Idiomas

Páginas

Jurídico

Confidential. © 2019 IHS Markit®. All Rights Reserved.

Cambios y tendencias económicas y del

mercado automotor: Perú

Encuentro AutomotorGuido Vildozo, Senior Manager, Americas Light Vehicle Sales Forecasts

Lima, 17 de Diciembre 2019

Confidential. © 2019 IHS Markit®. All Rights Reserved. 2

IHS Markit es una

compañía de ciencia

informática.

Con conocimiento en las

industrias globales mas

relevantes, utilizamos

tecnología y ciencia para

proveer datos, software y

perspectivas que permitan

a nuestros clientes tomar

decisiones informadas.

Confidential. © 2019 IHS MarkitTM. All Rights Reserved.

2008 2010 2013 20172016

Confidential. © 2019 IHS Markit®. All Rights Reserved.

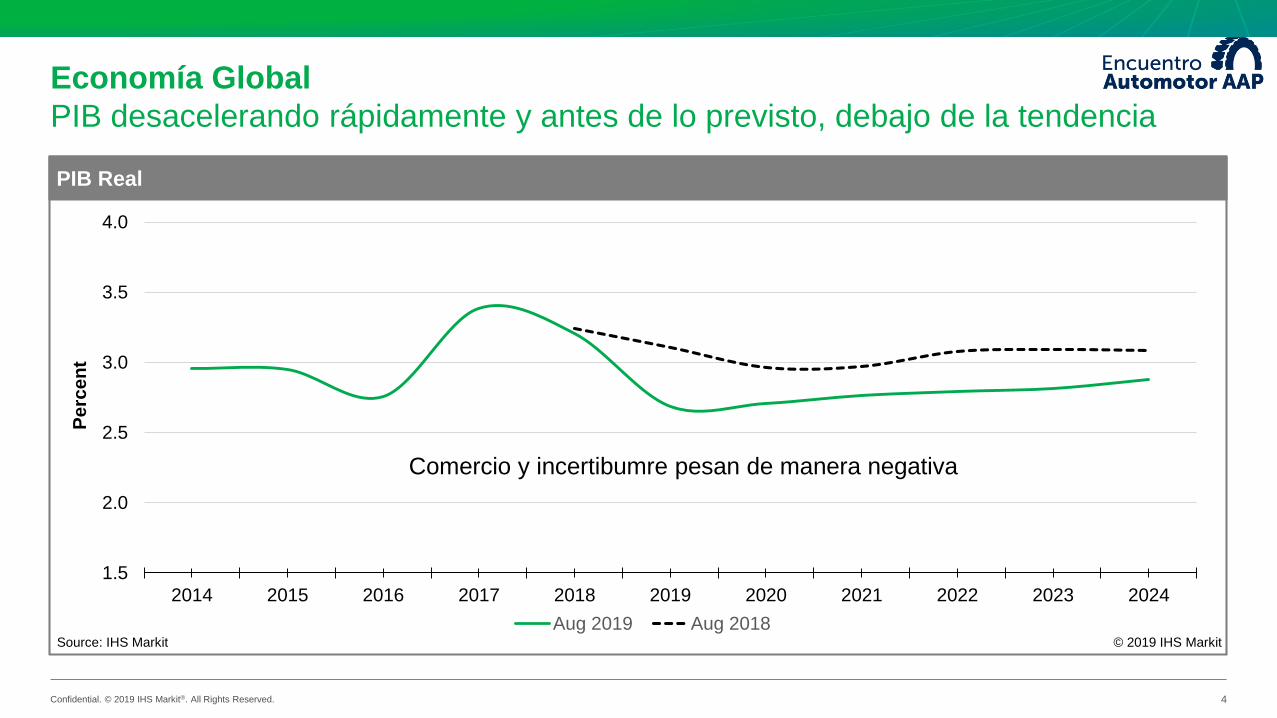

Economía Global

PIB desacelerando rápidamente y antes de lo previsto, debajo de la tendencia

4

Source: IHS Markit © 2019 IHS Markit

1.5

2.0

2.5

3.0

3.5

4.0

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Aug 2019 Aug 2018

Comercio y incertibumre pesan de manera negativa

PIB Real

Pe

rce

nt

Confidential. © 2019 IHS Markit®. All Rights Reserved.

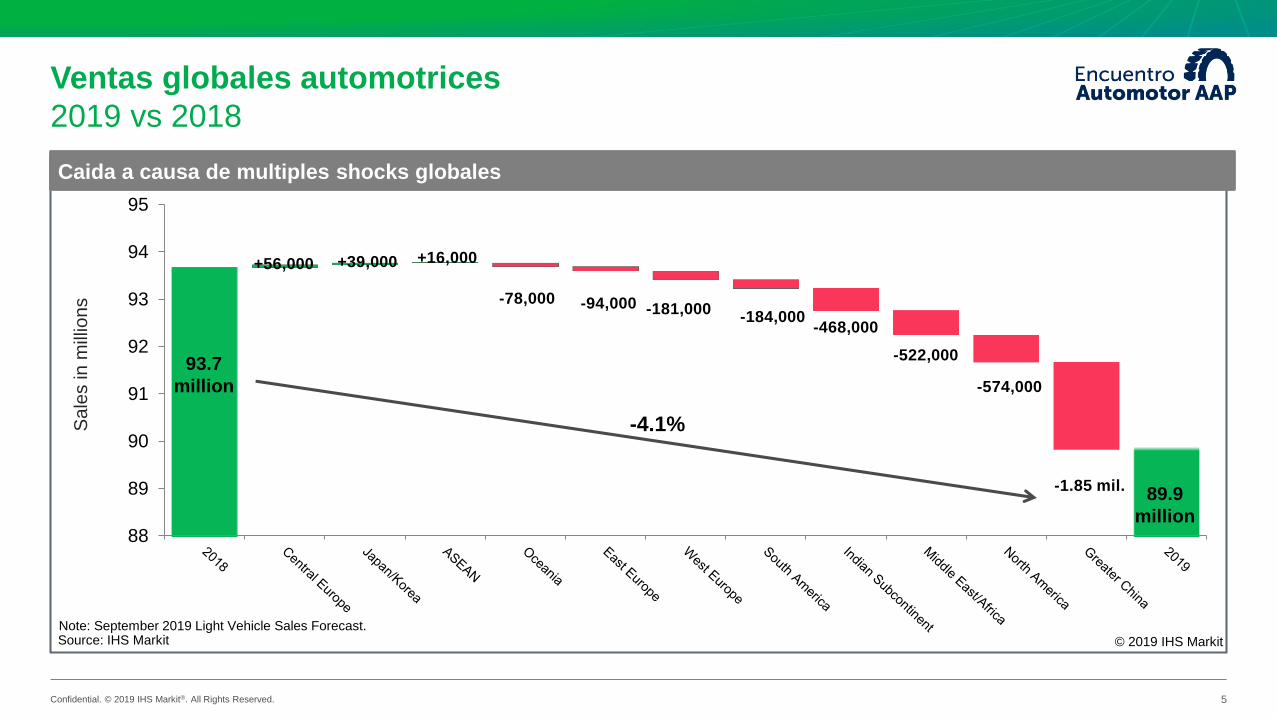

Ventas globales automotrices

2019 vs 2018

5

88

89

90

91

92

93

94

95

93.7

million

-4.1%Sa

les in

mill

ion

s

89.9

million

Caida a causa de multiples shocks globales

+56,000 +39,000 +16,000

-78,000 -94,000 -181,000

-522,000

-574,000

-1.85 mil.

Source: IHS Markit © 2019 IHS Markit

-184,000-468,000

Note: September 2019 Light Vehicle Sales Forecast.

Confidential. © 2019 IHS Markit®. All Rights Reserved.

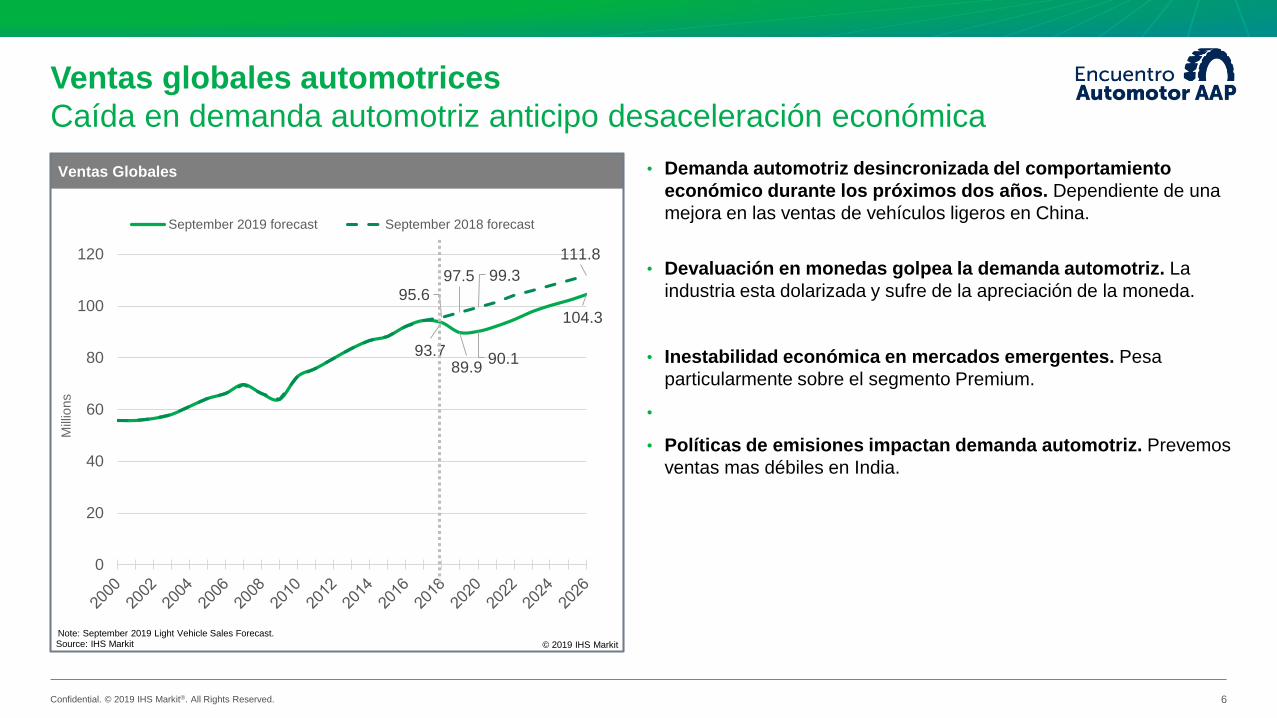

93.789.9

90.1

104.3

95.6

97.5 99.3

111.8

0

20

40

60

80

100

120

September 2019 forecast September 2018 forecast

Ventas globales automotrices

Caída en demanda automotriz anticipo desaceleración económica

• Demanda automotriz desincronizada del comportamiento

económico durante los próximos dos años. Dependiente de una

mejora en las ventas de vehículos ligeros en China.

• Devaluación en monedas golpea la demanda automotriz. La

industria esta dolarizada y sufre de la apreciación de la moneda.

• Inestabilidad económica en mercados emergentes. Pesa

particularmente sobre el segmento Premium.

•

• Políticas de emisiones impactan demanda automotriz. Prevemos

ventas mas débiles en India.

6

Source: IHS Markit

Ventas Globales

© 2019 IHS Markit

Mill

ions

Note: September 2019 Light Vehicle Sales Forecast.

Confidential. © 2019 IHS Markit®. All Rights Reserved.

