Conclave Presentation Markets

26

PENSION MARKETS AND PENSION MARKETS AND PRODUCTS IN INDIA PRODUCTS IN INDIA

-

Upload

siddhartha-jain -

Category

Documents

-

view

225 -

download

0

Transcript of Conclave Presentation Markets

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 1/26

PENSION MARKETS ANDPENSION MARKETS AND

PRODUCTS IN INDIAPRODUCTS IN INDIA

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 2/26

PRODUCTSPRODUCTSWhat is the right product?What is the right product?

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 3/26

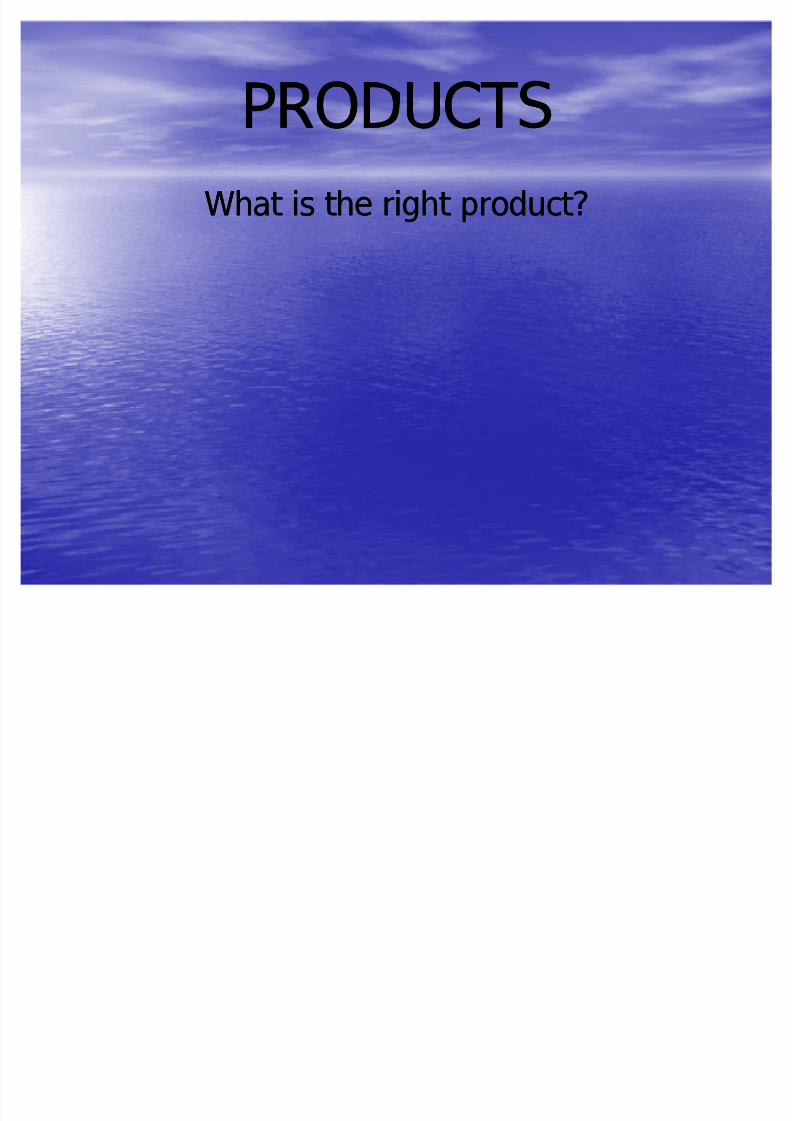

1

2

3

4

5

Flexibility in time and

amount of deposit

Account in your own name

Portability of the accoun

Earn Interest on your

deposits

Opportunity to change

your choices

Save in this acount till your

old age

Pension payment for the

rest of your life

Paid to nominee if you die

or after retirement

Low tax benefit

Urban Rural

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 4/26

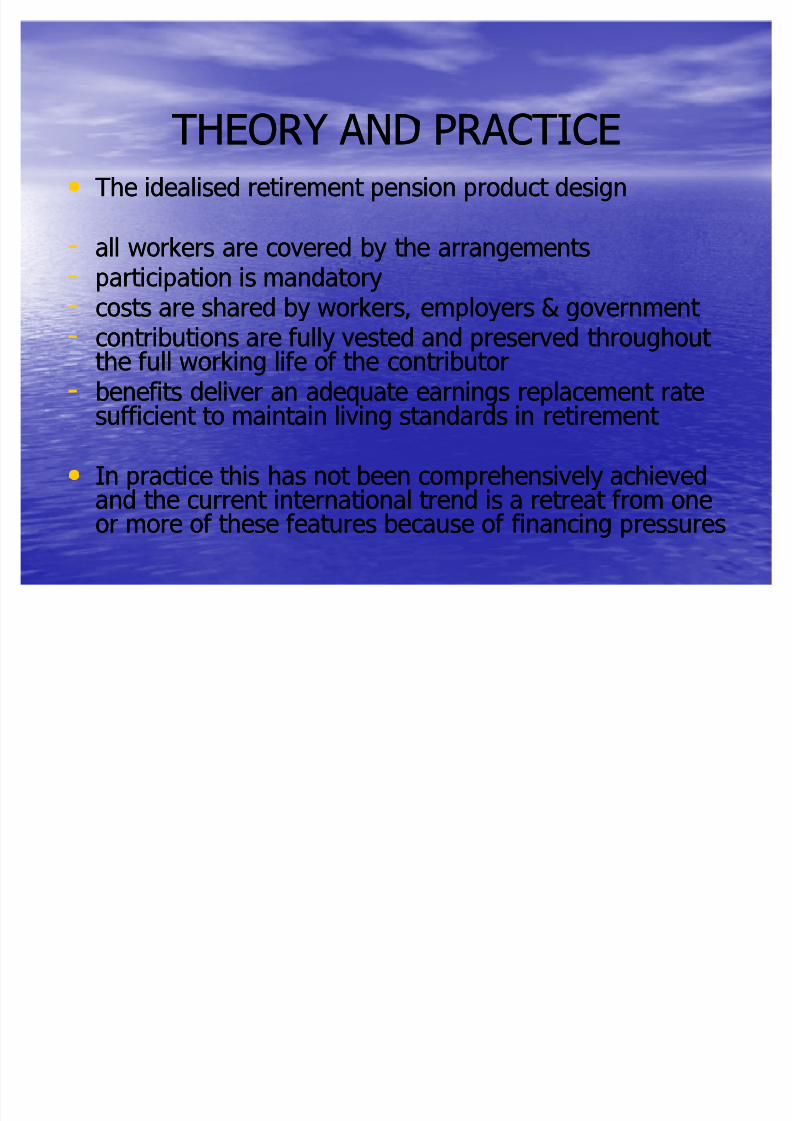

THEORY AND PRACTICETHEORY AND PRACTICE The idealised retirement pension product designThe idealised retirement pension product design

-- all workers are covered by the arrangementsall workers are covered by the arrangements

-- participation is mandatoryparticipation is mandatory-- costs are shared by workers, employers & government costs are shared by workers, employers & government -- contributions are fully vested and preserved throughout contributions are fully vested and preserved throughout

the full working life of the contributorthe full working life of the contributor-- benefits deliver an adequate earnings replacement ratebenefits deliver an adequate earnings replacement rate

sufficient to maintain living standards in retirement sufficient to maintain living standards in retirement

In practice this has not been comprehensively achievedIn practice this has not been comprehensively achievedand the current international trend is a retreat from oneand the current international trend is a retreat from oneor more of these features because of financing pressuresor more of these features because of financing pressures

