08 16 investor presentation

39

Investor Presentation August 2016

-

Upload

investorplygem -

Category

Investor Relations

-

view

1.588 -

download

0

Transcript of 08 16 investor presentation

Investor PresentationA u g u s t 2 0 1 6

These slides and the accompanying oral discussion may contain “forward-looking statements” within the meaning of the Private SecuritiesLitigation Reform Act of 1995. Such statements involve known and unknown risks, uncertainties and other factors that could cause the actualresults of Ply Gem Holdings, Inc. (the “Company”) to differ materially from the results expressed or implied, including: downturns in the homerepair and remodeling or the new construction end markets, or the economy or the availability of consumer credit; competition from otherexterior building products manufacturers and alternative building materials; inability to successfully develop new products or improve existingproducts; changes in the costs and availability of raw materials; consolidation and further growth of our customers; loss of, or a reduction inorders from, any of our significant customers; inclement weather conditions; increases in union organizing activity and work stoppages at ourfacilities or the facilities of our suppliers; our ability to employ, train and retain qualified personnel at a competitive cost; claims arising from theoperations of our various businesses prior to our acquisitions; product liability claims, including class action claims, relating to the products wemanufacture; litigation outside of product liability claims; loss of certain key personnel; interruptions in deliveries of raw materials or finishedgoods; environmental costs and liabilities; inability to realize anticipated synergies and cost savings with respect to acquisitions; manufacturing orassembly realignments; threats to, or impairments of, our intellectual property rights; increases in transportation and fuel costs; changes inforeign currency exchange and interest rates; material non-cash impairment charges; our significant amount of indebtedness; covenants in theABL Facility, the credit agreement governing our Senior Secured Term Loan Facility and the indenture governing the 6.50% Senior Notes;limitations on our net operating losses and payments under the tax receivable agreement to our stockholders; failure to successfullyconsummate and integrate acquisitions; actual or perceived security vulnerabilities or cyberattacks on our networks; failure to effectivelymanage labor inefficiencies associated with increased production and new employees added to the Company; failure to generate sufficient cashto service all of our indebtedness and make capital expenditures; control by the CI Partnerships; and the risks set forth in the Company’s filingswith the Securities and Exchange Commission. Consequently such forward-looking statements should be regarded as the Company’s currentplans, estimates and beliefs. Except as required by law, the Company does not undertake and specifically declines any obligation to publiclyrelease the results of any revisions to these forward-looking statements that may be made to reflect any future events or circumstances after thedate of such statements or to reflect the occurrence of anticipated or unanticipated events.

In addition, these slides and the accompanying oral discussion reference financial information determined by methods other than in accordance with accounting principles generally accepted in the United States of America (“GAAP”), such as adjusted EBITDA. The Company’s management uses these non-GAAP measures in its analysis of the Company’s performance. The Company believes that the presentation of certain non-GAAP measures provides useful supplemental information that is essential to a proper understanding of the operating results of the Company’s core business. These non-GAAP measures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. A reconciliation of each non-GAAP financial measure to the most directly comparable GAAP financial measure is provided in the appendix to the slides.

LegalDisclaimer

1

Ply Gem Overview

• Exceeding $1.8 Billion in net sales (1)

• Approximately 9,000 associates

One of the Largest Manufacturers of Exterior Building and Home Improvement Products in North America

3

CompanyOverview

(1) LTM 2Q16

46%54% 46%54%

NEW CONSTRUCTION / R&R(1)WINDOWS / SIDING (1)

11%

89%

U.S. / Canada(1)

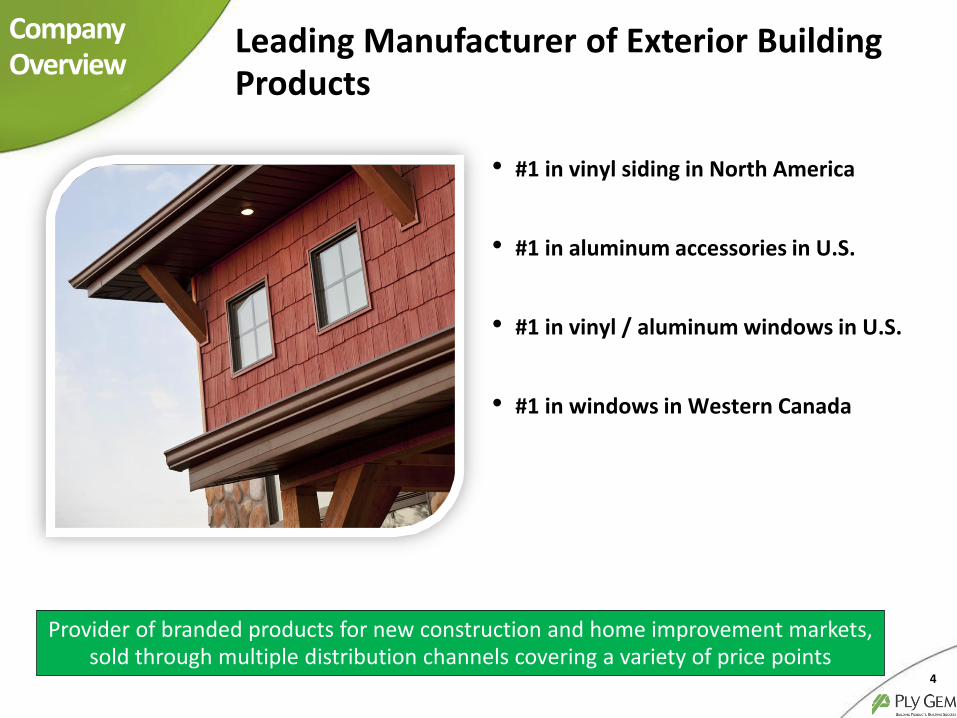

• #1 in vinyl siding in North America

• #1 in aluminum accessories in U.S.

• #1 in vinyl / aluminum windows in U.S.

• #1 in windows in Western Canada

Leading Manufacturer of Exterior Building Products

4

CompanyOverview

Provider of branded products for new construction and home improvement markets, sold through multiple distribution channels covering a variety of price points

Extensive Exterior Product Portfolio

5

CompanyOverview

Engineered roofing products

Gable vents and accessories

Gutter protection systems

Vinyl and aluminum soffitWindow mantles

Manufactured stoneVinyl and aluminum siding

ShuttersMounting blocks

Decorative corner posts

Rain removal systems

Door surround systems

Patio Doors

Windows

Rail and fencing

Outdoor structures

Exterior doors

PVC trim

• Provides differentiation for Ply Gem customers

• Provides a single sourcing opportunity

• Hits the sweet spot of an emerging trend

• Features NAHB Green Approved products

• Fulfills the “One Ply Gem” MISSION

Alexandria, VA Designed Exterior Remodel

BEFORE

Three Weeks later using The Designed Exterior concept

AFTER

Complete Exterior Solution Offering for CustomersCompanyOverview

6

Vinyl Siding Market Leader

• #1 vinyl siding manufacturer in North America (~39% share in the US)

• Vinyl siding has the largest share of cladding in the U.S. residential housing market and vinyl siding manufacturing is a consolidated industry with 4 participants holding over 90% share

• Strong trade brands

• Multi-channel distribution network servicing both new construction and R&R

• State-of-the-art automated manufacturing facilities with capacity

~$5,600

~$1,500$866

Exterior CladdingMarket Size

Vinyl SidingMarket Size

Ply Gem LTM 2Q16Net Sales

($ in mm)

Why Ply Gem Key Brands

North American Market Summary

7

CompanyOverview

(1)

Market size: According to Principia Partners.(1) Includes all product categories within Siding, Fencing & Stone segment

• #1 vinyl and aluminum window manufacturer in the U.S.

• #1 window and door manufacturer in Western Canada

• Multi-channel distribution network servicing both new construction and R&R covering every price point

• Highly efficient, vertically integrated production

• Continued to gain market share during downturn

$9,000

$1,015

Market Size Ply Gem LTM 2Q16Net Sales

($ in mm)

Market size: Company estimate – new construction and R&R.

