Inteligencia Competitiva INTELIGENCIA · PDF fileInteligencia Competitiva Contenido Personas...

15

Inteligencia Competitiva Inteligencia Competitiva Leganés Leganés , 30 noviembre 2007 , 30 noviembre 2007 ÍNDICE INTELIGENCIA COMPETITIVA Manuel González San Segundo Leganés, 30 Noviembre 2007

Transcript of Inteligencia Competitiva INTELIGENCIA · PDF fileInteligencia Competitiva Contenido Personas...

Inteligencia Competitiva Inteligencia Competitiva

LeganésLeganés, 30 noviembre 2007, 30 noviembre 2007

ÍNDICE

INTELIGENCIA COMPETITIVA

Manuel González San SegundoLeganés, 30 Noviembre 2007

Inteligencia CompetitivaInteligencia Competitiva

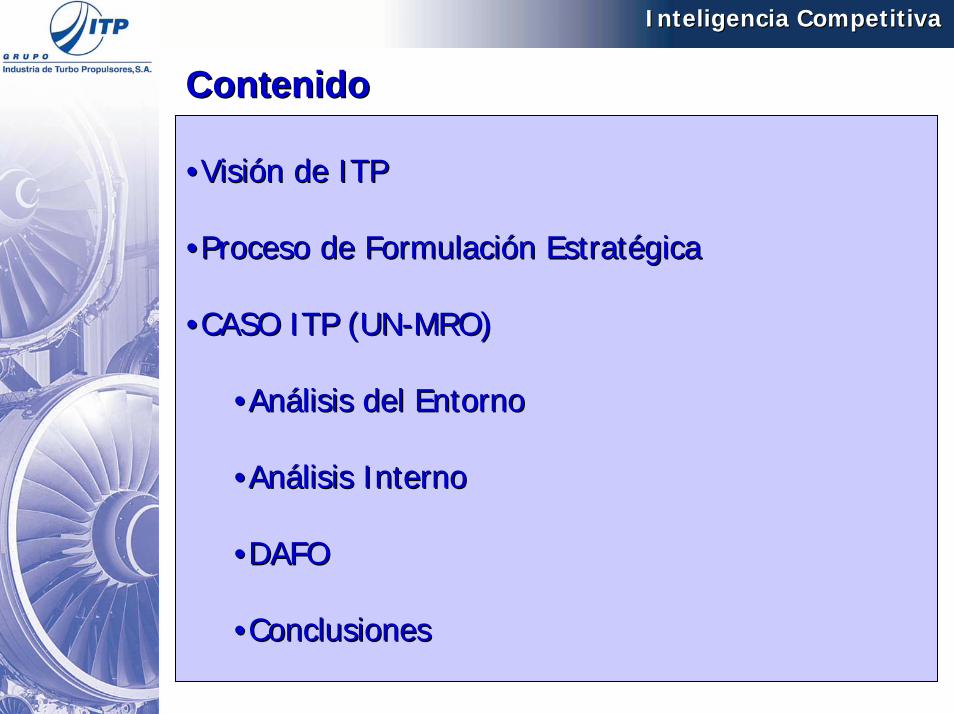

ContenidoContenido

Personas que han integrado el equipo••Visión de ITPVisión de ITP

••Proceso de Formulación EstratégicaProceso de Formulación Estratégica

••CASO ITP (UNCASO ITP (UN--MRO)MRO)

