluminiumsegments Rio Tinto, Valeand the upstreamsegments of Alcoa and Alcan (until June 2007).

EBIT Margin(%)

Year Ended June

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 9/24Slide 9

Business overview : contribution to group

Underlying EBIT Margin(a)

(FY2008)

(a) EBIT Margin excludes third party trading activities.

67%

30%

31%

62%

20%

25%

24%

48%

51%

58%

Underlying EBIT(FY2008, US$bn)

0

5

10

15

20

25

Iron Ore

Manganese

Energ y Coal

Metallurgical Coal

Diamonds andSpecialty Products

Base Metals

Petroleum

Stainless Steel Materials

Aluminium

Iron Ore

Manganese

Energ y Coal

Metallurgical Coal

Diamonds andSpecialty Products

Base Metals

Petroleum

Stainless St eelMaterials

Aluminium

Group

(Our portfolio is diversified and balanced across high margin commodities)

Energy(27%)

Non Ferrous(44%)

SteelmakingMaterials(29%)

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 10/24Slide 10

Business overview: key challenges• Raw material price pressures

• Global power supply

• Bringing on new capacity• Quality of Chinese bauxite

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 11/24

Slide 11

Aluminium investor presentation

Business overview – Operating performance – Significance to BHP Billiton portfolio – Comparison to peers – Key challenges for the industry

Aluminium and alumina commodity outlook – Global demand and China growth outlook – Global supply outlook – Cost curves

Future growth options

Key messages

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 12/24

Slide 12

Aluminium and alumina commodity outlookKey China Messages

• China has a significant influence on the Aluminium market

– Aluminium is required to supply the intensive urbanisation of China – A question of self sufficiency of aluminium supply – Is power a constraining factor? – Domestic aluminium supply is positioned high on the cost curve

• Short on quality bauxite and thus alumina – Domestic alumina additions are positioned high on the cost curve

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 13/24

Slide 13

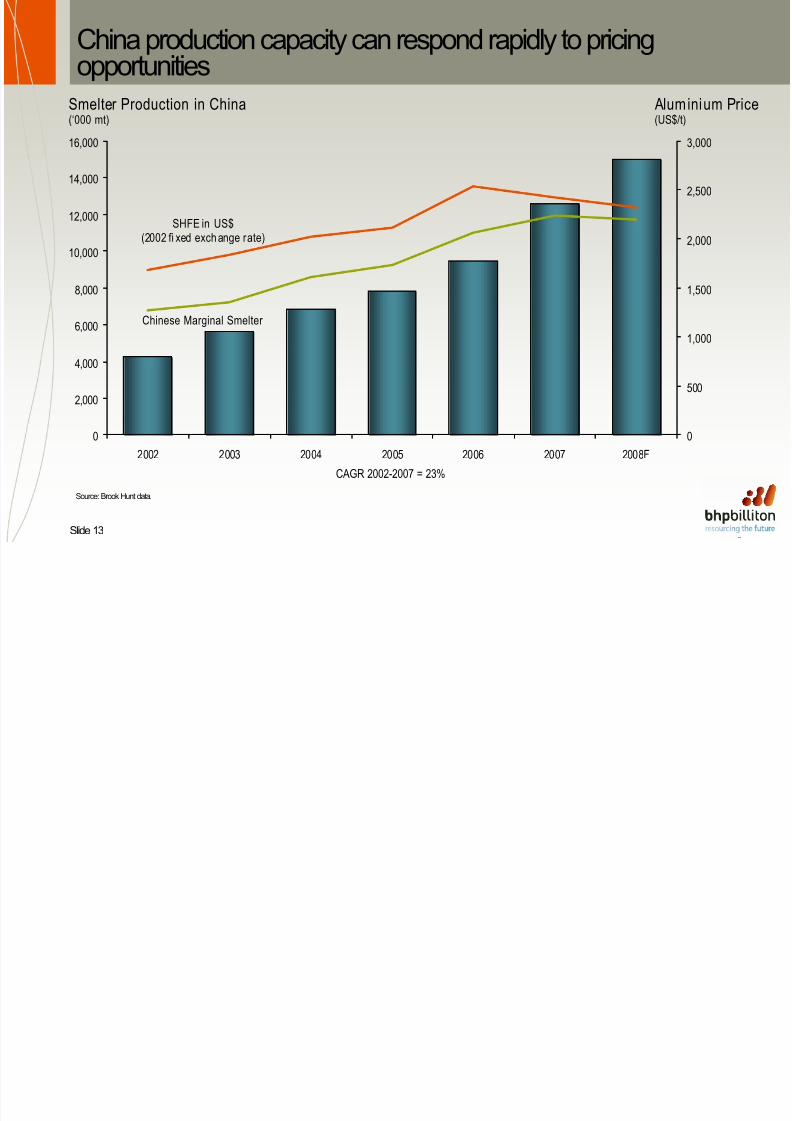

China production capacity can respond rapidly to pricingopportunities

Source: Brook Hunt data.