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 5/26

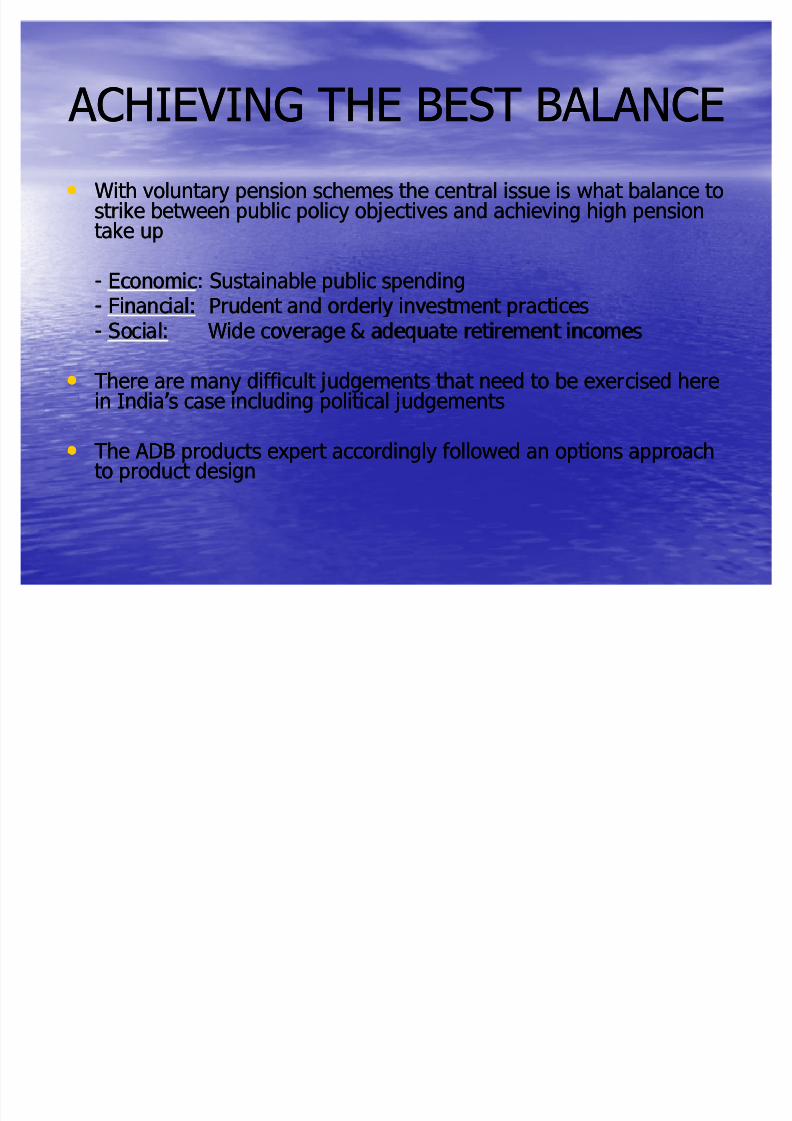

ACHIEVING THE BEST BALANCE ACHIEVING THE BEST BALANCE

With voluntary pension schemes the central issue is what balance toWith voluntary pension schemes the central issue is what balance tostrike between public policy objectives and achieving high pensionstrike between public policy objectives and achieving high pensiontake uptake up

-- EconomicEconomic: Sustainable public spending: Sustainable public spending-- Financial:Financial: Prudent and orderly investment practicesPrudent and orderly investment practices-- Social:Social: Wide coverage & adequate retirement incomesWide coverage & adequate retirement incomes

There are many difficult judgements that need to be exercised hereThere are many difficult judgements that need to be exercised herein Indias case including political judgementsin Indias case including political judgements

The ADB products expert accordingly followed an options approachThe ADB products expert accordingly followed an options approachto product designto product design