~

Vinyl and Aluminum Windows Market Leader

Why Ply Gem Key Brands

North American Market Summary

8

CompanyOverview

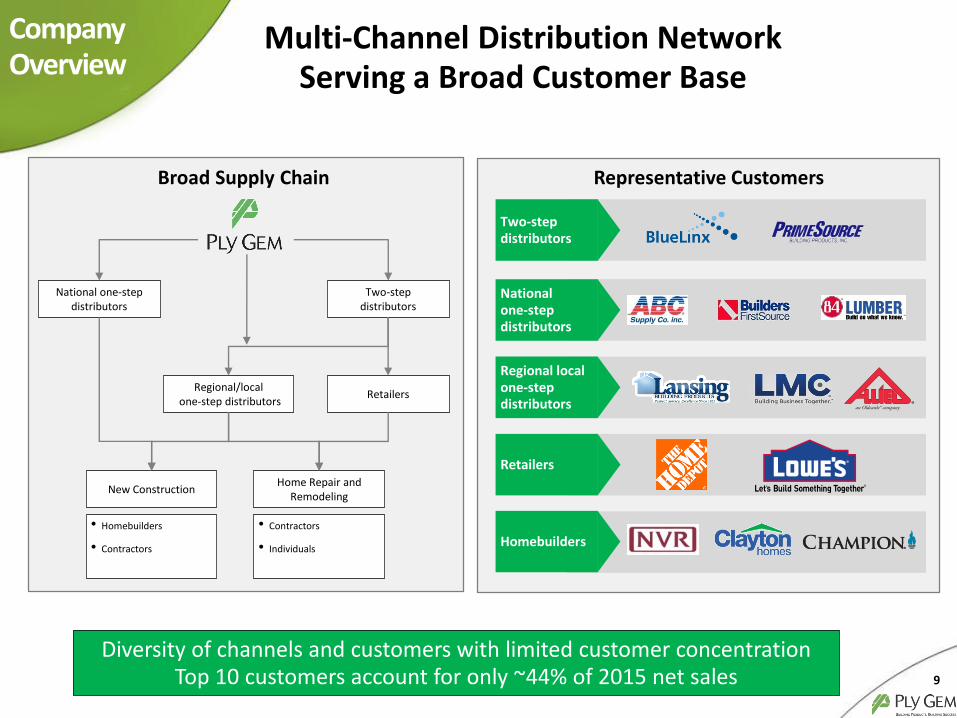

Regional local one-step distributors

Two-step distributors

National one-step distributors

Retailers

Homebuilders

New Construction

Regional/localone-step distributors

National one-stepdistributors

Retailers

Two-stepdistributors

Home Repair and Remodeling

• Homebuilders

• Contractors

• Contractors

• Individuals

Multi-Channel Distribution Network Serving a Broad Customer Base

CompanyOverview

9

Broad Supply Chain Representative Customers

Diversity of channels and customers with limited customer concentration Top 10 customers account for only ~44% of 2015 net sales

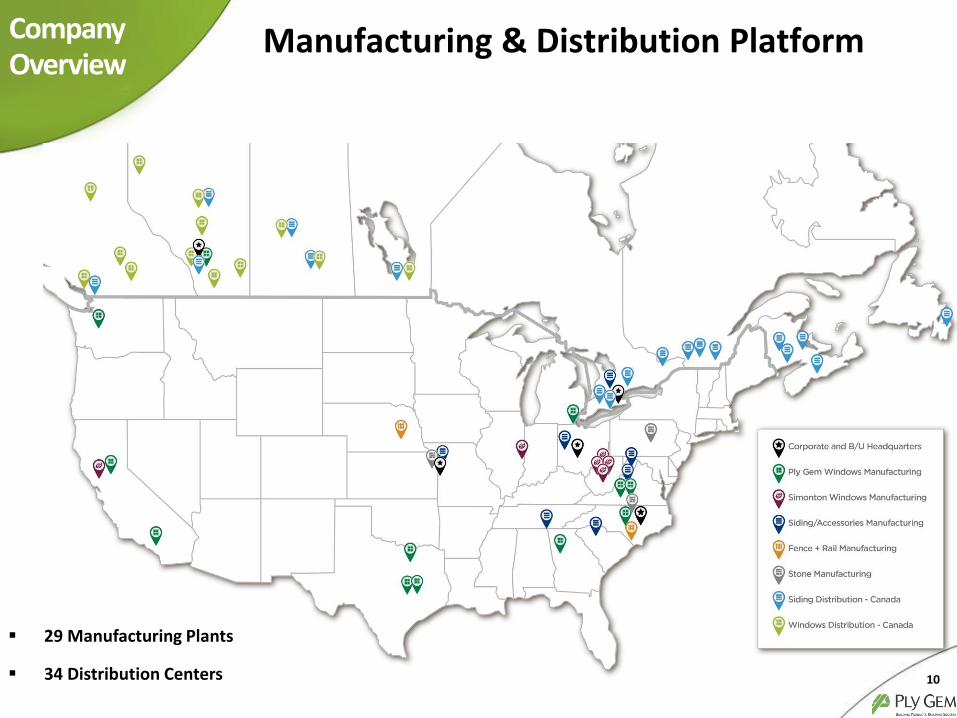

Manufacturing & Distribution Platform

10

CompanyOverview

29 Manufacturing Plants

34 Distribution Centers

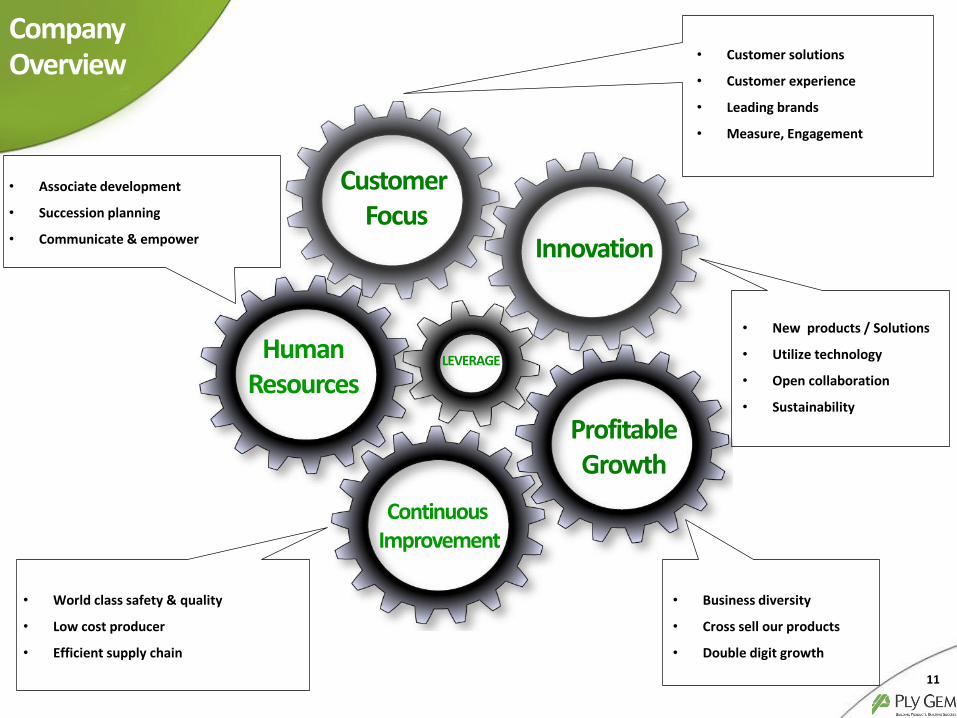

• Business diversity

• Cross sell our products

• Double digit growth

• World class safety & quality

• Low cost producer

• Efficient supply chain

Customer Focus

Innovation

ProfitableGrowth

Continuous Improvement

HumanResources

LEVERAGE

Company Overview

11

• Associate development

• Succession planning

• Communicate & empower

• Customer solutions

• Customer experience

• Leading brands

• Measure, Engagement

• New products / Solutions

• Utilize technology

• Open collaboration

• Sustainability

Market and Housing Update

Crisis of Confidence is Starting to Improve

13

MarketUpdate

-8.0

-3.0

2.0

7.0

4.0

6.0

8.0

10.0

40.0

60.0

80.0

100.0

2011 2012 2013 2014 2015 2016

Source: Bureau of Labor Statistics, Zillow, University of Michigan,Government of Canada, CREA, Conference Board of Canada

(*) Excluding Greater Vancouver and Greater Toronto

Unemployment RateAnnual Change in Home ValuesConsumer Sentiment

4.9%

5.4%

90.0

Canada

6.9%

8.4%(*)

104.6

U.S.

