RETENCION EN EL ORIGEN DE LA CONTRIBUCION SOBRE … · ingresos sobre dichos salarios, de acuerdo a...

31

ESTADO LIBRE ASOCIADO DE PUERTO RICO DEPARTAMENTO DE HACIENDA PO BOX 9024140 SAN JUAN PR 00902-4140 COMMONWEALTH OF PUERTO RICO DEPARTMENT OF THE TREASURY PO BOX 9024140 SAN JUAN PR 00902-4140 RETENCION EN EL ORIGEN DE LA CONTRIBUCION SOBRE INGRESOS EN EL CASO DE SALARIOS WITHHOLDING OF INCOME TAX AT SOURCE ON WAGES MANUAL PARA PATRONOS EMPLOYER'S GUIDE LAS TABLAS DE RETENCION QUE APARECEN EN ESTE FOLLETO SON DE APLICACION A SALARIOS PAGADOS DESPUES DEL 31 DE DICIEMBRE DE 2013 Y ANTES DEL 1 DE ENERO DE 2015 THE WITHHOLDING TABLES SHOWN IN THIS BOOKLET ARE APPLICABLE TO WAGES PAID AFTER DECEMBER 31, 2013 AND BEFORE JANUARY 1, 2015

Transcript of RETENCION EN EL ORIGEN DE LA CONTRIBUCION SOBRE … · ingresos sobre dichos salarios, de acuerdo a...

ESTADO LIBRE ASOCIADO DE PUERTO RICODEPARTAMENTO DE HACIENDA

PO BOX 9024140 SAN JUAN PR 00902-4140

COMMONWEALTH OF PUERTO RICODEPARTMENT OF THE TREASURY

PO BOX 9024140 SAN JUAN PR 00902-4140

RETENCION EN EL ORIGEN DE LACONTRIBUCION SOBRE INGRESOS

EN EL CASO DE SALARIOS

WITHHOLDING OF INCOME TAX ATSOURCE ON WAGES

MANUAL PARA PATRONOS

EMPLOYER'S GUIDE

LAS TABLAS DE RETENCION QUE APARECEN EN ESTE FOLLETOSON DE APLICACION A SALARIOS PAGADOS DESPUES DEL

31 DE DICIEMBRE DE 2013 Y ANTES DEL 1 DE ENERO DE 2015

THE WITHHOLDING TABLES SHOWN IN THIS BOOKLETARE APPLICABLE TO WAGES PAID AFTER DECEMBER 31, 2013 AND

BEFORE JANUARY 1, 2015

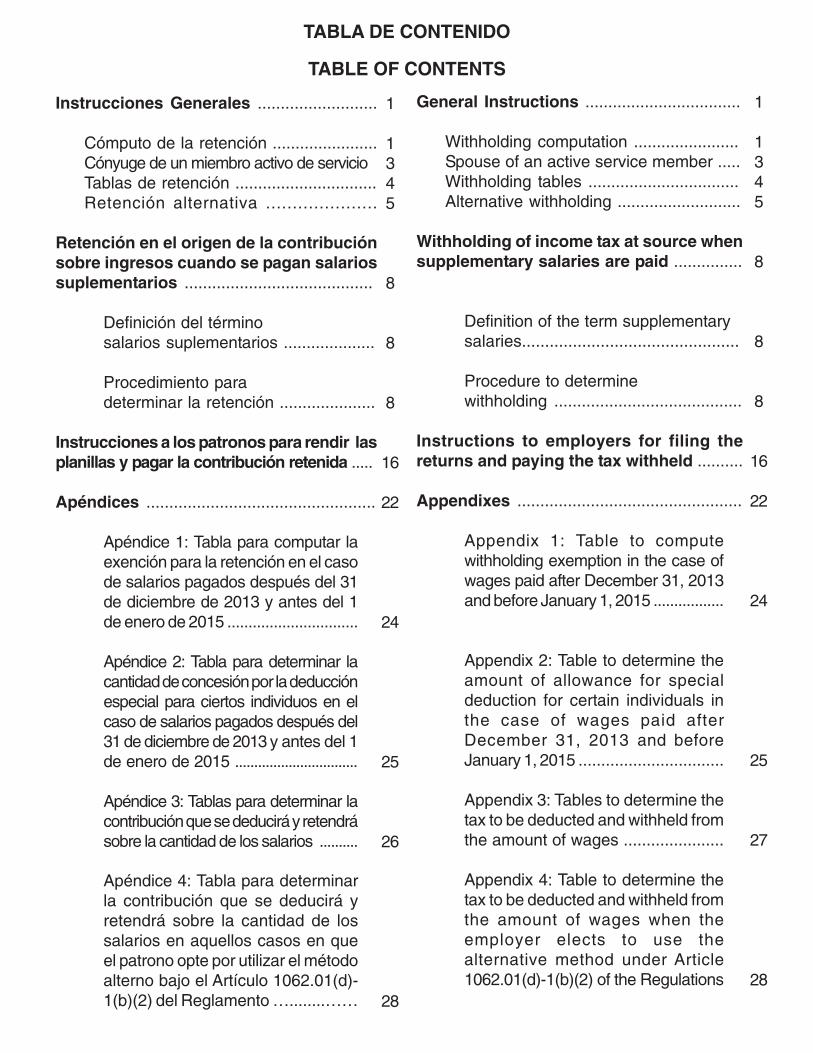

TABLA DE CONTENIDO

TABLE OF CONTENTS

Instrucciones Generales ..........................

Cómputo de la retención .......................Cónyuge de un miembro activo de servicioTablas de retención ...............................Retención alternativa .....................

Retención en el origen de la contribuciónsobre ingresos cuando se pagan salariossuplementarios .........................................

Definición del términosalarios suplementarios ....................

Procedimiento paradeterminar la retención .....................

Instrucciones a los patronos para rendir lasplanillas y pagar la contribución retenida .....

Apéndices ..................................................

Apéndice 1: Tabla para computar laexención para la retención en el casode salarios pagados después del 31de diciembre de 2013 y antes del 1de enero de 2015 ...............................

Apéndice 2: Tabla para determinar lacantidad de concesión por la deducciónespecial para ciertos individuos en elcaso de salarios pagados después del31 de diciembre de 2013 y antes del 1de enero de 2015 ................................

Apéndice 3: Tablas para determinar lacontribución que se deducirá y retendrásobre la cantidad de los salarios ..........

Apéndice 4: Tabla para determinarla contribución que se deducirá yretendrá sobre la cantidad de lossalarios en aquellos casos en queel patrono opte por utilizar el métodoalterno bajo el Artículo 1062.01(d)-1(b)(2) del Reglamento …........……

1

1345

8

8

8

16

22

24

25

26

28

General Instructions ..................................

Withholding computation .......................Spouse of an active service member .....Withholding tables .................................Alternative withholding ...........................

Withholding of income tax at source whensupplementary salaries are paid ...............

Definition of the term supplementarysalaries...............................................

Procedure to determinewithholding .........................................

Instructions to employers for filing thereturns and paying the tax withheld ..........

Appendixes .................................................

Appendix 1: Table to computewithholding exemption in the case ofwages paid after December 31, 2013and before January 1, 2015 .................

Appendix 2: Table to determine theamount of allowance for specialdeduction for certain individuals inthe case of wages paid afterDecember 31, 2013 and beforeJanuary 1, 2015 ................................

Appendix 3: Tables to determine thetax to be deducted and withheld fromthe amount of wages ......................

Appendix 4: Table to determine thetax to be deducted and withheld fromthe amount of wages when theemployer elects to use thealternative method under Article1062.01(d)-1(b)(2) of the Regulations

1

1345

8

8

8

16

22

24

25

27

28

INSTRUCCIONES GENERALES

GENERAL INSTRUCTIONS

1

La Sección 1062.01 del Código de Rentas Internasde Puerto Rico de 2011, según enmendado (Código),dispone que todo patrono que haga pagos desalarios deducirá y retendrá contribución sobreingresos sobre dichos salarios, de acuerdo a lastablas de retención aprobadas por el Secretario, lascuales forman parte de este folleto.

No obstante, todo empleado cuyo salario bruto anualno exceda de $20,000, no estará sujeto a retención decontribución sobre ingresos en el origen sobre dichossalarios. Sin embargo, el empleado podrá optarporque se le efectúe retención indicando la cantidaden el Certificado de Exención para la Retención(Formulario 499 R-4).

COMPUTO DE LA RETENCION

La base para el cómputo de la contribución que sededucirá y retendrá en el origen será la diferenciaentre los salarios y la exención para la retención aque tenga derecho el empleado.

La exención para la retención (véase Apéndice 1)se compone de las siguientes:

1. Exención personal,2. Exención personal adicional para veteranos (si aplica),3. Exención por dependientes,4. Concesión por deducción especial, y5. Concesión por deducciones (opcional).

En general, se utilizarán tres tablas para determinarla cantidad que se deberá deducir y retener sobrelos salarios pagados. No obstante, cuando el patronoopte por utilizar el método alterno bajo el Artículo1062.01(d)-1(b)(2) del Reglamento, se incorporaráel uso de una tabla adicional.

La primera tabla, "Tabla para Computar la Exenciónpara la Retención en el Caso de Salarios PagadosDespués del 31 de Diciembre de 2013 y Antes del 1de Enero de 2015" (Apéndice 1), se utiliza paradeterminar la cantidad de exención para la retencióna que tiene derecho el empleado de acuerdo con superíodo de nómina y a si opta por reclamar o noalgún componente de su exención, segúnenumerados anteriormente.

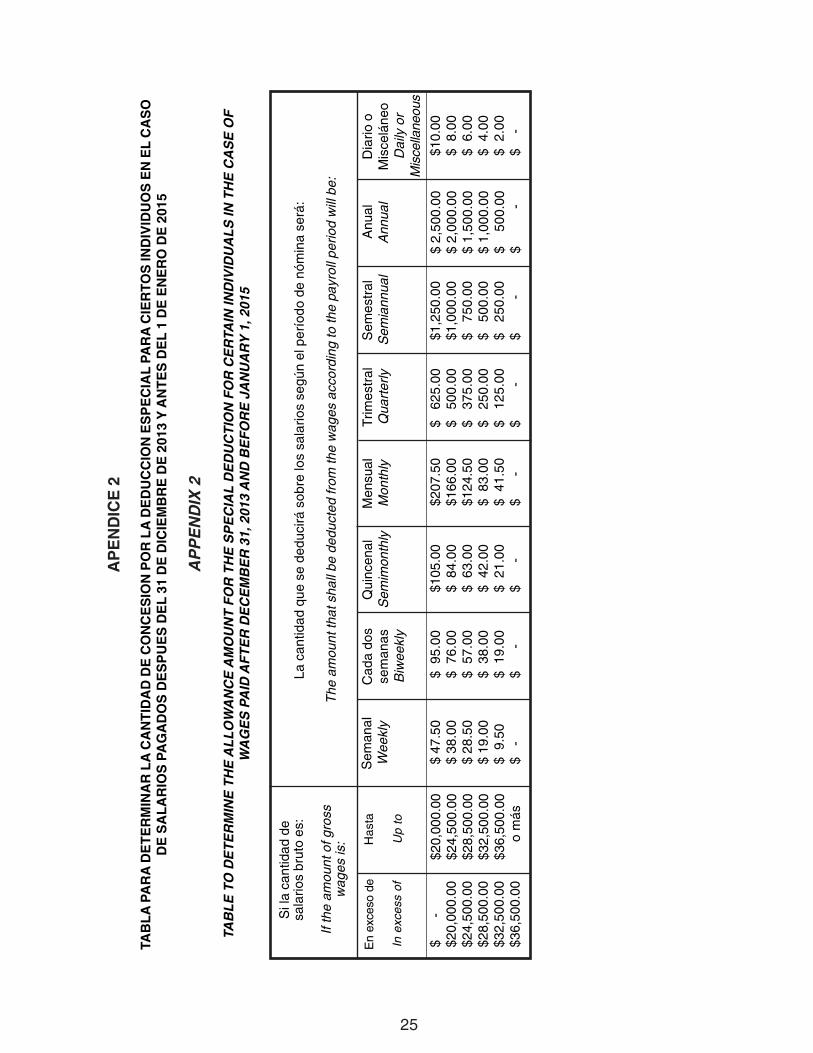

La segunda tabla, "Tabla para Determinar la Cantidadde Concesión por la Deducción Especial para CiertosIndividuos en el Caso de Salarios Pagados Despuésdel 31 de Diciembre de 2013 y Antes del 1 de Enero de2015" (Apéndice 2), establece la cantidad que sededucirá sobre los salarios por concepto de laconcesión por deducción especial para ciertosindividuos, según el período de nómina.

Section 1062.01 of the Puerto Rico InternalRevenue Code of 2011, as amended (Code),provides that every employer making paymentsof wages shall deduct and withhold income taxfrom such wages, according to the withholdingtables approved by the Secretary, which are partof this booklet.

Notwithstanding, every employee whose grossannual salary does not exceed $20,000, will notbe subject to the withholding of income tax atsource from such wages. However, theemployee may elect that an amount be withheldby indicating so on the Withholding ExemptionCertificate (Form 499 R-4.1).

WITHHOLDING COMPUTATION

The basis for the computation of the tax to be deductedand withheld at source shall be the difference betweenthe total wages and the withholding exemption to whichthe employee is entitled.

