RETOS Y OPORTUNIDADES DE LA INDUSTRIA EN … · Contribución al crecimiento NPC NRI Var% 2015 vs....

41

RETOS Y OPORTUNIDADES DE LA INDUSTRIA EN MÉXICO Héctor Granados Octubre, 2016

-

Upload

dangnguyet -

Category

Documents

-

view

216 -

download

0

Transcript of RETOS Y OPORTUNIDADES DE LA INDUSTRIA EN … · Contribución al crecimiento NPC NRI Var% 2015 vs....

RETOS Y OPORTUNIDADESDE LA INDUSTRIA EN MÉXICO

Héctor GranadosOctubre, 2016

OUTLOOK ECONOMÍA LATAM 2015 Y PERSPECTIVAS 2016

CONSUMO DESACELERADOCrecimiento promedio en últimos 10 años de 4.2%, en 2015 se ubicó en -0.1%

MENOR INVERSIÓNCrecimiento promedio en últimos 10 años de 5.3%, en 2015 se ubicó en -4.3%

DISMINUYE EXPORTACIONESCrecimiento promedio en últimos 10 años de 7.5%, en 2015 se ubicó en -13.1%

+30%

DEVALUACIÓN

17.0%

INFLACIÓN

Fuente: Latin Focus Agosto ‘16

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3Fuente: Latin Focus Agosto ‘16

LA REDUCCIÓN DEL PIB ES INFLUENCIADA POR LAS ECONOMÍAS IMPORTANTES DE LA REGIÓNLa expectativa regional continúa por debajo de las cifras globales.

7.0

3.3

0.0

3.12.5 2.1

0.32.4

-0.6

-3.8

-5.7

5.63.7 3.0

2.3 2.3 1.8

-3.2-1.2

-1.3-3.3

-9.2R. DOM PE CAM +

CARIBCO MX CHI ECU ARG P.RICO BRA

VZLA

2015

2016 P

RANKING ECONOMÍAS LATAM(% GDP 2015)

BRASIL 34%

MÉXICO 22%

VENEZUELA 4%

ARGENTINA 12%

CHILE 5%

PERÚ 4%

REP. DOMINICANA 1%

PUERTO RICO 1%

ECUADOR 2%

CAM Y CARIBE 8%

VARIACIÓN % ANUAL DEL PIB

2.6 3.0 2.6 3,0 2.8

1,0

2,8

-0,1

3,1

-0,3

GLOBAL LATAM

2012 2013 2014 2015 2016 P

COLOMBIA 6%

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

FACTORES QUE AFECTAN LA ECONOMÍA MEXICANA

Fuente: Petróleo - Banco de México | Dólar – Banamex (Histórico dólar americano) Agosto, 2016 | Corrupción - * Transparencia Internacional (FMI)

Precio promedio en dólarespor Barril:2014: 96.3 2015: 49.5

PRECIO DEL PETRÓLEO

Depreciación del Peso Mexicano 25%

Campeche; Tabasco; Tamaulipas; Chiapas;

Veracruz; San Luis Potosí; Puebla;

Nuevo León y Coahuila

ESTADOS MÁS AFECTADOS POR EL PETROLEO

13.2

18.8Ju

l'14

Sep

t'1

4

No

v'1

4

Ene'

15

Mar

'15

May

'15

Jul'1

5

Sep

t'1

5

No

v'1

5

Ene'

16

Mar

'16

May

'16

Jul'1

6

Tipo de CambioPeso Mexicano vs. USD

DEPRECIACIÓN DEL PESO

PIB sería 2% mayorsi baja la Corrupción*

CORRUPCIÓNPOLÍTICA

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

QUE FAVORECEN EL CONSUMO INTERNO5 FACTORESMotor de la Economía Mexicana

INFLACIÓN CONTROLADA2.5% Q2 ‘16 (A la baja)

1365

ELECCIONESGENERANDERRAMA ECONÓMICA

REMESAS2.38% PIB en

2015

Fuente: Banco de México | INEGI | Latin Focus Agosto ‘16

INVERSIÓNEXTRANJERA

RÉCORD EN 17 AÑOS14 mil 385 MDD Acumulado 2º Trim. 2016

En 2015 se crearon 733,499

Nuevos Empleos4.3% vs. 2014

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

EL 90% DE LAS REMESAS SE DESTINAN AL CONSUMOLas remesas superaron el ingreso por petróleo y turismo

Fuente: Banxico

% Var Remesas

-0.1%vs. Jul’15

1.3 millones de hogares reciben

remesas

2233.7

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Remesas – Millones de USD – Julio Año 2000 a 2016

24,77123,432

17,186

Remesas Petróleo Turismo

Millones de dólaresAño 2015

JULIO

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

EL TIPO DE CAMBIO HIZO QUE LAS REMESAS FUERAN AÚN MÁS BENEFICIOSAS

Hogares que reciben remesas: 1.3MM

Source: Banxico - INEGI

Remesas por Hogar (MMUSD)

Julio 2016Julio 2015Julio 2014

Var% remesas USD(Base=Jul14)

Tipo de cambio

Remesas por Hogar (MM MXN)

Var% remesas MXN(Base=Jul14)

Var% Salario Mínimo (Base=Jun14)

Var% Inflación (Base=Jul14)