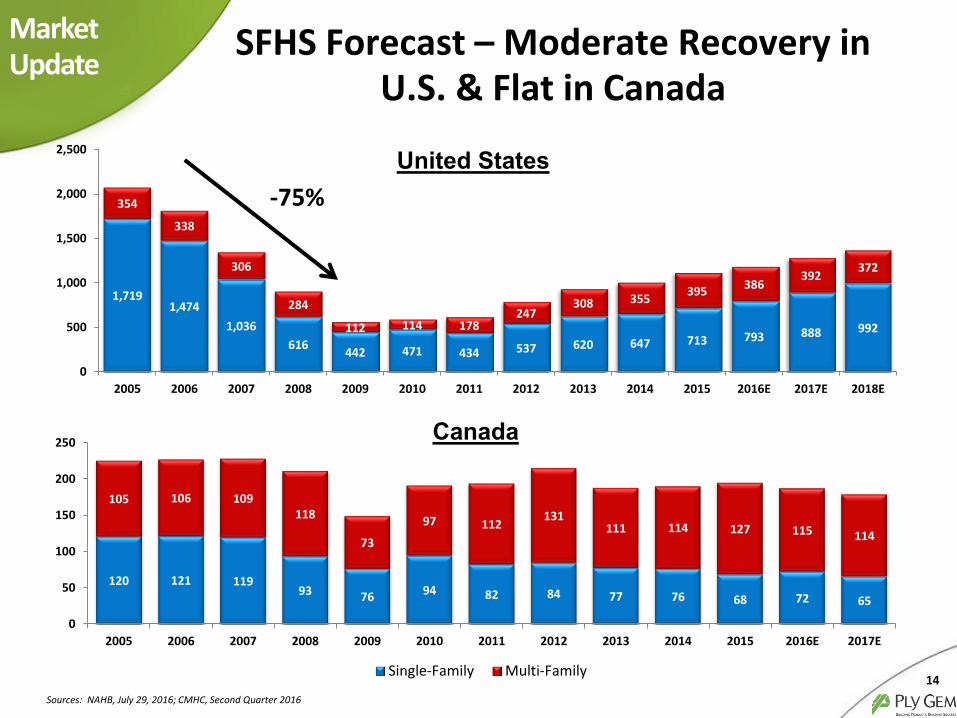

SFHS Forecast – Moderate Recovery in U.S. & Flat in Canada

14

MarketUpdate

1,7191,474

1,036

616442 471 434 537 620 647 713 793 888 992

354

338

306

284

112 114 178247

308 355395

386392

372

0

500

1,000

1,500

2,000

2,500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

120 121 11993 76 94 82 84 77 76 68 72 65

105 106 109118

73

97 112131

111 114 127 115 114

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Single-Family Multi-Family

United States

Canada

Sources: NAHB, July 29, 2016; CMHC, Second Quarter 2016

-75%

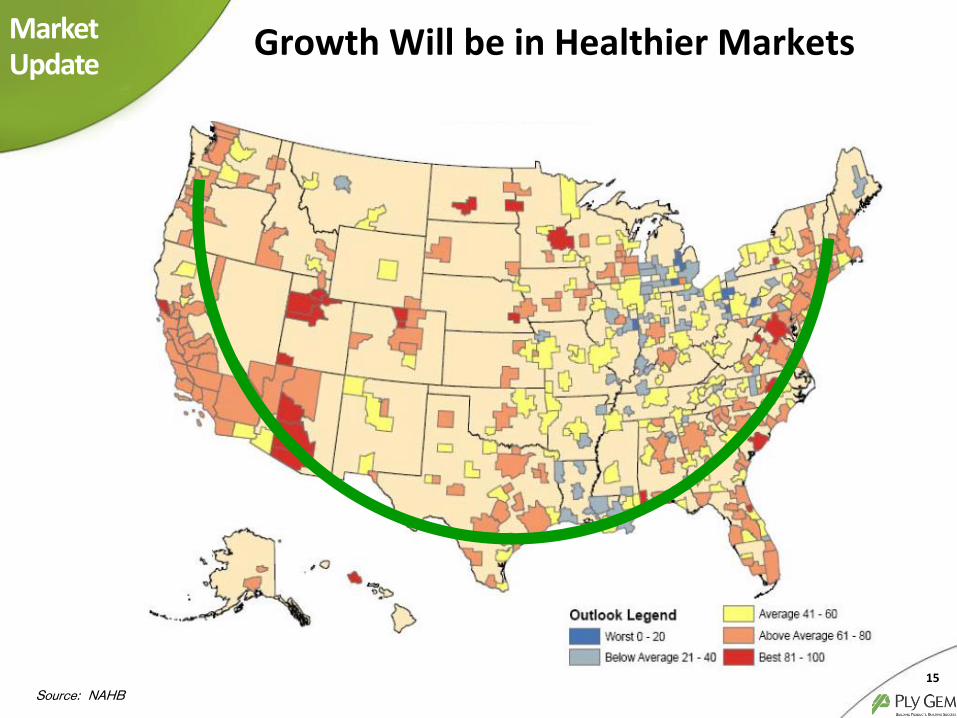

Growth Will be in Healthier Markets

15

MarketUpdate

Source: NAHB

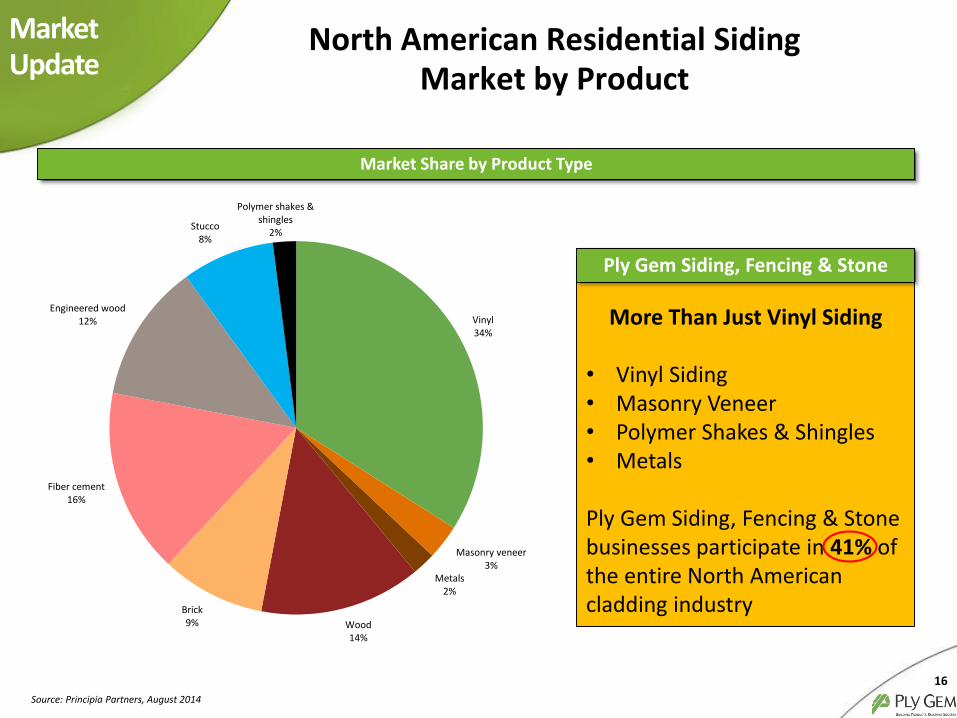

North American Residential Siding Market by Product

16

MarketUpdate

Source: Principia Partners, August 2014

Vinyl34%

Masonry veneer3%

Metals2%

Wood14%

Brick9%

Fiber cement16%

Engineered wood12%

Stucco8%

Polymer shakes & shingles

2%

Market Share by Product Type

More Than Just Vinyl Siding

• Vinyl Siding • Masonry Veneer • Polymer Shakes & Shingles• Metals

Ply Gem Siding, Fencing & Stone businesses participate in 41% of the entire North American cladding industry

Ply Gem Siding, Fencing & Stone

Vinyl Siding Regional Dominance

17

MarketUpdate

74%

57%

22%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Northeast U.S. Midwest U.S. South U.S. West U.S.