The withholding exemption consists of the following:(see Appendix 1)

1. Personal exemption,2. Additional personal exemption for veterans (if applicable),3. Exemption for dependents,4. Allowance for special deduction, and5. Allowance for deductions (optional).

In general, three tables will be used to determinethe amount to be deducted and withheld from thewages paid. However, if the employer elects to usethe alternative method under Article 1062.01(d)-1(b)(2) of the Regulations, an additional table maybe used.

The first table, "Table to Compute the WithholdingExemption in the Case of Wages Paid AfterDecember 31, 2013 and Before January 1, 2015"(Appendix 1), must be used to determine theamount of the withholding exemption to which theemployee is entitled in accordance with his/herpayroll period and whether or not he/she claimsany component of his/her exemption, as previouslyindicated.

The second table, "Table to Determine the AllowanceAmount for the Special Deduction for CertainIndividuals in the Case of Wages Paid AfterDecember 31, 2013 and Before January 1, 2015"(Appendix 2), sets forth the amount to be deductedfrom wages in connection with the amount allowedfor the special deduction for certain individuals,according to the payroll period.

2

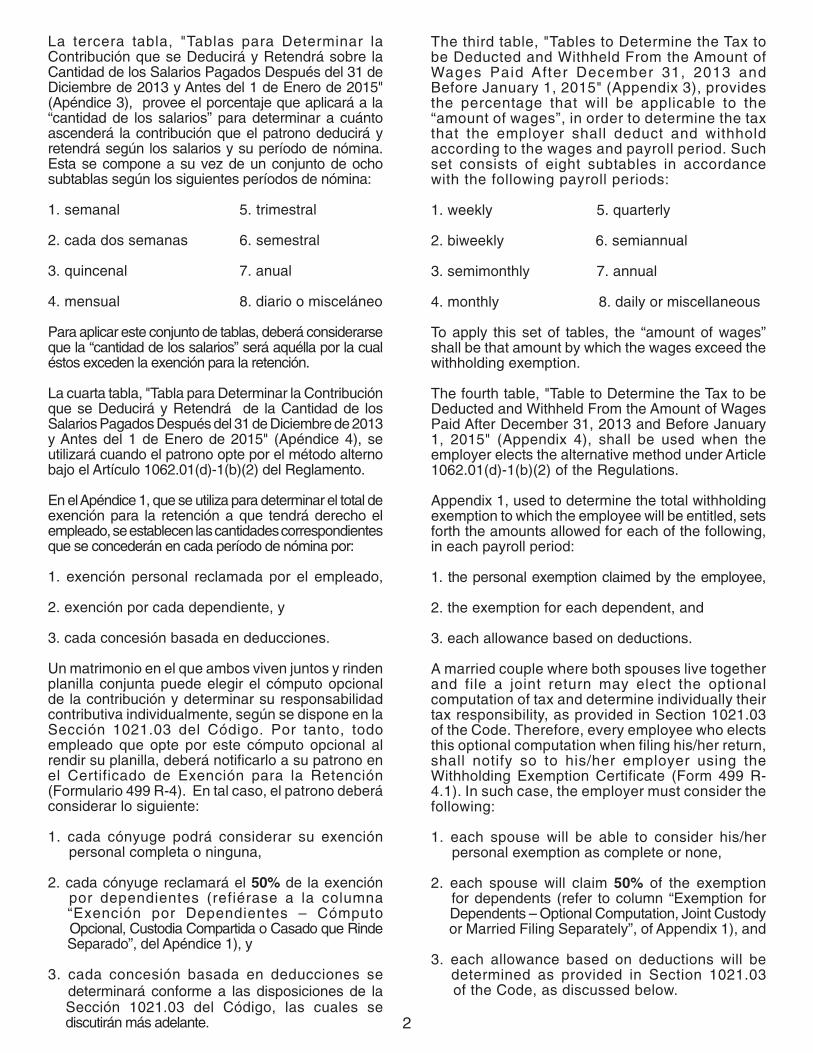

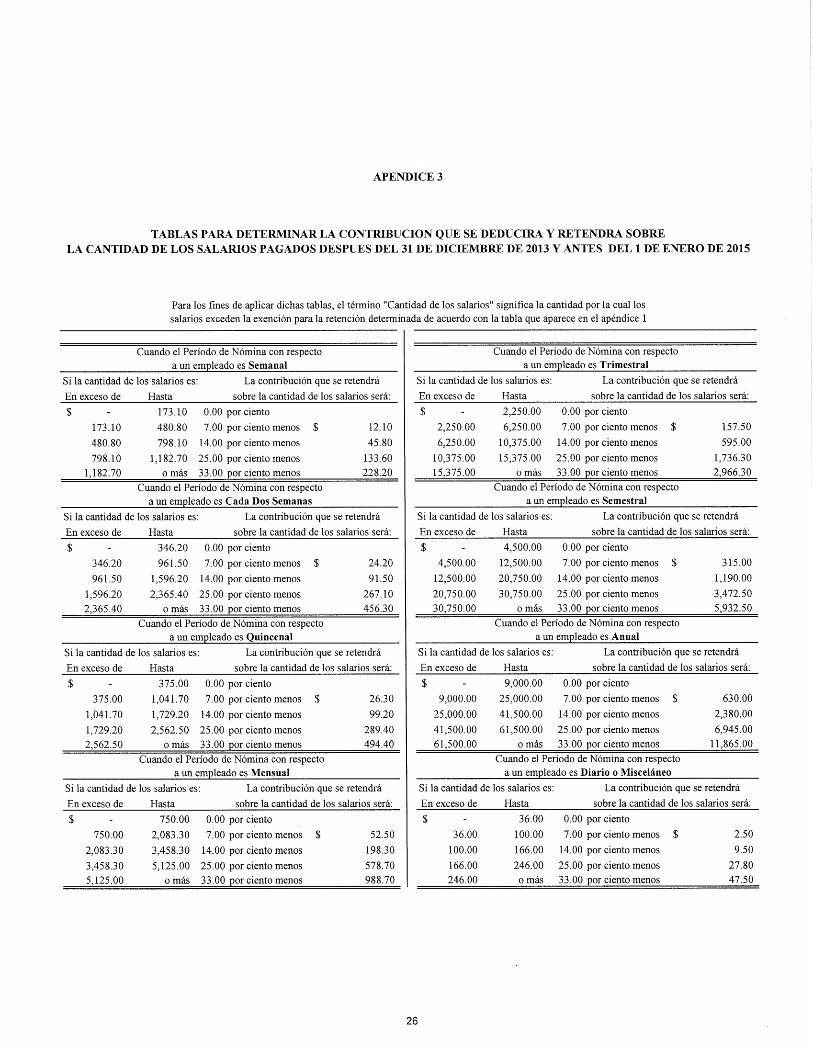

La tercera tabla, "Tablas para Determinar laContribución que se Deducirá y Retendrá sobre laCantidad de los Salarios Pagados Después del 31 deDiciembre de 2013 y Antes del 1 de Enero de 2015"(Apéndice 3), provee el porcentaje que aplicará a la“cantidad de los salarios” para determinar a cuántoascenderá la contribución que el patrono deducirá yretendrá según los salarios y su período de nómina.Esta se compone a su vez de un conjunto de ochosubtablas según los siguientes períodos de nómina:

1. semanal 5. trimestral

2. cada dos semanas 6. semestral

3. quincenal 7. anual

4. mensual 8. diario o misceláneo

Para aplicar este conjunto de tablas, deberá considerarseque la “cantidad de los salarios” será aquélla por la cualéstos exceden la exención para la retención.

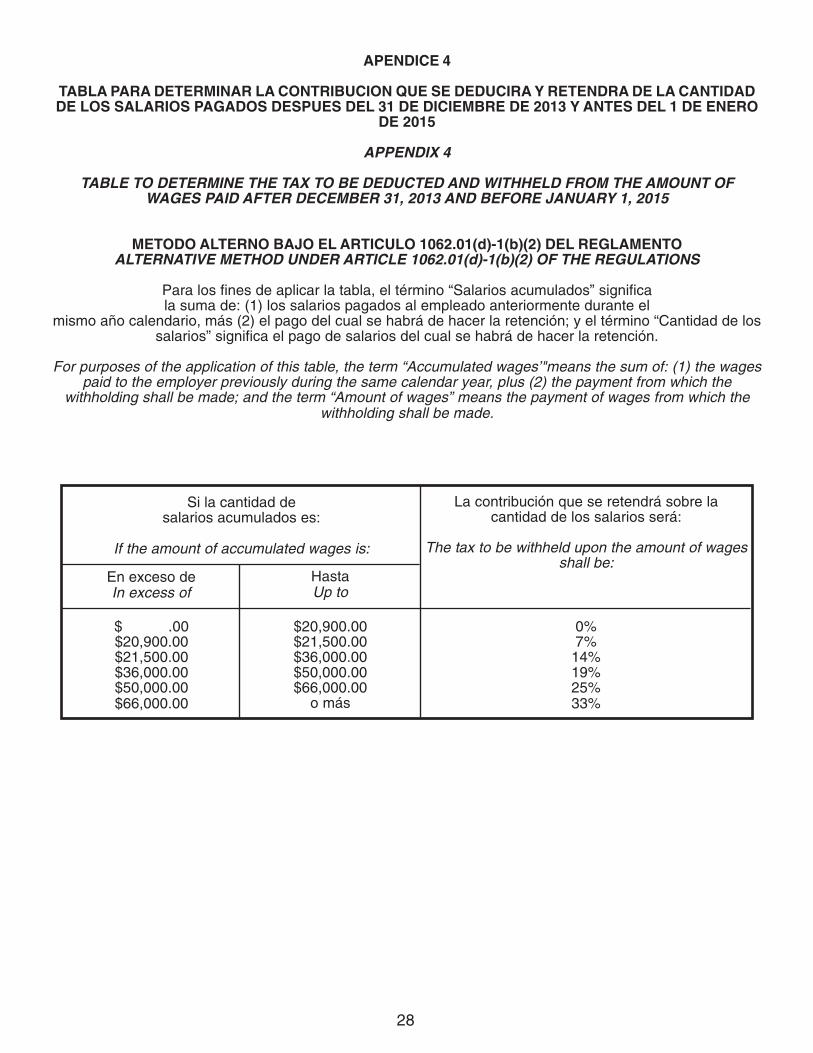

La cuarta tabla, "Tabla para Determinar la Contribuciónque se Deducirá y Retendrá de la Cantidad de losSalarios Pagados Después del 31 de Diciembre de 2013y Antes del 1 de Enero de 2015" (Apéndice 4), seutilizará cuando el patrono opte por el método alternobajo el Artículo 1062.01(d)-1(b)(2) del Reglamento.

En el Apéndice 1, que se utiliza para determinar el total deexención para la retención a que tendrá derecho elempleado, se establecen las cantidades correspondientesque se concederán en cada período de nómina por:

1. exención personal reclamada por el empleado,

2. exención por cada dependiente, y

3. cada concesión basada en deducciones.

Un matrimonio en el que ambos viven juntos y rindenplanilla conjunta puede elegir el cómputo opcionalde la contribución y determinar su responsabilidadcontributiva individualmente, según se dispone en laSección 1021.03 del Código. Por tanto, todoempleado que opte por este cómputo opcional alrendir su planilla, deberá notificarlo a su patrono enel Certificado de Exención para la Retención(Formulario 499 R-4). En tal caso, el patrono deberáconsiderar lo siguiente:

1. cada cónyuge podrá considerar su exención personal completa o ninguna,

2. cada cónyuge reclamará el 50% de la exención por dependientes (refiérase a la columna “Exención por Dependientes – Cómputo Opcional, Custodia Compartida o Casado que Rinde Separado”, del Apéndice 1), y

3. cada concesión basada en deducciones se determinará conforme a las disposiciones de la Sección 1021.03 del Código, las cuales se discutirán más adelante.

The third table, "Tables to Determine the Tax tobe Deducted and Withheld From the Amount ofWages Paid After December 31, 2013 andBefore January 1, 2015" (Appendix 3), providesthe percentage that will be applicable to the“amount of wages”, in order to determine the taxthat the employer shall deduct and withholdaccording to the wages and payroll period. Suchset consists of eight subtables in accordancewith the following payroll periods:

1. weekly 5. quarterly

2. biweekly 6. semiannual

3. semimonthly 7. annual

4. monthly 8. daily or miscellaneous

To apply this set of tables, the “amount of wages”shall be that amount by which the wages exceed thewithholding exemption.

The fourth table, "Table to Determine the Tax to beDeducted and Withheld From the Amount of WagesPaid After December 31, 2013 and Before January1, 2015" (Appendix 4), shall be used when theemployer elects the alternative method under Article1062.01(d)-1(b)(2) of the Regulations.

Appendix 1, used to determine the total withholdingexemption to which the employee will be entitled, setsforth the amounts allowed for each of the following,in each payroll period:

1. the personal exemption claimed by the employee,

2. the exemption for each dependent, and

3. each allowance based on deductions.

A married couple where both spouses live togetherand file a joint return may elect the optionalcomputation of tax and determine individually theirtax responsibility, as provided in Section 1021.03of the Code. Therefore, every employee who electsthis optional computation when filing his/her return,shall notify so to his/her employer using theWithholding Exemption Certificate (Form 499 R-4.1). In such case, the employer must consider thefollowing:

1. each spouse will be able to consider his/her personal exemption as complete or none,

2. each spouse will claim 50% of the exemption for dependents (refer to column “Exemption for Dependents – Optional Computation, Joint Custody or Married Filing Separately”, of Appendix 1), and

3. each allowance based on deductions will be determined as provided in Section 1021.03 of the Code, as discussed below.