••Análisis del EntornoAnálisis del Entorno

••Análisis InternoAnálisis Interno

••DAFODAFO

••ConclusionesConclusiones

Inteligencia CompetitivaInteligencia Competitiva

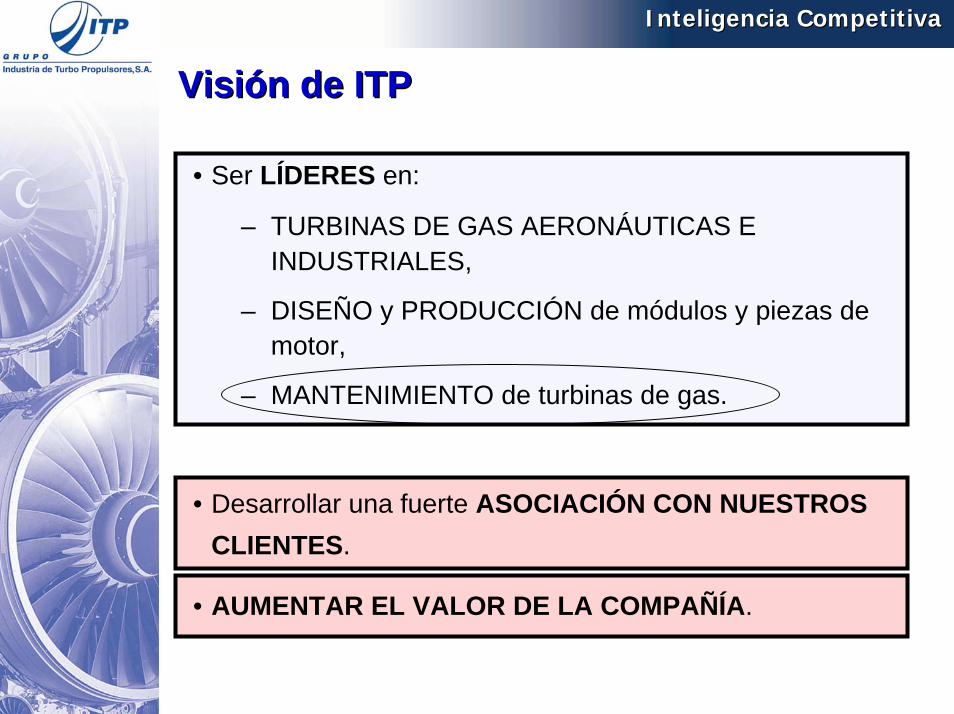

Visión de ITPVisión de ITP

• Ser LÍDERES en:

– TURBINAS DE GAS AERONÁUTICAS E INDUSTRIALES,

– DISEÑO y PRODUCCIÓN de módulos y piezas de motor,

– MANTENIMIENTO de turbinas de gas.

• Desarrollar una fuerte ASOCIACIÓN CON NUESTROS CLIENTES.

• AUMENTAR EL VALOR DE LA COMPAÑÍA.