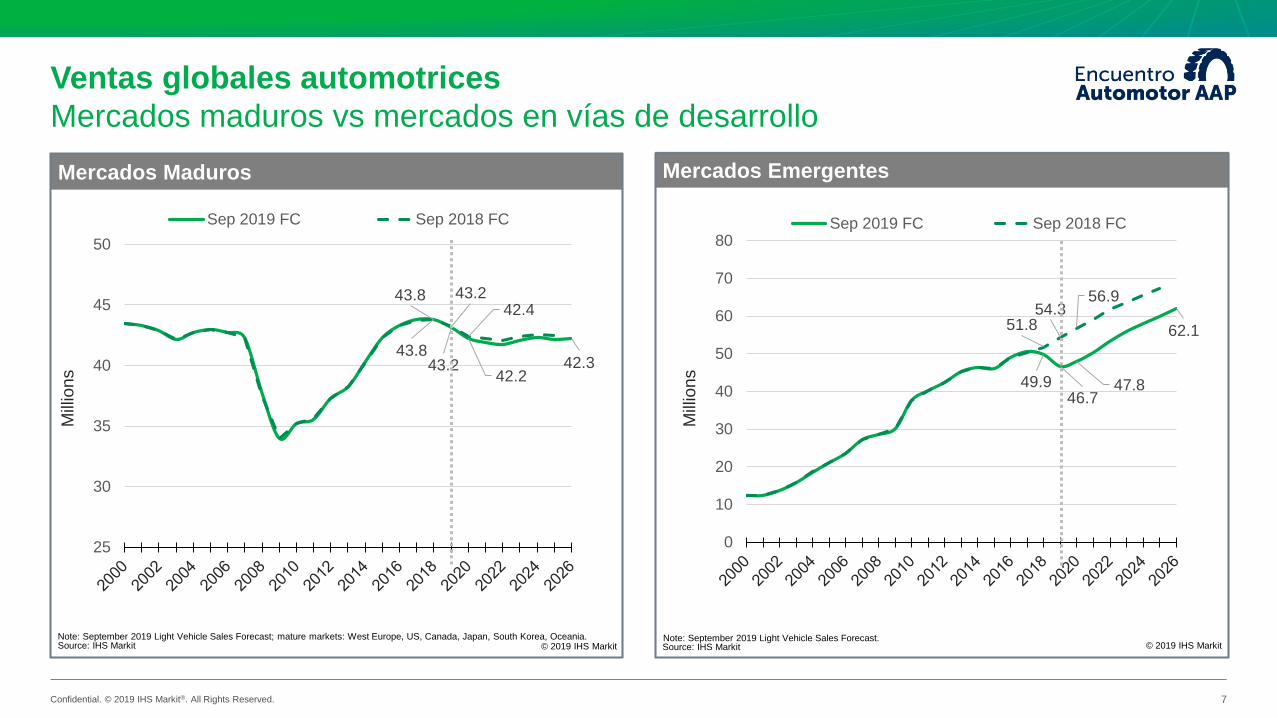

Ventas globales automotrices

Mercados maduros vs mercados en vías de desarrollo

7

43.843.2

42.242.3

43.8 43.242.4

25

30

35

40

45

50

Sep 2019 FC Sep 2018 FC

Source: IHS Markit

Mercados Maduros

© 2019 IHS Markit

Mill

ions

49.946.7

47.8

62.151.854.3

56.9

0

10

20

30

40

50

60

70

80Sep 2019 FC Sep 2018 FC

Source: IHS Markit

Mercados Emergentes

© 2019 IHS Markit

Mill

ions

Note: September 2019 Light Vehicle Sales Forecast; mature markets: West Europe, US, Canada, Japan, South Korea, Oceania. Note: September 2019 Light Vehicle Sales Forecast.

Confidential. © 2019 IHS Markit®. All Rights Reserved.

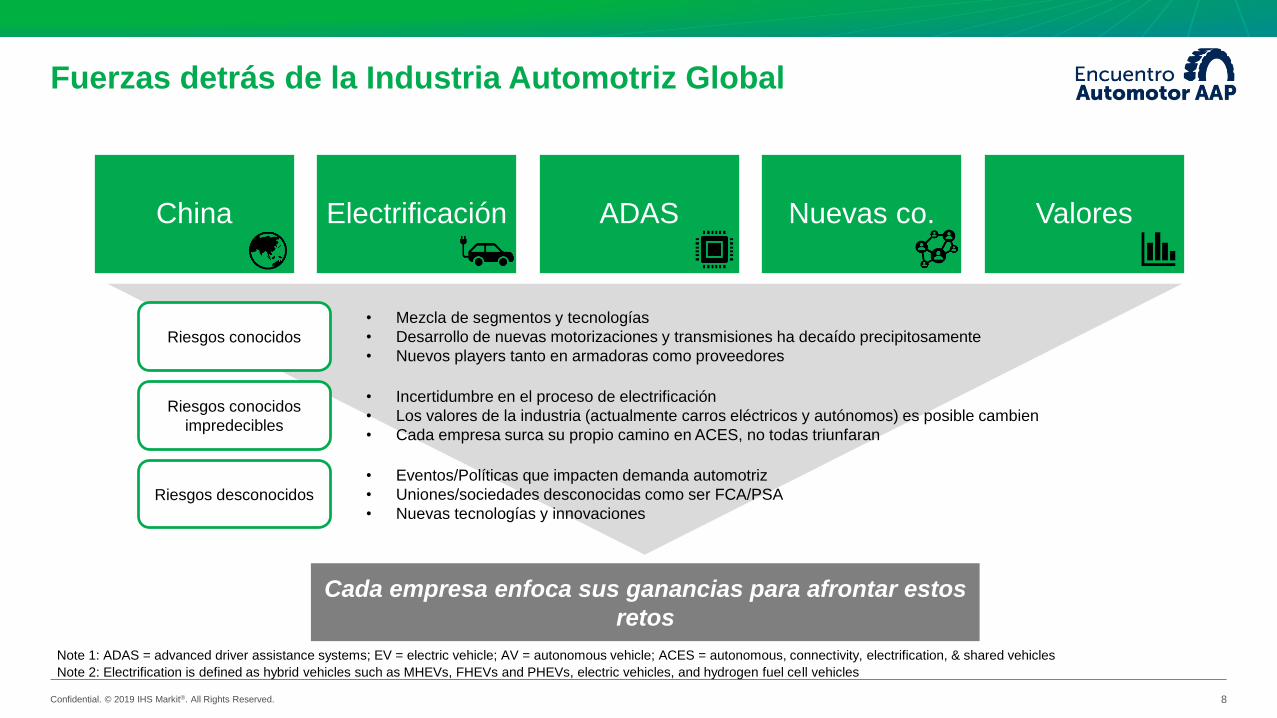

Fuerzas detrás de la Industria Automotriz Global

8

China Electrificación ADAS Nuevas co. Valores

• Mezcla de segmentos y tecnologías

• Desarrollo de nuevas motorizaciones y transmisiones ha decaído precipitosamente

• Nuevos players tanto en armadoras como proveedores

Note 1: ADAS = advanced driver assistance systems; EV = electric vehicle; AV = autonomous vehicle; ACES = autonomous, connectivity, electrification, & shared vehicles

• Incertidumbre en el proceso de electrificación

• Los valores de la industria (actualmente carros eléctricos y autónomos) es posible cambien

• Cada empresa surca su propio camino en ACES, no todas triunfaran

• Eventos/Políticas que impacten demanda automotriz

• Uniones/sociedades desconocidas como ser FCA/PSA

• Nuevas tecnologías y innovaciones

Riesgos desconocidos

Riesgos conocidos

impredecibles

Riesgos conocidos

Cada empresa enfoca sus ganancias para afrontar estos

retos

Note 2: Electrification is defined as hybrid vehicles such as MHEVs, FHEVs and PHEVs, electric vehicles, and hydrogen fuel cell vehicles

Confidential. © 2019 IHS Markit®. All Rights Reserved.

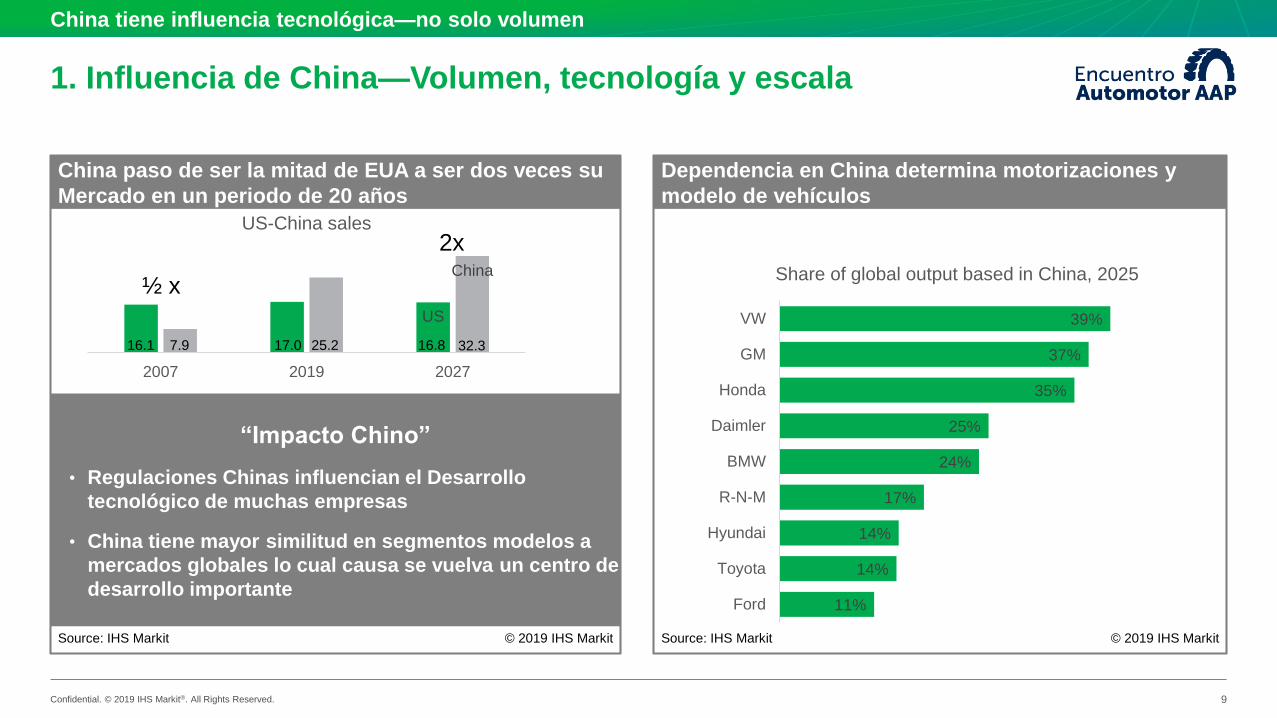

China paso de ser la mitad de EUA a ser dos veces su

Mercado en un periodo de 20 años

© 2019 IHS MarkitSource: IHS Markit

2x

US

China

2007 2019 2027

US-China sales

Dependencia en China determina motorizaciones y

modelo de vehículos

© 2019 IHS MarkitSource: IHS Markit

1. Influencia de China—Volumen, tecnología y escala

China tiene influencia tecnológica—no solo volumen

9

Dependency on China volume also dictates global propulsion and platform strategies

½ x

“Impacto Chino”

• Regulaciones Chinas influencian el Desarrollo

tecnológico de muchas empresas

• China tiene mayor similitud en segmentos modelos a

mercados globales lo cual causa se vuelva un centro de

desarrollo importante

Dependency on China volume also dictates global propulsion and platform strategies

11%

14%

14%

17%

24%

25%

35%

37%

39%

Ford

Toyota

Hyundai

R-N-M

BMW

Daimler

Honda

GM

VW

Share of global output based in China, 2025

16.1 7.9 16.817.0 25.2 32.3

Confidential. © 2019 IHS Markit®. All Rights Reserved.

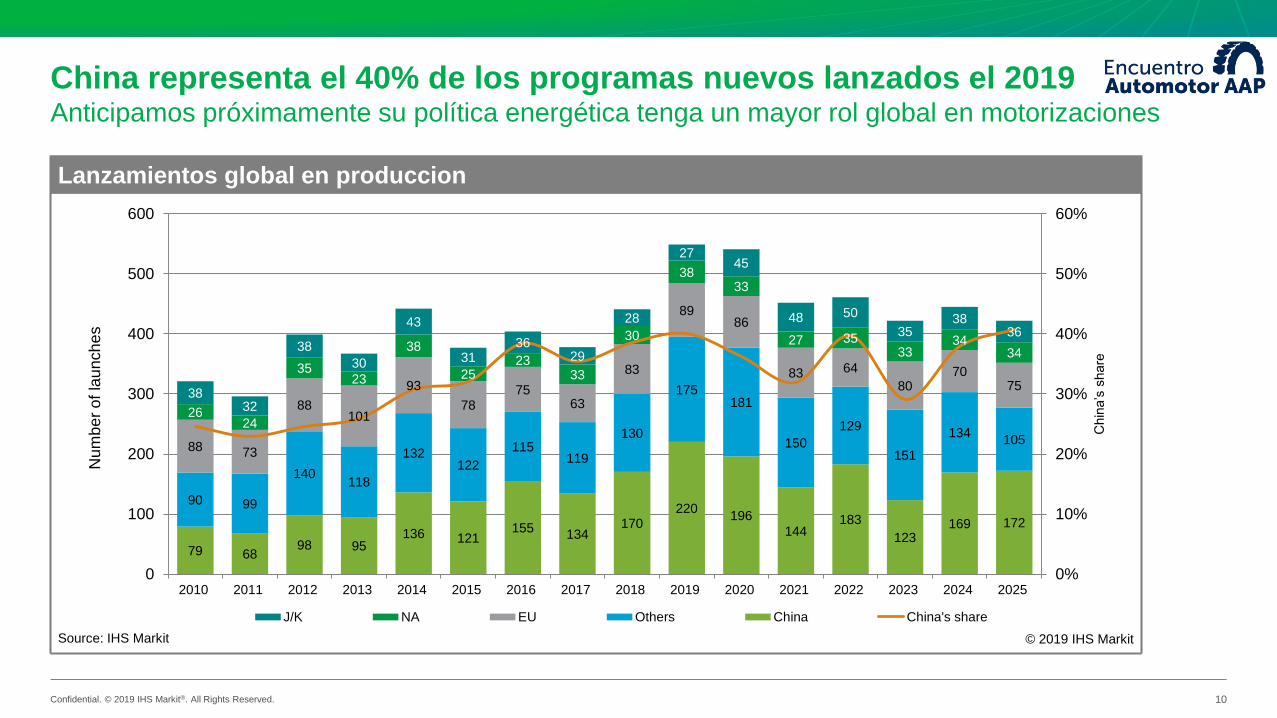

China representa el 40% de los programas nuevos lanzados el 2019Anticipamos próximamente su política energética tenga un mayor rol global en motorizaciones

10

79 6898 95

136 121155

134170

220196

144183

123169 172

90 99

140118

132122

115119

130

175181

150

129

151

134105

88 73

88101

93

7875

63

83

8986

83 64

8070

75

2624

3523

38

2523

33

30

3833

27 3533

3434

3832

38

30

43

3136

29

28

2745

48 50

3538

36

0%

10%

20%

30%

40%

50%

60%

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Chin

a’s

share

Num

be

r o

f la

un

ch

es

J/K NA EU Others China China's share

Lanzamientos global en produccion

Source: IHS Markit © 2019 IHS Markit

Confidential. © 2019 IHS Markit®. All Rights Reserved.