3

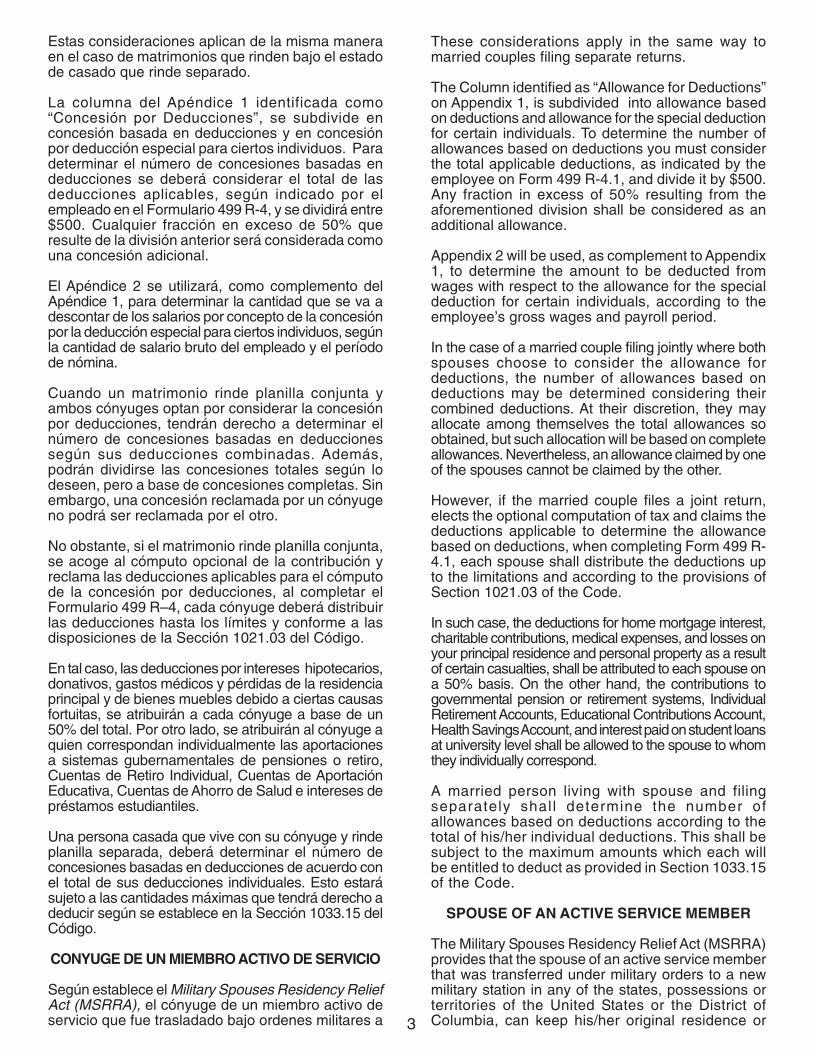

Estas consideraciones aplican de la misma maneraen el caso de matrimonios que rinden bajo el estadode casado que rinde separado.

La columna del Apéndice 1 identificada como“Concesión por Deducciones”, se subdivide enconcesión basada en deducciones y en concesiónpor deducción especial para ciertos individuos. Paradeterminar el número de concesiones basadas endeducciones se deberá considerar el total de lasdeducciones aplicables, según indicado por elempleado en el Formulario 499 R-4, y se dividirá entre$500. Cualquier fracción en exceso de 50% queresulte de la división anterior será considerada comouna concesión adicional.

El Apéndice 2 se utilizará, como complemento delApéndice 1, para determinar la cantidad que se va adescontar de los salarios por concepto de la concesiónpor la deducción especial para ciertos individuos, segúnla cantidad de salario bruto del empleado y el períodode nómina.

Cuando un matrimonio rinde planilla conjunta yambos cónyuges optan por considerar la concesiónpor deducciones, tendrán derecho a determinar elnúmero de concesiones basadas en deduccionessegún sus deducciones combinadas. Además,podrán dividirse las concesiones totales según lodeseen, pero a base de concesiones completas. Sinembargo, una concesión reclamada por un cónyugeno podrá ser reclamada por el otro.

No obstante, si el matrimonio rinde planilla conjunta,se acoge al cómputo opcional de la contribución yreclama las deducciones aplicables para el cómputode la concesión por deducciones, al completar elFormulario 499 R–4, cada cónyuge deberá distribuirlas deducciones hasta los límites y conforme a lasdisposiciones de la Sección 1021.03 del Código.

En tal caso, las deducciones por intereses hipotecarios,donativos, gastos médicos y pérdidas de la residenciaprincipal y de bienes muebles debido a ciertas causasfortuitas, se atribuirán a cada cónyuge a base de un50% del total. Por otro lado, se atribuirán al cónyuge aquien correspondan individualmente las aportacionesa sistemas gubernamentales de pensiones o retiro,Cuentas de Retiro Individual, Cuentas de AportaciónEducativa, Cuentas de Ahorro de Salud e intereses depréstamos estudiantiles.

Una persona casada que vive con su cónyuge y rindeplanilla separada, deberá determinar el número deconcesiones basadas en deducciones de acuerdo conel total de sus deducciones individuales. Esto estarásujeto a las cantidades máximas que tendrá derecho adeducir según se establece en la Sección 1033.15 delCódigo.

CONYUGE DE UN MIEMBRO ACTIVO DE SERVICIO

Según establece el Military Spouses Residency ReliefAct (MSRRA), el cónyuge de un miembro activo deservicio que fue trasladado bajo ordenes militares a

These considerations apply in the same way tomarried couples filing separate returns.

The Column identified as “Allowance for Deductions”on Appendix 1, is subdivided into allowance basedon deductions and allowance for the special deductionfor certain individuals. To determine the number ofallowances based on deductions you must considerthe total applicable deductions, as indicated by theemployee on Form 499 R-4.1, and divide it by $500.Any fraction in excess of 50% resulting from theaforementioned division shall be considered as anadditional allowance.

Appendix 2 will be used, as complement to Appendix1, to determine the amount to be deducted fromwages with respect to the allowance for the specialdeduction for certain individuals, according to theemployee’s gross wages and payroll period.

In the case of a married couple filing jointly where bothspouses choose to consider the allowance fordeductions, the number of allowances based ondeductions may be determined considering theircombined deductions. At their discretion, they mayallocate among themselves the total allowances soobtained, but such allocation will be based on completeallowances. Nevertheless, an allowance claimed by oneof the spouses cannot be claimed by the other.

However, if the married couple files a joint return,elects the optional computation of tax and claims thedeductions applicable to determine the allowancebased on deductions, when completing Form 499 R-4.1, each spouse shall distribute the deductions upto the limitations and according to the provisions ofSection 1021.03 of the Code.

In such case, the deductions for home mortgage interest,charitable contributions, medical expenses, and losses onyour principal residence and personal property as a resultof certain casualties, shall be attributed to each spouse ona 50% basis. On the other hand, the contributions togovernmental pension or retirement systems, IndividualRetirement Accounts, Educational Contributions Account,Health Savings Account, and interest paid on student loansat university level shall be allowed to the spouse to whomthey individually correspond.

A married person living with spouse and filingseparately shal l determine the number ofallowances based on deductions according to thetotal of his/her individual deductions. This shall besubject to the maximum amounts which each willbe entitled to deduct as provided in Section 1033.15of the Code.

SPOUSE OF AN ACTIVE SERVICE MEMBER

The Military Spouses Residency Relief Act (MSRRA)provides that the spouse of an active service memberthat was transferred under military orders to a newmilitary station in any of the states, possessions orterritories of the United States or the District ofColumbia, can keep his/her original residence or

4

una nueva estación militar en alguno de los estados,posesiones o territorios de Estados Unidos o elDistrito de Columbia, puede mantener su residenciao domicilio original para propósitos de tributación. Porlo tanto, si el empleado es el cónyuge de un militar quefue trasladado a Puerto Rico y opta por acogerse a lasdisposiciones de MSRRA, no estará sujeto a retenciónde contribución sobre ingresos en el origen en PuertoRico sobre los salarios generados aquí. Para estospropósitos, es necesario que el empleado seleccionela opción provista en el Certificado de Exención para laRetención (Formulario 499 R-4).

Aunque el patrono no venga obligado a retener en elorigen sobre los salarios para propósitos de Puerto Rico,podría estar sujeto a retener impuestos federales segúndisponga el Internal Revenue Service.

TABLAS DE RETENCION

Las Tablas de Retención que aparecen en las páginassiguientes consideran los cambios implantados alSistema de Retención sobre Salarios de acuerdo conel Código.

En el Apéndice 1, aparece la tabla para determinarla cantidad de exención para retención.

En el Apéndice 2, aparece la tabla para determinarel importe que se deducirá del total de los salariospor la deducción especial para ciertos individuos.

En el Apéndice 3, aparecen las tablas paradeterminar el importe de la contribución que sededucirá y retendrá sobre el total de los salarios.

En el Apéndice 4, aparece la tabla para determinar elimporte de la contribución que se deducirá y retendrásobre el total de los salarios en aquellos casos dondeel patrono opte por utilizar el método alterno bajo elArtículo 1062.01(d)-1(b)(2) del Reglamento.

ESTAS TABLAS SERAN DE APLICACION A SALARIOSQUE SE PAGUEN DESPUES DEL 31 DE DICIEMBREDE 2013 Y ANTES DEL 1 DE ENERO DEL 2015.

A continuación se ilustra mediante ejemplos laaplicación de las tablas de retención:

Ejemplo 1: "A" es una persona soltera que no haceaportaciones de su salario a un sistemagubernamental de pensiones o retiro (con excepcióndel Seguro Social) y reclama la totalidad de laexención personal y la concesión por deducciones."A" es artista gráfico y recibe un sueldo mensual de$2,200. Estima que durante el año podrá reclamar$4,500 por concepto de intereses hipotecarios y asílo hace constar en el Certificado de Exención para laRetención (Formulario 499 R-4).

El total de contribución que se retendrá sobre$2,200 será $46.20, determinado como sigue:Salario Total………....……….........……... $2,200.00

domicile for tax purposes. Therefore, if the employeeis the spouse of an active service member that wastransferred to Puerto Rico and makes an electionto be covered under the provisions of MSRRA,earned wages within Puerto Rico will not be subjectto income tax withholding at source. For thesepurposes, it is necessary that the employee selectsthe option provided in the Withholding ExemptionCertificate (Form 499 R-4.1).

Even though the employer will not be required towithhold at source on wages for Puerto Ricopurposes, it could be required to withhold federaltaxes if so instructed by the Internal Revenue Service.

WITHHOLDING TABLES

The Withholding Tables on the following pages,consider the changes introduced to the System ofWithholding of Income Tax at Source on Wages bythe Code.

Appendix 1 contains the table to determine thewithholding exemption.

Appendix 2 contains the table to determine the amountthat will be deducted from total wages with respect tothe special deduction for certain individuals.

Appendix 3 contains the tables to determine theamount of the tax that will be deducted and withheldfrom the total wages.

Appendix 4 contains the table to determine theamount of the tax that will be deducted and withheldfrom total wages when the employer elects to usethe alternative method under Article 1062.01(d)-1(b)(2) of the Regulations.

THESE TABLES SHALL BE APPLICABLE WITHRESPECT TO WAGES PAID AFTER DECEMBER31, 2013 AND BEFORE JANUARY 1, 2015.

The following are some examples to ilustrate theapplication of the withholding tables:

Example 1: “A” is a single person who does not makecontributions from his salary to a governmentalpension or retirement system (except for SocialSecurity), and claims all of the personal exemptionand the allowance for deductions. “A” is a graphicartist and receives a monthly salary of $2,200. Heestimates that, for this year, he will be able to claim$4,500 of mortgage interest, and indicates so on theWithholding Exemption Certificate (Form 499 R-4.1).