Inteligencia CompetitivaInteligencia Competitiva

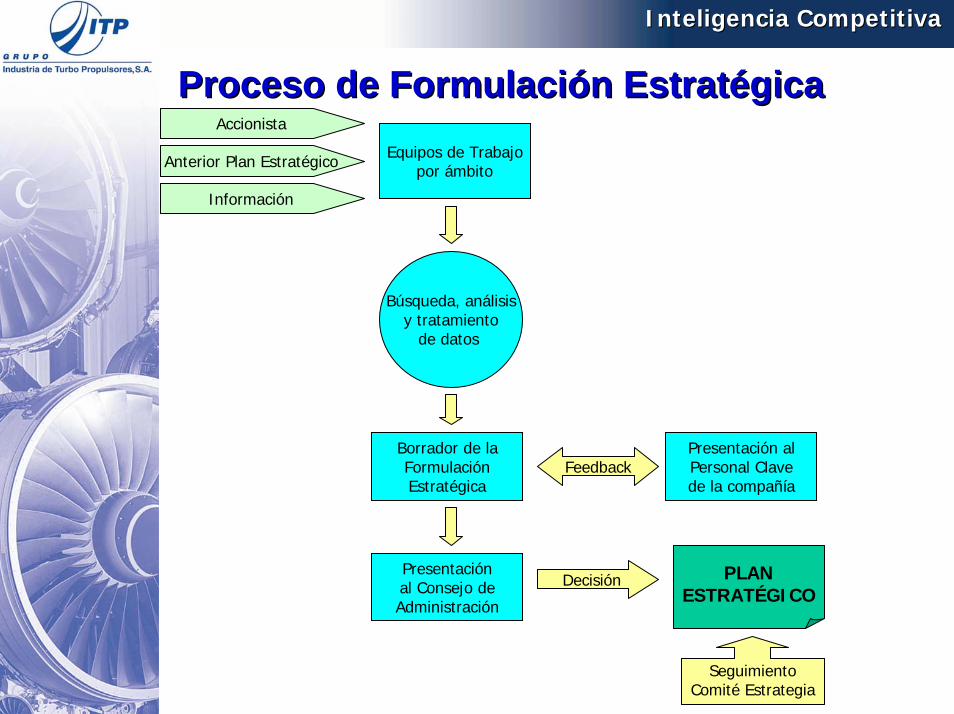

Proceso de Formulación EstratégicaProceso de Formulación Estratégica

Anterior Plan Estratégico Equipos de Trabajopor ámbito

Accionista

Información

Búsqueda, análisisy tratamiento

de datos

Borrador de laFormulaciónEstratégica

Presentación alPersonal Clavede la compañía

Presentaciónal Consejo deAdministración

Feedback

PLANESTRATÉGICO

Decisión

SeguimientoComité Estrategia

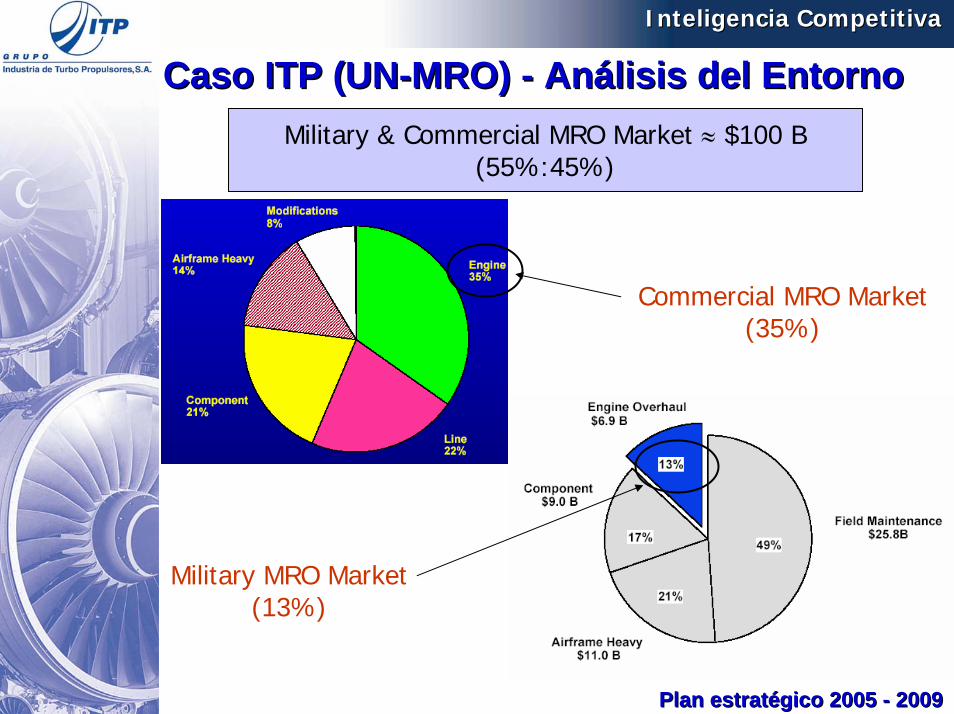

Caso ITP (UNCaso ITP (UN--MRO) MRO) -- Análisis del EntornoAnálisis del Entorno

Plan estratégico 2005 Plan estratégico 2005 -- 20092009

Military & Commercial MRO Market ≈ $100 B(55%:45%)

Commercial MRO Market(35%)

Military MRO Market(13%)

Inteligencia CompetitivaInteligencia Competitiva

MantenimientoMantenimientoXIII ConvenciónXIII Convención

Plan estratégico 2005 Plan estratégico 2005 -- 20092009

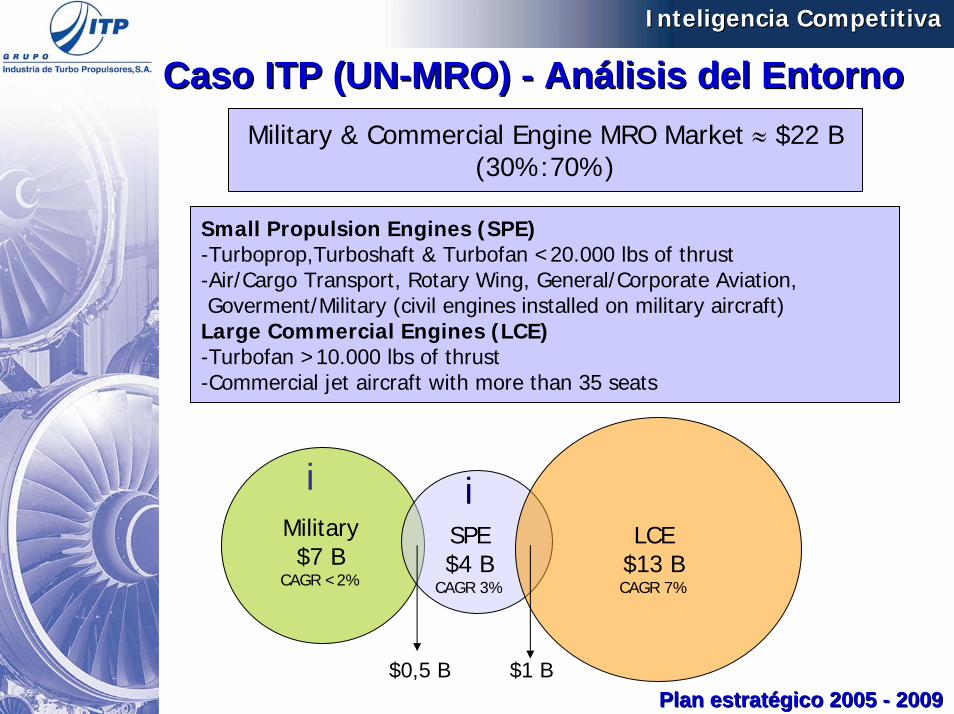

Small Propulsion Engines (SPE)-Turboprop,Turboshaft & Turbofan <20.000 lbs of thrust-Air/Cargo Transport, Rotary Wing, General/Corporate Aviation,Goverment/Military (civil engines installed on military aircraft)

Large Commercial Engines (LCE)-Turbofan >10.000 lbs of thrust-Commercial jet aircraft with more than 35 seats

Military & Commercial Engine MRO Market ≈ $22 B(30%:70%)