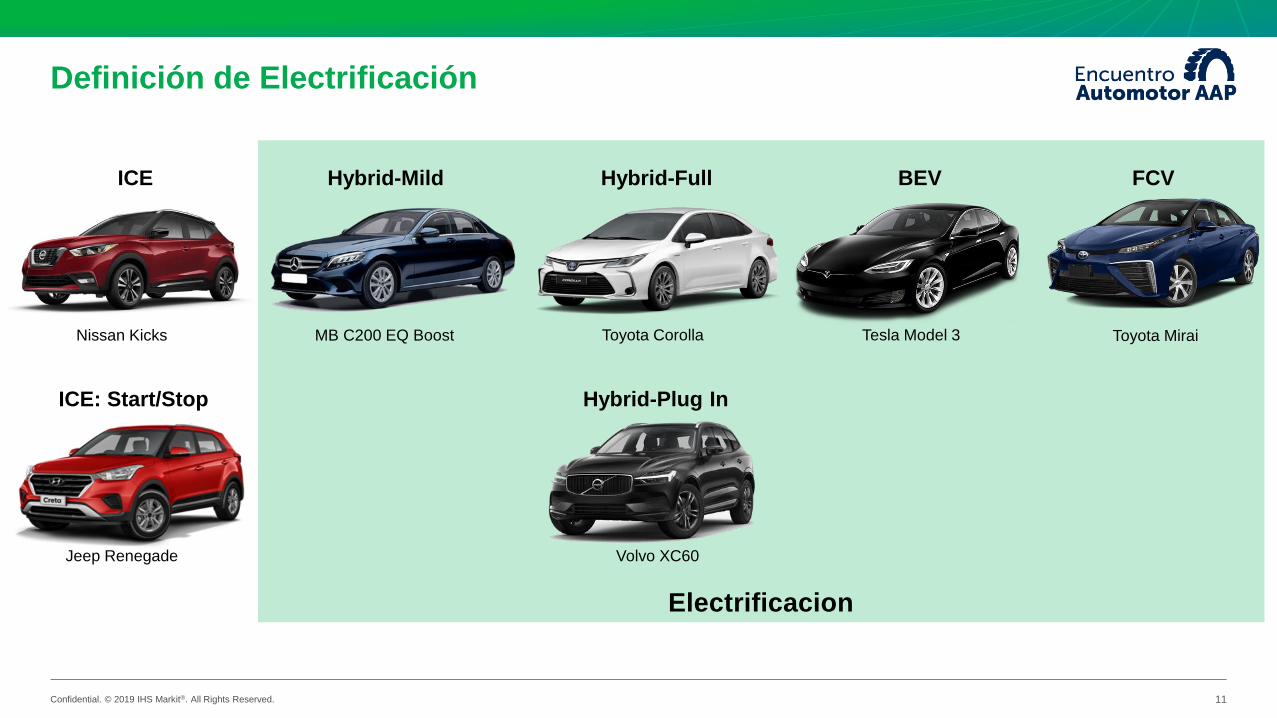

Electrificacion

Definición de Electrificación

11

ICE

Nissan Kicks

Hybrid-Full

Toyota Corolla

ICE: Start/Stop

Jeep Renegade

Hybrid-Plug In

Volvo XC60

BEV

Tesla Model 3

FCV

Toyota Mirai

Hybrid-Mild

MB C200 EQ Boost

Confidential. © 2019 IHS Markit®. All Rights Reserved.

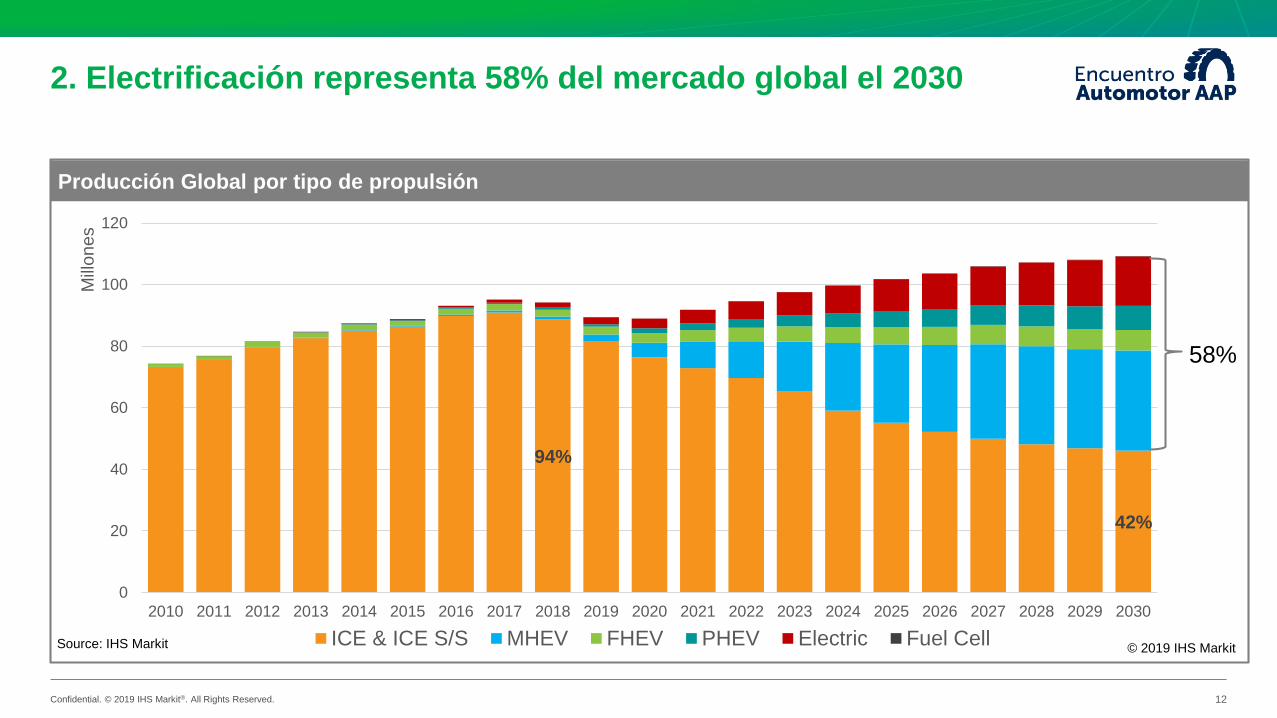

2. Electrificación representa 58% del mercado global el 2030

12

94%

42%

0

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Mill

on

es

ICE & ICE S/S MHEV FHEV PHEV Electric Fuel Cell

Producción Global por tipo de propulsión

58%

Source: IHS Markit © 2019 IHS Markit

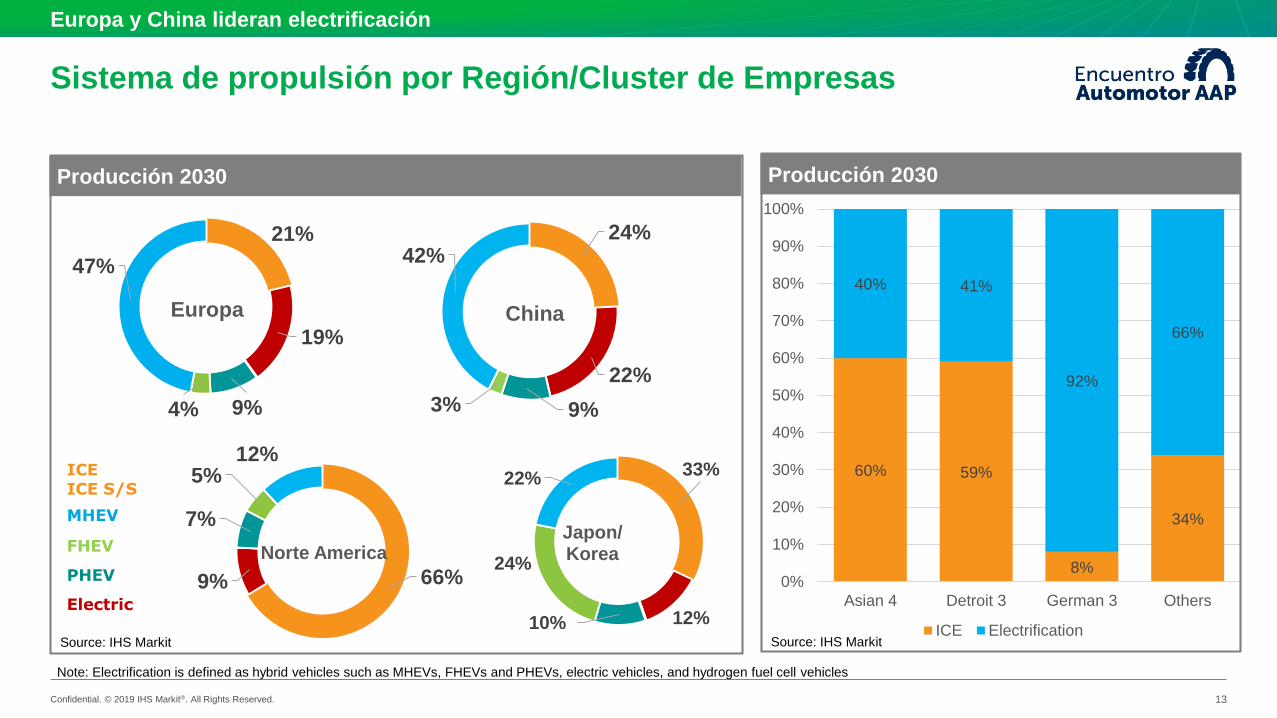

Confidential. © 2019 IHS Markit®. All Rights Reserved.

Sistema de propulsión por Región/Cluster de Empresas

13

Europa y China lideran electrificación

Producción 2030

Electric

MHEV

FHEV

ICEICE S/S

PHEV

24%

22%

9%3%

42%

China

21%

19%

9%4%

47%

Europa

33%

12%10%

24%

22%

Japon/Korea

66%9%

7%

5%12%

Norte America

Source: IHS Markit

60% 59%

8%

34%

40% 41%

92%

66%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Asian 4 Detroit 3 German 3 Others

ICE Electrification

Producción 2030

Note: Electrification is defined as hybrid vehicles such as MHEVs, FHEVs and PHEVs, electric vehicles, and hydrogen fuel cell vehicles

Source: IHS Markit

Confidential. © 2019 IHS Markit®. All Rights Reserved.