1,998 2,235 2,234

+11.8% -0.1%

13.2 16.1 18.8

20,322 27,617 32,220

+35.9% +16.7%

+4.2% +8.5%

-32.7% +16.8%

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

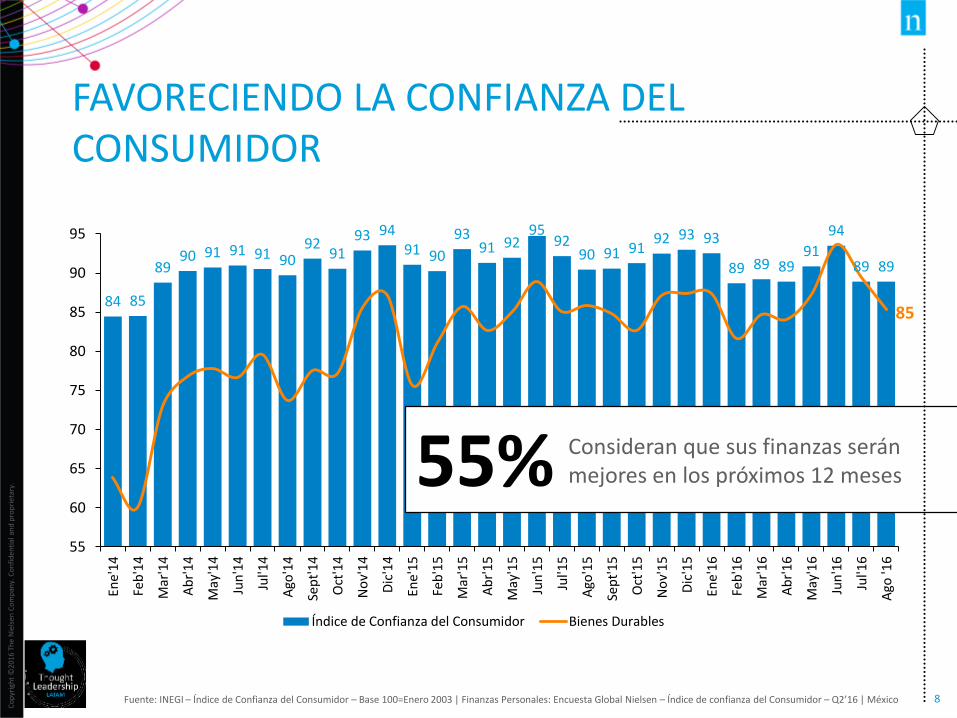

FAVORECIENDO LA CONFIANZA DEL CONSUMIDOR

Fuente: INEGI – Índice de Confianza del Consumidor – Base 100=Enero 2003 | Finanzas Personales: Encuesta Global Nielsen – Índice de confianza del Consumidor – Q2’16 | México

84 85

8990 91 91 91 90

9291

93 9491 90

9391 92

9592

90 91 9192 93 93

89 89 8991

94

89 89

55

60

65

70

75

80

85

90

95

Ene'

14

Feb

'14

Mar

'14

Ab

r'1

4

May

'14

Jun

'14

Jul'1

4

Ago

'14

Sep

t'14

Oct

'14

No

v'1

4

Dic

'14

Ene'

15

Feb

'15

Mar

'15

Ab

r'1

5

May

'15

Jun

'15

Jul'1

5

Ago

'15

Sep

t'15

Oct

'15

No

v'1

5

Dic

'15

Ene'

16

Feb

'16

Mar

'16

Ab

r'1

6

May

'16

Jun

'16

Jul'1

6

Ago

'16

Índice de Confianza del Consumidor Bienes Durables

85

55% Consideran que sus finanzas serán mejores en los próximos 12 meses

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

3.5

6.9

3.6

-1.0

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

-1.0

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2009 2010 2011 2012 2013 2014 2015

TOTAL CANASTOS NIELSEN MÉXICOPORCENTAJE DE VARIACIÓN ANUAL (AÑOS MÓVILES)

REFORMA HACENDARIA

Ventas Volumen Ventas Valor Precio Ponderado

TT: +11.5%TI: +7.8%Agosto 2016

2016

LO CUAL SE VE REFLEJADO EN EL CANASTO NIELSEN

Fuente: Nielsen Retail Index | Canastos Nielsen | Total México | Variación porcentual Año Móvil vs. Año Móvil previo | Periodos hasta AMJ ‘16

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

+8.4%

+10.8%

+5.1%

+3.1%

-28.0%

+6.9%

EL ÁREA 3 NIELSEN FUE LA QUE MAYOR CONTRIBUCIÓN TUVO AL CRECIMIENTO DEL CANASTO NIELSEN, AL IGUAL QUE DE LAS REMESAS

• Fuente: Banco de México | Var % 2015 vs. 2014, último período disponible en la fuente