The total tax to be withheld on the monthly $2,200will be $46.20, determined as follows:Total Wages ……………..........……....….. $2,200.00

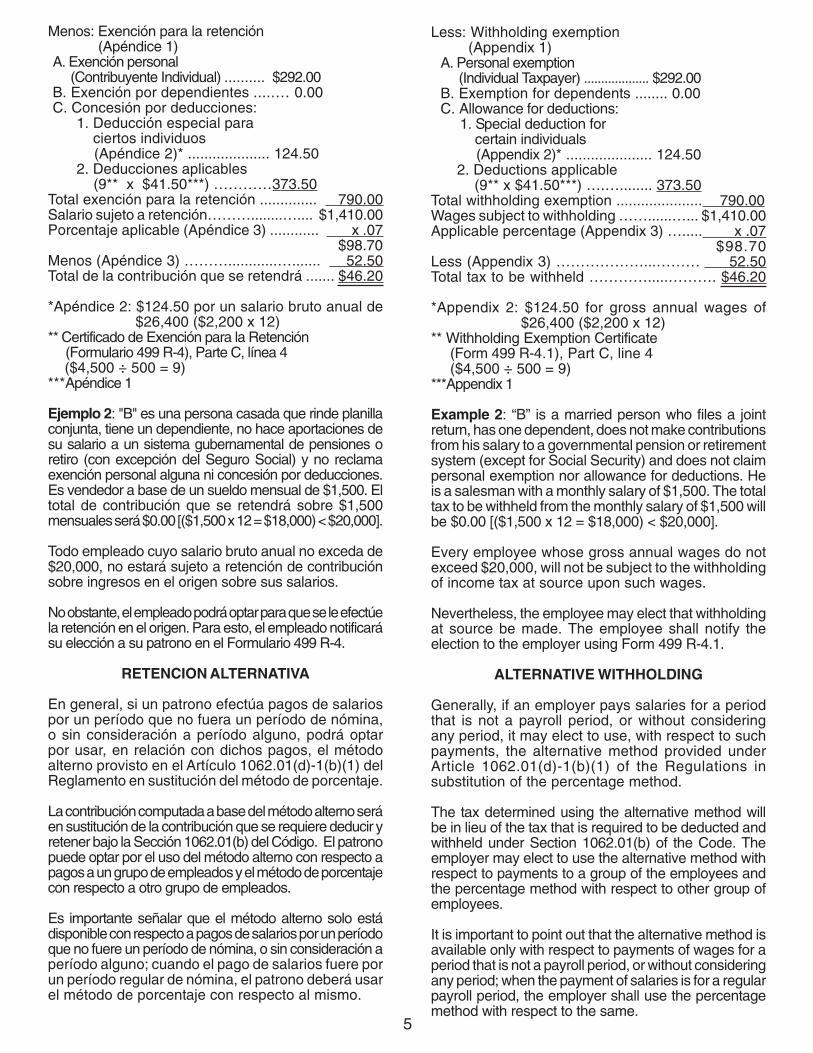

5

Menos: Exención para la retención (Apéndice 1)A. Exención personal (Contribuyente Individual) .......... $292.00B. Exención por dependientes .....… 0.00C. Concesión por deducciones:

1. Deducción especial para ciertos individuos (Apéndice 2)* .................... 124.502. Deducciones aplicables (9** x $41.50***) …………373.50

Total exención para la retención .............. 790.00Salario sujeto a retención………........….... $1,410.00Porcentaje aplicable (Apéndice 3) ............ x .07 $98.70Menos (Apéndice 3) ………............…....... 52.50Total de la contribución que se retendrá ....... $46.20

*Apéndice 2: $124.50 por un salario bruto anual de $26,400 ($2,200 x 12)** Certificado de Exención para la Retención (Formulario 499 R-4), Parte C, línea 4 ($4,500 ÷ 500 = 9)***Apéndice 1

Ejemplo 2: "B" es una persona casada que rinde planillaconjunta, tiene un dependiente, no hace aportaciones desu salario a un sistema gubernamental de pensiones oretiro (con excepción del Seguro Social) y no reclamaexención personal alguna ni concesión por deducciones.Es vendedor a base de un sueldo mensual de $1,500. Eltotal de contribución que se retendrá sobre $1,500mensuales será $0.00 [($1,500 x 12 = $18,000) < $20,000].

Todo empleado cuyo salario bruto anual no exceda de$20,000, no estará sujeto a retención de contribuciónsobre ingresos en el origen sobre sus salarios.

No obstante, el empleado podrá optar para que se le efectúela retención en el origen. Para esto, el empleado notificarásu elección a su patrono en el Formulario 499 R-4.

RETENCION ALTERNATIVA

En general, si un patrono efectúa pagos de salariospor un período que no fuera un período de nómina,o sin consideración a período alguno, podrá optarpor usar, en relación con dichos pagos, el métodoalterno provisto en el Artículo 1062.01(d)-1(b)(1) delReglamento en sustitución del método de porcentaje.

La contribución computada a base del método alterno seráen sustitución de la contribución que se requiere deducir yretener bajo la Sección 1062.01(b) del Código. El patronopuede optar por el uso del método alterno con respecto apagos a un grupo de empleados y el método de porcentajecon respecto a otro grupo de empleados.

Es importante señalar que el método alterno solo estádisponible con respecto a pagos de salarios por un períodoque no fuere un período de nómina, o sin consideración aperíodo alguno; cuando el pago de salarios fuere porun período regular de nómina, el patrono deberá usarel método de porcentaje con respecto al mismo.

Less: Withholding exemption (Appendix 1)

A. Personal exemption (Individual Taxpayer) ................... $292.00B. Exemption for dependents ........ 0.00C. Allowance for deductions: 1. Special deduction for certain individuals (Appendix 2)* ..................... 124.50 2. Deductions applicable (9** x $41.50***) ….…........ 373.50

Total withholding exemption ..................... 790.00Wages subject to withholding ……......…... $1,410.00Applicable percentage (Appendix 3) …..... x .07 $98.70Less (Appendix 3) ………………...……… 52.50Total tax to be withheld ………….....………. $46.20

*Appendix 2: $124.50 for gross annual wages of $26,400 ($2,200 x 12)

** Withholding Exemption Certificate(Form 499 R-4.1), Part C, line 4($4,500 ÷ 500 = 9)

***Appendix 1

Example 2: “B” is a married person who files a jointreturn, has one dependent, does not make contributionsfrom his salary to a governmental pension or retirementsystem (except for Social Security) and does not claimpersonal exemption nor allowance for deductions. Heis a salesman with a monthly salary of $1,500. The totaltax to be withheld from the monthly salary of $1,500 willbe $0.00 [($1,500 x 12 = $18,000) < $20,000].

Every employee whose gross annual wages do notexceed $20,000, will not be subject to the withholdingof income tax at source upon such wages.

Nevertheless, the employee may elect that withholdingat source be made. The employee shall notify theelection to the employer using Form 499 R-4.1.

ALTERNATIVE WITHHOLDING

Generally, if an employer pays salaries for a periodthat is not a payroll period, or without consideringany period, it may elect to use, with respect to suchpayments, the alternative method provided underArticle 1062.01(d)-1(b)(1) of the Regulations insubstitution of the percentage method.

The tax determined using the alternative method willbe in lieu of the tax that is required to be deducted andwithheld under Section 1062.01(b) of the Code. Theemployer may elect to use the alternative method withrespect to payments to a group of the employees andthe percentage method with respect to other group ofemployees.

It is important to point out that the alternative method isavailable only with respect to payments of wages for aperiod that is not a payroll period, or without consideringany period; when the payment of salaries is for a regularpayroll period, the employer shall use the percentagemethod with respect to the same.

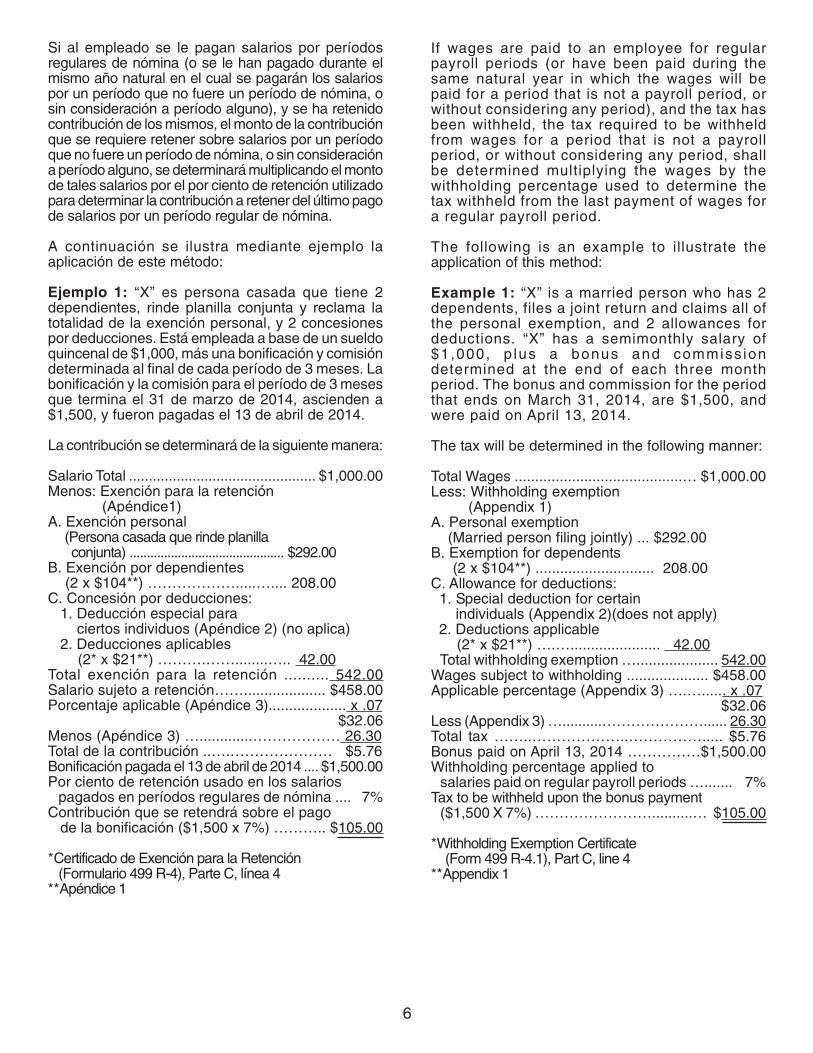

Si al empleado se le pagan salarios por períodosregulares de nómina (o se le han pagado durante elmismo año natural en el cual se pagarán los salariospor un período que no fuere un período de nómina, osin consideración a período alguno), y se ha retenidocontribución de los mismos, el monto de la contribuciónque se requiere retener sobre salarios por un períodoque no fuere un período de nómina, o sin consideracióna período alguno, se determinará multiplicando el montode tales salarios por el por ciento de retención utilizadopara determinar la contribución a retener del último pagode salarios por un período regular de nómina.

A continuación se ilustra mediante ejemplo laaplicación de este método:

Ejemplo 1: “X” es persona casada que tiene 2dependientes, rinde planilla conjunta y reclama latotalidad de la exención personal, y 2 concesionespor deducciones. Está empleada a base de un sueldoquincenal de $1,000, más una bonificación y comisióndeterminada al final de cada período de 3 meses. Labonificación y la comisión para el período de 3 mesesque termina el 31 de marzo de 2014, ascienden a$1,500, y fueron pagadas el 13 de abril de 2014.

La contribución se determinará de la siguiente manera:

Salario Total ............................................... $1,000.00Menos: Exención para la retención (Apéndice1)A. Exención personal (Persona casada que rinde planilla conjunta) ............................................. $292.00B. Exención por dependientes (2 x $104**) ……………….....….... 208.00C. Concesión por deducciones: 1. Deducción especial para ciertos individuos (Apéndice 2) (no aplica) 2. Deducciones aplicables (2* x $21**) ……….……........….. 42.00Total exención para la retención .......... 542.00Salario sujeto a retención…….................... $458.00Porcentaje aplicable (Apéndice 3)................... x .07 $32.06Menos (Apéndice 3) ….............……………… 26.30Total de la contribución ..….………………… $5.76Bonificación pagada el 13 de abril de 2014 .... $1,500.00Por ciento de retención usado en los salarios pagados en períodos regulares de nómina .... 7%Contribución que se retendrá sobre el pago de la bonificación ($1,500 x 7%) ……….. $105.00

*Certificado de Exención para la Retención (Formulario 499 R-4), Parte C, línea 4**Apéndice 1

If wages are paid to an employee for regularpayroll periods (or have been paid during thesame natural year in which the wages will bepaid for a period that is not a payroll period, orwithout considering any period), and the tax hasbeen withheld, the tax required to be withheldfrom wages for a period that is not a payrollperiod, or without considering any period, shallbe determined multiplying the wages by thewithholding percentage used to determine thetax withheld from the last payment of wages fora regular payroll period.

The following is an example to illustrate theapplication of this method:

Example 1: “X” is a married person who has 2dependents, files a joint return and claims all ofthe personal exemption, and 2 allowances fordeductions. “X” has a semimonthly salary of$1,000, p lus a bonus and commiss iondetermined at the end of each three monthperiod. The bonus and commission for the periodthat ends on March 31, 2014, are $1,500, andwere paid on April 13, 2014.