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 6/26

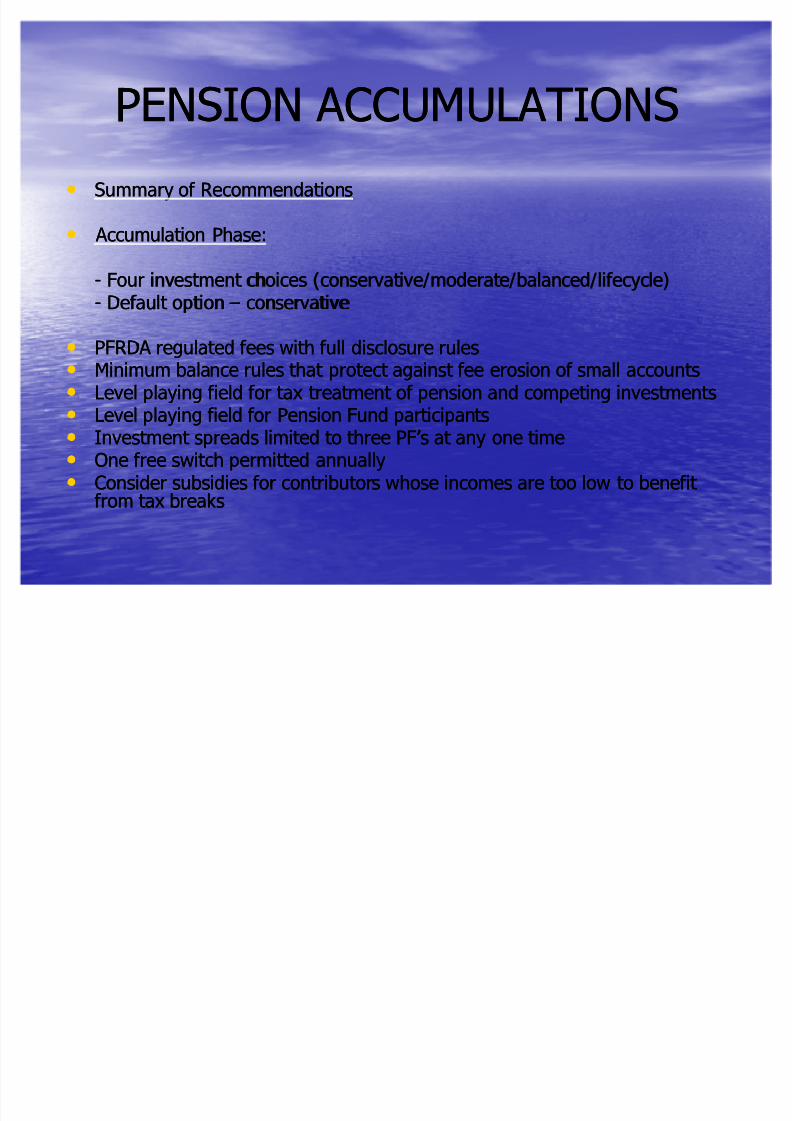

PENSION ACCUMULATIONSPENSION ACCUMULATIONS

Summary of RecommendationsSummary of Recommendations

Accumulation Phase: Accumulation Phase:

-- Four investment choices (conservative/moderate/balanced/lifecycle)Four investment choices (conservative/moderate/balanced/lifecycle)-- Default optionDefault option conservativeconservative

PFRDA regulated fees with full disclosure rulesPFRDA regulated fees with full disclosure rules Minimum balance rules that protect against fee erosion of small accountsMinimum balance rules that protect against fee erosion of small accounts Level playing field for tax treatment of pension and competing investmentsLevel playing field for tax treatment of pension and competing investments

Level playing field for Pension Fund participantsLevel playing field for Pension Fund participants Investment spreads limited to three PFs at any one timeInvestment spreads limited to three PFs at any one time One free switch permitted annuallyOne free switch permitted annually Consider subsidies for contributors whose incomes are too low to benefit Consider subsidies for contributors whose incomes are too low to benefit