13.7%

30.6%

18.1%

8.2%

4.4%

24.9%

Contribución al crecimiento NPC NRIVar% 2015 vs. 2014

+5.7%

REMESAS 24,771mdd+8.4%

+28.1%

+8.5%+10.7%

+18.8%

+25.6%

Contribución a remesas

Variación vs. 2014

2015 CANASTO NIELSEN + 5.5%

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

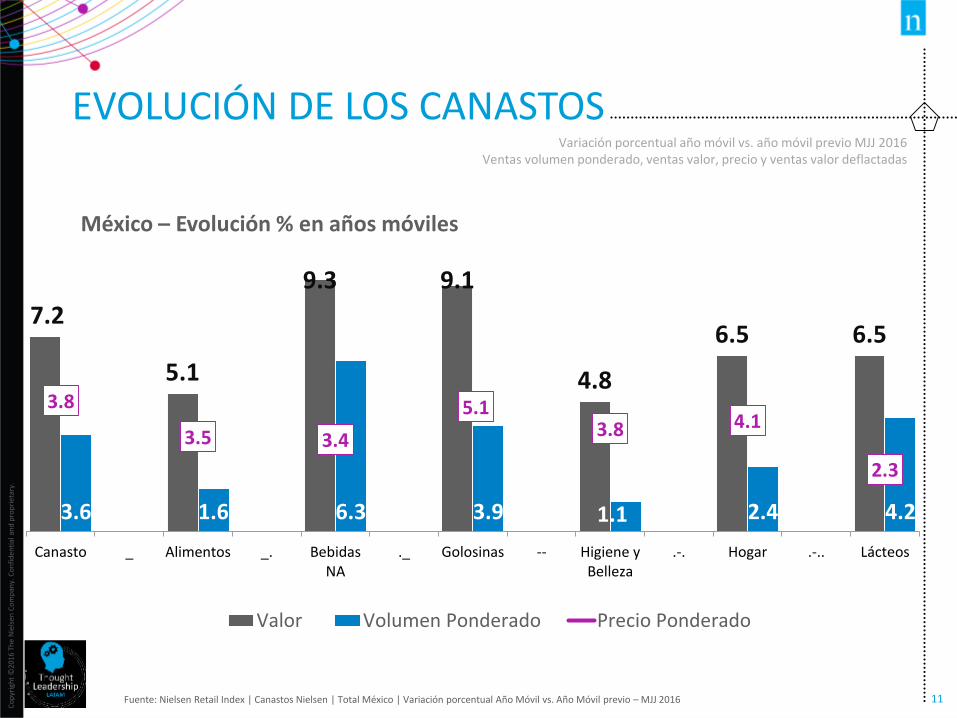

EVOLUCIÓN DE LOS CANASTOSVariación porcentual año móvil vs. año móvil previo MJJ 2016

Ventas volumen ponderado, ventas valor, precio y ventas valor deflactadas

Fuente: Nielsen Retail Index | Canastos Nielsen | Total México | Variación porcentual Año Móvil vs. Año Móvil previo – MJJ 2016

México – Evolución % en años móviles

7.2

5.1

9.3 9.1

4.8

6.5 6.5

3.6 1.6 6.3 3.9 1.1 2.4 4.2

3.8

3.5 3.4

5.13.8 4.1

2.3

Canasto _ Alimentos _. BebidasNA

._ Golosinas -- Higiene yBelleza

.-. Hogar .-.. Lácteos

Valor Volumen Ponderado Precio Ponderado

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

EL CANASTO DE ALIMENTOS…

Fuente: Nielsen Retail Index| Fabricantes exitosos | Canasto de Alimentos| Año Móvil Enero ‘16

21%% Ventas Valor proviene de las Marcas Exitosas

55%Contribución al Crecimiento delCanasto de Alimentos

+9%vs. el 4.2% del canasto

Las Marcas exitosas de alimentos, crecen

De las 2,419 Marcas de alimentos solo 35 logran crecer en ventas volumen y en ventas valor por arriba de la inflación

¿QUÉ HACEN LAS MARCAS EXITOSAS PARA CRECER?

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

7%

9%

11%

18%

19%Affordability

% Variación de Ventas Valor por tipo de estrategia

Affordability + Innovación

Innovación

Valor por su Dinero

Puntos de Precio

23%14%

6%

8%

20%

14%

14%

11%

37%

52%

% Marcas % Contribución al crecimiento

Fuente: Nielsen Retail Index | Canasto de Alimentos | Affordability: Impulsan las presentaciones más pequeñas de su portafolio | Valor por su Dinero: Impulsa presentaciones grandes dentro de su portafolio | Price Points: Utiliza estrategias diferenciadas de precio y tamaño

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

LA ESPECIALIZACIÓN Y SEGMENTO SALUDABLE, JUEGAN UN PAPEL CLAVE EN LA INNOVACIÓN

Fuente: Nielsen Índice de Confianza del Consumidor (Q1 2016)2

23% INTOLERANTES A LA LACTOSA

19% VEGETARIANOS

9% VEGANOS

51% CONSUMEN

SÚPER ALIMENTOS

42% GUSTAN DE

ENDULZANTES NATURALES

DE LAS MARCAS EXITOSAS,JUEGAN EN UN SEGMENTO SALUDABLE

39%

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

DEBIDO A LOS NIVELES DE OBESIDAD QUE HEMOS ALCANZADO EN EL PAÍS

Fuente: Nielsen Índice de Confianza del Consumidor (Q1 2016) | México

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

450,000,000

500,000,000

Ch

ina

Ind

ia

U.S

.

Bra

zil

Ru

ssia

Mex

ico

Ind

on

esia

Nig

eria

Egyp

t

Turk

ey

Iran

Pak

ista

n

Ger

man

y

U.K

.

Fran

ce

Ital

y

Jap

an

Sou

th A

fric

a

Ban

glad

esh

Spai

n

Co

lom

bia

Arg

enti

na

TOP 22 PAÍSES EN SOBREPESO

34%% vs. Total Population

22% 67% 54% 59% 64% 24% 33% 62% 66% 62% 23% 55% 63% 61% 59% 24% 54% 18% 61% 57% 62%

47% Diagnosticados con Presión Arterial9.2% Diagnosticados con Diabetes

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

¿CÓMO REACCIONA EL CONSUMIDOR?

Fuente; Global Survey 2014 Health Wellness and Nutrition, Flexitariano: (comen principalmente plantas con inclusión ocasional de carne, pollo o mariscos), incluyendo pescetarian, pollotarian o pollo-pescetarian