The tax will be determined in the following manner:

Total Wages .........................................… $1,000.00Less: Withholding exemption (Appendix 1)A. Personal exemption (Married person filing jointly) ... $292.00B. Exemption for dependents (2 x $104**) ............................. 208.00C. Allowance for deductions: 1. Special deduction for certain individuals (Appendix 2)(does not apply) 2. Deductions applicable (2* x $21**) ….…...................... 42.00 Total withholding exemption ….................... 542.00Wages subject to withholding .................... $458.00Applicable percentage (Appendix 3) ….…...... x .07 $32.06Less (Appendix 3) …..........…………………...... 26.30Total tax ……..………………..……………..... $5.76Bonus paid on April 13, 2014 ……………$1,500.00Withholding percentage applied to salaries paid on regular payroll periods …....... 7%Tax to be withheld upon the bonus payment ($1,500 X 7%) ……………………..........… $105.00

*Withholding Exemption Certificate (Form 499 R-4.1), Part C, line 4**Appendix 1

6

7

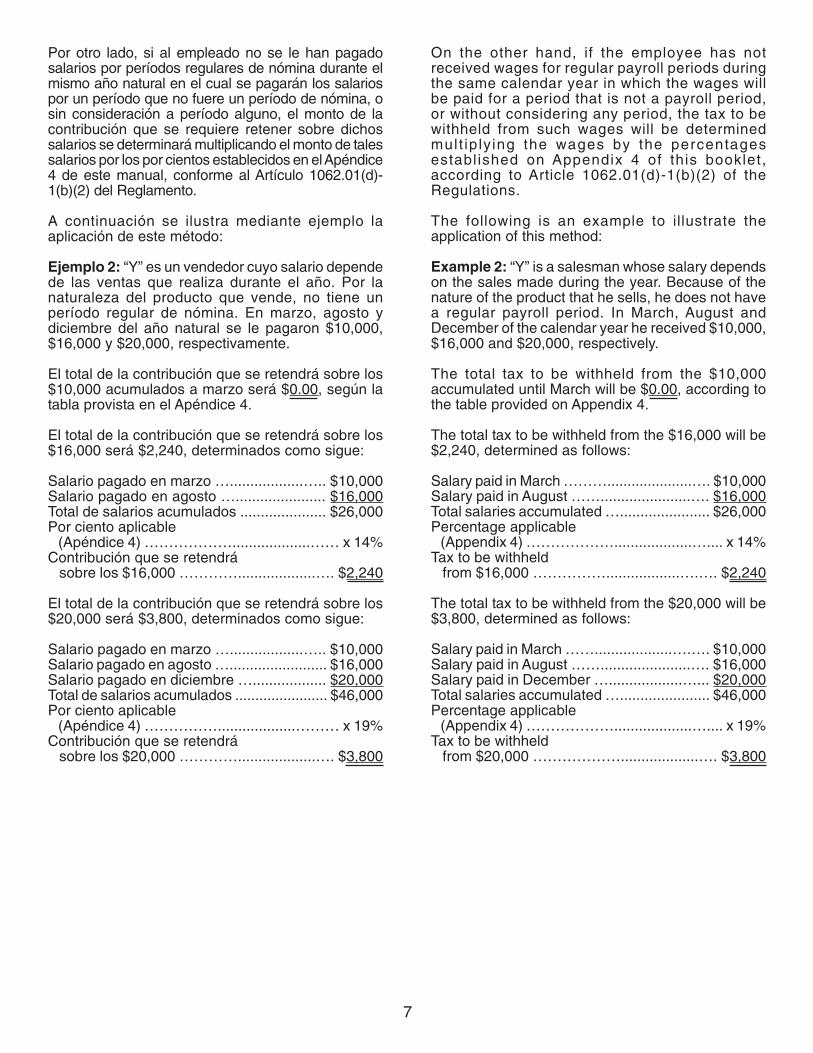

Por otro lado, si al empleado no se le han pagadosalarios por períodos regulares de nómina durante elmismo año natural en el cual se pagarán los salariospor un período que no fuere un período de nómina, osin consideración a período alguno, el monto de lacontribución que se requiere retener sobre dichossalarios se determinará multiplicando el monto de talessalarios por los por cientos establecidos en el Apéndice4 de este manual, conforme al Artículo 1062.01(d)-1(b)(2) del Reglamento.

A continuación se ilustra mediante ejemplo laaplicación de este método:

Ejemplo 2: “Y” es un vendedor cuyo salario dependede las ventas que realiza durante el año. Por lanaturaleza del producto que vende, no tiene unperíodo regular de nómina. En marzo, agosto ydiciembre del año natural se le pagaron $10,000,$16,000 y $20,000, respectivamente.

El total de la contribución que se retendrá sobre los$10,000 acumulados a marzo será $0.00, según latabla provista en el Apéndice 4.

El total de la contribución que se retendrá sobre los$16,000 será $2,240, determinados como sigue:

Salario pagado en marzo …..................….. $10,000Salario pagado en agosto …...................... $16,000Total de salarios acumulados ..................... $26,000Por ciento aplicable (Apéndice 4) ………………...................…… x 14%Contribución que se retendrá sobre los $16,000 …………...................…. $2,240

El total de la contribución que se retendrá sobre los$20,000 será $3,800, determinados como sigue:

Salario pagado en marzo …..................….. $10,000Salario pagado en agosto …........................ $16,000Salario pagado en diciembre ….................. $20,000Total de salarios acumulados ....................... $46,000Por ciento aplicable (Apéndice 4) ……………...................……… x 19%Contribución que se retendrá sobre los $20,000 …………...................…. $3,800

On the other hand, if the employee has notreceived wages for regular payroll periods duringthe same calendar year in which the wages willbe paid for a period that is not a payroll period,or without considering any period, the tax to bewithheld from such wages will be determinedmult ip ly ing the wages by the percentagesestabl ished on Appendix 4 of this booklet,according to Article 1062.01(d)-1(b)(2) of theRegulations.

The following is an example to illustrate theapplication of this method:

Example 2: “Y” is a salesman whose salary dependson the sales made during the year. Because of thenature of the product that he sells, he does not havea regular payroll period. In March, August andDecember of the calendar year he received $10,000,$16,000 and $20,000, respectively.

The total tax to be withheld from the $10,000accumulated until March will be $0.00, according tothe table provided on Appendix 4.

The total tax to be withheld from the $16,000 will be$2,240, determined as follows:

Salary paid in March ……….....................…. $10,000Salary paid in August ……......................…. $16,000Total salaries accumulated …...................... $26,000Percentage applicable (Appendix 4) ………………...................….... x 14%Tax to be withheld from $16,000 ……………..................….…. $2,240

The total tax to be withheld from the $20,000 will be$3,800, determined as follows:

Salary paid in March ……...................….…. $10,000Salary paid in August ……......................…. $16,000Salary paid in December …..................…... $20,000Total salaries accumulated …...................... $46,000Percentage applicable (Appendix 4) ………………...................….... x 19%Tax to be withheld from $20,000 ………………...................…. $3,800

RETENCION EN EL ORIGEN DE LA CONTRIBUCION SOBRE INGRESOSCUANDO SE PAGAN SALARIOS SUPLEMENTARIOS

WITHHOLDING OF INCOME TAX AT SOURCEWHEN SUPPLEMENTARY SALARIES ARE PAID

8

A continuación se describe el procedimientoestablecido por el Departamento de Hacienda para ladeducción y retención en el origen de la contribución sobreingresos cuando se pagan salarios suplementarios.

DEFINICION DEL TERMINOSALARIOS SUPLEMENTARIOS

La remuneración de un empleado puede consistirde salarios pagados por un período de nóminaordinario y de salarios suplementarios pagados porel mismo período, por un período diferente o sinconsideración a período alguno. El término salariossuplementarios se aplica a la remuneración adicionalque se paga como bonificaciones, comisiones,tiempo extra u otros pagos similares consideradoscomo salarios, y por tanto, sujetos a retención.

PROCEDIMIENTO PARA DETERMINAR LARETENCION

El pago de salarios suplementarios puede o nocoincidir con el pago ordinario correspondiente alperíodo de nómina. Además, a veces se pagan salariossuplementarios por dos o más períodos de nóminaordinarios consecutivos. El procedimiento paradeterminar la retención sobre el pago de salariossuplementarios dependerá de:

1. si el pago de éstos coincide o no con el pagoordinario de salarios, y

2. del número de períodos de nómina ordinarioscomprendidos en el período por el cual sepagan los salarios suplementarios.

Es importante señalar que al determinar la retenciónen el origen de la contribución sobre ingresos en elcaso de salarios suplementarios, no se considerarála concesión por la deducción especial para ciertosindividuos provista en el Apéndice 2 de este manual.Esto es debido a que la deducción especial dependedel salario bruto anual del empleado, el cual no sepuede determinar con exactitud en el caso de salariossuplementarios.

A continuación se ilustran en detalle, medianteejemplos, las distintas situaciones que podríanpresentarse en casos de pagos de salariossuplementarios.

Hereinafter, the procedure established by theDepartment of the Treasury for the deductionand withholding of income tax at source whensupplementary salaries are paid is described.

DEFINITION OF THE TERMSUPPLEMENTARY SALARIES

The remuneration of an employee may consistof wages paid for an ordinary payroll period andof supplementary salaries paid for the same or adifferent period, or without considering any period.The term supplementary salaries applies to theadditional remuneration that is paid such asbonuses, commissions, overtime or other similarpayments considered as salaries, and therefore,subject to withholding.

PROCEDURE TO DETERMINE THEWITHHOLDING

The payment of supplementary salaries maycoincide or not with the corresponding payroll periodordinary payment. Furthermore, sometimessupplementary salaries are paid for two or moreconsecutive ordinary payroll periods. The procedureto determine the income tax to be withheld upon thesupplementary salaries will depend on:

1. whether their payment coincides or not withthe salaries ordinary payment, and

2. the number of ordinary payroll periodscomprised in the period for which thesupplementary salaries are paid.

It is important to point out that to determine thewithholding of income tax at source in the case ofsupplementary salaries, the allowance for thespecial deduction for certain individuals providedon Appendix 2 of this booklet will not be considered.This is because the special deduction depends onthe gross annual salary of the employee, whichcannot be determined accurately in the case ofsupplementary salaries.

Hereinafter, the different situations that mayocurr in cases of payment of supplementarysalaries, are illustrated in detail and by means ofexamples.

9

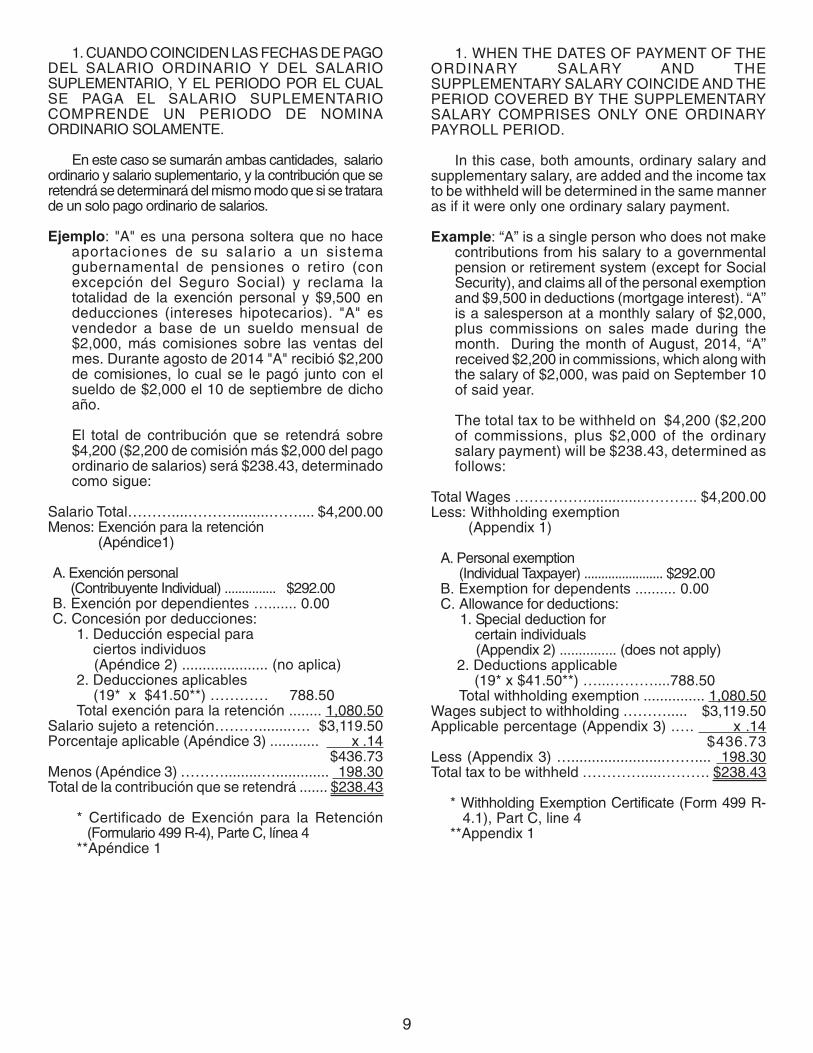

1. CUANDO COINCIDEN LAS FECHAS DE PAGODEL SALARIO ORDINARIO Y DEL SALARIOSUPLEMENTARIO, Y EL PERIODO POR EL CUALSE PAGA EL SALARIO SUPLEMENTARIOCOMPRENDE UN PERIODO DE NOMINAORDINARIO SOLAMENTE.

En este caso se sumarán ambas cantidades, salarioordinario y salario suplementario, y la contribución que seretendrá se determinará del mismo modo que si se tratarade un solo pago ordinario de salarios.

Ejemplo: "A" es una persona soltera que no haceaportaciones de su salario a un sistemagubernamental de pensiones o retiro (conexcepción del Seguro Social) y reclama latotalidad de la exención personal y $9,500 endeducciones (intereses hipotecarios). "A" esvendedor a base de un sueldo mensual de$2,000, más comisiones sobre las ventas delmes. Durante agosto de 2014 "A" recibió $2,200de comisiones, lo cual se le pagó junto con elsueldo de $2,000 el 10 de septiembre de dichoaño.