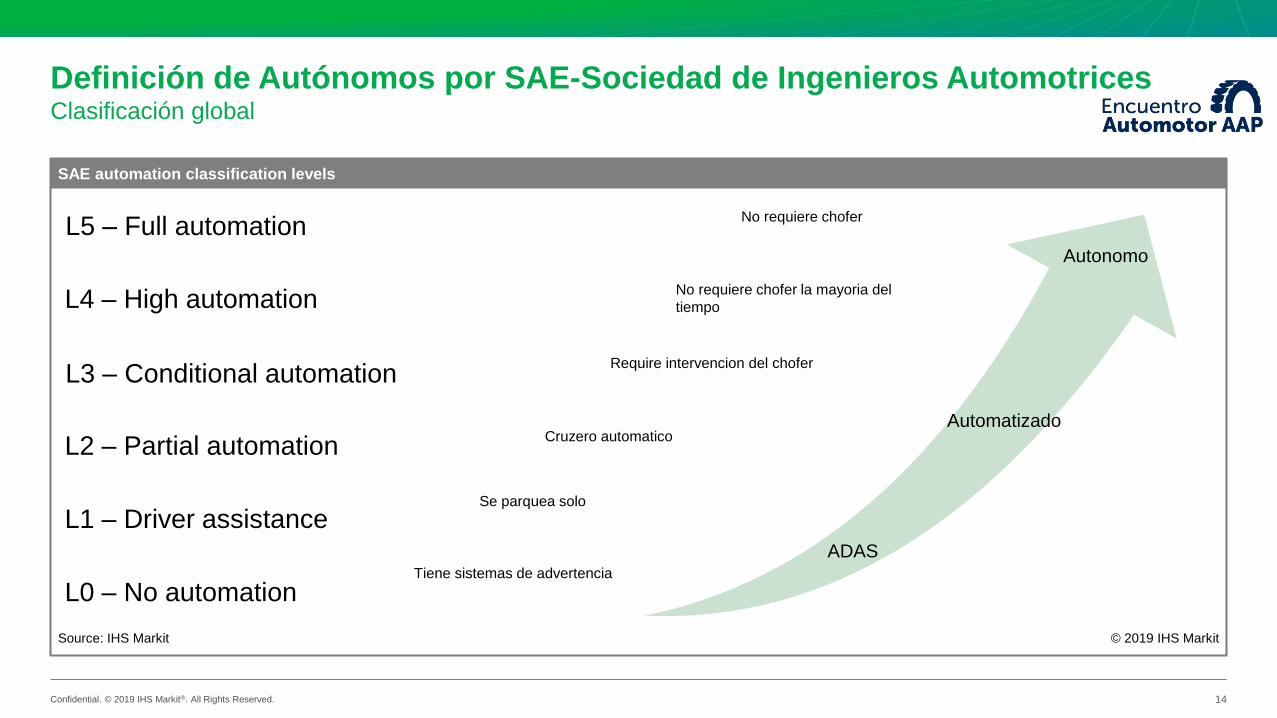

Definición de Autónomos por SAE-Sociedad de Ingenieros AutomotricesClasificación global

14

L5 – Full automation

L0 – No automation

L1 – Driver assistance

L2 – Partial automation

L3 – Conditional automation

L4 – High automation

Tiene sistemas de advertencia

Se parquea solo

Cruzero automatico

Require intervencion del chofer

No requiere chofer la mayoria del

tiempo

No requiere chofer

ADAS

Autonomo

Automatizado

SAE automation classification levels

© 2019 IHS MarkitSource: IHS Markit

Confidential. © 2019 IHS Markit®. All Rights Reserved.

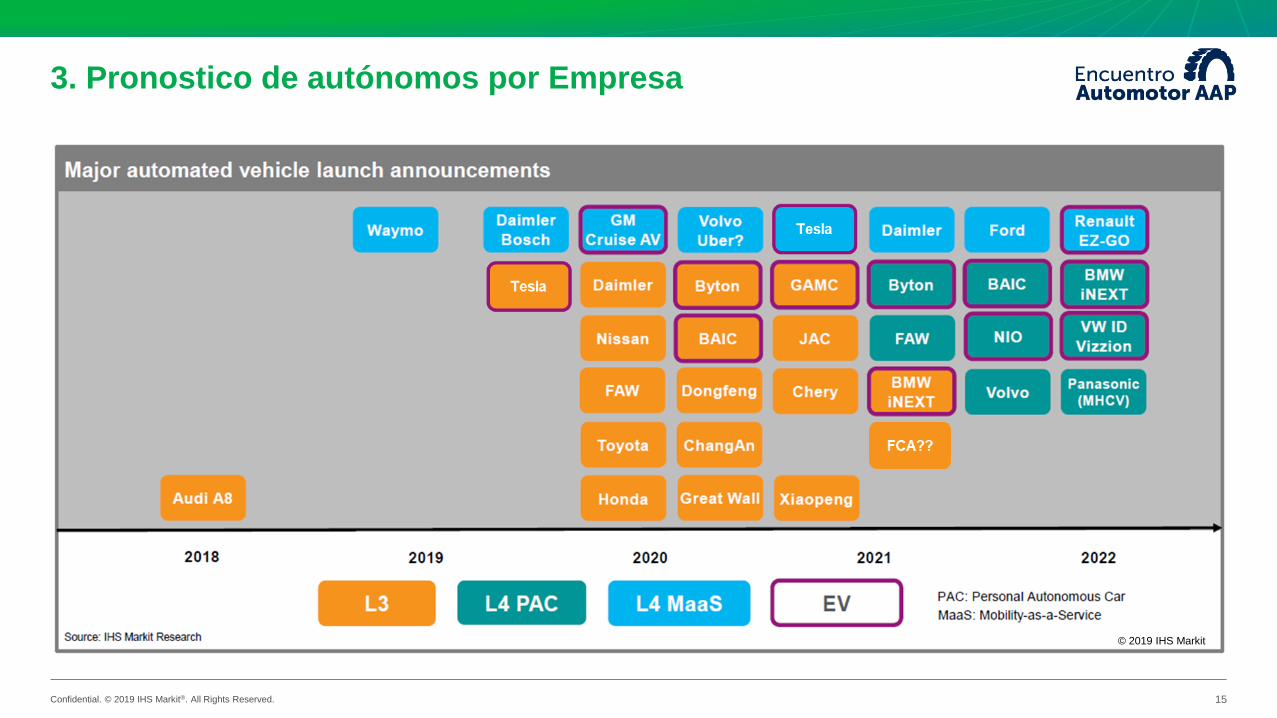

© 2019 IHS Markit

3. Pronostico de autónomos por Empresa

15

Confidential. © 2019 IHS Markit®. All Rights Reserved.

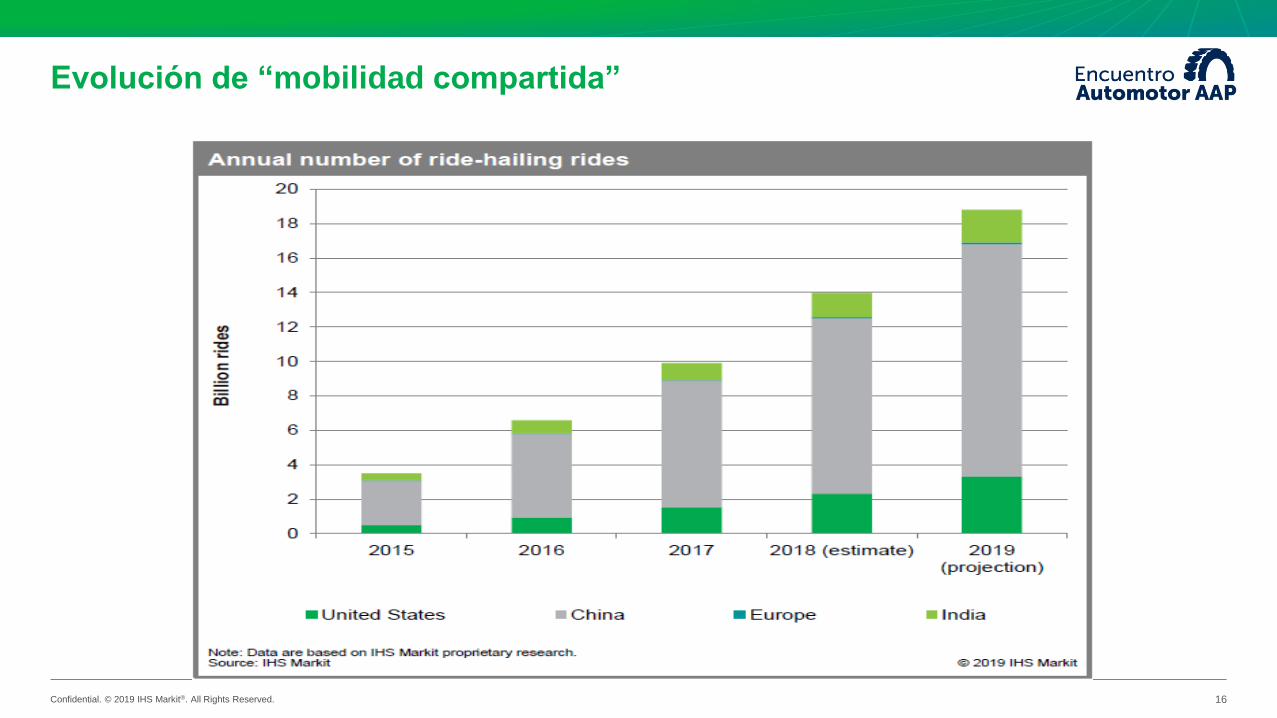

Evolución de “mobilidad compartida”

16

Confidential. © 2019 IHS Markit®. All Rights Reserved.

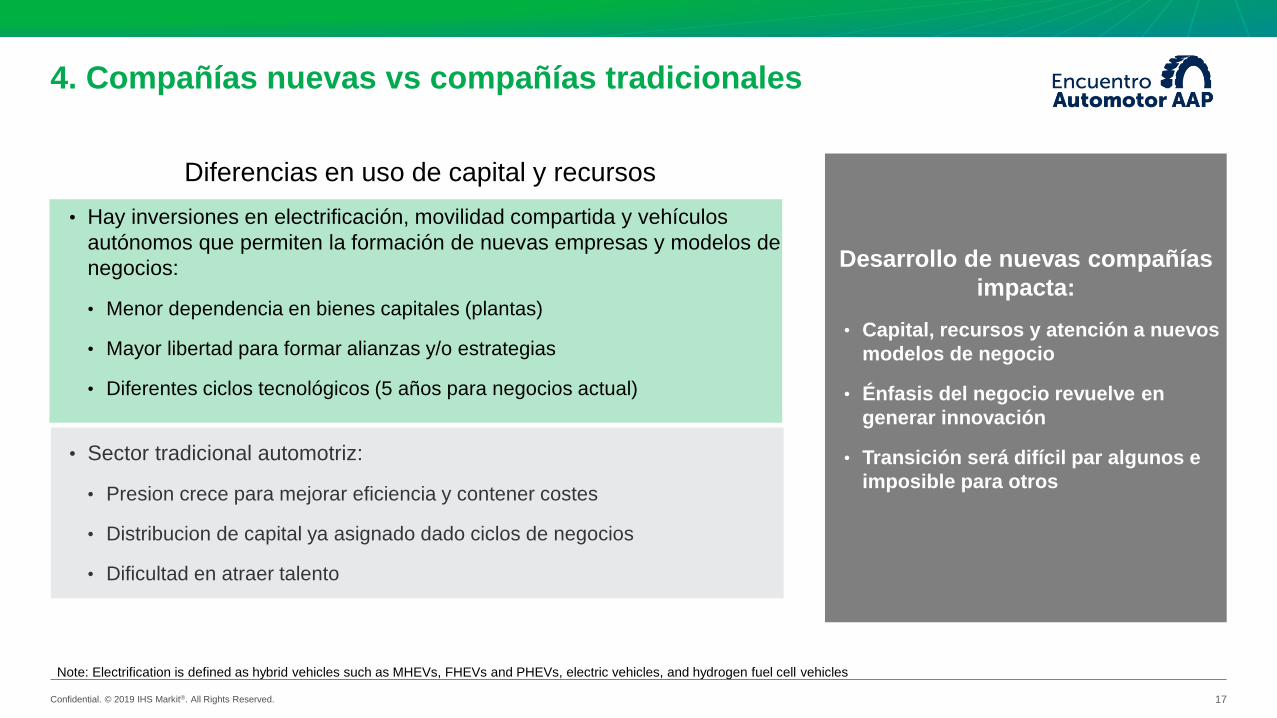

Diferencias en uso de capital y recursos

• Hay inversiones en electrificación, movilidad compartida y vehículos

autónomos que permiten la formación de nuevas empresas y modelos de

negocios:

• Menor dependencia en bienes capitales (plantas)

• Mayor libertad para formar alianzas y/o estrategias

• Diferentes ciclos tecnológicos (5 años para negocios actual)

• Sector tradicional automotriz:

• Presion crece para mejorar eficiencia y contener costes

• Distribucion de capital ya asignado dado ciclos de negocios

• Dificultad en atraer talento

4. Compañías nuevas vs compañías tradicionales

17

Desarrollo de nuevas compañías

impacta:

• Capital, recursos y atención a nuevos

modelos de negocio

• Énfasis del negocio revuelve en

generar innovación

• Transición será difícil par algunos e

imposible para otros

Note: Electrification is defined as hybrid vehicles such as MHEVs, FHEVs and PHEVs, electric vehicles, and hydrogen fuel cell vehicles

Confidential. © 2019 IHS Markit®. All Rights Reserved.