Vinyl Siding Brick Stucco Fiber Cement Wood Other

Source: 2015 U.S. Census Bureau

Vinyl Siding Share by Region

Median Age of Owner-Occupied Housing

18

MarketUpdate

Source: 2013 AHS, U.S. Census Bureau

27 27

29 2930

31 3132

3435

37

0

5

10

15

20

25

30

35

40

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Year

s o

f A

ge

• Aging trend signals a growing market for remodelers

• Implied additional demand for more new construction over longer term

• Approximately 2/3 of owner-occupied home in the U.S. were built before 1980

• Homes constructed after 2000 represent just 17% of the U.S. owner-occupied homes, with only 2% built after 2010

Top Growth Products for Replacement Contractors

19

55

3027

25 2421

1310

8

0

10

20

30

40

50

60

2014

Windows

Siding

Doors

Roofing

Bathtubs & Showers

Decking

Flooring

Kitchen Cabinets

Water Pipes

MarketUpdate

Source: Hanley Wood August 2013 Audience Survey

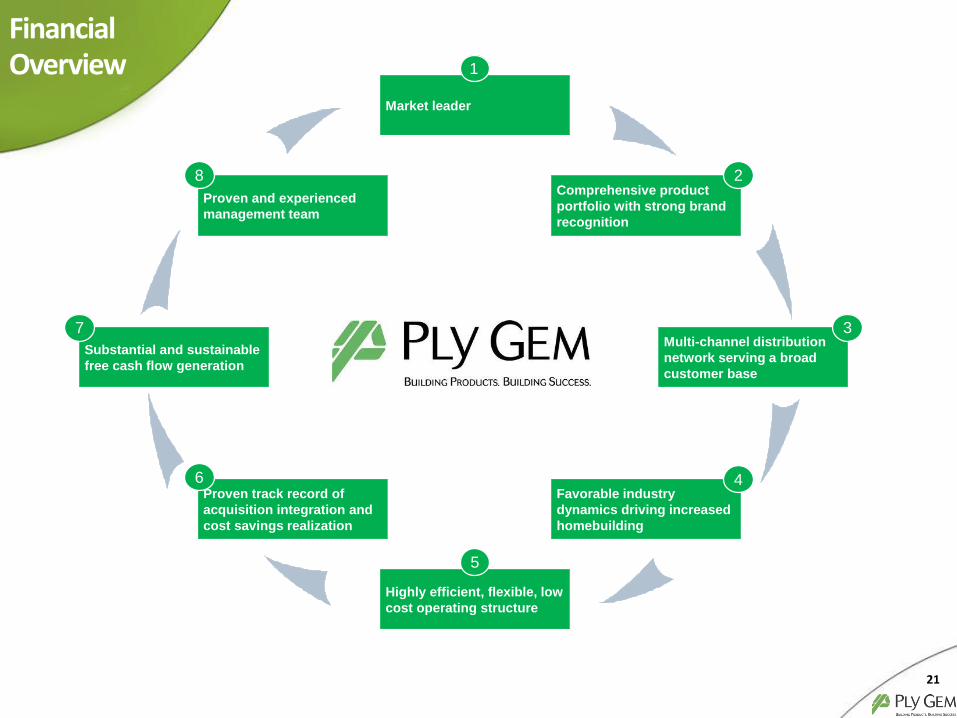

Financial Overview

Market leader

Highly efficient, flexible, low

cost operating structure

Comprehensive product

portfolio with strong brand

recognition

Proven and experienced

management team

Favorable industry

dynamics driving increased

homebuilding

Proven track record of

acquisition integration and

cost savings realization

Multi-channel distribution

network serving a broad

customer base

Substantial and sustainable

free cash flow generation

FinancialOverview 1

2

3

4

5

6

7

8

21

Proven Track Record of Acquisition Integration / Cost Savings Realization

AcquisitionSynergies

22

Expected Achieved

MW Windows

($331M)

2004 2005 2006 2007 2008

Alenco

Windows

($127M)

MHE (Alcoa) siding business

($296M)

CT Windows

($37M)

United Stone

Veneer

($4M)

Ply Gem

purchased

by CI Capital

Expected Achieved Expected Achieved

2013

Gienow

(CAD$20M)

Acq

uis

itio

ns

Co

st s

avin

gs($

in M

)

Mitten

(CAD$79M)

$6.8$11.0 $4.0 $4.9

$22.0

$55.0

2014

Simonton

($130M)

2015

Canyon

Stone

($21M)

Acquisitions provide incremental capabilities and growth along with significant synergy opportunities

• Expected and realized $18.1M in cost savings for combined Gienow / Mitten acquisitions

• Simonton acquisition cost savings and synergies expected to be $18.0M

• Canyon Stone acquisition cost savings and synergies expected to be $1.0M

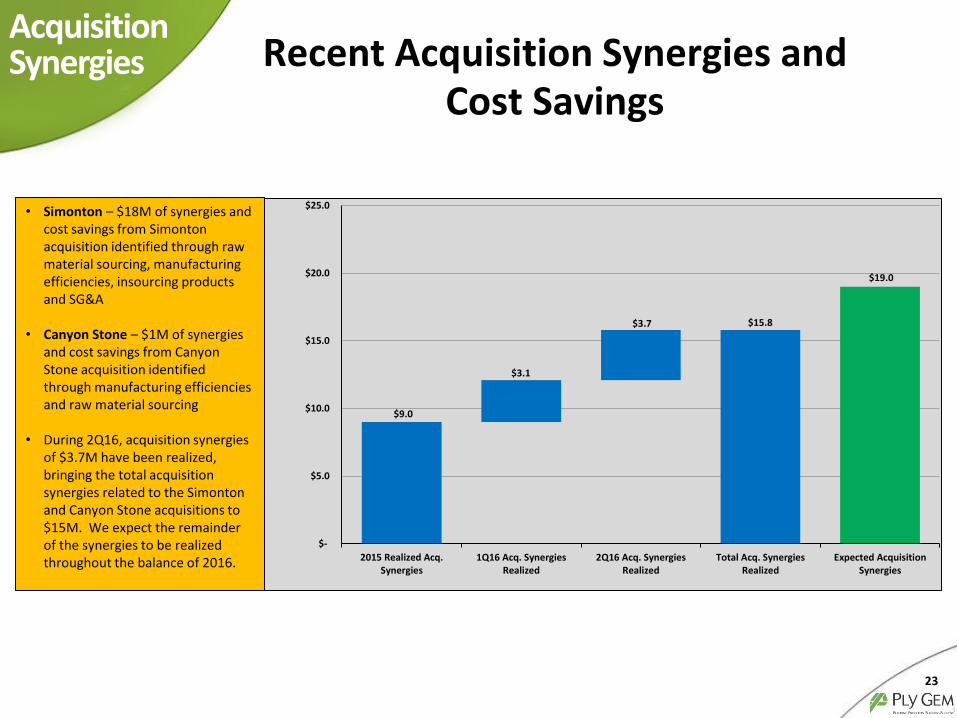

Recent Acquisition Synergies and Cost Savings

AcquisitionSynergies

• Simonton – $18M of synergies and cost savings from Simonton acquisition identified through raw material sourcing, manufacturing efficiencies, insourcing products and SG&A

• Canyon Stone – $1M of synergies and cost savings from Canyon Stone acquisition identified through manufacturing efficiencies and raw material sourcing

• During 2Q16, acquisition synergies of $3.7M have been realized, bringing the total acquisition synergies related to the Simonton and Canyon Stone acquisitions to $15M. We expect the remainder of the synergies to be realized throughout the balance of 2016.