79% Hacen ejercicio de manera regular

71% Llevan una dieta para prevenir enfermedades crónicas

69% Monitorean los ingredientes que consumen para controlar su dieta

59%

38%

35%

32%

24%

20%

19%

15%

9%

5%

Bajo en Grasa

Bajo en Azúcar

Bajo en Sodio

Bajo en Carb

Deslactosado

Libre de Gluten

Vegetariano

Flexitariana

Vegano

Kosher

Sacrifican el consumo

de algunos alimentos

73% Revisan cuidadosamente en las etiquetas el contenido nutricional

72% Prestan mucha atención a los ingredientes incluidos en su comida

77% Quieren saber todo de la

procedencia de sus alimentos

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

LA CARNE ROJA ES UNO DE LOS ALIMENTOS QUE EL CONSUMIDOR EVALUA AL CUIDAR SU SALUD

Fuente: Nielsen Global Survey Ingredientes de los A,limentos 2016

Preferencia por la Carne Roja% de Respondientes On-line

Trato de Incluirla

No importa si la incluyo o no

16%Condición Médica

que la Prohíbe

67%Eligieron no consumirlapor el bien de su salud

Trato de Evitarla

20%

53%

27%

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

19

RES 39.6%

POLLO 42.3%

CERDO 10.4%

TIPO DE CARNE PREFERIDO POR LOS

CONSUMIDORES

Fuente: Estudio de Consumo de Carne Berumen | Nielsen Global Survey Ingredientes de los A,limentos 2016

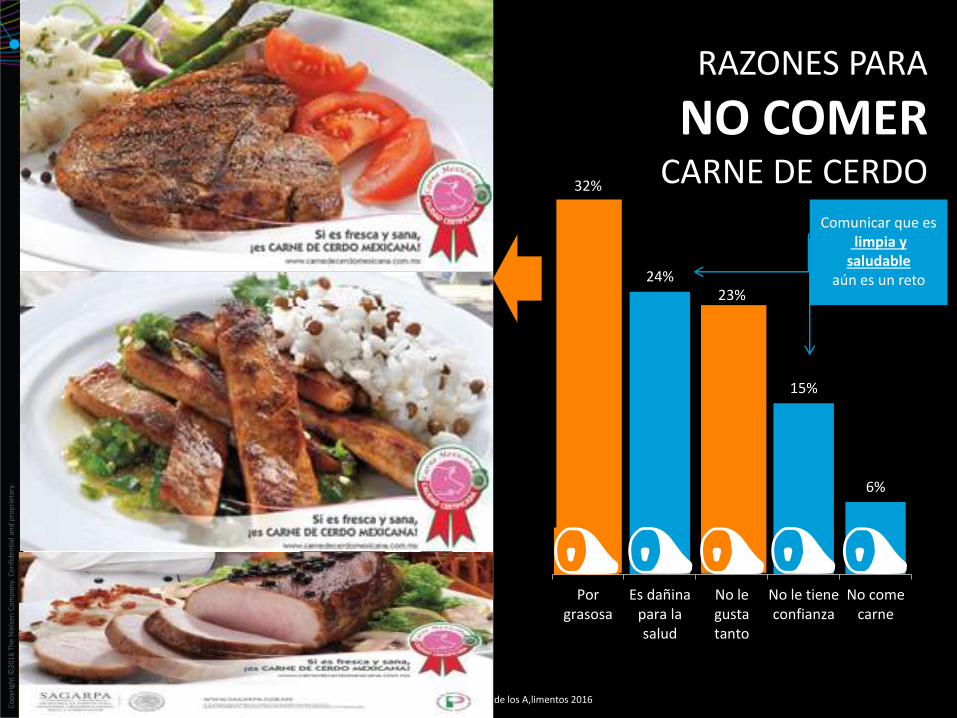

32%

24%23%

15%

6%

Porgrasosa

Es dañinapara lasalud

No legustatanto

No le tieneconfianza

No comecarne

RAZONES PARA

NO COMERCARNE DE CERDO

Comunicar que eslimpia y

saludable aún es un reto

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

75% de los encuestados prefieren marcas locales cuando compran cualquier tipo de carne

DETALLISTAS Y CONSUMIDORESDEBEN CONOCER LOS BENEFICIOS DE LA CARNE DE CERDO

52% de los encuestados consideran que tener un departamento de carne de alta calidad es muy influyente para seleccionar una tienda

38%35%

28% 27%

21% 20%18% 17%

15%13%

10%8%

Precio Sabor Surtido IngredientesNaturales

Fortificados Sustentable Promoción Tamaño Conveniencia Orgánico Bajo o sin… Marca