El total de contribución que se retendrá sobre$4,200 ($2,200 de comisión más $2,000 del pagoordinario de salarios) será $238.43, determinadocomo sigue:

Salario Total………....……….........…….... $4,200.00Menos: Exención para la retención (Apéndice1)

A. Exención personal (Contribuyente Individual) ............... $292.00B. Exención por dependientes …....... 0.00C. Concesión por deducciones:

1. Deducción especial para ciertos individuos (Apéndice 2) ..................... (no aplica)2. Deducciones aplicables (19* x $41.50**) ………… 788.50Total exención para la retención ........ 1,080.50

Salario sujeto a retención………........…. $3,119.50Porcentaje aplicable (Apéndice 3) ............ x .14 $436.73Menos (Apéndice 3) ……….........…............. 198.30Total de la contribución que se retendrá ....... $238.43

* Certificado de Exención para la Retención (Formulario 499 R-4), Parte C, línea 4**Apéndice 1

1. WHEN THE DATES OF PAYMENT OF THEORDINARY SALARY AND THESUPPLEMENTARY SALARY COINCIDE AND THEPERIOD COVERED BY THE SUPPLEMENTARYSALARY COMPRISES ONLY ONE ORDINARYPAYROLL PERIOD.

In this case, both amounts, ordinary salary andsupplementary salary, are added and the income taxto be withheld will be determined in the same manneras if it were only one ordinary salary payment.

Example: “A” is a single person who does not makecontributions from his salary to a governmentalpension or retirement system (except for SocialSecurity), and claims all of the personal exemptionand $9,500 in deductions (mortgage interest). “A”is a salesperson at a monthly salary of $2,000,plus commissions on sales made during themonth. During the month of August, 2014, “A”received $2,200 in commissions, which along withthe salary of $2,000, was paid on September 10of said year.

The total tax to be withheld on $4,200 ($2,200of commissions, plus $2,000 of the ordinarysalary payment) will be $238.43, determined asfollows:

Total Wages ……………..............……….. $4,200.00Less: Withholding exemption (Appendix 1)

A. Personal exemption (Individual Taxpayer) ....................... $292.00B. Exemption for dependents .......... 0.00C. Allowance for deductions: 1. Special deduction for certain individuals (Appendix 2) ............... (does not apply) 2. Deductions applicable (19* x $41.50**) …...………....788.50

Total withholding exemption ............... 1,080.50Wages subject to withholding ………..... $3,119.50Applicable percentage (Appendix 3) .…. x .14 $436.73Less (Appendix 3) ….......................…….... 198.30Total tax to be withheld ………….....………. $238.43

* Withholding Exemption Certificate (Form 499 R- 4.1), Part C, line 4**Appendix 1

10

2. CUANDO NO COINCIDEN LAS FECHAS DEPAGO DEL SALARIO ORDINARIO Y ELSUPLEMENTARIO Y EL PERIODO POR EL CUALSE PAGA EL SALARIO SUPLEMENTARIOCOMPRENDE UN PERIODO DE NOMINAORDINARIO SOLAMENTE.

Los salarios suplementarios se sumarán a los salariospagados por el período de nómina inmediatamenteprecedente dentro del mismo año natural o por el períodode nómina corriente. La cantidad de contribución que seretendrá se determinará como si el agregado de los salariossuplementarios y los salarios ordinarios constituyeran unsolo pago de salarios para el período de nómina regular.

Ejemplo: "B" es un contribuyente individual que tienetres dependientes, no hace aportaciones de susalario a un sistema gubernamental de pensioneso retiro (con excepción del Seguro Social), reclamala totalidad de la exención personal y no tienededucciones. "B" recibe un salario semanal de$550.00 pagadero el sábado de cada semana. Elmiércoles de determinada semana a "B" se lepagaron $90.00 por tiempo extra de la semanaanterior.

La contribución se determinará de la siguiente manera:

Salario Total ($550 + $90) ……………....... $640.00Menos: Exención para la retención (Apéndice1)A. Exención personal (Contribuyente Individual) ................... $67.00B. Exención por dependientes (3 x $48*) ..................................... 144.00C. Concesión por deducciones:

1. Deducción especial para ciertos individuos (Apéndice 2) .......................... (no aplica)2. Deducciones aplicables ............. 0.00Total exención para la retención .......... 211.00

Salario sujeto a retención……………...…... $429.00Porcentaje aplicable (Apéndice 3) ........... x .07 $30.03Menos (Apéndice 3) ….…............................. 12.10Total de la contribución ……….……….......... $17.93Contribución previamente retenida …............ 11.63Contribución que se retendrá sobre pago por tiempo extra …...............…...….......… $6.30

*Apéndice 1

2. WHEN THE DATES OF PAYMENT OF THEORDINARY AND THE SUPPLEMENTARYSALARIES DO NOT COINCIDE AND THE PERIODFOR WHICH THE SUPPLEMENTARY SALARY ISPAID COMPRISES ONLY ONE ORDINARYPAYROLL PERIOD.

The supplementary salaries will be added to thewages paid during the immediately preceding payrollperiod of the same calendar year or during the currentpayroll period. The amount of tax to be withheld willbe determined as if the sum of the supplementarysalaries and the ordinary salaries constitute only onesalaries payment for the ordinary payroll period.

Example: “B” is an individual taxpayer, who hasthree dependents, does not make contributionsfrom his salary to a governmental pension orretirement system (except for Social Security),claims all of the personal exemption and nodeductions. “B” receives a weekly salary of$550.00 payable every Saturday. On a givenWednesday, $90.00 of the preceding weekovertime was paid to “B”.

The tax will be determined in the following mannner:

Total Wages ($550 + $90) ……..……….…. $640.00Less: Withholding exemption (Appendix 1)

A. Personal exemption (Individual Taxpayer) ...................... $67.00B. Exemption for dependents (3 x $48*) ................................... 144.00C. Allowance for deductions:

1. Special deduction for certain individuals (Appendix 2) ....................... (does not apply) 2. Deductions applicable ............. 0.00 Total withholding exemption …..........… 211.00Wages subject to withholding ................... $429.00Applicable percentage (Appendix 3)….......... x .07 $30.03Less (Appendix 3) ……………….................… 12.10Total tax …………..………………..…......……. $17.93Tax previously withheld ……………….......... 11.63Tax to be withheld from overtime payment ....................................... $6.30

*Appendix 1

11

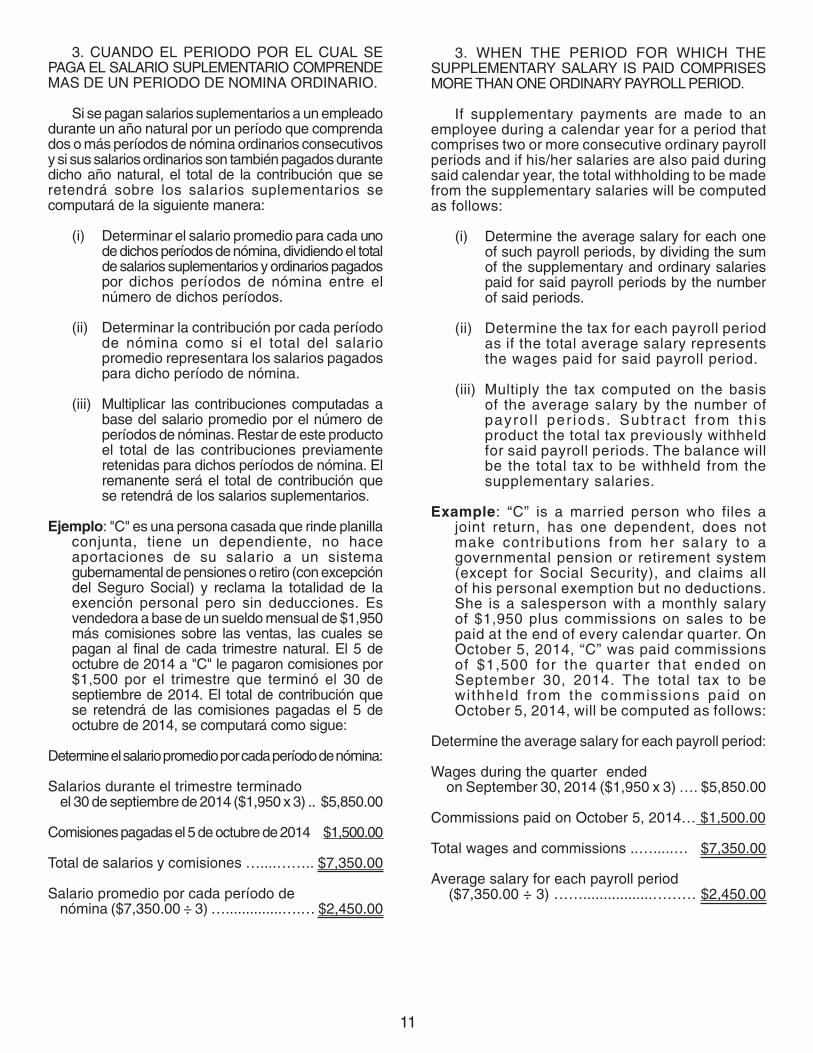

3. CUANDO EL PERIODO POR EL CUAL SEPAGA EL SALARIO SUPLEMENTARIO COMPRENDEMAS DE UN PERIODO DE NOMINA ORDINARIO.

Si se pagan salarios suplementarios a un empleadodurante un año natural por un período que comprendados o más períodos de nómina ordinarios consecutivosy si sus salarios ordinarios son también pagados durantedicho año natural, el total de la contribución que seretendrá sobre los salarios suplementarios secomputará de la siguiente manera:

(i) Determinar el salario promedio para cada unode dichos períodos de nómina, dividiendo el totalde salarios suplementarios y ordinarios pagadospor dichos períodos de nómina entre elnúmero de dichos períodos.

(ii) Determinar la contribución por cada períodode nómina como si el total del salariopromedio representara los salarios pagadospara dicho período de nómina.

(iii) Multiplicar las contribuciones computadas abase del salario promedio por el número deperíodos de nóminas. Restar de este productoel total de las contribuciones previamenteretenidas para dichos períodos de nómina. Elremanente será el total de contribución quese retendrá de los salarios suplementarios.

Ejemplo: "C" es una persona casada que rinde planillaconjunta, tiene un dependiente, no haceaportaciones de su salario a un sistemagubernamental de pensiones o retiro (con excepcióndel Seguro Social) y reclama la totalidad de laexención personal pero sin deducciones. Esvendedora a base de un sueldo mensual de $1,950más comisiones sobre las ventas, las cuales sepagan al final de cada trimestre natural. El 5 deoctubre de 2014 a "C" le pagaron comisiones por$1,500 por el trimestre que terminó el 30 deseptiembre de 2014. El total de contribución quese retendrá de las comisiones pagadas el 5 deoctubre de 2014, se computará como sigue:

Determine el salario promedio por cada período de nómina:

Salarios durante el trimestre terminado el 30 de septiembre de 2014 ($1,950 x 3) .. $5,850.00

Comisiones pagadas el 5 de octubre de 2014 $1,500.00

Total de salarios y comisiones …....…….. $7,350.00

Salario promedio por cada período de nómina ($7,350.00 ÷ 3) …..............….… $2,450.00

3. WHEN THE PERIOD FOR WHICH THESUPPLEMENTARY SALARY IS PAID COMPRISESMORE THAN ONE ORDINARY PAYROLL PERIOD.

If supplementary payments are made to anemployee during a calendar year for a period thatcomprises two or more consecutive ordinary payrollperiods and if his/her salaries are also paid duringsaid calendar year, the total withholding to be madefrom the supplementary salaries will be computedas follows:

(i) Determine the average salary for each oneof such payroll periods, by dividing the sumof the supplementary and ordinary salariespaid for said payroll periods by the numberof said periods.

(ii) Determine the tax for each payroll periodas if the total average salary representsthe wages paid for said payroll period.

(iii) Multiply the tax computed on the basisof the average salary by the number ofpayro l l per iods. Subtract f rom th isproduct the total tax previously withheldfor said payroll periods. The balance willbe the total tax to be withheld from thesupplementary salaries.