Military$7 B

CAGR <2%

SPE$4 B

CAGR 3%

LCE$13 BCAGR 7%

$0,5 B $1 B

i i

Inteligencia CompetitivaInteligencia Competitiva

Caso ITP (UNCaso ITP (UN--MRO) MRO) -- Análisis del EntornoAnálisis del Entorno

MantenimientoMantenimientoXIII ConvenciónXIII Convención

Plan estratégico 2005 Plan estratégico 2005 -- 20092009

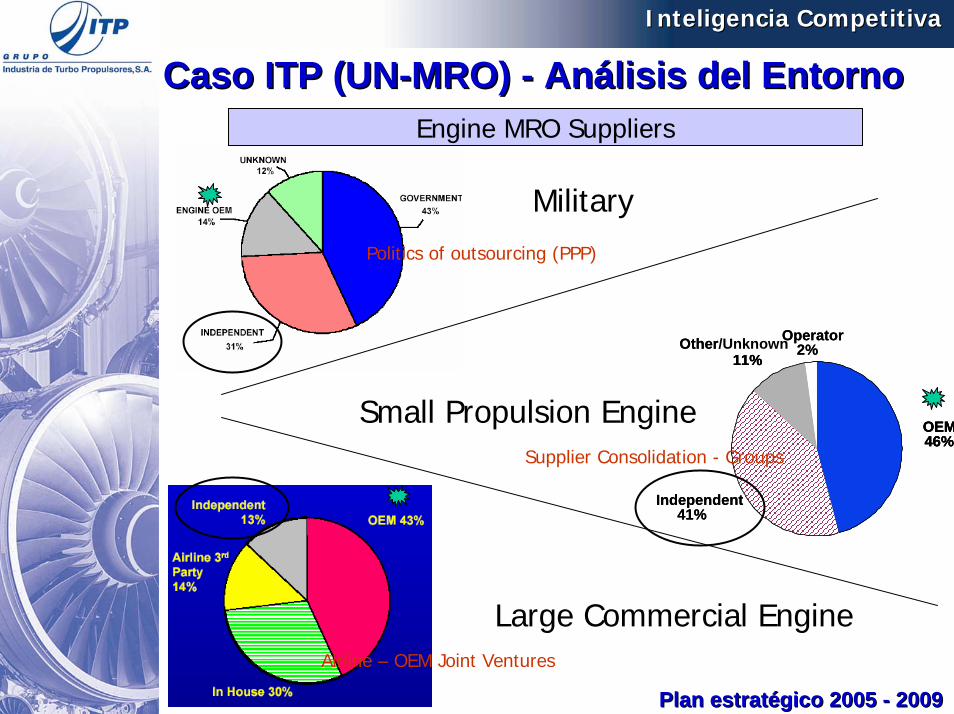

Engine MRO Suppliers

OEM46%

Independent41%

Other/Unknown11%

Operator2%

OEM46%OEM46%

Independent41%

11%Other

11%Operator

2%

Military

Small Propulsion Engine

Large Commercial Engine

Politics of outsourcing (PPP)