FUENTE: Global Survey Healthy lifestyle

Atributos más importantes al comprar carne de cualquier tipo

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

21

ES IMPORTANTE BUSCAR UN BALANCE EN COMO COMUNICAMOS

EQUITYVOLUMEN

MEDIATRADE

ROI – Vehículos de marketing

Fuente: Nielsen Marketing Mix | Ejemplo real

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

22

IDENTIFICANDO LOS MEDIOS CLAVE PARA UNA ESTRATEGIA DE MEDIANO Y LARGO PLAZO

Fuente:: Nielsen Marketing Mix | FMCG | LatAm

TRADE EMPAQUES ESPECIALES 1.6

PROMOCIONES AL CONSUMIDOR 1.5

TPR 1.5

DEMOLADIES 0.2

MEDIA ONLINE 1.7

IMPRESOS 0.9

TV 0.8

ESPECTACULARES 0.6

RADIO 0.5

ROI

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

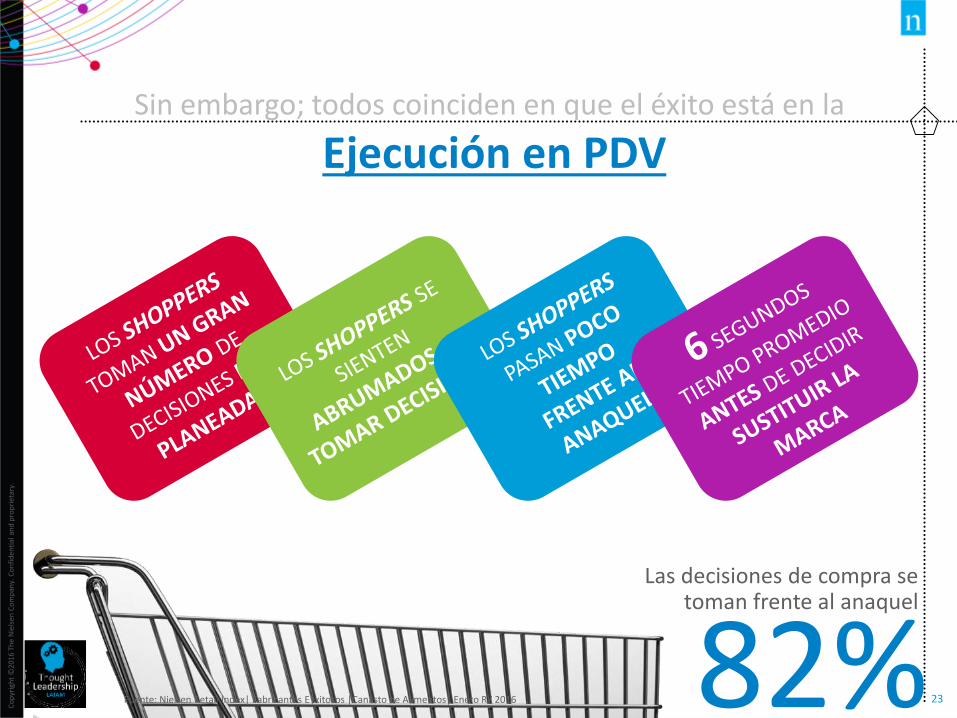

2382%Las decisiones de compra se

toman frente al anaquel

Sin embargo; todos coinciden en que el éxito está en la

Ejecución en PDV

Fuente: Nielsen Retail Index| Fabricantes E|xitosos |Canasto de Alimentos| Enero RY 2016

CAMINO AL ÉXITO

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

25

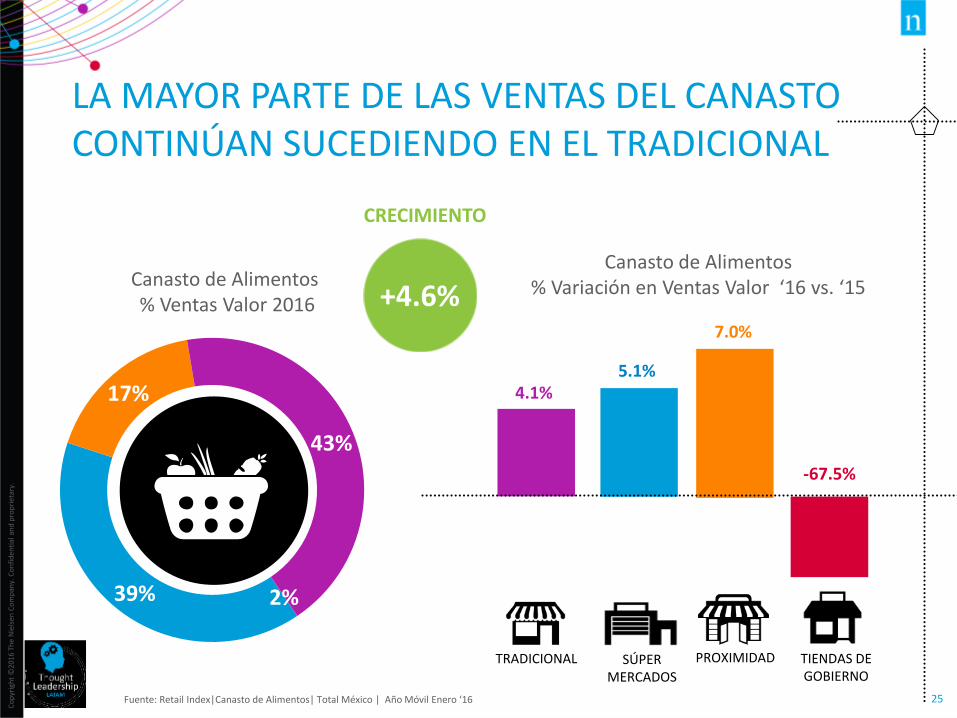

LA MAYOR PARTE DE LAS VENTAS DEL CANASTO CONTINÚAN SUCEDIENDO EN EL TRADICIONAL

Fuente: Retail Index|Canasto de Alimentos| Total México | Año Móvil Enero ‘16

Canasto de Alimentos % Ventas Valor 2016

SÚPER MERCADOS

PROXIMIDADTRADICIONAL TIENDAS DEGOBIERNO

39%

17%

43%

2%

5.1%

7.0%

4.1%

-67.5%

Canasto de Alimentos% Variación en Ventas Valor ‘16 vs. ‘15

CRECIMIENTO

+4.6%

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

26

QUE TAMBIÉN ES UN CANAL CLAVE PARA LOS COMPRADORES DE CARNE

Global Survey Fresh Food 2014

8% 7% 9%13%

9% 10%

39%

47%50%

18%

61%

23%

Category 1 Category 2 Category 3 Category 4

PEQUEÑOS FORMATOS

CANALES TRADICIONALES

Carne y Pollo Frutas y Verduras

Lácteos Panadería DelicatesenPescados y Mariscos

Dónde compran más los consumidores…

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

27

¿CÓMO CRECER EN EL CANAL TRADICIONAL?