Example: “C” is a married person who files ajoint return, has one dependent, does notmake contributions from her salary to agovernmental pension or retirement system(except for Social Security), and claims allof his personal exemption but no deductions.She is a salesperson with a monthly salaryof $1,950 plus commissions on sales to bepaid at the end of every calendar quarter. OnOctober 5, 2014, “C” was paid commissionsof $1,500 for the quarter that ended onSeptember 30, 2014. The total tax to bewithheld from the commissions paid onOctober 5, 2014, will be computed as follows:

Determine the average salary for each payroll period:

Wages during the quarter ended on September 30, 2014 ($1,950 x 3) …. $5,850.00

Commissions paid on October 5, 2014… $1,500.00

Total wages and commissions ..….....… $7,350.00

Average salary for each payroll period ($7,350.00 ÷ 3) …….................……… $2,450.00

12

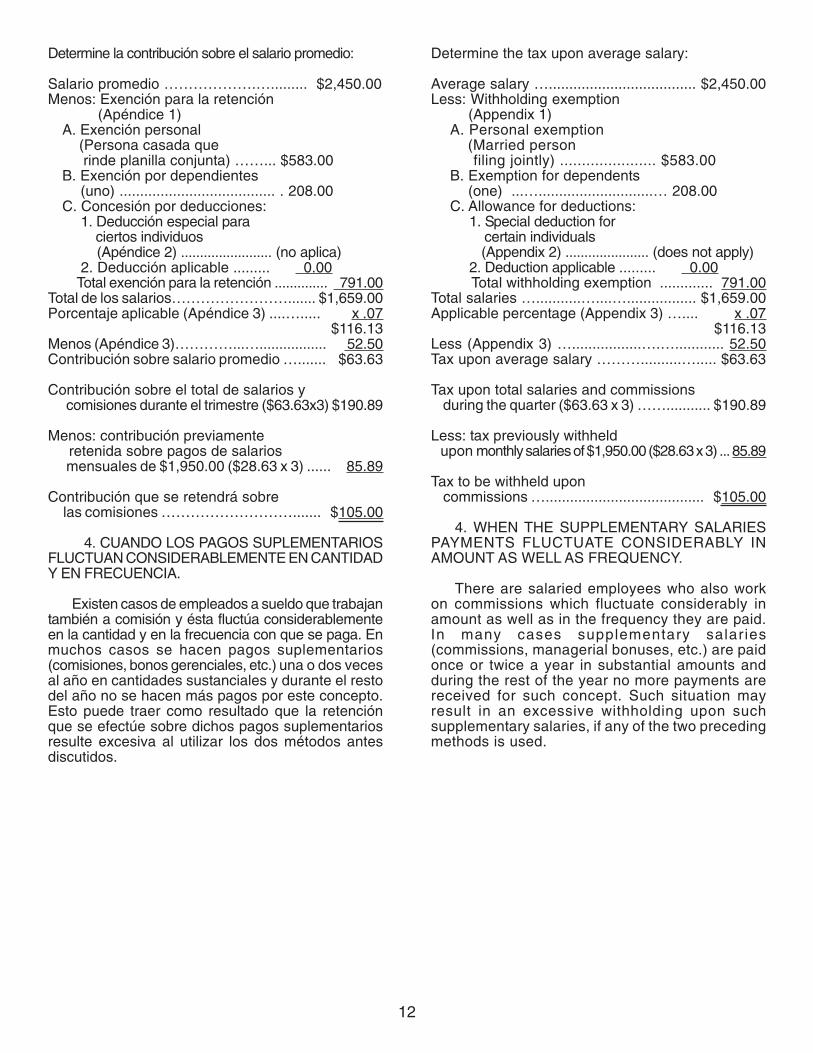

Determine la contribución sobre el salario promedio:

Salario promedio ……………….…......... $2,450.00Menos: Exención para la retención (Apéndice 1)

A. Exención personal (Persona casada que rinde planilla conjunta) ……... $583.00B. Exención por dependientes (uno) ...................................... . 208.00C. Concesión por deducciones:

1. Deducción especial para ciertos individuos (Apéndice 2) ........................ (no aplica) 2. Deducción aplicable ......... 0.00Total exención para la retención .............. 791.00

Total de los salarios……………………....... $1,659.00Porcentaje aplicable (Apéndice 3) ....…..... x .07 $116.13Menos (Apéndice 3)…………...…................. 52.50Contribución sobre salario promedio …....... $63.63

Contribución sobre el total de salarios y comisiones durante el trimestre ($63.63x3) $190.89

Menos: contribución previamente retenida sobre pagos de salarios mensuales de $1,950.00 ($28.63 x 3) ...... 85.89

Contribución que se retendrá sobre las comisiones ………………………....... $105.00

4. CUANDO LOS PAGOS SUPLEMENTARIOSFLUCTUAN CONSIDERABLEMENTE EN CANTIDADY EN FRECUENCIA.

Existen casos de empleados a sueldo que trabajantambién a comisión y ésta fluctúa considerablementeen la cantidad y en la frecuencia con que se paga. Enmuchos casos se hacen pagos suplementarios(comisiones, bonos gerenciales, etc.) una o dos vecesal año en cantidades sustanciales y durante el restodel año no se hacen más pagos por este concepto.Esto puede traer como resultado que la retenciónque se efectúe sobre dichos pagos suplementariosresulte excesiva al utilizar los dos métodos antesdiscutidos.

Determine the tax upon average salary:

Average salary ….................................... $2,450.00Less: Withholding exemption (Appendix 1)

A. Personal exemption (Married person filing jointly) ...................... $583.00B. Exemption for dependents (one) ...…............................… 208.00C. Allowance for deductions:

1. Special deduction for certain individuals (Appendix 2) ...................... (does not apply)2. Deduction applicable ......... 0.00

Total withholding exemption ............. 791.00Total salaries …...........…....…................. $1,659.00Applicable percentage (Appendix 3) ….... x .07 $116.13Less (Appendix 3) ….................….…............ 52.50Tax upon average salary ………..........…..... $63.63

Tax upon total salaries and commissions during the quarter ($63.63 x 3) ……........... $190.89

Less: tax previously withheld upon monthly salaries of $1,950.00 ($28.63 x 3) ... 85.89

Tax to be withheld upon commissions …....................................... $105.00

4. WHEN THE SUPPLEMENTARY SALARIESPAYMENTS FLUCTUATE CONSIDERABLY INAMOUNT AS WELL AS FREQUENCY.

There are salaried employees who also workon commissions which fluctuate considerably inamount as well as in the frequency they are paid.In many cases supplementary salaries(commissions, managerial bonuses, etc.) are paidonce or twice a year in substantial amounts andduring the rest of the year no more payments arereceived for such concept. Such situation mayresult in an excessive withholding upon suchsupplementary salaries, if any of the two precedingmethods is used.

13

En dichos casos, al igual que en otros similares,el patrono podrá computar el total de la contribuciónque se retendrá sobre los salarios suplementariosde la siguiente forma:

(1) Elevar los salarios totales del empleado en cadaperíodo de nómina a base anual. Para ello, semultiplicará el salario ordinario en un período denómina regular por el número de períodos denómina que hay en un año. A este producto se lesumarán los pagos suplementarios recibidosdurante el período de nómina que se trate.

(2) Computar la contribución que se retendrá sobrelos salarios totales del empleado (elevados a baseanual del modo indicado en el renglón (1))mediante las tablas de retención aplicables acuando el período de nómina es anual.

(3) Determinar qué parte de la contribución(computada de acuerdo con el renglón (2))corresponde a los períodos de nóminatranscurridos hasta el período de nómina de quese trate. Para hacer esto, se aplicará a dichacontribución la proporción que el total de lossalarios realmente recibidos (incluyendo pagossuplementarios) durante los períodos de nóminatranscurridos guarde con los salarios totales delempleado elevados a base anual, según indicadoen el renglón (1).

(4) Restar el total de la retención efectuadaanteriormente de la contribución correspondientea los períodos de nómina transcurridos. Elresultado será la retención que se efectuará sobreel pago que se haga.

Cualquier patrono que adopte el métodoanterior, deberá seguir usando el mismo métododurante todo el año natural de que se trate.

Ejemplo: "D" es una persona casada que rinde planillaconjunta. Tiene un dependiente y reclama la totalidadde la exención personal. Es vendedor en una empresaprivada a base de un sueldo mensual de $1,800 máscomisiones sobre las ventas. Estas se le pagan juntoal salario ordinario del mes en que las devengue.Debido a la naturaleza del equipo que vende, enalgunos meses no efectúa venta alguna. Por tanto,no recibe comisiones en esos meses. Por el contrario,en algunos meses efectúa ventas considerables porlas cuales recibe comisiones cuantiosas. En marzo,junio y noviembre del año natural se le pagaroncomisiones ascendentes a $10,000, $6,000 y $8,000,respectivamente. El total de la contribución que se leretendrá se computa como sigue:

In such cases, as well as in similar ones, theemployer may compute the total tax to be withheldfrom the supplementary salaries in the followingmanner:

(1) Annualize the employee’s total wages ineach payroll period. To do so, multiplythe ordinary salary in a given payrollper iod t imes the number of payrol lperiods in a year. Add to this amount thesupp lementary payments rece ivedduring the given payroll period.

(2) Compute the tax to be withheld upon theemployee's total salaries (annualized asindicated in item (1)), using the withholdingtables applicable to an annual payrollperiod.

(3) Determine which part of the tax (computedunder item (2)) corresponds to the payrollperiods elapsed until the given payroll period.To do so, apply to said tax the ratio whichthe total salaries actually received (includingsupplementary payments) during the givenpayroll periods bears with the employee’stotal salaries on an annual basis, as indicatedin item (1).

(4) Subtract the total tax already withheldfrom the tax corresponding to the givenpayroll periods. The result shall be thetax that has to be withheld upon thepayment made.

Any employer who adopts the aforementionedmethod, shall continue using the same methodduring the whole calendar year.

Example: “D” is a married person filing jointly, has onedependent and claims all of his personal exemption.He is a salesman in a private business at a monthlysalary of $1,800 plus commissions upon sales. Thecommissions are paid to him along with the ordinarysalary of the month in which they are earned. Dueto the nature of the equipment that “D” sells, thereare months in which no sales are made. Therefore,he does not receive commissions during thosemonths. On the contrary, in other months he makesconsiderable sales, and consequently, thecommissions are substantial. In March, June andNovember of the calendar year he receivedcommissions payments amounting to $10,000,$6,000 and $8,000, respectively. The total tax tobe withheld is computed as follows:

14

1 2 3 4 5 6 7 8 9

Período deNómina

PayrollPeriod

SalarioOrdinario

Anual

AnnualOrdinarySalary

TotalComisionesRecibidas

TotalCommissions

Received

SalariosTotales

Elevados aBase Anual(Col. 1 más

Col. 2)

TotalSalaries on

Annual Basis(Col.1 plus

Col. 2)

Exención para laRetención a

Base de Períodode Nómina

Anual

WithholdingExemption

based on anAnnual Payroll

Period

Total de losSalarios(Col. 3menosCol. 4)

Total Salaries(Col. 3 minus

Col. 4)

Contribución quese retendrá

sobre el total delos Salarios de

la Col. 5

Tax to bewithheld upon

the totalSalaries of

Col. 5

ContribuciónCorrespondiente a Períodos de

NóminaTranscurridos

TaxCorrespondingto the ElapsedPayroll Periods

RetenciónEfectuada

Anteriormente

TaxPreviouslyWithheld

Retención delPeríodo de

Nómina(Col. 7 menos

Col. 8)

Withholding for thePayroll Period(Col. 7 minus

Col. 8)

1

2

3

4

5

6

7

8

9

10

11

12

$21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

21,600.00

-

-

$10,000.00

-

-

$16,000.00

-

-

-

-

$24,000.00

-

$21,600.00

21,600.00

31,600.00

31,600.00

31,600.00

37,600.00

37,600.00

37,600.00

37,600.00

37,600.00

45,600.00

45,600.00

$14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

14,000.00

$7,600.00

7,600.00

17,600.00

17,600.00

17,600.00

23,600.00

23,600.00

23,600.00

23,600.00

23,600.00

31,600.00

31,600.00

$0.00

0.00

602.00

602.00

602.00

1,022.00

1,022.00

1,022.00

1,022.00

1,022.00

2,044.00

2,044.00

$0.00

0.00

294.98

325.08

361.20

725.62

776.72

827.82

878.92

919.80

1,962.24

2,044.00

$0.00

0.00

0.00

294.98

325.08

361.20

725.62

776.72

827.82

878.92

919.80

1,962.24

$0.00

0.00

294.98

30.10

36.12

364.42

51.10

51.10

51.10

40.88

1,042.44

81.76

*( )

Asumiendo que el empleado reclama nueve concesiones por deducciones.Assuming that the employee claims nine allowances for deductions.

*( )

*( )

No obstante, el patrono podrá, a su elección, utilizarla Retención Alternativa provista en el Artículo1062.01(d)-1(b)(1) del Reglamento, previamentediscutida en el Ejemplo 1 de la página 6 de estemanual.

Notwithstanding, the employer may elect to use theAlternative Withholding provided under Article1062.01(d)-1(b)(1) of the Regulations, previousllydiscussed in Example 1, page 6 of this booklet.

5. RETENCION QUE SE EFECTUARASOBRE PAGOS POR BONO NAVIDEÑO.

El patrono determinará esta retención mediante unode los siguientes métodos:

(a) Cuando el bono navideño no exceda de $600,el patrono no retendrá contribución del bonopagado.

(b) Cuando el bono navideño exceda de $600pero no exceda de $1,500, el patrono deberáretener una contribución de 7 por ciento sobreel total del bono.

(c) Si el bono excede de $1,500, el patrono podráusar uno de los tres (3) métodos que sepresentan a continuación, para determinar laretención aplicable al bono:

Bajo el primer método, el patronodeterminará el total del sueldo recibidopor el empleado hasta la fecha máscercana a la fecha de pago del bono.Sumar el bono al sueldo. Luego secomputará la contribución que seretendrá sobre dicho agregado como siéste comprendiera un período anual. Dela contribución así determinada, se restala contribución retenida, si alguna, y elresultado será el total de contribución quedebe retener sobre el bono.

Bajo el segundo método, el patronodeterminará un porcentaje efectivo deretención para cada empleado. Esteporcentaje surgirá de la relación queguarde el total de la contribución retenidaen el período de nómina más cercano ala fecha de pago del bono sobre el totaldel sueldo del empleado en dichoperíodo. Este porcentaje se multiplicarápor el total del bono.

El tercer método es aquél establecido enel Artículo 1062.01(d)-1 del Reglamento,identificado anteriormente como métodoalterno.

5. AMOUNT OF INCOME TAX TO BEWITHHELD IN THE CASE OF CHRISTMASBONUS PAYMENT.

The employer will determine this withholding throughthe use of any of the following methods:

(a) When the Christmas bonus does not exceed$600, the employer will not withhold taxesfrom the bonus paid.

(b) When the Christmas bonus exceeds $600but does not exceed $1,500, the employermust withhold a 7% tax from the total amountof the bonus.