Supplier Consolidation - Groups

Airline – OEM Joint Ventures

Inteligencia CompetitivaInteligencia Competitiva

Caso ITP (UNCaso ITP (UN--MRO) MRO) -- Análisis del EntornoAnálisis del Entorno

MantenimientoMantenimientoXIII ConvenciónXIII Convención

Plan estratégico 2005 Plan estratégico 2005 -- 20092009

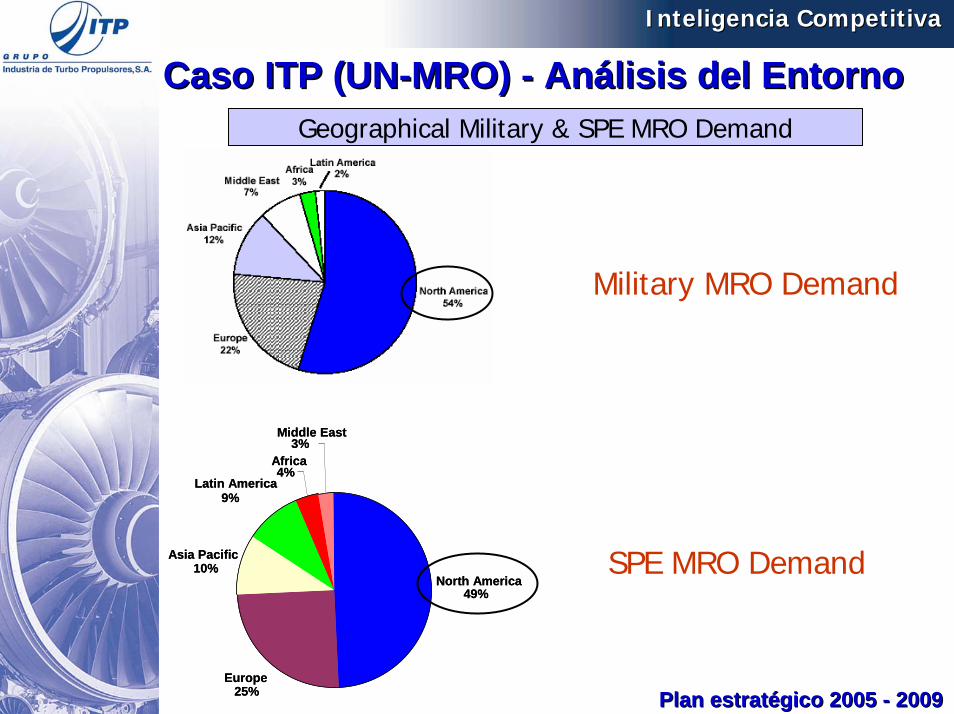

Geographical Military & SPE MRO Demand

North America49%

Europe25%

Asia Pacific10%

Latin America9%

Africa4%

Middle East3%

North America49%

Europe25%

Asia Pacific10%

Latin America9%

Africa4%

Middle East3%

Military MRO Demand

SPE MRO Demand

Inteligencia CompetitivaInteligencia Competitiva

Caso ITP (UNCaso ITP (UN--MRO) MRO) -- Análisis del EntornoAnálisis del Entorno

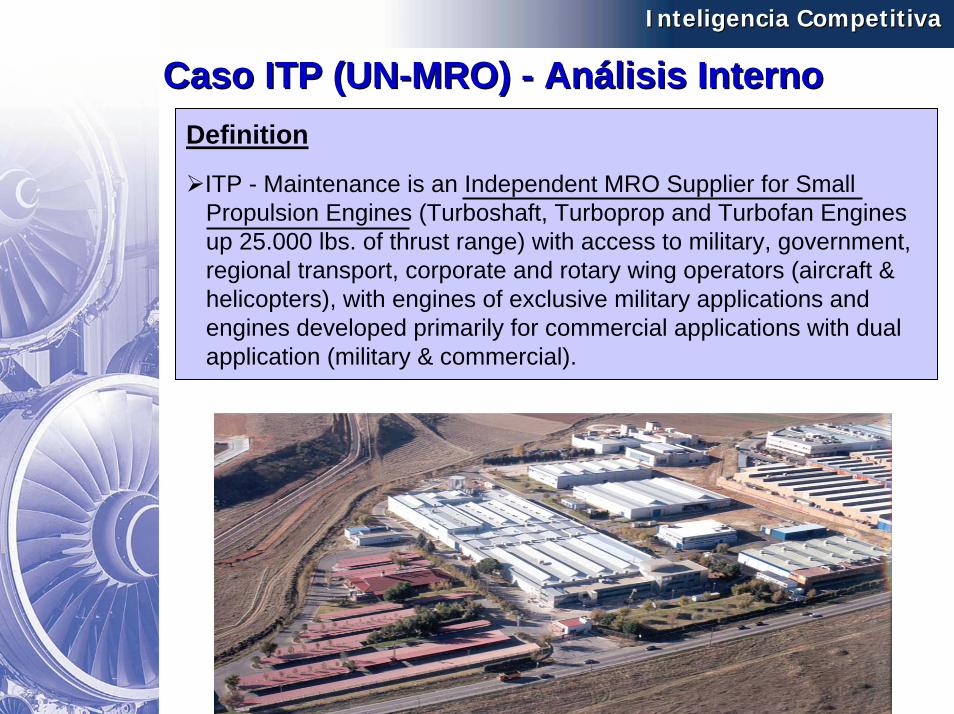

Definition

ITP - Maintenance is an Independent MRO Supplier for SmallPropulsion Engines (Turboshaft, Turboprop and Turbofan Engines up 25.000 lbs. of thrust range) with access to military, government,regional transport, corporate and rotary wing operators (aircraft &helicopters), with engines of exclusive military applications andengines developed primarily for commercial applications with dual application (military & commercial).

Inteligencia CompetitivaInteligencia Competitiva

Caso ITP (UNCaso ITP (UN--MRO) MRO) -- Análisis InternoAnálisis Interno

General DataTotal Engine MRO turnover: $100 M (2005)

Military Engine MRO Account for 80%

Approvals: EASA part145 (ES.145.003), FAA Repair Station (ISUY164X),PECAL/AQAP 2110 (7016/02/98/00),EN9100:2003 (OP-0002/02),prEN9110 (OP-0007/2005),ISO14001 (CGM-01/043),OSHAS18000

Total MRO staff: 350

Annual MRO Capacity (manhours): 330.000

Annual MRO Output: 300 engines / 175 modules

Total engine MRO shop space (m2): 20.000 Ajalvir + 2.500 Arganda

Other facilities: 2 Turbofan Cells (25.000 lbs), 2 Turboshaft Cells (5.000 shp),2 Turboshaft Cells (Development TP400 + MTR390)