Smelter Production in China(‘000 mt)

Aluminium Price(US$/t)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2002 2003 2004 2005 2006 2007 2008F

0

500

1,000

1,500

2,000

2,500

3,000

SHFE in US$(2002 fi xed exchange rate)

Chinese Marginal Smelter

CAGR 2002-2007 = 23%

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 14/24

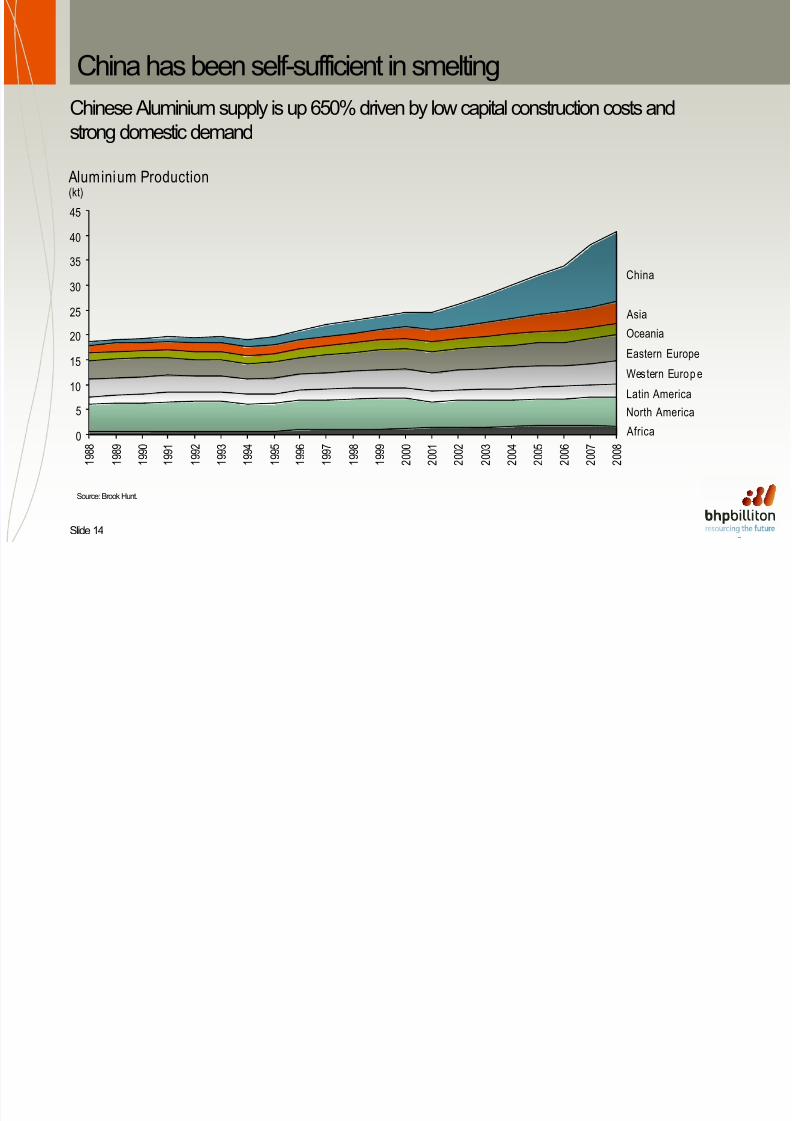

Slide 14

China has been self-sufficient in smeltingChinese Aluminium supply is up 650% driven by low capital construction costs andstrong domestic demand

Aluminium Production(kt)

China

AsiaOceania

Eastern Europe

Western Europ e

Latin AmericaNorth America Africa

Source: Brook Hunt.