ICE

Fullhybrid

BEV

Chassis/wheels & tires

Climate

Interior/seating/safety

BIW/glass

Powertrain/driveline

Electrical/electronics

Battery/E-Motor/charge

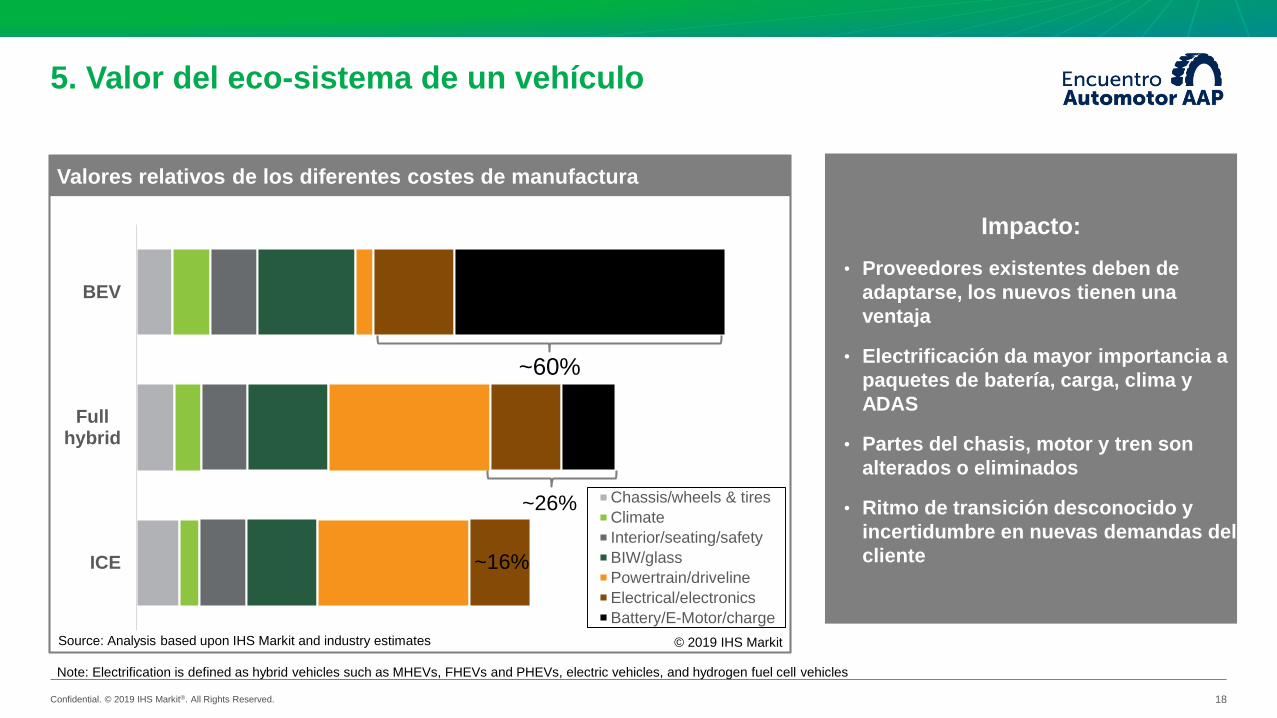

5. Valor del eco-sistema de un vehículo

18

Valores relativos de los diferentes costes de manufactura

Impacto:

• Proveedores existentes deben de

adaptarse, los nuevos tienen una

ventaja

• Electrificación da mayor importancia a

paquetes de batería, carga, clima y

ADAS

• Partes del chasis, motor y tren son

alterados o eliminados

• Ritmo de transición desconocido y

incertidumbre en nuevas demandas del

cliente

~60%

Source: Analysis based upon IHS Markit and industry estimates

Note: Electrification is defined as hybrid vehicles such as MHEVs, FHEVs and PHEVs, electric vehicles, and hydrogen fuel cell vehicles

© 2019 IHS Markit

~26%

~16%

Confidential. © 2019 IHS Markit®. All Rights Reserved.

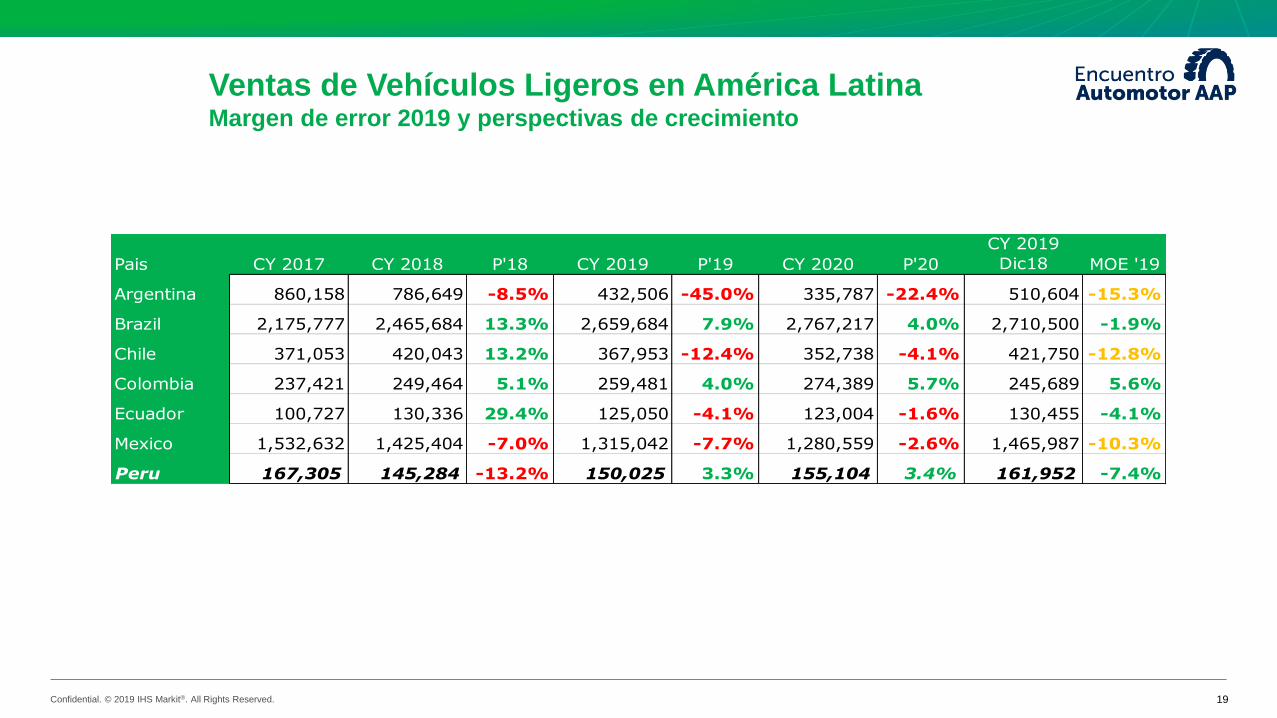

Ventas de Vehículos Ligeros en América LatinaMargen de error 2019 y perspectivas de crecimiento

Pais CY 2017 CY 2018 P'18 CY 2019 P'19 CY 2020 P'20

CY 2019

Dic18 MOE '19

Argentina 860,158 786,649 -8.5% 432,506 -45.0% 335,787 -22.4% 510,604 -15.3%

Brazil 2,175,777 2,465,684 13.3% 2,659,684 7.9% 2,767,217 4.0% 2,710,500 -1.9%

Chile 371,053 420,043 13.2% 367,953 -12.4% 352,738 -4.1% 421,750 -12.8%

Colombia 237,421 249,464 5.1% 259,481 4.0% 274,389 5.7% 245,689 5.6%

Ecuador 100,727 130,336 29.4% 125,050 -4.1% 123,004 -1.6% 130,455 -4.1%

Mexico 1,532,632 1,425,404 -7.0% 1,315,042 -7.7% 1,280,559 -2.6% 1,465,987 -10.3%

Peru 167,305 145,284 -13.2% 150,025 3.3% 155,104 3.4% 161,952 -7.4%

19

Confidential. © 2019 IHS Markit®. All Rights Reserved.

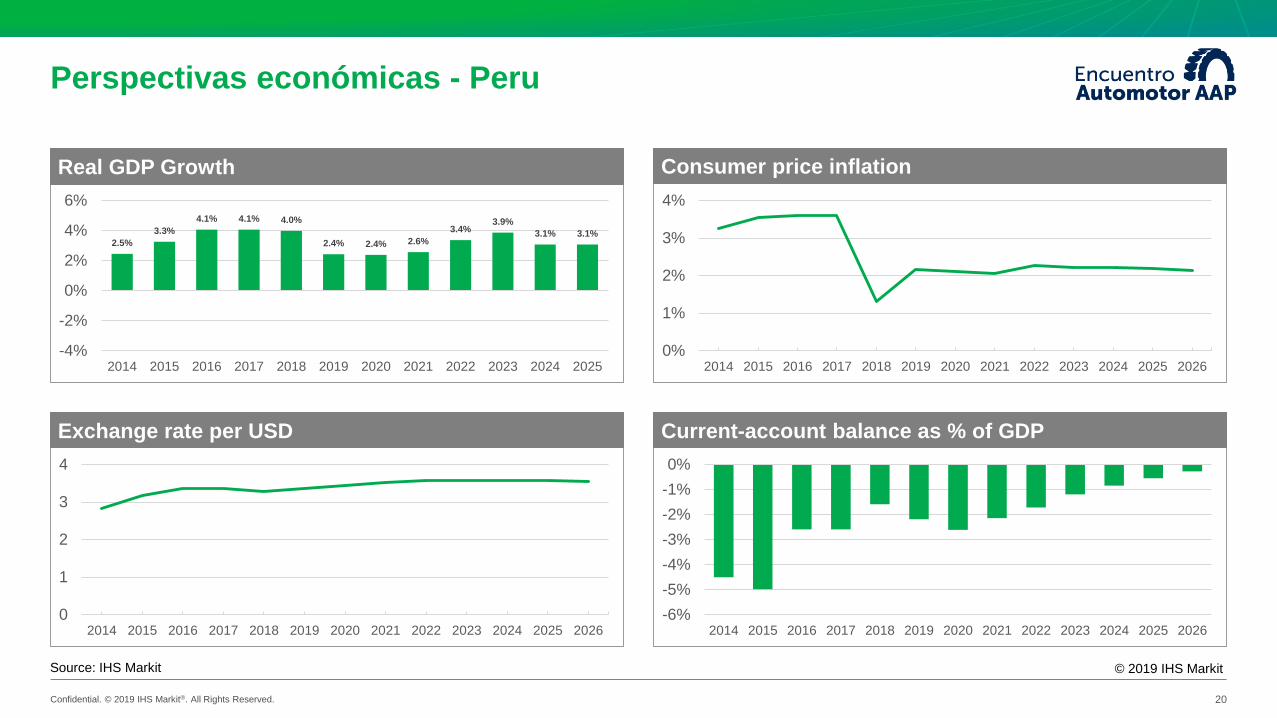

Perspectivas económicas - Peru

20

Source: IHS Markit © 2019 IHS Markit

2.5%

3.3%

4.1% 4.1% 4.0%

2.4% 2.4% 2.6%

3.4%3.9%

3.1% 3.1%

-4%

-2%

0%

2%

4%

6%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Real GDP growth

0%

1%

2%

3%

4%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Consumer price inflation

0

1

2

3

4

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Exchange rate per USD

-6%

-5%

-4%

-3%

-2%

-1%

0%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Current Account Balance as a % of GDP

Real GDP Growth Consumer price inflation

Exchange rate per USD Current-account balance as % of GDP

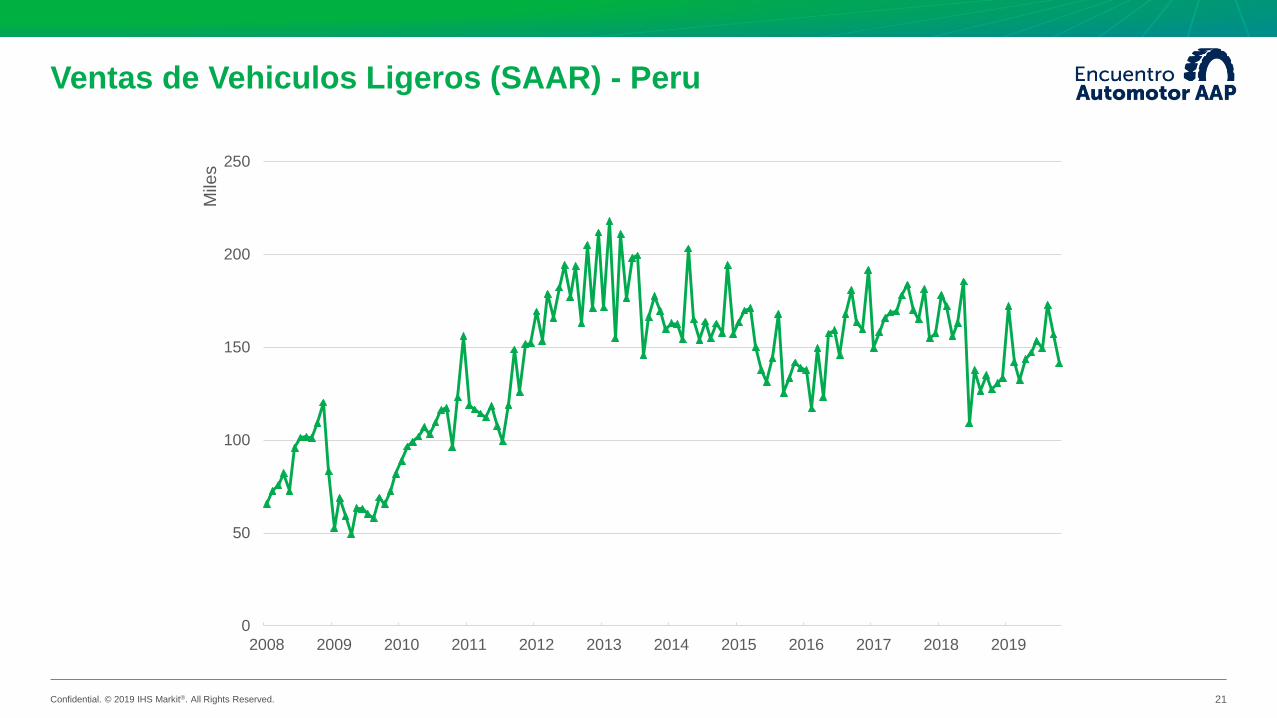

Confidential. © 2019 IHS Markit®. All Rights Reserved. 21

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Mile

s

Ventas de Vehiculos Ligeros (SAAR) - Peru

Confidential. © 2019 IHS Markit®. All Rights Reserved.