Inteligencia CompetitivaInteligencia Competitiva

Caso ITP (UNCaso ITP (UN--MRO) MRO) -- Análisis InternoAnálisis Interno

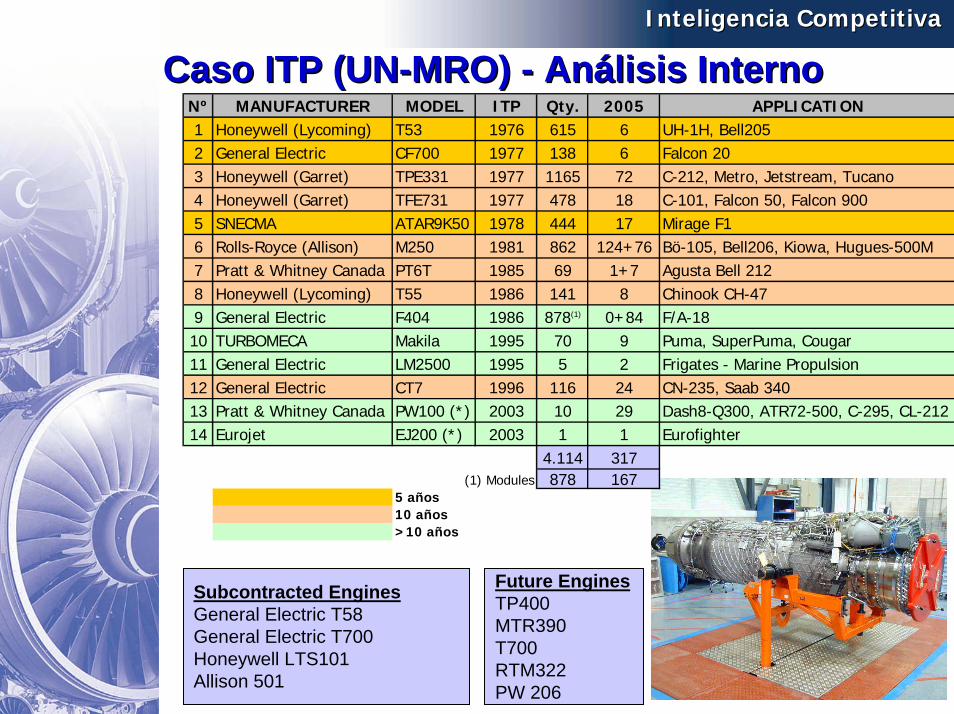

Subcontracted EnginesGeneral Electric T58General Electric T700Honeywell LTS101Allison 501

Future EnginesTP400MTR390T700RTM322PW 206

Nº MANUFACTURER MODEL ITP Qty. 2005 APPLICATION1 Honeywell (Lycoming) T53 1976 615 6 UH-1H, Bell2052 General Electric CF700 1977 138 6 Falcon 203 Honeywell (Garret) TPE331 1977 1165 72 C-212, Metro, Jetstream, Tucano4 Honeywell (Garret) TFE731 1977 478 18 C-101, Falcon 50, Falcon 9005 SNECMA ATAR9K50 1978 444 17 Mirage F16 Rolls-Royce (Allison) M250 1981 862 124+76 Bö-105, Bell206, Kiowa, Hugues-500M 7 Pratt & Whitney Canada PT6T 1985 69 1+7 Agusta Bell 2128 Honeywell (Lycoming) T55 1986 141 8 Chinook CH-479 General Electric F404 1986 878(1) 0+84 F/A-1810 TURBOMECA Makila 1995 70 9 Puma, SuperPuma, Cougar11 General Electric LM2500 1995 5 2 Frigates - Marine Propulsion12 General Electric CT7 1996 116 24 CN-235, Saab 34013 Pratt & Whitney Canada PW100 (*) 2003 10 29 Dash8-Q300, ATR72-500, C-295, CL-21214 Eurojet EJ200 (*) 2003 1 1 Eurofighter