Estrategia de Segmentación

Lealtad del Tendero y/o Distribuidor

Conocimiento del Shopper

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

28

ENTENDIENDO AL SHOPPER

25%

48% 9%

9%

9%

Compra Diaria

Fuera deCasa Ítem

Urgente

NoComestibles

Otros

% Shoppers por misión en el Canal Tradicionalvs. 48% en LatAm

HOMBRES51%

Y ESTÁN

3 minutos por visita

Shoppers hacen al menos

37 VISITAS AL MES

Fuente: Nielsen Shopper Trends en México

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

29

MOMENTOS DE CONSUMO QUE AYUDEN A INCREMENTAR NUESTRAS OPORTUNIDADES

33%

22%

16%

16%

13%

Compra diaria

Consumo fuera decasa

Abastecimiento

Remplazos oProductos…

Otros

MODERN TRADE TRADITIONAL TRADE

38%

34%

17%

11%

2%

Consumo fuera decasa

Compra diaria

Remplazos oProductos Urgentes

Otros

Abastecimiento

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

30

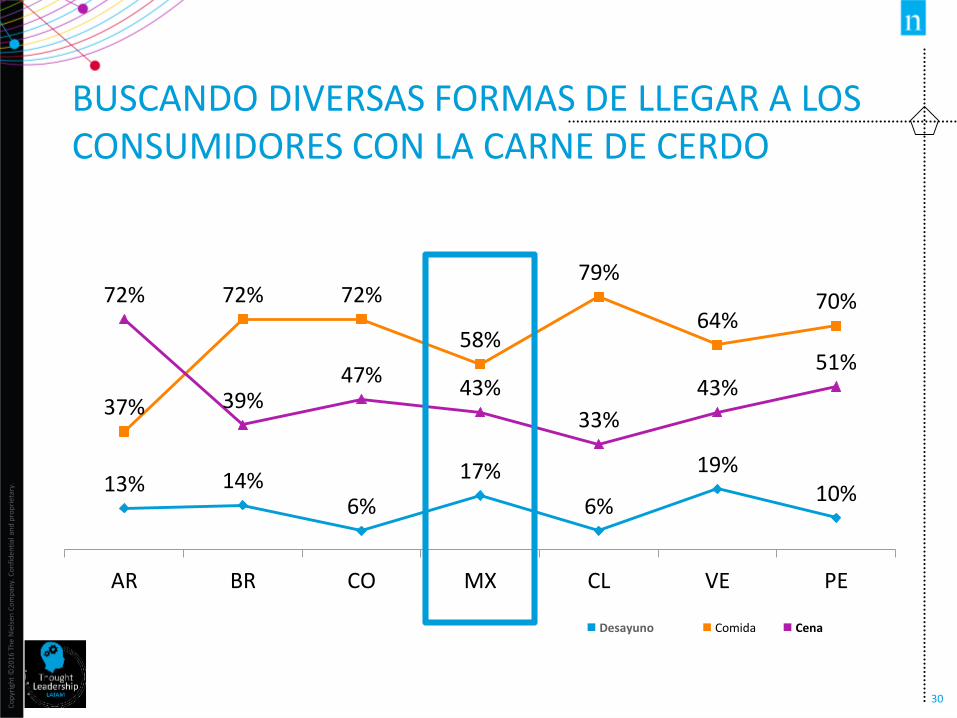

BUSCANDO DIVERSAS FORMAS DE LLEGAR A LOS CONSUMIDORES CON LA CARNE DE CERDO

13% 14%6%

17%

6%

19%10%

37%

72% 72%

58%

79%

64%70%72%

39%47%

43%

33%

43%51%

AR BR CO MX CL VE PE

Desayuno Comida Cena

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

31

OFRECIENDO EL PRODUCTO LISTO PARA COMER

Fuente: Global Survey

Es muy influyente para elegir la tienda que cuente con una amplia variedad de comida fresca y ya preparada

Prefiero visitar algún tipo de tienda si proporciona servicios como…

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

32

ES CLAVE CONSIDERAR UNA ESTRATEGIA DE SEGMENTACIÓN PARA SER MÁS EFICIENTES

Fuente: Nielsen Spectra

Basado en un target de segmentación:

Target

Puntos de interés

Formatos de GCA

Saturación de

Tradicionales

Consumidor Objetivo

89

112 94

127

Family with Teens

Housewife <40 and Oldest Kid 12-17

Young Family

Housewife <40 and Oldest Kid 6-11

New Family

Housewife <40 and Oldest Kid <6

TotalD/ED+C/C-A/B/C+

85

82

Total

Senior Couple

Housewife 60+ and No Kids <18

Mature Couple

Housewife 45-59 and No Kids <18

Young Couple

Housewife <45 and No Kids <18

Mature Family

Housewife 50+ with Any Kids <18

Established Family

Housewife 40-49 with Any Kids <18

115

10073 105 127 92

87

86

99

105

104

117

98

85 148 106

88 124 143 106

70

76 133

76 111 132

105 127

59 89 112

58 87 112

LifeStyle

BehaviorStage

62 87 111 86 88

Familias y Parejas NSE Medio/Bajo

Zonas con comercio:

-Tradicional-popular

-Comida (restaurantes, comida para llevar y comida rápida)