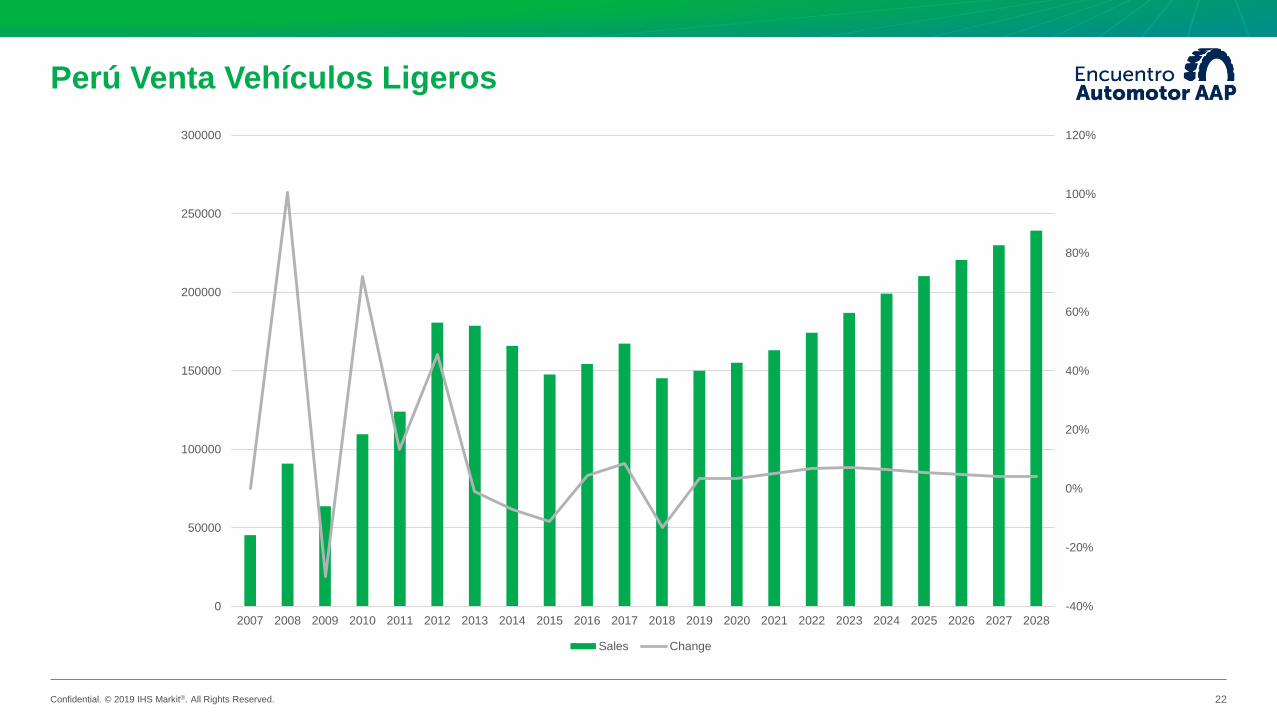

Perú Venta Vehículos Ligeros

22

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

0

50000

100000

150000

200000

250000

300000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Sales Change

Confidential. © 2019 IHS Markit®. All Rights Reserved.

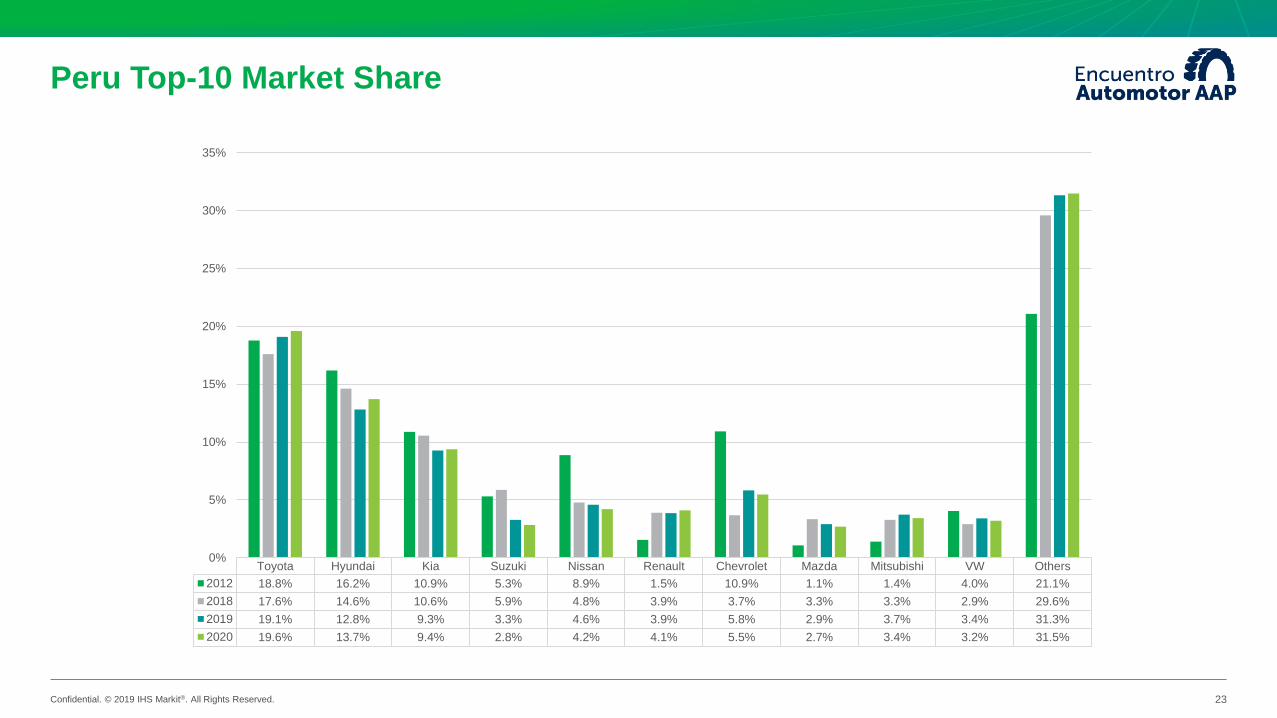

Peru Top-10 Market Share

23

Toyota Hyundai Kia Suzuki Nissan Renault Chevrolet Mazda Mitsubishi VW Others

2012 18.8% 16.2% 10.9% 5.3% 8.9% 1.5% 10.9% 1.1% 1.4% 4.0% 21.1%

2018 17.6% 14.6% 10.6% 5.9% 4.8% 3.9% 3.7% 3.3% 3.3% 2.9% 29.6%

2019 19.1% 12.8% 9.3% 3.3% 4.6% 3.9% 5.8% 2.9% 3.7% 3.4% 31.3%

2020 19.6% 13.7% 9.4% 2.8% 4.2% 4.1% 5.5% 2.7% 3.4% 3.2% 31.5%

0%

5%

10%

15%

20%

25%

30%

35%

Confidential. © 2019 IHS Markit®. All Rights Reserved.

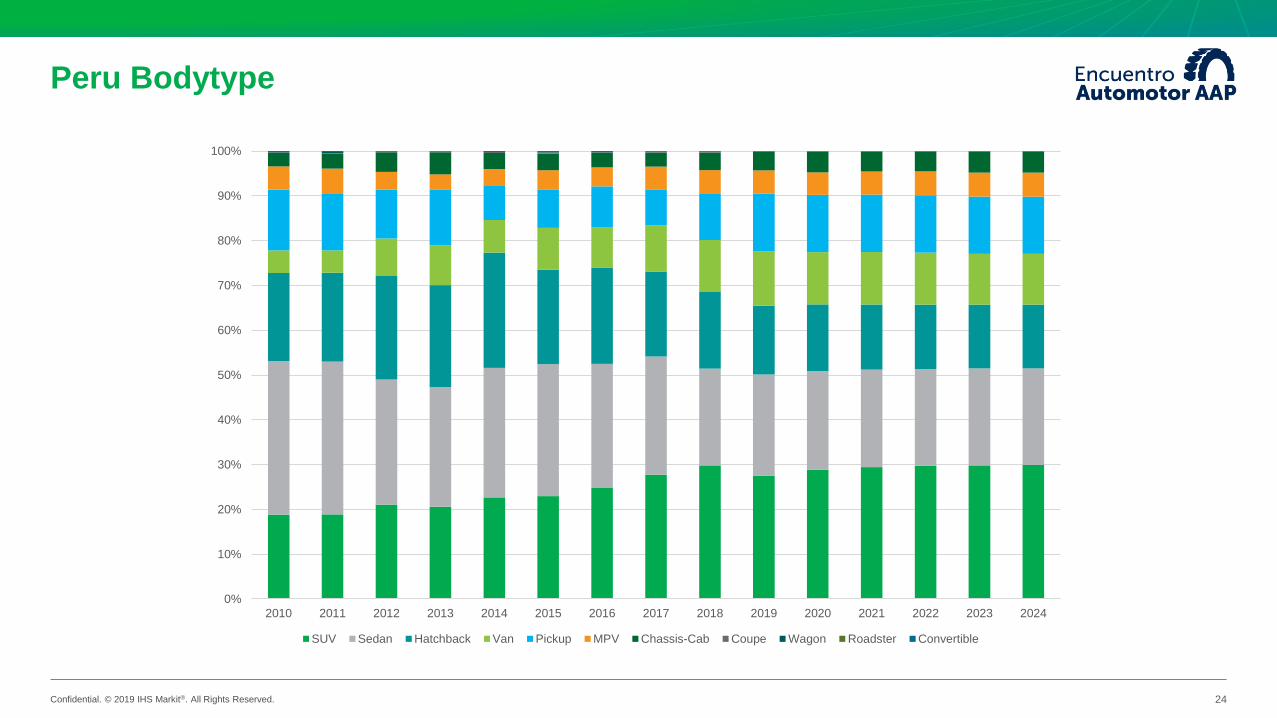

Peru Bodytype

24

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

SUV Sedan Hatchback Van Pickup MPV Chassis-Cab Coupe Wagon Roadster Convertible

Confidential. © 2019 IHS Markit®. All Rights Reserved. 25Source: IHS Automotive

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Toyota 2017

Toyota 2025

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Portfolio Age

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Toyota Brand YOY Industry YOY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hilux Yaris Etios RAV4 Avanza Others