4.114 317(1) Modules 878 167

5 años10 años>10 años

Inteligencia CompetitivaInteligencia Competitiva

Caso ITP (UNCaso ITP (UN--MRO) MRO) -- Análisis InternoAnálisis Interno

MantenimientoMantenimientoXX

PP

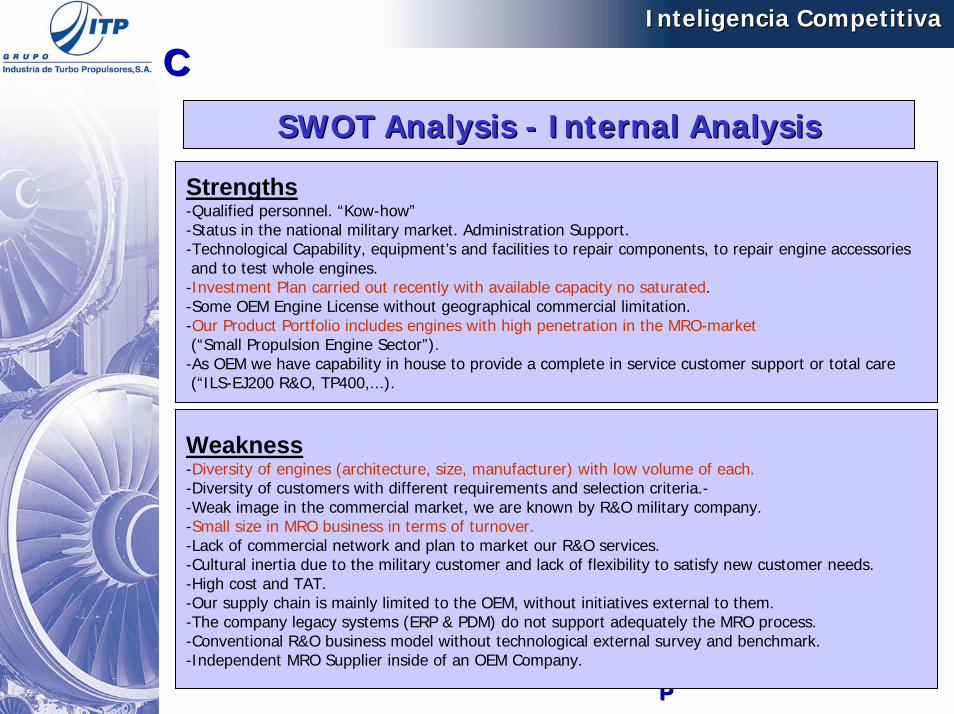

SWOT SWOT AnalysisAnalysis -- Internal AnalysisInternal Analysis

Strengths-Qualified personnel. “Kow-how”-Status in the national military market. Administration Support.-Technological Capability, equipment’s and facilities to repair components, to repair engine accessoriesand to test whole engines.

-Investment Plan carried out recently with available capacity no saturated.-Some OEM Engine License without geographical commercial limitation.-Our Product Portfolio includes engines with high penetration in the MRO-market(“Small Propulsion Engine Sector”).

-As OEM we have capability in house to provide a complete in service customer support or total care(“ILS-EJ200 R&O, TP400,...).

Weakness-Diversity of engines (architecture, size, manufacturer) with low volume of each.-Diversity of customers with different requirements and selection criteria.--Weak image in the commercial market, we are known by R&O military company.-Small size in MRO business in terms of turnover.-Lack of commercial network and plan to market our R&O services.-Cultural inertia due to the military customer and lack of flexibility to satisfy new customer needs.-High cost and TAT.-Our supply chain is mainly limited to the OEM, without initiatives external to them.-The company legacy systems (ERP & PDM) do not support adequately the MRO process.-Conventional R&O business model without technological external survey and benchmark.-Independent MRO Supplier inside of an OEM Company.