(c) If the bonus exceeds $1,500, the employermay use one of the following three (3)methods to determine the withholdingapplicable to the bonus:

Under the first method, the employer shalldetermine the wages received by theemployee during the year, up to the dateclosest to the bonus payment. Add thebonus payment to said wages. The taxto be withheld is computed upon saidaggregate as if it were an annual payrollperiod. From the tax so determined, thetax previously withheld, if any, issubtracted, and the result will constitutethe total tax to be withheld upon the bonuspayment.

Under the second method, the employershall determine an effective withholdingrate for each employee. This rate will bethe ratio that the total tax withheld duringthe payroll period closest to the bonuspayment bears to the total employee’ssalary in said period. Multiply this ratetimes the bonus total.

The third method is the one establishedunder Article 1062.01(d)-1, previouslyidentified as alternative method.

15

(i)

(ii)

(iii)

(i)

(ii)

(iii)

La Sección 6080.05 del Código dispone quetodo patrono obligado a deducir y retenercontribuciones sobre salarios, deberá pagar éstasal Secretario de Hacienda según se establezca enlos reglamentos promulgados en relación a laforma, el tiempo y las condiciones que regirán elpago o depósito de dichas contribuciones retenidas.

El Reglamento Núm. 5924 del 26 de febrero de 1999,promulgado al amparo de la Sección 6130 del Códigode Rentas Internas de Puerto Rico de 1994, segúnenmendado (Reglamento), establece las reglas para eldepósito de la contribución sobre ingresos retenida sobresalarios y para la determinación de la clase dedepositante. Hasta que se emitan reglamentos bajo laSección 6080.05 del Código, las disposiciones delReglamento continúan en vigor. Bajo dichasdisposiciones, los patronos vendrán obligados a efectuarsus depósitos de la contribución retenida como sigue:

Patronos cuya retención en un trimestreno haya excedido de $500.00. Estospatronos no vendrán obligados a realizar eldepósito mensual, y en su lugar, pagarán dichacontribución cuando rindan la planilla trimestral.

Patronos nuevos y patronos que hayanretenido e informado $50,000 o menosdurante el período comprendido entre el 1de julio del año antepasado (2012) y el 30de junio del año pasado (2013). Estospatronos se considerarán depositantesmensuales y depositarán sus contribuciones nomás tarde del decimoquinto (15) día del messiguiente a la retención.

Patronos que hayan retenido e informadomás de $50,000 durante el períodocomprendido entre el 1 de julio del añoantepasado (2012) y el 30 de junio del añopasado (2013). Estos patronos se considerarándepositantes bisemanales y deberán depositarlas contribuciones retenidas los miércoles oviernes, dependiendo del día en que se paguela nómina. Esto es, si el patrono paga la nóminaun miércoles, jueves o viernes, deberá realizarel depósito el miércoles siguiente. En cambio,si paga la nómina un sábado, domingo, luneso martes, realizarán el depósito el viernessiguiente.

Patronos que hayan retenido $100,000 omás en cualquier día de un período dedepósito. Estos patronos deberán realizar sudepósito no más tarde de la hora de cierre delpróximo día bancario.

Section 6080.05 of the Code provides thatevery employer required to deduct and withholdincome tax from salaries, shall pay such amountsto the Secretary of the Treasury according to theregulations regarding the form, time and conditionsgoverning the payment and deposit of suchwithheld taxes.

Regulation No. 5924 of February 26, 1999,issued under the provisions of Section 6130of the Puerto Rico Internal Revenue Code of1994, as amended (Regulations), establishesthe rules for the deposit of the income taxwi thhe ld f rom sa lar ies and for thedetermination of the type of depositor. Untilsuch time as regulations are issued underSection 6080.05 of the Code, the provisionsof the Regulations continue in full force andeffect. Under said provisions, the employerswill be required to make the deposit of the taxwithheld as follows:

Employers whose quarterly withholdingshave not exceeded $500.00. Theseemployers are not required to make the monthlydeposit; instead, they will pay said income taxwhen filing the quarterly return.

New employers and employers who havewithheld and reported $50,000 or lessduring the lookback period which beginsJuly 1 and ends June 30 of the precedingyear (2013). These employers will beconsidered monthly depositors and will deposittheir income tax not later than the fifteenth (15)day of the month following the month in whichthe withholding was made.

Employers who have withheld and reportedover $50,000 during the lookback periodwhich begins July 1 and ends June 30 ofthe preceding year (2013). These employerswill be considered semiweekly depositors andshall deposit the income tax withheld onWednesdays or Fridays, depending on the daythe payroll is paid. That is, if the employer paysthe payroll on Wednesday, Thursday or Friday,the deposit must be made the followingWednesday. However, if the payroll is paid onSaturday, Sunday, Monday or Tuesday, thedeposit must be made the following Friday.

Employers who have withheld $100,000or more in any day of a deposit period.These employers shall make the depositnot later than the closing hour of the nextbanking day.16

INSTRUCCIONES A LOS PATRONOS PARARENDIR LAS PLANILLAS Y PAGAR LA CONTRIBUCION RETENIDA

INSTRUCTIONS TO EMPLOYERS TO FILE THE RETURNSAND PAYING THE TAX WITHHELD

1.

2.

3.

4.

1.

2.

3.

4.

17

La determinación de si un patrono es depositantemensual o bisemanal se hará anualmente, abase del historial de pago de los últimos 12meses terminados el 30 de junio del año anterior(2013).

I. PLANILLA TRIMESTRAL PATRONAL DE CONTRIBUCION SOBRE INGRESOS RETENIDA (FORMULARIO 499R-1B)

Contenido de la Planilla - Esta contendrá todala información sobre la contribución sobre ingresosretenida de los salarios pagados por el patrono a susempleados durante el trimestre por el cual se rindecomo lo dispone la Sección 1062.01 del Código. Laplanilla se preparará a nombre del patrono que hacelos pagos y se firmará electrónicamente por éste, lapersona que ejerza el control del pago de salarios oserá firmada por un Especialista debidamenteregistrado y activo en el Registro Oficial deEspecialistas. Si el patrono es una corporación,firmará el presidente, principal ejecutivo u oficial contítulo análogo. Si es una sociedad, firmará el sociogestor.

En caso de que un patrono tenga un crédito decontribución retenida de trimestres anteriores, dichopatrono debe reclamar este crédito en la línea 5 delFormulario 499R-1B. Explique la razón del ajuste enun anejo el cual debe incluirse con la planilla.

Fecha en que deberá rendirse el Formulario499R-1B y efectuarse el pago - La planilla deberásometerse no más tarde del 30 de abril, 31 de julio,31 de octubre y 31 de enero de cada año. La mismadeberá estar acompañada de un cheque o giro postala nombre del Secretario de Hacienda con un cupónde depósito por aquella parte de la contribución queno haya sido pagada o depositada según seestablece en las Secciones 6041.05 o 6080.05 delCódigo.

Dónde deberá rendirse - La planilla deberáprepararse y rendirse electrónicamente accediendoal siguiente enlace:

http://planillatrimestralpatronal.hacienda.pr.gov/.

II. DEPOSITO DE CONTRIBUCION RETENIDA SOBRE SALARIOS (FORMULARIO 499.R-1)

El total de la contribución deducida y retenida porun patrono sobre los salarios de sus empleados deberádepositarse en cualesquiera de las institucionesbancarias designadas como depositarias de fondospúblicos y autorizadas como tal por el Secretario deHacienda.

El depósito se hará de la forma, en el tiempo ybajo las condiciones indicadas a principio de estasección. El depósito deberá estar acompañado deel cupón preimpreso que emite el Departamento.

The determination of whether an employer is amonthly or semiweekly depositor will be madeannually based on the employer’s tax withholdingpayment history during the 12 month lookbackperiod ending on June 30 of the preceding year(2013).

I. EMPLOYER'S QUARTERLY RETURN OFINCOME TAX WITHHELD (FORM 499R-1B)

Content of the Return - The return shallinclude all information on the income tax withheldupon the wages paid by the employer to his/heremployees, during the quarter for which it is filed,as provided by Section 1062.01 of the Code. Thereturn shall be prepared on behalf of the employerwho makes the payments and shall be signedelectronically by him/her, by the person whoexercises the control over the payment of wagesor by a Specialist who is active in the SpecialistOfficial Registry. If the employer is a corporation,the president, principal executive or officer with asimilar title must sign. If the employer is apartnership, the managing partner must sign.

In the case of an employer that has a creditfrom previous quarters, said employer must claimthis credit on line 5 of Form 499R-1B. Explain thereason for the adjustment in a schedule and includeit with the return.

Date in which Form 499R-1B must befiled and payment must be made - The returnshall be filed on or before April 30, July 31,October 31 and January 31 of each year. Thesame shall be accompanied by a check ormoney order payable to the Secretary of theTreasury with a deposit coupon for said portionof the tax wh ich has not been pa id ordeposited, as established by Sections 6041.05or 6080.05 of the Code.

Where it should be filed - The return shall beprepared and filed electronically by accesing thefollowing link:

http://planillatrimestralpatronal.hacienda.pr.gov/.

II. DEPOSIT OF INCOME TAX WITHHELD ON WAGES (FORM 499.R-1)

The amount of tax deducted and withheld byan employer upon the wages paid to his/heremployees shall be deposited in any of the bankinginstitutions designated as depositaries of publicfunds and authorized as such by the Secretary ofthe Treasury.

The deposit shall be made in the form, time andunder the conditions described at the beginning ofthis section. The deposit shall be made accompaniedby the printed coupon issued by the Department.

Los patronos que no hayan recibido estoscupones preimpresos deberán comunicarse con elCentro de Llamadas y Correspondencia delNegociado de Servicio al Contribuyente al (787) 722-0216, opción número 1 del directorio.

También, los patronos pueden utilizar el serviciode Colecturía Virtual para realizar los depósitos dela contribución deducida y retenida sobre salarios.Este servicio está disponible en nuestra página deInternet: www.hacienda.gobierno.pr y no requiere loscupones preimpresos.

III. ESTADO DE RECONCILIACION DE CONTRIBUCION SOBRE INGRESOS RETENIDA (FORMULARIO 499R-3)

Todo patrono obligado a deducir y retenercontribuciones sobre los salarios de sus empleados,deberá rendir un estado de reconciliación anual dondeconste el total de la contribución deducida y retenidadurante el año natural sobre dichos salarios, según loestablece la Sección 1062.01 del Código. Este estadose rendirá electrónicamente además de cualesquieraotros documentos, no más tarde del 31 de enero delaño siguiente al año natural para el cual se rinde.

IV. COMPROBANTE DE RETENCION(FORMULARIO 499R-2/W-2PR)

Todo patrono obligado a deducir y retenercontribuciones sobre los salarios de sus empleados, oque estará así obligado de haber los empleadosreclamado solamente la exención personal admitida aun individuo soltero, suministrará a cada uno de dichosempleados con respecto a su empleo durante el añonatural, una declaración escrita en la que constará eltotal de los salarios pagados por el patrono durantedicho año natural y el total de la contribución deduciday retenida bajo la Sección 1062.01 del Código sobredichos salarios, no más tarde del 31 de enero del añosiguiente. Si su empleo terminara antes del cierre dedicho año natural, entonces deberá suministrar elcomprobante de retención el día en que se efectuaráel último pago de salarios.

Asegúrese de que las copias que deberá entregaral empleado contengan el número de confirmación deradicación electrónica provisto por el Departamento unavez completada la radicación electrónica de esteformulario.

V. INTERESES, RECARGOS Y PENALIDADES

1. Intereses - El Código dispone que se añadanintereses a razón del 10% anual sobre cualquierbalance de contribuciones que no haya sidopagado a la fecha de su vencimiento.

2. Recargos - Cuando proceda añadir intereses,se cobrará además, un recargo de 5% del totalno pagado, si la demora es por más de 30días y no más de 60 días. Si la demora excedede 60 días, el recargo será por 10% del totalno pagado.

Employers who have not received thepreprinted coupons must contact the Calls andCorrespondence Center of the Taxpayer's ServiceBureau at (787) 722-0216, option number 1 of thedirectory.

Also, employers can use the Payments Onlineservice to deposit the tax deducted and withheld fromsalaries. This service is available at our webpage:www.hacienda.gobierno.pr and does not require thepreprinted coupons.

III. RECONCILIATION STATEMENT OF INCOME TAX WITHHELD (FORM 499R-3)

Every employer required to deduct and withholdtaxes upon the wages of his/her employees, shallfile an annual reconciliation statement showing thetotal tax deducted and withheld during the calendaryear upon said wages, as established by Section1062.01 of the Code. Said statement shall be filedelectronically in addition to any other documents,on or before January 31 of the year following thecalendar year for which it is filed.

IV. WITHHOLDING STATEMENT (FORM 499R-2/W-2PR)

Every employer required to deduct and withholdtaxes from the wages of his/her employees, or whois so required if the employees had claimed only thepersonal exemption allowed to an individual who issingle, shall furnish to each of such employees withrespect to his/her employment during the calendaryear, a written statement showing the total wagespaid by the employer during such calendar year andthe total tax deducted and withheld under Section1062.01 of the Code upon such wages, on or beforeJanuary 31 of the following year. If his/heremployment terminates before the close of suchcalendar year, then the withholding statement shallbe furnished on the day the last payment of wages ismade.