-Papelerías

Sub desarrollo de Express

Sobre desarrollo Bodegas

Optimización de resultados

ECOSISTEMA ÓPTIMO

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

33

Municipios Oriente TARGET POISFORMATO

GCA

TRADICIO-

NALES

Atlautla (MEX) Potencial Potencial

Chimalhuacán (MEX) Potencial Potencial Potencial Potencial

Valle de Chalco Solidaridad (MEX) Potencial Potencial Potencial

Juchitepec (MEX) Potencial Potencial

Tepetlixpa (MEX) Potencial Potencial

Chalco (MEX) Potencial Potencial Potencial Potencial

Temamatla (MEX) Potencial Potencial

Ayapango (MEX) Potencial

Ozumba (MEX) Potencial Potencial

La Paz (MEX) Potencial Potencial

Amecameca (MEX) Potencial Potencial

Tenango del Aire (MEX) Potencial Potencial

Chicoloapan (MEX) Potencial Potencial Potencial

Tlalmanalco (MEX) Potencial Potencial

Cocotitlán (MEX) Potencial Potencial

Ixtapaluca (MEX) Potencial Potencial Potencial Potencial

Tláhuac (DF) Potencial Potencial Potencial

Milpa Alta (DF) Potencial Potencial Potencial

Iztapalapa (DF) Potencial Potencial Potencial Potencial

Nezahualcóyotl (MEX) Potencial Potencial Potencial

Iztacalco (DF) Potencial Potencial Potencial

Xochimilco (DF) Potencial Potencial Potencial Potencial

La Magdalena Contreras (DF) Potencial Potencial

Venustiano Carranza (DF) Potencial Potencial Potencial

Naucalpan de Juárez (MEX) Potencial Potencial Potencial Potencial

Gustavo A. Madero (DF) Potencial Potencial Potencial

Cuajimalpa de Morelos (DF) Potencial Potencial

Cuauhtémoc (DF) Potencial Potencial Potencial

Álvaro Obregón (DF) Potencial Potencial

Tlalpan (DF) Potencial Potencial

Huixquilucan (MEX) Potencial Potencial

Miguel Hidalgo (DF) Potencial

Coyoacán (DF) Potencial Potencial

Benito Juárez (DF) Potencial

P1

P1

P1

P1

P1

P1

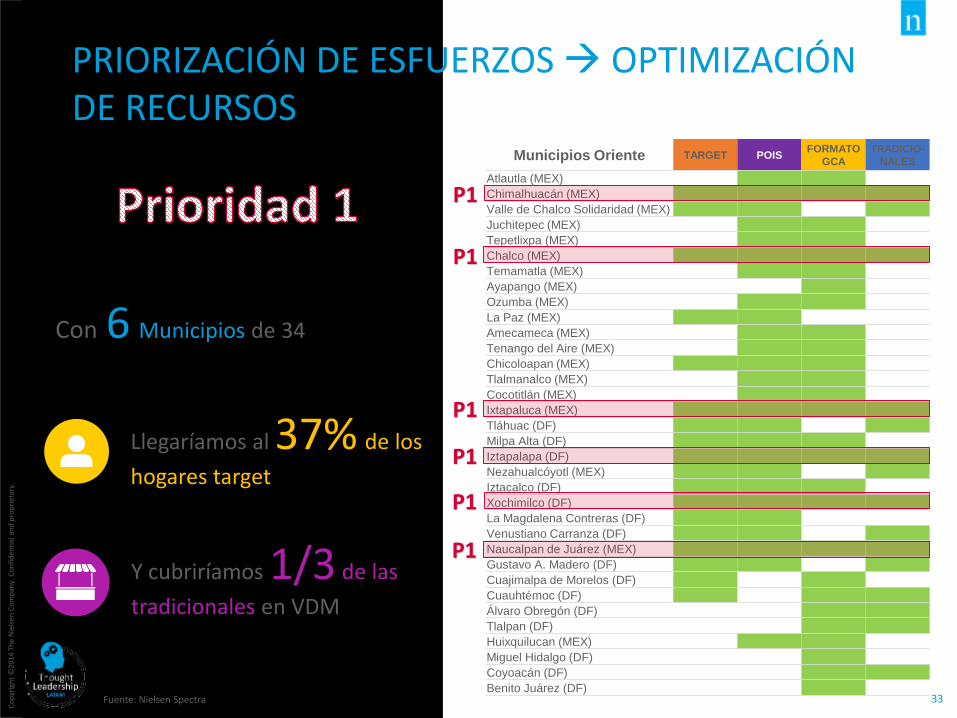

PRIORIZACIÓN DE ESFUERZOS OPTIMIZACIÓN DE RECURSOS

Con 6 Municipios de 34

Llegaríamos al 37% de los

hogares target

Y cubriríamos 1/3 de las

tradicionales en VDM

Fuente: Nielsen Spectra

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

34

CON ESTA SEGMENTACIÓN PODEMOS REDUCIR EL SCOPE Y ATERRIZAR DE FORMA EFICIENTE A NIVEL RUTA O MAYORISTA LAS ESTRATEGIAS

En base a estas prioridades podemos aterrizar los esfuerzos a rutas

Prioridad 1

Prioridad 2

Prioridad 3

Y de esta manera priorizar la inversión y el “go to market” de nuestras marcas

Distribución Indirecta / Mayoristas

Distribución Directa / Rutas

Fuente: Nielsen Spectra

DECLARA QUE EL TENDERO TIENE ALGUNA INFLUENCIA EN SU DESICIÓN DE COMPRA

DE LOS MEXICANOS ENCUESTADOS

Fuente: Nielsen Shopper Solutions 2015

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

36

TENDERO Y DISTRIBUIDOR

PARA LOS TENDEROS MEXICANOS:¿Qué consideras que los fabricantes deben hacer para ayudarte en tu negocio?

Fuente: Encuesta a Dueños de Tiendas 2015

LA VOZ DE LOS TENDEROS NECESITA

SER ESCUCHADA

8%

8%

15%

27%

25%

Beneficios extras para minegocio (Pintar Paredes)