from tax breaksfrom tax breaks

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 7/26

BENEFITSBENEFITS

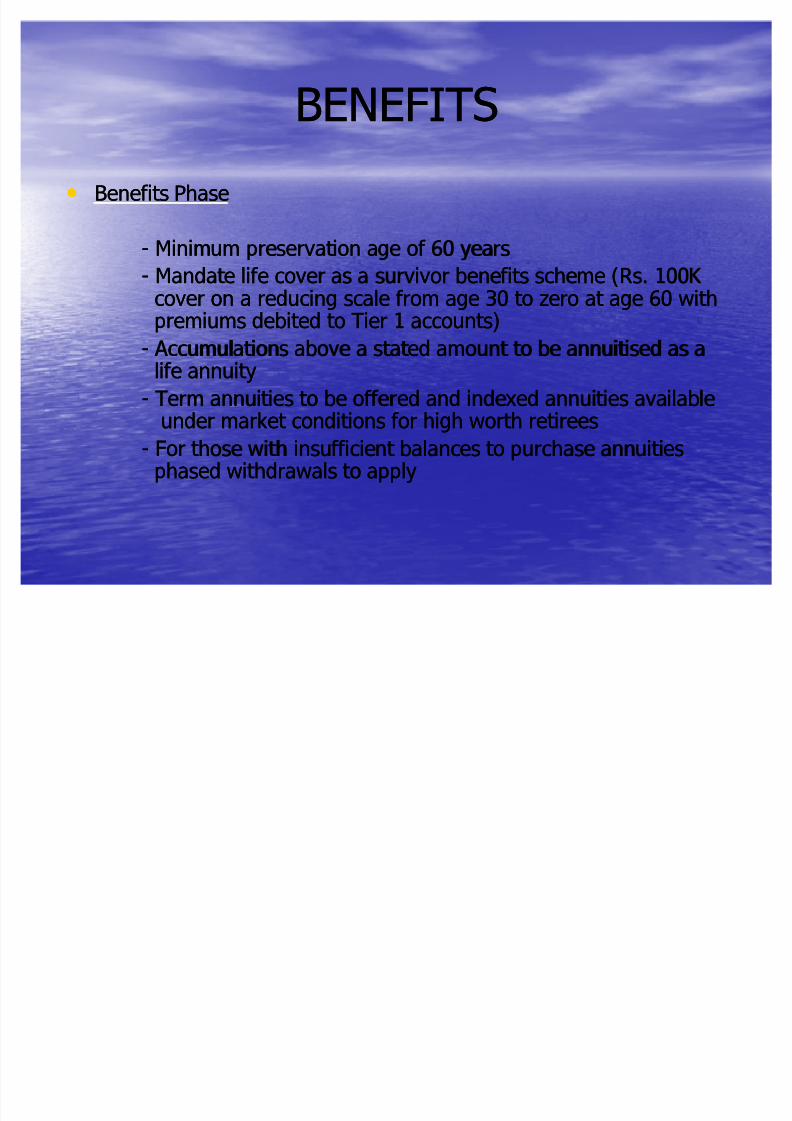

Benefits PhaseBenefits Phase

-- Minimum preservation age of 60 yearsMinimum preservation age of 60 years

-- Mandate life cover as a survivor benefits scheme (Rs. 100K Mandate life cover as a survivor benefits scheme (Rs. 100K cover on a reducing scale from age 30 to zero at age 60 withcover on a reducing scale from age 30 to zero at age 60 withpremiums debited to Tier 1 accounts)premiums debited to Tier 1 accounts)

-- Accumulations above a stated amount to be annuitised as a Accumulations above a stated amount to be annuitised as alife annuitylife annuity

-- Term annuities to be offered and indexed annuities availableTerm annuities to be offered and indexed annuities availableunder market conditions for high worth retireesunder market conditions for high worth retirees

-- For those with insufficient balances to purchase annuitiesFor those with insufficient balances to purchase annuitiesphased withdrawals to applyphased withdrawals to apply

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 8/26

SUNSCRIBER SERVICESSUNSCRIBER SERVICES

Subscriber ServicesSubscriber Services

-- Plain language advising on investment options and PFPlain language advising on investment options and PFperformanceperformance

-- Accessible and speedy complaints resolutions mechanism Accessible and speedy complaints resolutions mechanismto be institutedto be instituted

-- Financial advisory services to be offeredFinancial advisory services to be offered

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 9/26

NPS MARKETSNPS MARKETSGrowing the NPS market Growing the NPS market

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 10/26

IDENTIFYING THE CONSTRAINTSIDENTIFYING THE CONSTRAINTS

NPS is to be based on voluntaryNPS is to be based on voluntaryparticipation with minimal public subsidiesparticipation with minimal public subsidies

for contributorsfor contributors

-- Participation levels therefore will beParticipation levels therefore will bedriven principally by consumer sentiment driven principally by consumer sentiment

NPS pensions will be sold not bought NPS pensions will be sold not bought

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 11/26

IDENTIFYING THE CONSTRAINTSIDENTIFYING THE CONSTRAINTS

Savings preferences presently operateSavings preferences presently operateover relatively short over relatively short--term time horizonsterm time horizons

and are investment drivenand are investment driven

-- A psyche change is required for A psyche change is required forvoluntary pensions to gain a foothold involuntary pensions to gain a foothold in

the market the market

Psyche change must be actively cultivatedPsyche change must be actively cultivated

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 12/26

IDENTIFYING THE CONSTRAINTSIDENTIFYING THE CONSTRAINTS

Pension products have a low profilePension products have a low profilepresently among Indian consumerspresently among Indian consumers

-- Effective profiling of pension utilities forEffective profiling of pension utilities forworkers is requiredworkers is required

-- Achieving this will require long term Achieving this will require long termcommitment commitment

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 13/26

IDENTIFYING THE CONSTRAINTSIDENTIFYING THE CONSTRAINTS

Lack of data on the savings capacities andLack of data on the savings capacities andpreferences of workers for informed decisionpreferences of workers for informed decisionmakingmaking

-- Evidence led decision making is not possibleEvidence led decision making is not possibleuntil the necessary data sets are createduntil the necessary data sets are created

ADB data is a good beginning but more is required ADB data is a good beginning but more is required