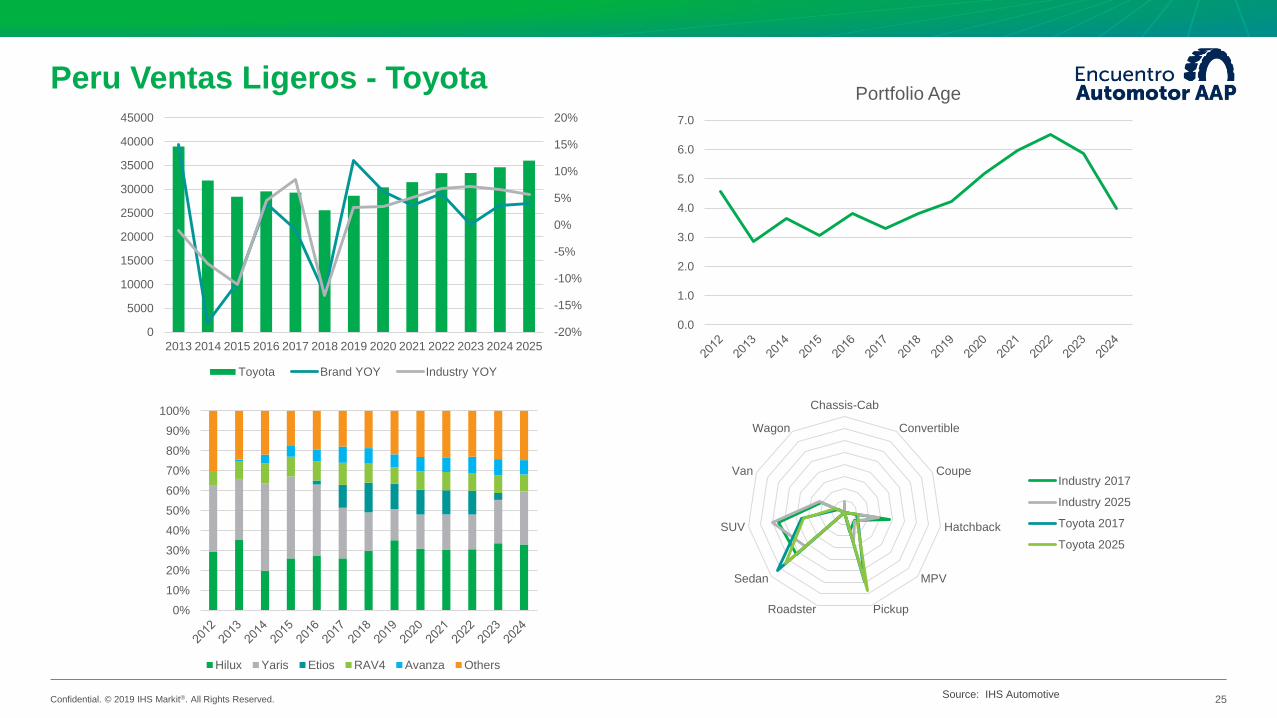

Peru Ventas Ligeros - Toyota

Confidential. © 2019 IHS Markit®. All Rights Reserved. 26Source: IHS Automotive

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Hyundai 2017

Hyundai 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Accent Grand i10 Tucson i20 Elantra Others

-30%

-20%

-10%

0%

10%

20%

30%

0

5000

10000

15000

20000

25000

30000

35000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Hyundai Brand YOY Industry YOY

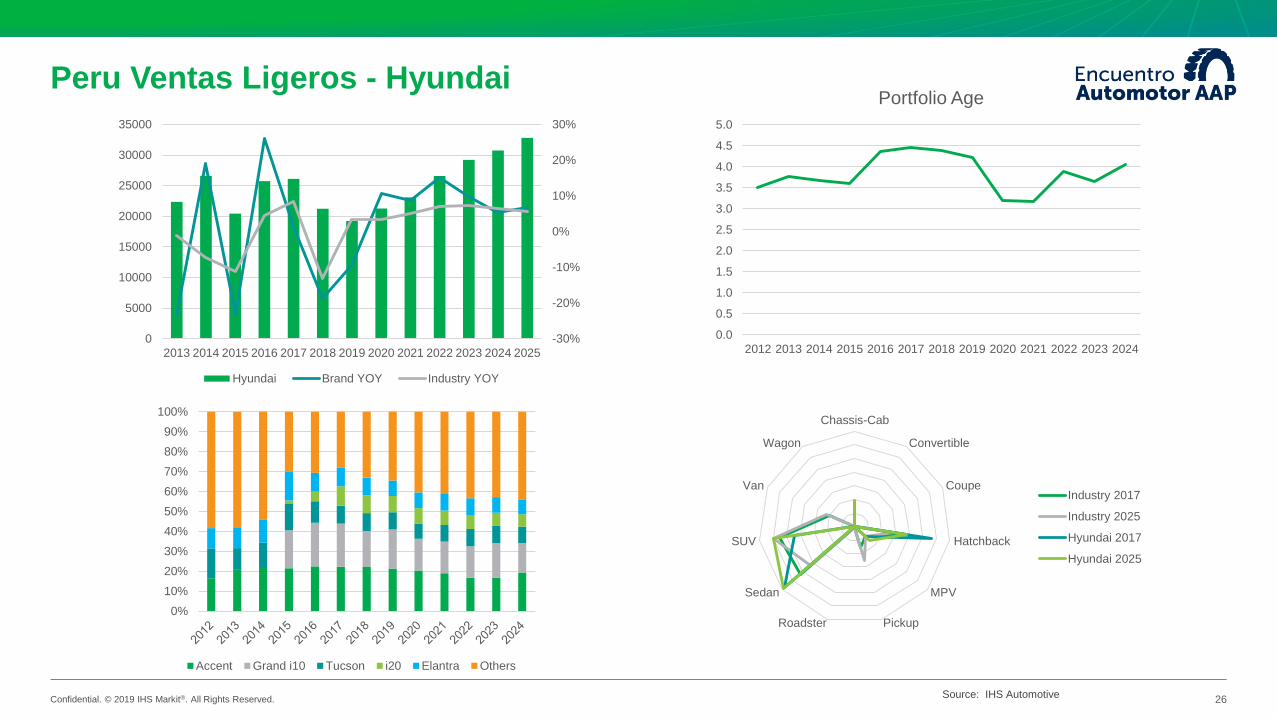

Peru Ventas Ligeros - Hyundai

Confidential. © 2019 IHS Markit®. All Rights Reserved. 27Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Kia 2017

Kia 2025

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

5000

10000

15000

20000

25000

30000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Kia Brand YOY Industry YOY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rio Picanto Cerato Sportage Bongo Others

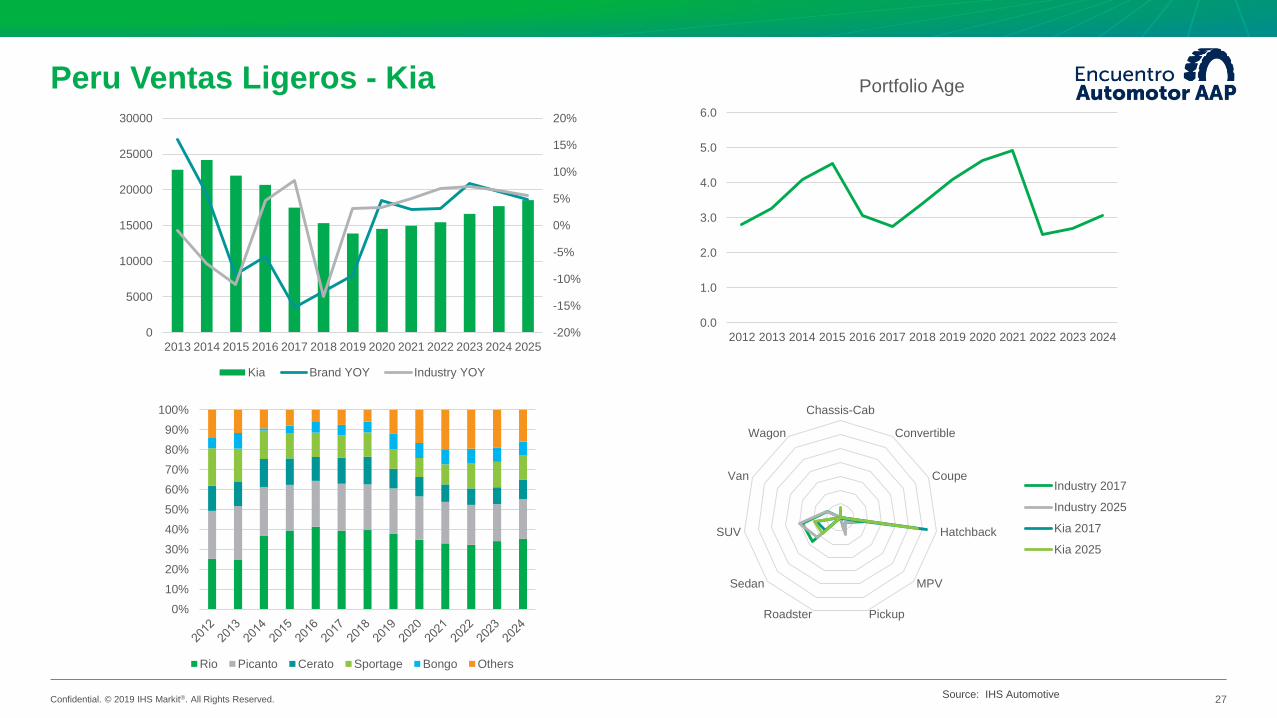

Peru Ventas Ligeros - Kia

Confidential. © 2019 IHS Markit®. All Rights Reserved. 28Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

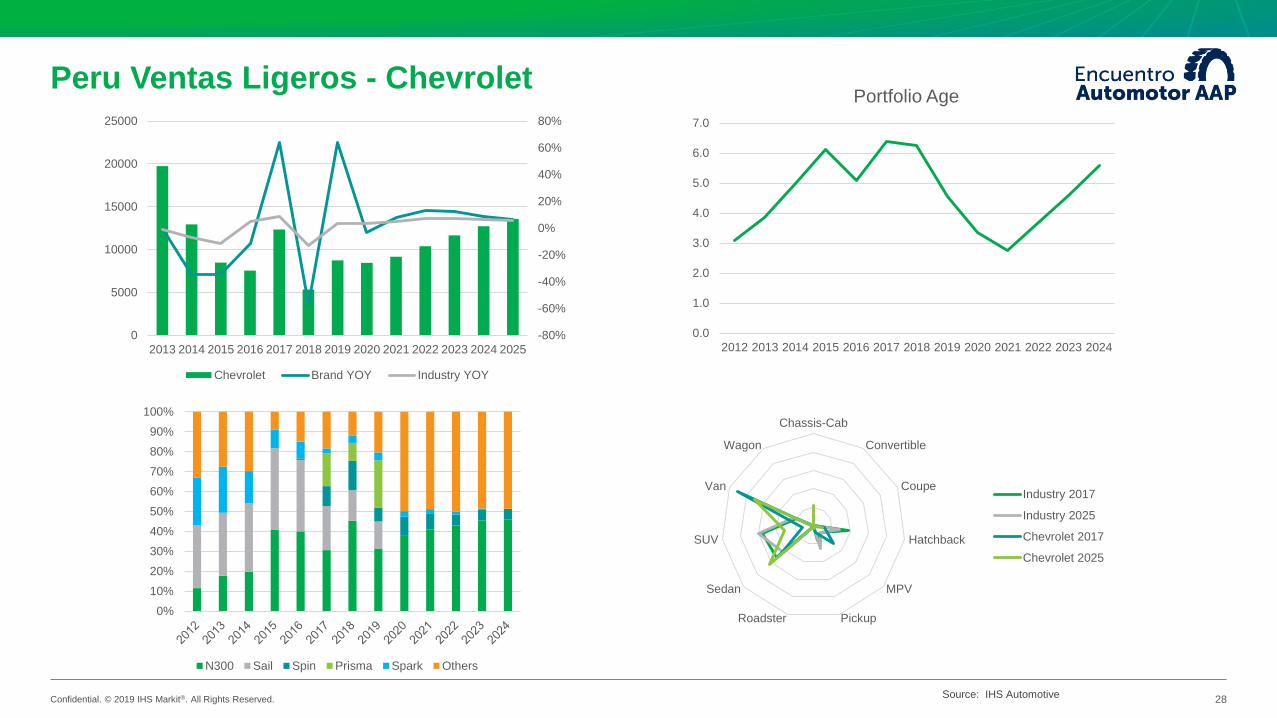

Chevrolet 2017

Chevrolet 2025

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

0

5000

10000

15000

20000

25000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Chevrolet Brand YOY Industry YOY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

N300 Sail Spin Prisma Spark Others

Peru Ventas Ligeros - Chevrolet

Confidential. © 2019 IHS Markit®. All Rights Reserved. 29Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