Inteligencia CompetitivaInteligencia Competitiva

CC

MantenimientoMantenimientoXX

PP

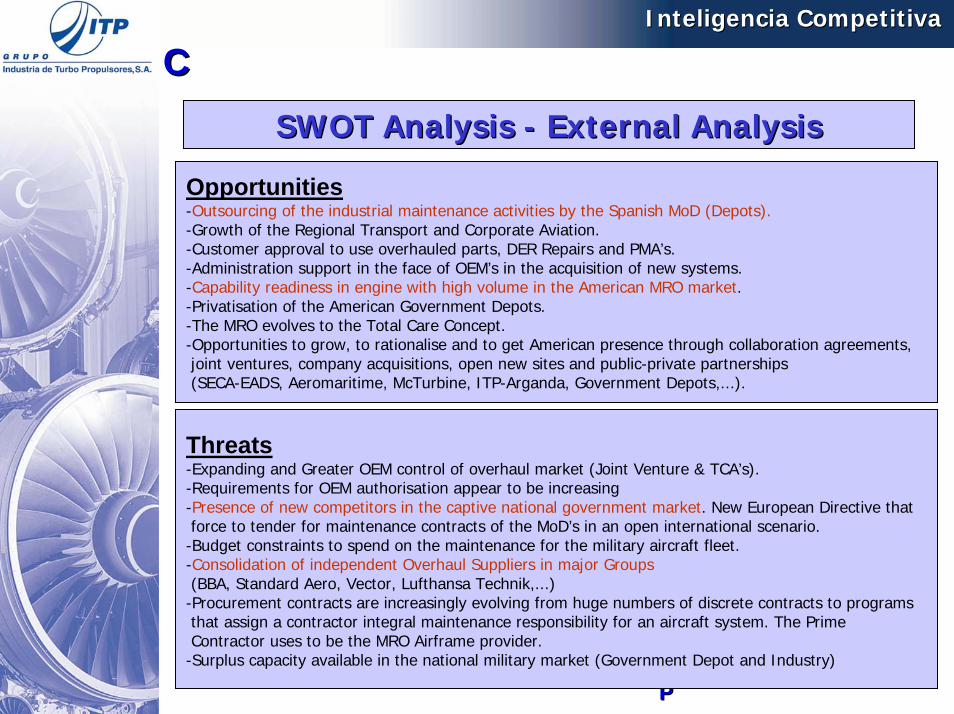

SWOT SWOT AnalysisAnalysis -- ExternalExternal AnalysisAnalysis

Opportunities-Outsourcing of the industrial maintenance activities by the Spanish MoD (Depots).-Growth of the Regional Transport and Corporate Aviation.-Customer approval to use overhauled parts, DER Repairs and PMA’s.-Administration support in the face of OEM’s in the acquisition of new systems.-Capability readiness in engine with high volume in the American MRO market.-Privatisation of the American Government Depots.-The MRO evolves to the Total Care Concept.-Opportunities to grow, to rationalise and to get American presence through collaboration agreements,joint ventures, company acquisitions, open new sites and public-private partnerships(SECA-EADS, Aeromaritime, McTurbine, ITP-Arganda, Government Depots,...).

Threats-Expanding and Greater OEM control of overhaul market (Joint Venture & TCA’s).-Requirements for OEM authorisation appear to be increasing-Presence of new competitors in the captive national government market. New European Directive thatforce to tender for maintenance contracts of the MoD’s in an open international scenario.

-Budget constraints to spend on the maintenance for the military aircraft fleet.-Consolidation of independent Overhaul Suppliers in major Groups(BBA, Standard Aero, Vector, Lufthansa Technik,...)

-Procurement contracts are increasingly evolving from huge numbers of discrete contracts to programsthat assign a contractor integral maintenance responsibility for an aircraft system. The PrimeContractor uses to be the MRO Airframe provider.

-Surplus capacity available in the national military market (Government Depot and Industry)

Inteligencia CompetitivaInteligencia Competitiva

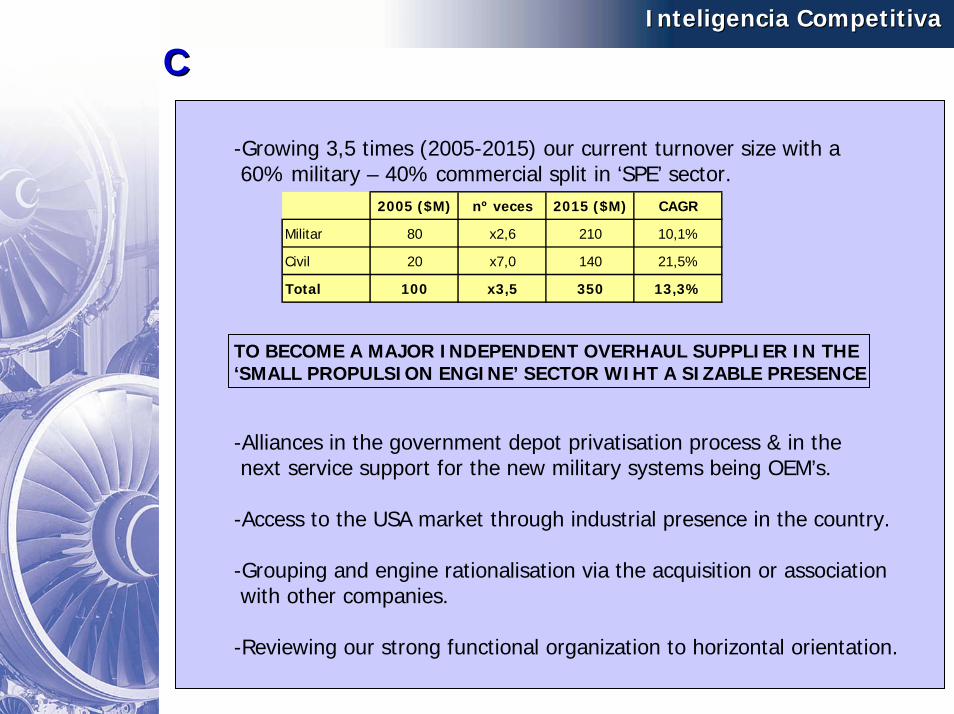

CC

-Growing 3,5 times (2005-2015) our current turnover size with a 60% military – 40% commercial split in ‘SPE’ sector.

TO BECOME A MAJOR INDEPENDENT OVERHAUL SUPPLIER IN THE‘SMALL PROPULSION ENGINE’ SECTOR WIHT A SIZABLE PRESENCE

-Alliances in the government depot privatisation process & in thenext service support for the new military systems being OEM’s.

-Access to the USA market through industrial presence in the country.

-Grouping and engine rationalisation via the acquisition or associationwith other companies.

-Reviewing our strong functional organization to horizontal orientation.

2005 ($M) nº veces 2015 ($M) CAGR

Militar 80 x2,6 210 10,1%

Civil 20 x7,0 140 21,5%

Total 100 x3,5 350 13,3%

MantenimientoMantenimientoXX Inteligencia CompetitivaInteligencia Competitiva

CC

MantenimientoMantenimientoXIII ConvenciónXIII Convención

Plan estratégico 2005 Plan estratégico 2005 -- 20092009

Inteligencia CompetitivaInteligencia Competitiva

GRACIAS