$15.8

$19.0

$9.0

$3.1

$3.7

$-

$5.0

$10.0

$15.0

$20.0

$25.0

2015 Realized Acq.Synergies

1Q16 Acq. SynergiesRealized

2Q16 Acq. SynergiesRealized

Total Acq. SynergiesRealized

Expected AcquisitionSynergies

23

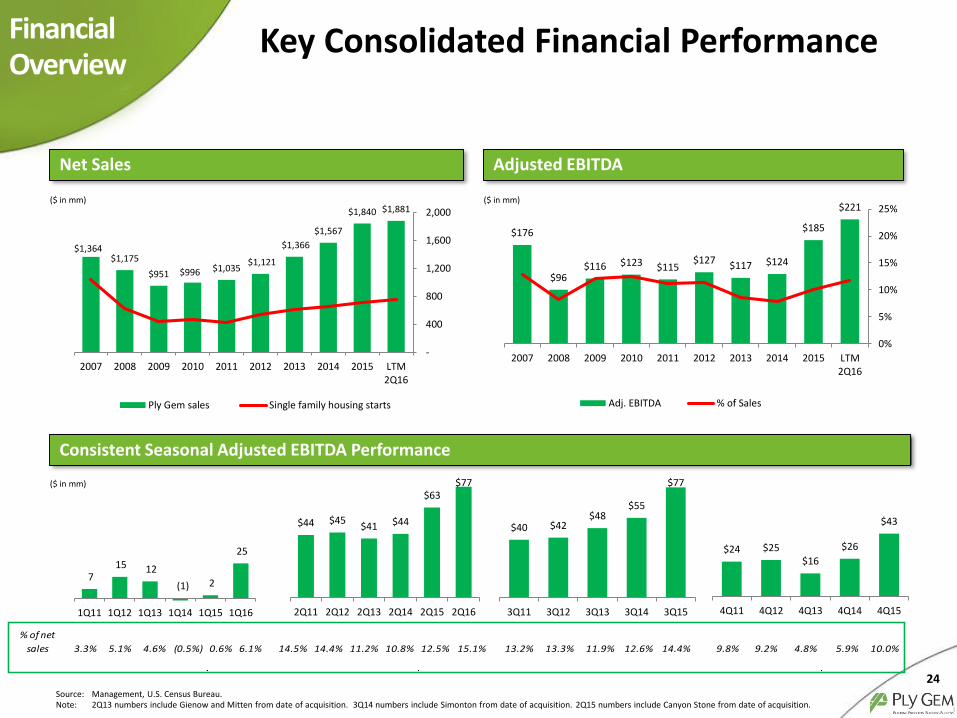

Net Sales Adjusted EBITDA

$176

$96$116 $123 $115

$127$117 $124

$185

$221

0%

5%

10%

15%

20%

25%

2007 2008 2009 2010 2011 2012 2013 2014 2015 LTM2Q16

Adj. EBITDA % of Sales

$1,364$1,175

$951 $996 $1,035$1,121

$1,366

$1,567

$1,840 $1,881

-

400

800

1,200

1,600

2,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 LTM2Q16

Ply Gem sales Single family housing starts

Key Consolidated Financial Performance

($ in mm)($ in mm)

Source: Management, U.S. Census Bureau.Note: 2Q13 numbers include Gienow and Mitten from date of acquisition. 3Q14 numbers include Simonton from date of acquisition. 2Q15 numbers include Canyon Stone from date of acquisition.

24

FinancialOverview

Consistent Seasonal Adjusted EBITDA Performance

7 15 12

(1) 2

25

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16

$44 $45$41 $44

$63$77

2Q11 2Q12 2Q13 2Q14 2Q15 2Q16

$24 $25$16

$26

$43

4Q11 4Q12 4Q13 4Q14 4Q15

$40 $42$48

$55

$77

3Q11 3Q12 3Q13 3Q14 3Q15

% of net

sales 3.3% 5.1% 4.6% (0.5%) 0.6% 6.1% 14.5% 14.4% 11.2% 10.8% 12.5% 15.1% 13.2% 13.3% 11.9% 12.6% 14.4% 9.8% 9.2% 4.8% 5.9% 10.0%

($ in mm)

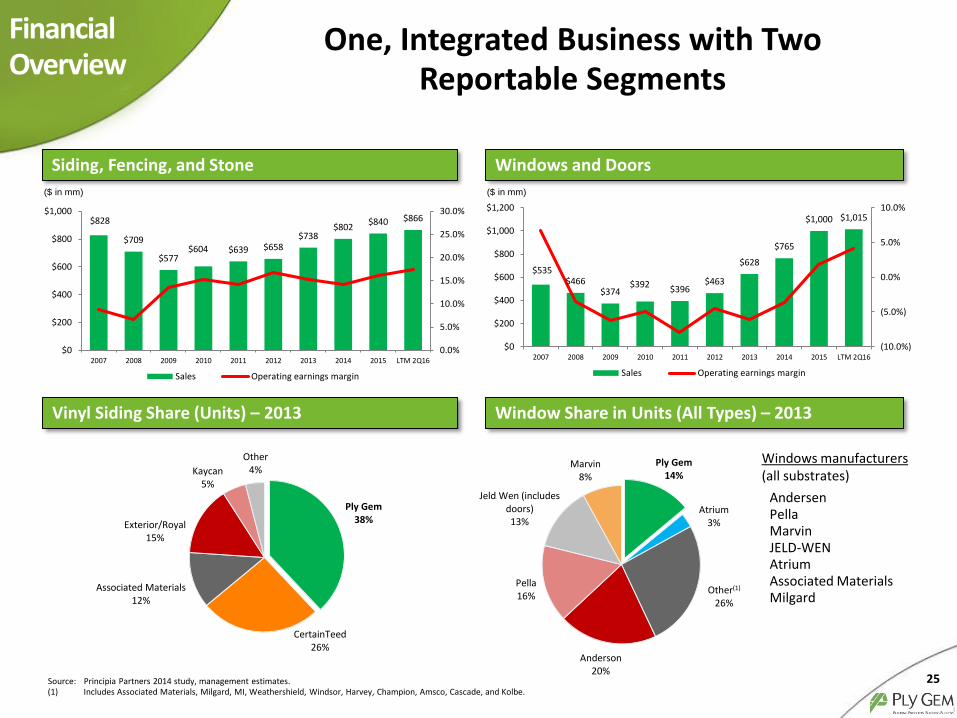

Ply Gem38%

CertainTeed26%

Associated Materials12%

Exterior/Royal15%

Kaycan5%

Other4%

Ply Gem14%

Atrium3%

Other(1)

26%

Pella16%

Jeld Wen (includes doors)13%

Marvin8%

Anderson 20%

$535$466

$374$392 $396

$463

$628

$765

$1,000 $1,015

(10.0%)

(5.0%)

0.0%

5.0%

10.0%

$0

$200

$400

$600

$800

$1,000

$1,200

2007 2008 2009 2010 2011 2012 2013 2014 2015 LTM 2Q16

Sales Operating earnings margin

AndersenPellaMarvinJELD-WENAtriumAssociated MaterialsMilgard

Windows manufacturers(all substrates)

Source: Principia Partners 2014 study, management estimates.

One, Integrated Business with Two Reportable Segments

($ in mm) ($ in mm)

Siding, Fencing, and Stone Windows and Doors

Window Share in Units (All Types) – 2013Vinyl Siding Share (Units) – 2013

25

FinancialOverview

(1) Includes Associated Materials, Milgard, MI, Weathershield, Windsor, Harvey, Champion, Amsco, Cascade, and Kolbe.