Visitas más frecuentes

Paquetes Promocionales

Más producto por Volumende Compra

Más Crédito

Mencionada como la más importante

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

37

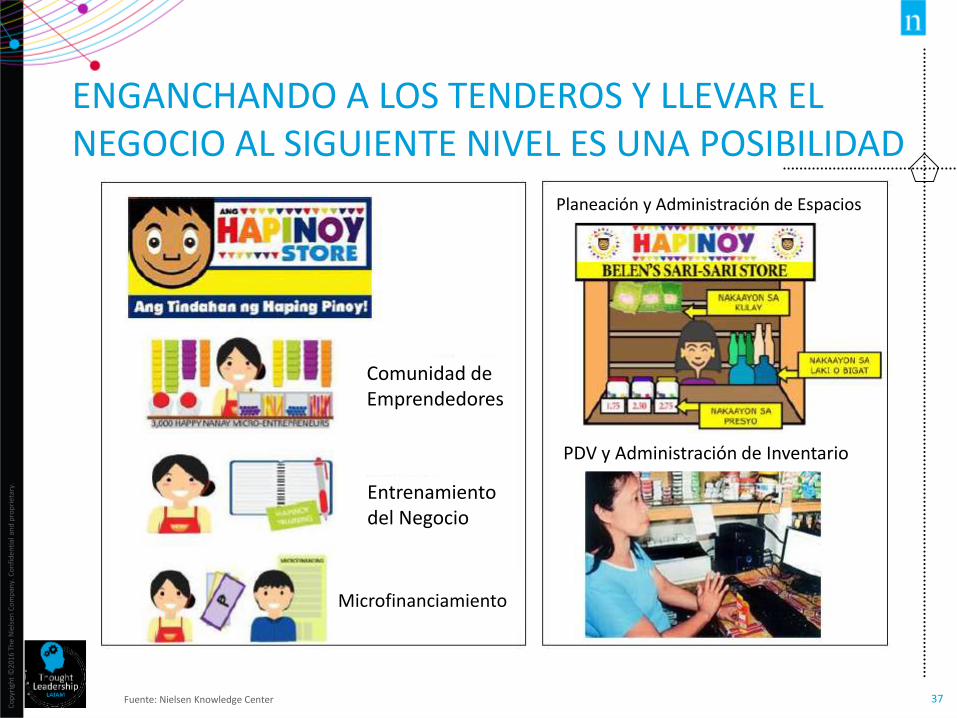

ENGANCHANDO A LOS TENDEROS Y LLEVAR EL NEGOCIO AL SIGUIENTE NIVEL ES UNA POSIBILIDAD

Comunidad de Emprendedores

Entrenamiento del Negocio

Microfinanciamiento

PDV y Administración de Inventario

Planeación y Administración de Espacios

Fuente: Nielsen Knowledge Center

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

38

EN AUTOSERVICIOS, LA HISTORIA NO ES DIFERENTE, NO ESTAR PRESENTE TIENE UN COSTO MUY ALTO…

Fuente: Nielsen On Shelf Availability

63%REPRESENTAN VENTA PERDIDA

AGOTAMIENTOS

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

39

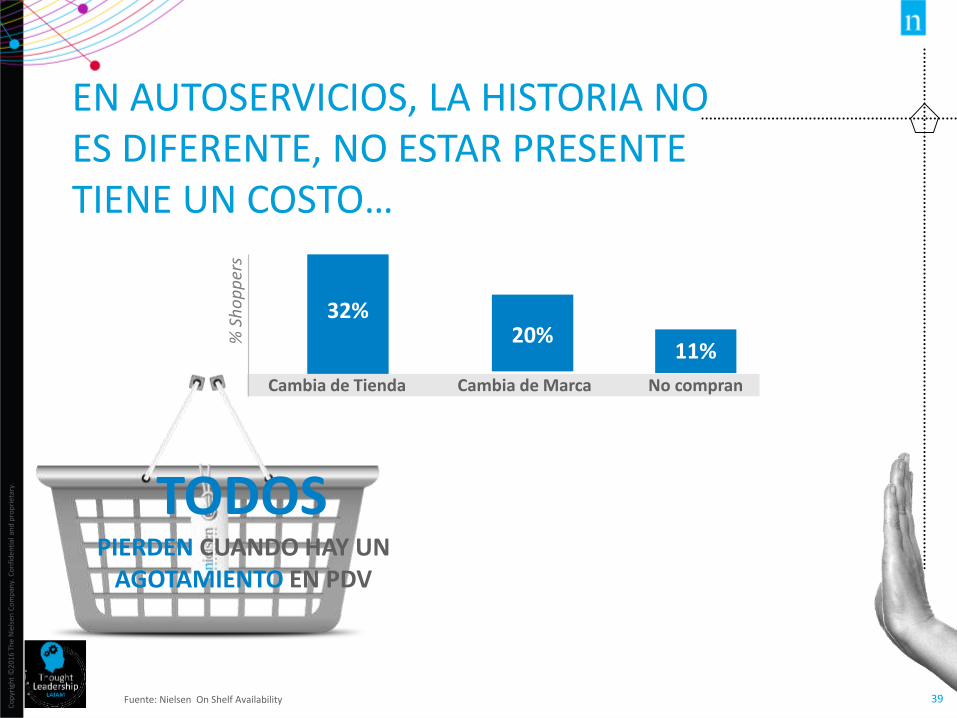

EN AUTOSERVICIOS, LA HISTORIA NO ES DIFERENTE, NO ESTAR PRESENTE TIENE UN COSTO…

Fuente: Nielsen On Shelf Availability

Cambia de Tienda Cambia de Marca No compran

PIERDEN CUANDO HAY UN AGOTAMIENTO EN PDV

TODOS

32%20%

11%

% S

ho

pp

ers

Co

pyr

igh

t ©

2016

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

40

HAY QUE RECORDAR QUE PARA INCREMENTAR DEMANDA EN EL PDV NO TODO ES PRECIOIMPACTO PROMEDIO POR TIENDAÍTEM AL EJECUTAR SOBRE UN SKU REGULAR

Fuente: Nielsen Analytic Consulting *Price & Promo° 140 ítems analizados y 200,000 observaciones promedio por ítem

10% de Descuento 21% 16%

20% de Descuento 51% 36%

30% 39%Exhibiciones en Punto de Venta

37% 22%POP

64% 43%Empaques Promocionales

TOTAL ALIMENTOS