0

5

10

15

20

2530

35

40

45

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 15/24

Slide 15

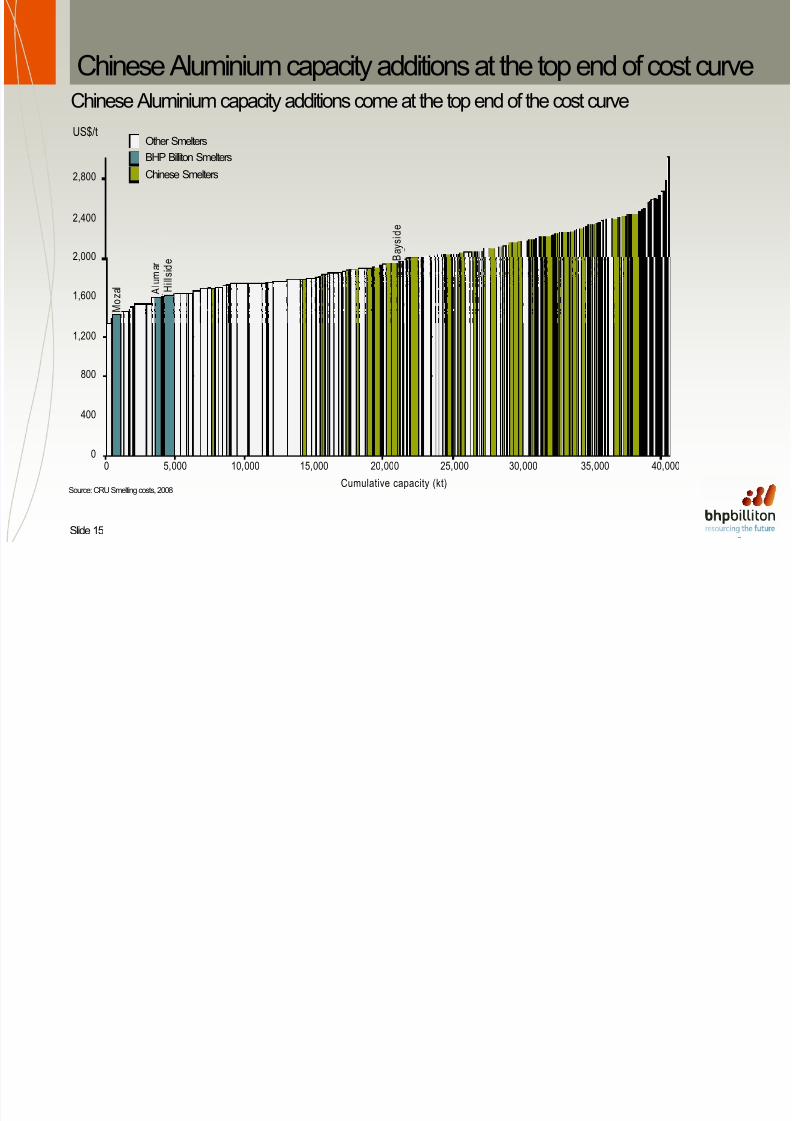

Chinese SmeltersBHP Billiton SmeltersOther Smelters

2,800

2,400

2,000

1,600

1,200

800

400

00 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

A l u m a r B

a y s i d e

H i l l s i d e

M o z a l

Chinese Aluminium capacity additions at the top end of cost curveChinese Aluminium capacity additions come at the top end of the cost curve

Source: CRU Smelting costs, 2008

US$/t

Cumulative capacity (kt)

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 16/24

Slide 16

China has a track record of bringing on new power capacityAbility to bring on new power capacity on time as plannedSources of Chinese power (GW)

Wind / Other Nuclear

Hydro

Coal

Source: CEC.

0

150

300

450

600

750

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 17/24

Slide 17

Aluminium stocks

Source: LME, SHFE and Comex.

Exchange Stocks(kt)

LME Cash pric($/t Nominal)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

J a n - 0

4

A p r - 0 4

J u l - 0 4

O c t - 0 4

J a n - 0

5

A p r - 0 5

J u l - 0 5

O c t - 0 5

J a n - 0

6

A p r - 0

6

J u l - 0 6

O c t - 0 6

J a n - 0

7

A p r - 0 7

J u l - 0 7

O c t - 0 7

J a n - 0

8

A p r - 0

8

J u l - 0 8

O c t - 0 8

0

500

1,000

1,500

2,000

2,500

3,000

3,500Comex

SHFE

LME

LME Cash (RH)

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 18/24

Slide 18

Chinese demand for imported Alumina and Bauxite

Source: BHP Billiton Internal Analysis, Chinese customs data, CNIA.