$828

$709

$577$604 $639 $658

$738$802

$840 $866

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$0

$200

$400

$600

$800

$1,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 LTM 2Q16

Sales Operating earnings margin

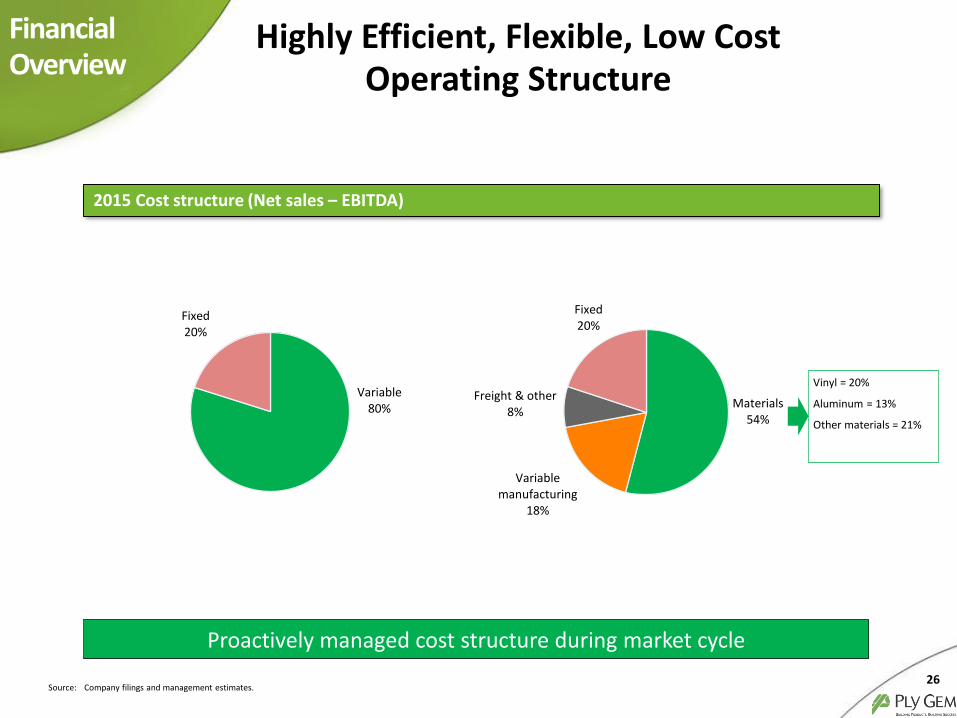

2015 Cost structure (Net sales – EBITDA)

Variable80%

Fixed20%

Materials54%

Variable manufacturing

18%

Freight & other8%

Fixed20%

Vinyl = 20%

Aluminum = 13%

Other materials = 21%

Highly Efficient, Flexible, Low Cost Operating Structure

Source: Company filings and management estimates.26

FinancialOverview

Proactively managed cost structure during market cycle

$20$17

$8$11 $11

$25 $26$24

$34$38

0.0%

1.0%

2.0%

3.0%

4.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 LTM2Q16

Capex % of Sales

FCF: Adjusted EBITDA – Capital Expenditures Capital Spending

$390

$650

2016 2017 2018 2019 2020 2021 2022

ABL Term Loan Senior Notes

Debt Maturity – 2Q16

Substantial / Sustainable Free Cash Flow

History of strong EBITDA performance, modest capital expenditure requirements and efficient use of working capital27

FinancialOverview

$156

$80

$108 $112$103 $103

$91$101

$151

$183

2007 2008 2009 2010 2011 2012 2013 2014 2015 LTM2Q16

($ in mm) ($ in mm)

($ in mm)

No near-term maturities

28

8.9

7.8

6.7

8.4

5.2 4.9

4.4

-

2.0

4.0

6.0

8.0

10.0

2011 2012 2013 2014 2015 1Q16 LTM 2Q16 LTM

Leve

rage

Rat

io

Leverage Ratio

($ in Millions) 2011 2012 2013 2014 2015 1Q16 LTM 2Q16 LTM

Senior Notes $950.0 $1,000.0 $852.0 $650.0 $650.0 $650.0 $650.0

Term Loan Facility - - - 426.8 422.5 391.4 390.3

ABL 55.0 15.0 - - - 10.0 -

Total Debt $1,005.0 $1,015.0 $852.0 $1,076.8 $1,072.5 $1,051.4 $1,040.3

Cash 11.7 27.2 69.8 33.2 109.4 34.3 64.5

Net Debt $993.3 $987.8 $782.2 $1,043.6 $963.1 $1,017.1 $975.8

Adj. EBITDA $112.2 $126.8 $117.5 $124.2 $184.6 $207.1 $221.4

Interest Coverage 1.2 1.3 1.4 1.9 3.1 3.4 3.7

Leverage Ratio 8.9 7.8 6.7 8.4 5.2 4.9 4.4

Historical Leverage Ratio

Significant De-Leveraging

One-Half Turn Improvement

in 2Q16

29

$-

$100

$200

$300

$400

2007 Trough LTM 2Q16 Mid-Cycle

Adjusted EBITDA(in millions)

Previous Mid-Cycle (2007)

Cycle Trough (2009-2011)

LTM 2Q16 Future Mid-Cycle

U.S. Single Family Housing Starts (in thousands) 1,036 450 760 (*) 1,000

Net Sales $1.4B $0.9B $1.9B ~$2.8B

Gross Margin 20.6% 21.1% 24.3% >25%

Adj. EBITDA $176M $118M $221.4M ~$350M - $400M

• The U.S. housing market can support approximately 1 million single family housing starts based on current household formation rates

• Gross margin improvement from leverage on volume, regional/custom builders returning to the market, and continued pricing discipline within the window industry

Mid-CycleOutlook Mid-Cycle Outlook

(*) Source: U.S. Census Bureau

Appendix

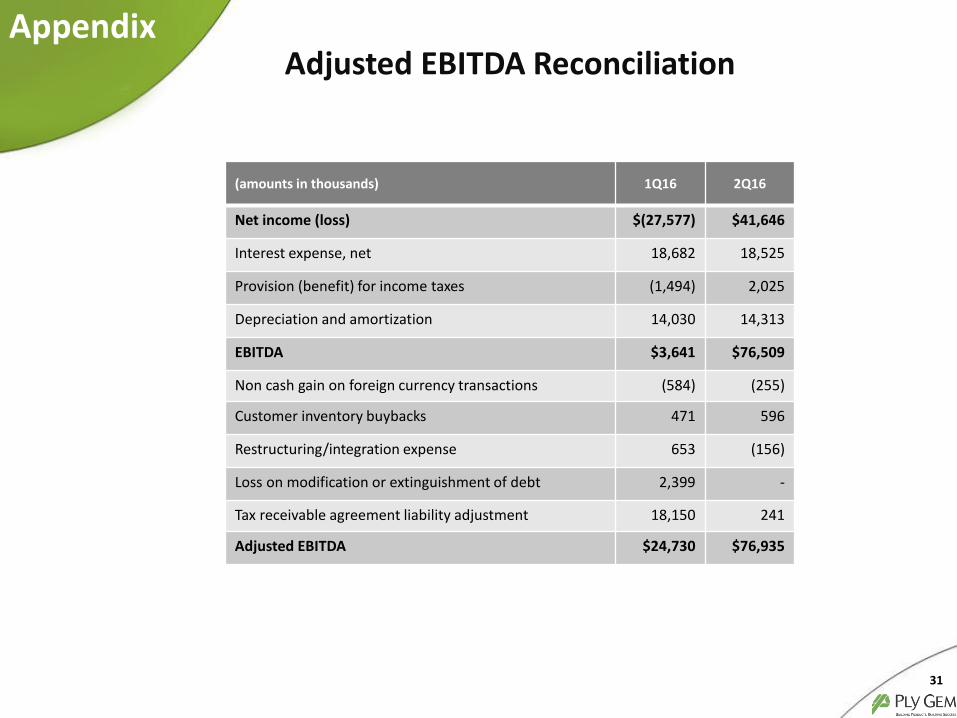

(amounts in thousands) 1Q16 2Q16

Net income (loss) $(27,577) $41,646

Interest expense, net 18,682 18,525

Provision (benefit) for income taxes (1,494) 2,025

Depreciation and amortization 14,030 14,313

EBITDA $3,641 $76,509

Non cash gain on foreign currency transactions (584) (255)

Customer inventory buybacks 471 596

Restructuring/integration expense 653 (156)