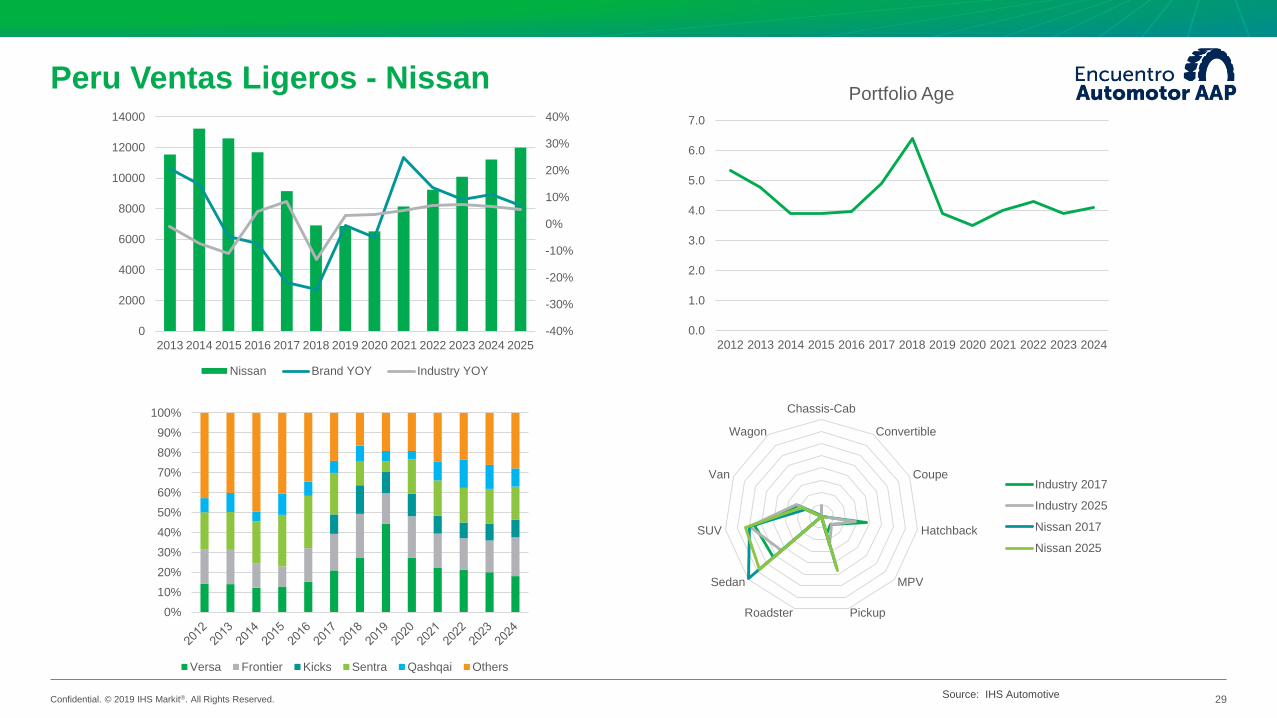

Nissan 2017

Nissan 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Versa Frontier Kicks Sentra Qashqai Others

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

2000

4000

6000

8000

10000

12000

14000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Nissan Brand YOY Industry YOY

Peru Ventas Ligeros - Nissan

Confidential. © 2019 IHS Markit®. All Rights Reserved. 30Source: IHS Automotive

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

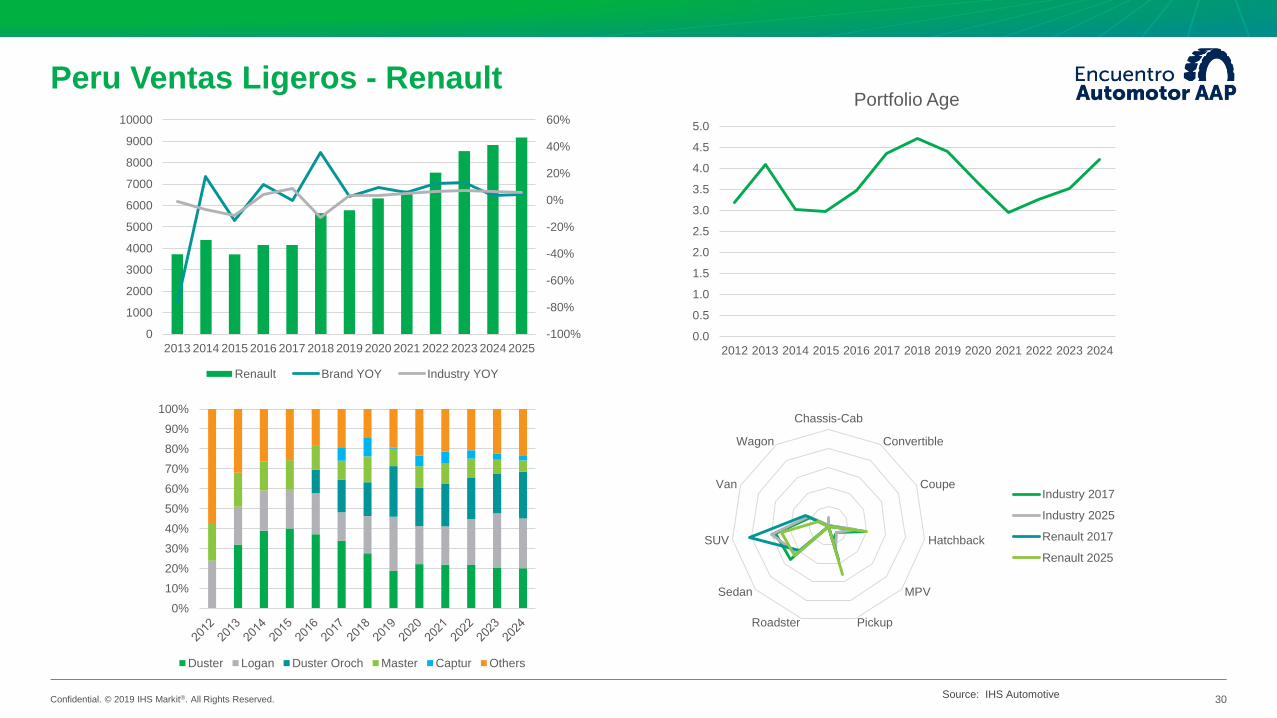

Renault 2017

Renault 2025

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Renault Brand YOY Industry YOY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Duster Logan Duster Oroch Master Captur Others

Peru Ventas Ligeros - Renault

Confidential. © 2019 IHS Markit®. All Rights Reserved. 31Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

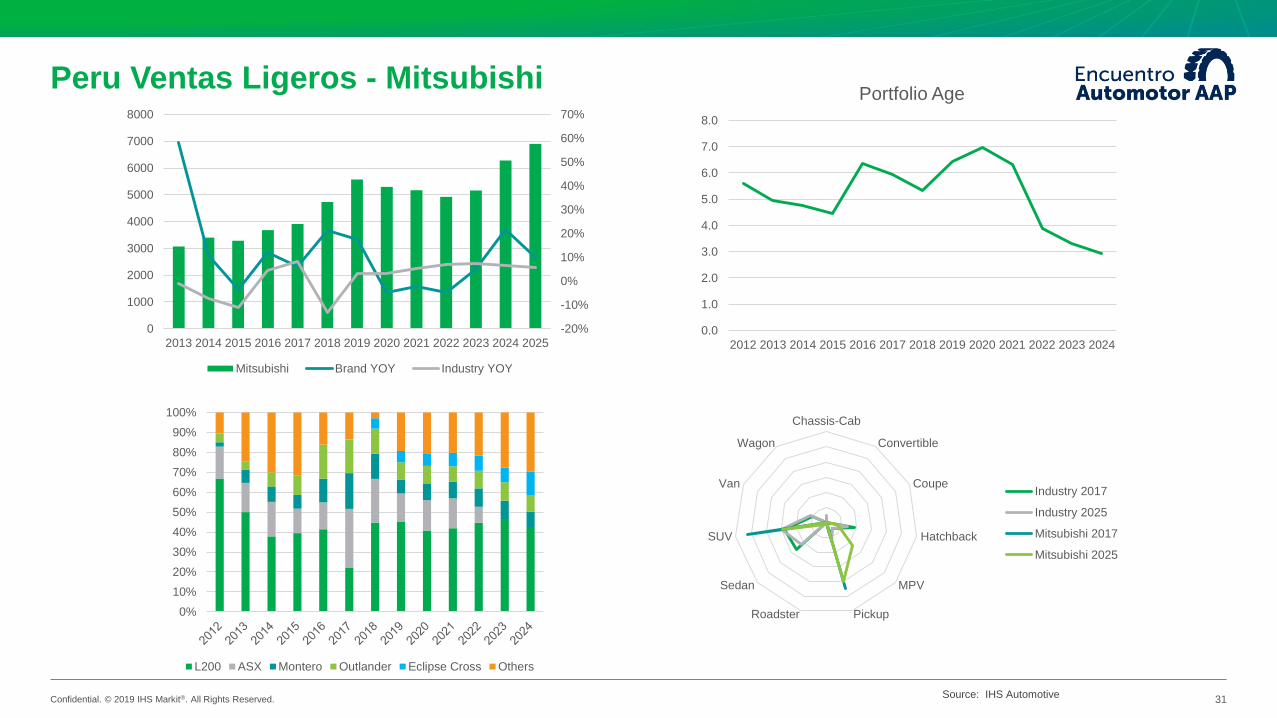

Mitsubishi 2017

Mitsubishi 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

L200 ASX Montero Outlander Eclipse Cross Others

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

0

1000

2000

3000

4000

5000

6000

7000

8000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Mitsubishi Brand YOY Industry YOY

Peru Ventas Ligeros - Mitsubishi

Confidential. © 2019 IHS Markit®. All Rights Reserved. 32Source: IHS Automotive

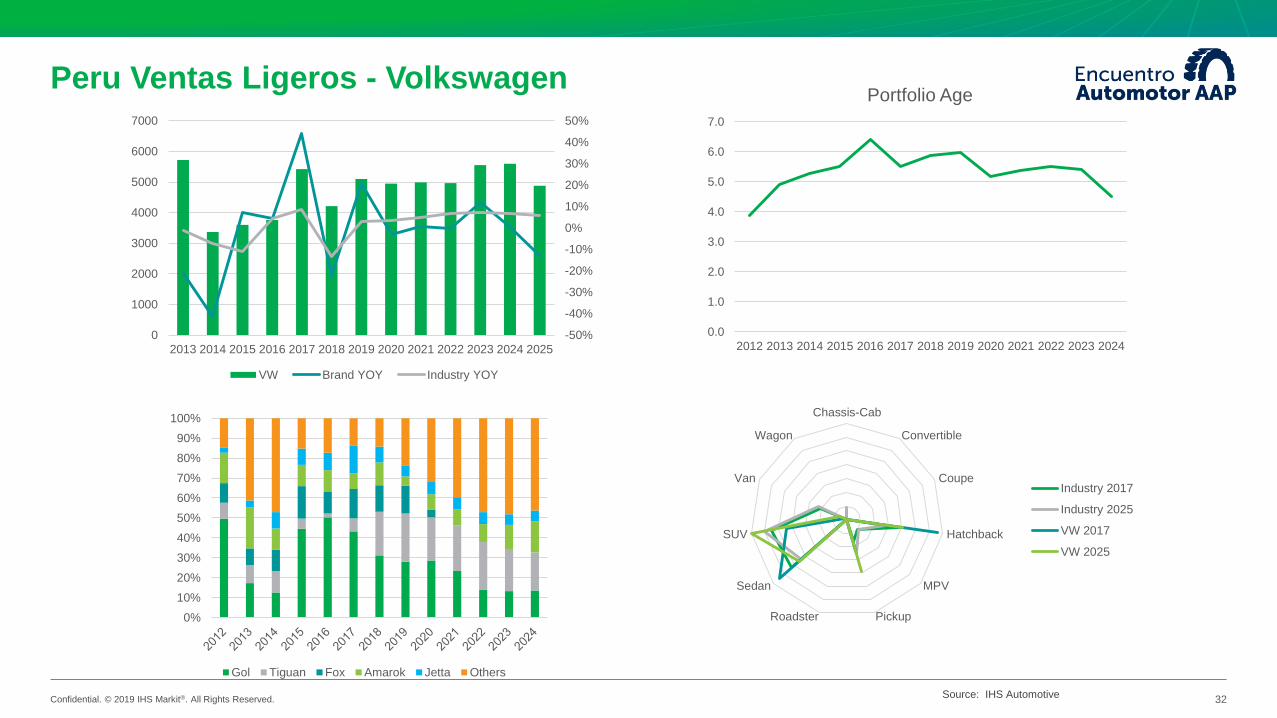

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

VW 2017

VW 2025

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

1000

2000

3000

4000

5000

6000

7000

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

VW Brand YOY Industry YOY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gol Tiguan Fox Amarok Jetta Others

Peru Ventas Ligeros - Volkswagen

IHS Markit Customer Care

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600

Disclaimer

The information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission of IHS Markit Ltd. or any of its affiliates ("IHS Markit") is

strictly prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the

time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or

subsequently becomes inaccurate. IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without

limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with

any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's

owners (or their products/services). IHS Markit is not responsible for either the content or output of external websites. Copyright © 2019, IHS Markit®. All rights reserved and all intellectual property rights are retained by IHS Markit.

2018 Spring Automotive Client Briefing - CITY

Guido Vildozo, Senior Manager

+1 781 301 9037

Christopher Hopson, Manager

+1 781 301 9107

Roberto Barros, Senior Analyst

+55 19 3578 1221

João Rebouças, Market Analyst

+55 19 3578 1219

Nicholas Hess, Market Analyst

+1 248 728 6985

Thank you, Muchas Gracias

Muito Obrigado!

Top Related