Alumina(kt)

0

5,000

10,000

15,000

20,000

25,000

30,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008YTD

Domestic Alumina Productio

Chinese Bauxite

Domestic Alumina ProductioImported Bauxit e Ore

Alumina Imports

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 19/24

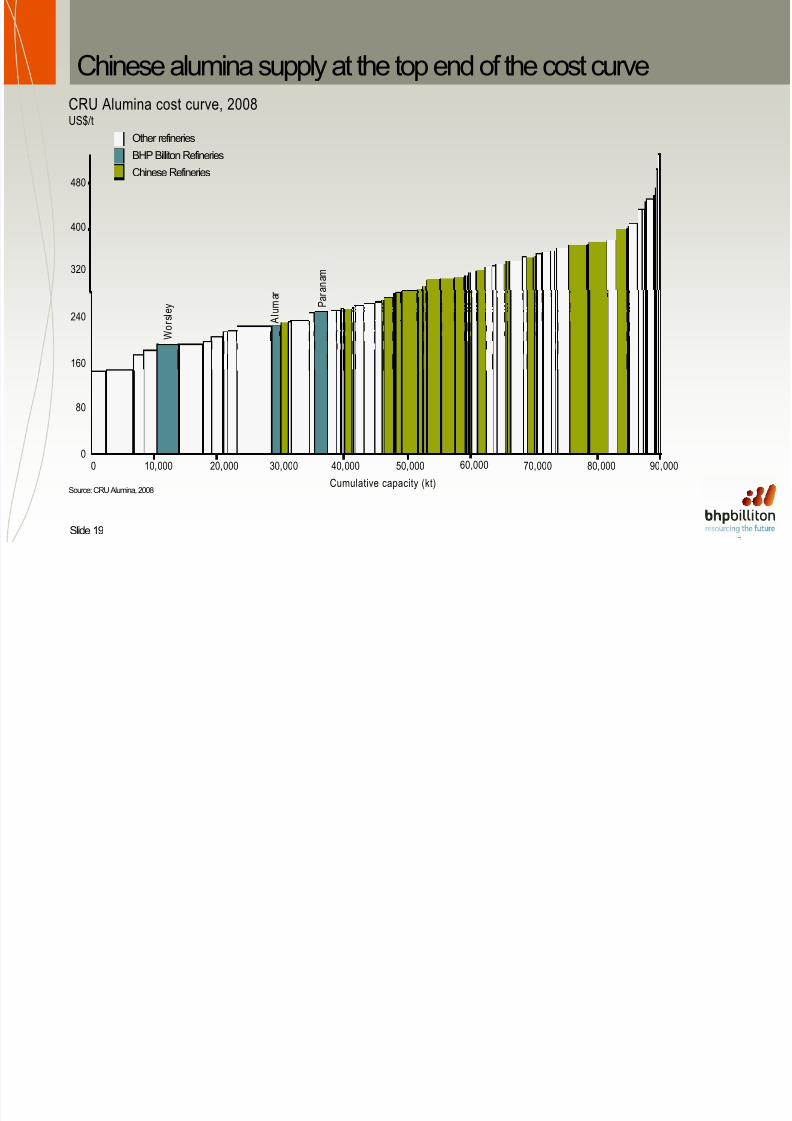

Slide 19

Chinese alumina supply at the top end of the cost curveCRU Alumina cost curve, 2008US$/t

Source: CRU Alumina, 2008 Cumulative capacity (kt)

BHP Billiton RefineriesChinese Refineries

Other refineries

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

480

400

320

240

160

80

0

A l u m a r

P a r a n a m

W o r s l e y

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 20/24

Slide 20

Aluminium investor presentation

Business overview – Operating performance – Significance to BHP Billiton portfolio – Comparison to peers – Key challenges for the industry

Aluminium and alumina commodity outlook

– Global demand and China growth outlook – Global supply outlook – Cost curves – Input costs

Future growth options

Key messages

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 21/24

Slide 21

World’s top 10 bauxite deposit countries(Bt)

Reserves

Most attractive bauxite depositsMost attractive bauxite deposits are in Guinea

Guinea8.6 Bt

Australia7.9 Bt

Brazil2.5 Bt

India1.4 Bt

China2.3 BtJamaica

2.5 Bt

Greece0.6 Bt

Suriname0.6 Bt

Kazakhstan0.4 Bt

Guyana

0.9 Bt

Source: USGS.

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 22/24

Slide 22

Guinea projectGuinea• Long life, world class bauxite

resource with embedded options

• Strong government support

• Currently finalising feasibility study

• Greenfield projects are morechallenging in new geographies

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 23/24

Slide 23

Aluminium investor presentation

Business overview – Operating performance – Significance to BHP Billiton portfolio – Comparison to peers – Key challenges for the industry

Aluminium and alumina commodity outlook

– Global demand and China growth outlook – Global supply outlook (The key constraints) – Cost curves – Input costs

Growth profile and capital projects

Key messages

8/14/2019 Aluminium Site Presentation 08

http://slidepdf.com/reader/full/aluminium-site-presentation-08 24/24