Loss on modification or extinguishment of debt 2,399 -

Tax receivable agreement liability adjustment 18,150 241

Adjusted EBITDA $24,730 $76,935

Appendix

31

Adjusted EBITDA Reconciliation

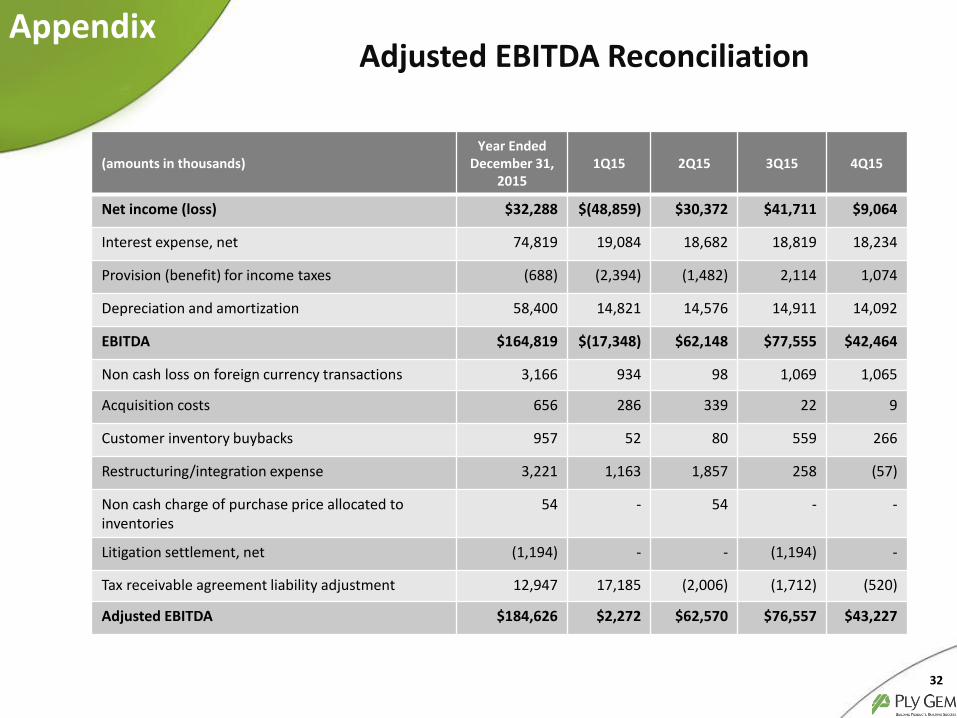

(amounts in thousands)Year Ended

December 31, 2015

1Q15 2Q15 3Q15 4Q15

Net income (loss) $32,288 $(48,859) $30,372 $41,711 $9,064

Interest expense, net 74,819 19,084 18,682 18,819 18,234

Provision (benefit) for income taxes (688) (2,394) (1,482) 2,114 1,074

Depreciation and amortization 58,400 14,821 14,576 14,911 14,092

EBITDA $164,819 $(17,348) $62,148 $77,555 $42,464

Non cash loss on foreign currency transactions 3,166 934 98 1,069 1,065

Acquisition costs 656 286 339 22 9

Customer inventory buybacks 957 52 80 559 266

Restructuring/integration expense 3,221 1,163 1,857 258 (57)

Non cash charge of purchase price allocated to inventories

54 - 54 - -

Litigation settlement, net (1,194) - - (1,194) -

Tax receivable agreement liability adjustment 12,947 17,185 (2,006) (1,712) (520)

Adjusted EBITDA $184,626 $2,272 $62,570 $76,557 $43,227

Appendix

32

Adjusted EBITDA Reconciliation

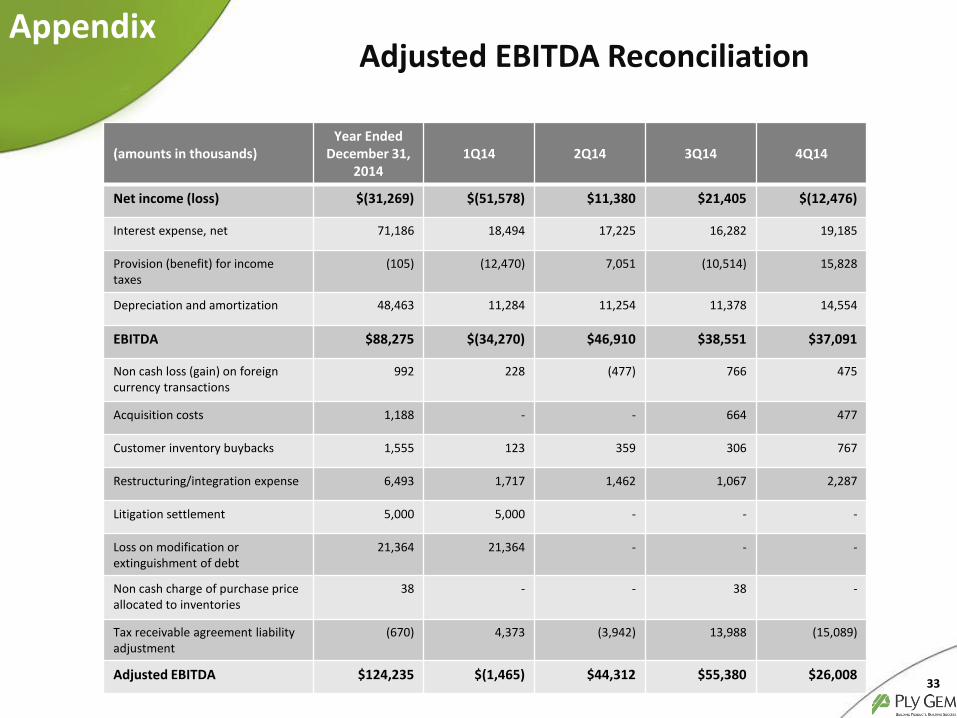

(amounts in thousands)Year Ended

December 31, 2014

1Q14 2Q14 3Q14 4Q14

Net income (loss) $(31,269) $(51,578) $11,380 $21,405 $(12,476)

Interest expense, net 71,186 18,494 17,225 16,282 19,185

Provision (benefit) for income taxes

(105) (12,470) 7,051 (10,514) 15,828

Depreciation and amortization 48,463 11,284 11,254 11,378 14,554

EBITDA $88,275 $(34,270) $46,910 $38,551 $37,091

Non cash loss (gain) on foreign currency transactions

992 228 (477) 766 475

Acquisition costs 1,188 - - 664 477

Customer inventory buybacks 1,555 123 359 306 767

Restructuring/integration expense 6,493 1,717 1,462 1,067 2,287

Litigation settlement 5,000 5,000 - - -

Loss on modification or extinguishment of debt

21,364 21,364 - - -

Non cash charge of purchase price allocated to inventories

38 - - 38 -

Tax receivable agreement liability adjustment

(670) 4,373 (3,942) 13,988 (15,089)

Adjusted EBITDA $124,235 $(1,465) $44,312 $55,380 $26,008

Appendix

33

Adjusted EBITDA Reconciliation

(amounts in thousands)Year Ended

December 31, 2013

1Q13 2Q13 3Q13 4Q13

Net income (loss) $(79,520) $(28,107) $(50,877) $16,895 $(17,431)

Interest expense, net 91,684 23,653 24,833 21,760 21,438

Provision (benefit) for income taxes 298 3,849 (731) (1,442) (1,378)

Depreciation and amortization 45,646 9,715 11,171 12,097 12,663

EBITDA $58,108 $9,110 $(15,604) $49,310 $15,292

Non cash loss (gain) on foreign currency transactions

1,533 33 346 376 778

Acquisition costs 1,490 315 1,025 150 -

Customer inventory buybacks 4,837 - 2,172 2,503 162

Restructuring/integration expense 11,759 2,380 1,439 1,529 6,411

Non cash charge of purchase price allocated to inventories

2,015 - 883 1,132 -

Management fee 410 235 175 - -

Loss on modification or extinguishment of debt

18,948 - 18,948 - -

Initial public offering costs 23,527 - 23,527 - -

Tax receivable agreement liability adjustment

(5,167) - 8,143 (6,669) (6,641)

Adjusted EBITDA $117,460 $12,073 $41,054 $48,331 $16,002

Appendix

34

Adjusted EBITDA Reconciliation

(amounts in thousands)Year Ended

December 31, 2012

1Q12 2Q12 3Q12 4Q12

Net income (loss) $(39,055) $(25,642) $5,267 $(3,673) $(15,007)

Interest expense, net 103,042 25,041 25,919 27,526 24,557

Provision (benefit) for income taxes

2,835 1,872 (204) (89) 1,256

Depreciation and amortization 52,277 13,317 13,189 13,073 12,698

EBITDA $119,099 $14,588 $44,171 $36,837 $23,504

Non cash loss (gain) on foreign currency transactions

(409) (68) (96) (100) (145)

Customer inventory buybacks 768 445 119 59 144

Restructuring/integration expense

1,677 - 152 339 1,186

Management fee 2,520 302 902 859 457

Loss on modification or extinguishment of debt

3,607 - - 3,607 -

Adjusted EBITDA $127,262 $15,267 $45,248 $41,601 $25,146

Appendix

35

Adjusted EBITDA Reconciliation

(amounts in thousands)Year Ended

December 31, 2011

1Q11 2Q11 3Q11 4Q11

Net income (loss) $(84,507) $(70,892) $2,063 $(458) $(15,220)

Interest expense, net 101,384 26,424 24,911 25,176 24,873

Provision (benefit) for income taxes

683 2,472 (959) 466 (1,296)

Depreciation and amortization 54,020 13,690 13,393 13,471 13,466

EBITDA $71,580 $(28,306) $39,408 $38,655 $21,823

Non cash loss (gain) on foreign currency transactions

(492) (133) (218) (115) (26)

Environmental remediation 1,580 - - - 1,580

Customer inventory buybacks 10,087 6,692 2,971 315 110

Restructuring/integration expense

1,616 429 477 547 163

Gain on modification or extinguishment of debt

27,863 27,863 - - -

Management fee 2,267 100 900 800 467

Adjusted EBITDA $114,501 $6,645 $43,538 $40,201 $24,117

Appendix

36

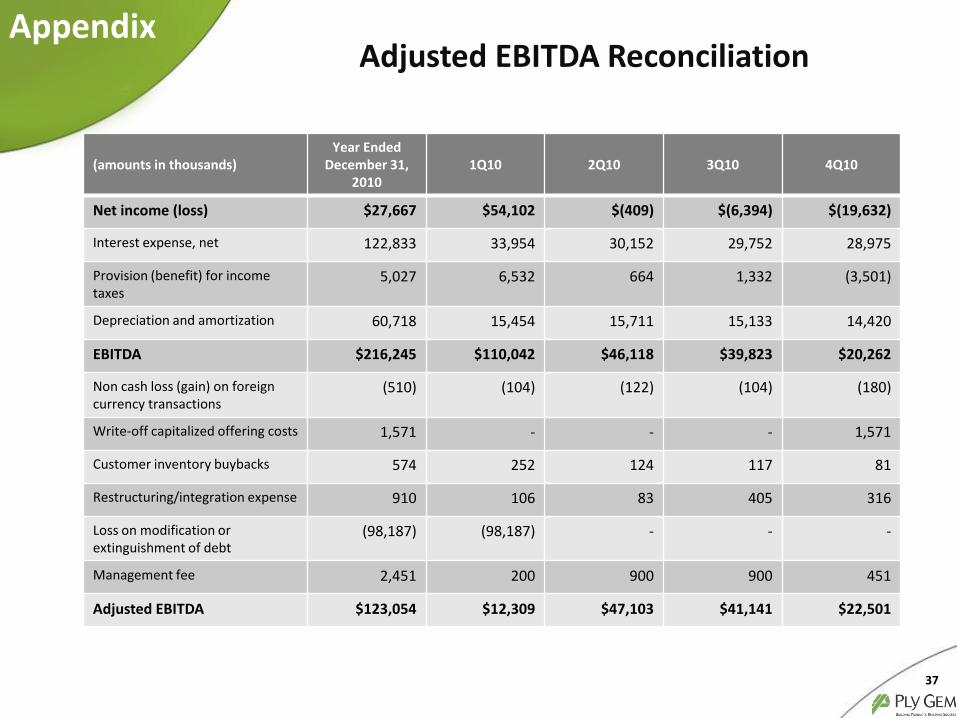

Adjusted EBITDA Reconciliation

(amounts in thousands)Year Ended

December 31, 2010

1Q10 2Q10 3Q10 4Q10

Net income (loss) $27,667 $54,102 $(409) $(6,394) $(19,632)

Interest expense, net 122,833 33,954 30,152 29,752 28,975

Provision (benefit) for income taxes

5,027 6,532 664 1,332 (3,501)

Depreciation and amortization 60,718 15,454 15,711 15,133 14,420

EBITDA $216,245 $110,042 $46,118 $39,823 $20,262

Non cash loss (gain) on foreign currency transactions

(510) (104) (122) (104) (180)

Write-off capitalized offering costs 1,571 - - - 1,571

Customer inventory buybacks 574 252 124 117 81

Restructuring/integration expense 910 106 83 405 316

Loss on modification or extinguishment of debt

(98,187) (98,187) - - -

Management fee 2,451 200 900 900 451

Adjusted EBITDA $123,054 $12,309 $47,103 $41,141 $22,501

Appendix

37

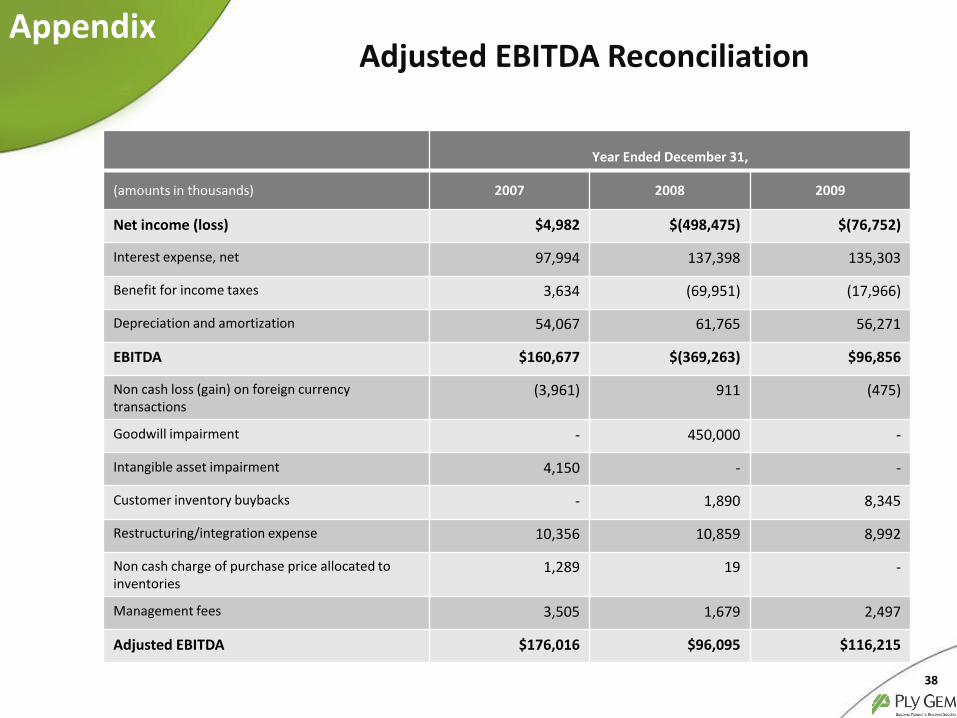

Adjusted EBITDA Reconciliation

Year Ended December 31,

(amounts in thousands) 2007 2008 2009

Net income (loss) $4,982 $(498,475) $(76,752)

Interest expense, net 97,994 137,398 135,303

Benefit for income taxes 3,634 (69,951) (17,966)

Depreciation and amortization 54,067 61,765 56,271

EBITDA $160,677 $(369,263) $96,856

Non cash loss (gain) on foreign currency transactions

(3,961) 911 (475)

Goodwill impairment - 450,000 -

Intangible asset impairment 4,150 - -

Customer inventory buybacks - 1,890 8,345

Restructuring/integration expense 10,356 10,859 8,992

Non cash charge of purchase price allocated to inventories

1,289 19 -

Management fees 3,505 1,679 2,497

Adjusted EBITDA $176,016 $96,095 $116,215

Adjusted EBITDA ReconciliationAppendix

38