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 14/26

KEY OBJECTIVES OF THE ADB SURVEY KEY OBJECTIVES OF THE ADB SURVEY

1.1. Assess the potential size of the market in India Assess the potential size of the market in Indiafor NPS pensions at the present timefor NPS pensions at the present time

2. Provide a facility for segmenting that market 2. Provide a facility for segmenting that market

3. Provide guidance for shaping NPS marketing3. Provide guidance for shaping NPS marketingand sales strategiesand sales strategies

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 15/26

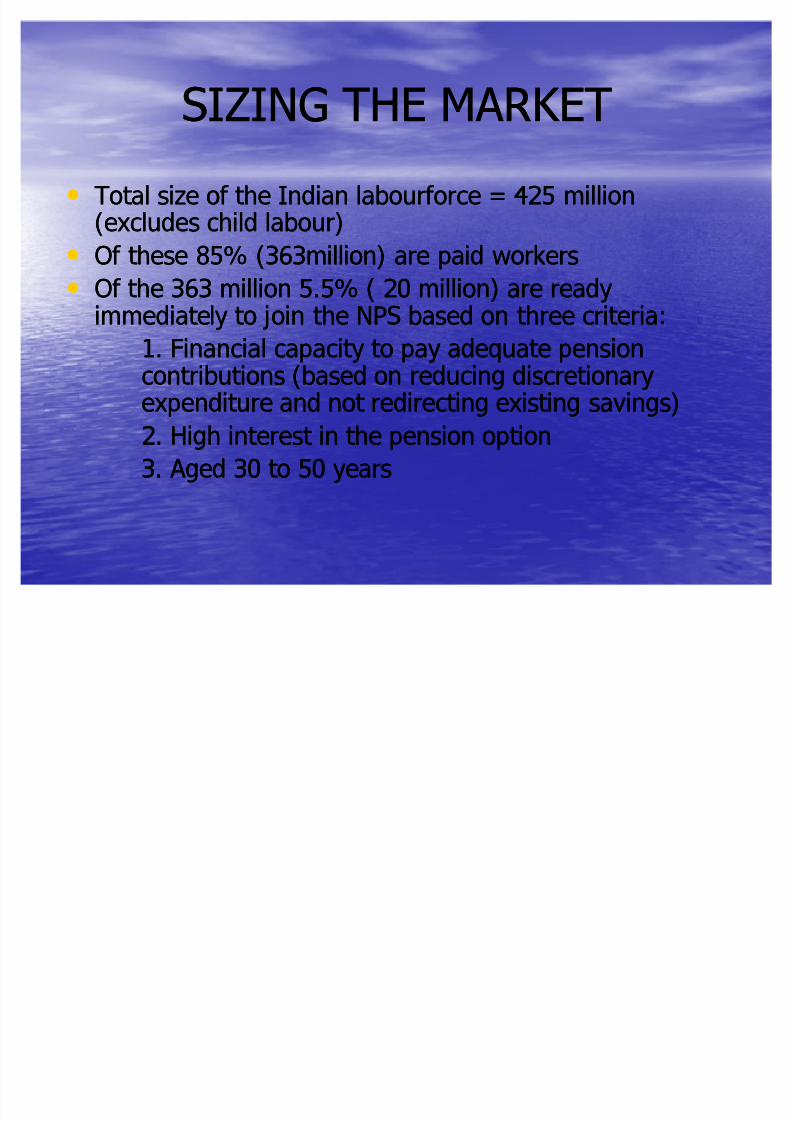

SIZING THE MARKETSIZING THE MARKET

Total size of the Indian labourforce = 425 millionTotal size of the Indian labourforce = 425 million(excludes child labour)(excludes child labour)

Of these 85% (363million) are paid workersOf these 85% (363million) are paid workers

Of the 363 million 5.5% ( 20 million) are readyOf the 363 million 5.5% ( 20 million) are readyimmediately to join the NPS based on three criteria:immediately to join the NPS based on three criteria:

1. Financial capacity to pay adequate pension1. Financial capacity to pay adequate pensioncontributions (based on reducing discretionarycontributions (based on reducing discretionary

expenditure and not redirecting existing savings)expenditure and not redirecting existing savings)2. High interest in the pension option2. High interest in the pension option

3. Aged 30 to 50 years3. Aged 30 to 50 years

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 16/26

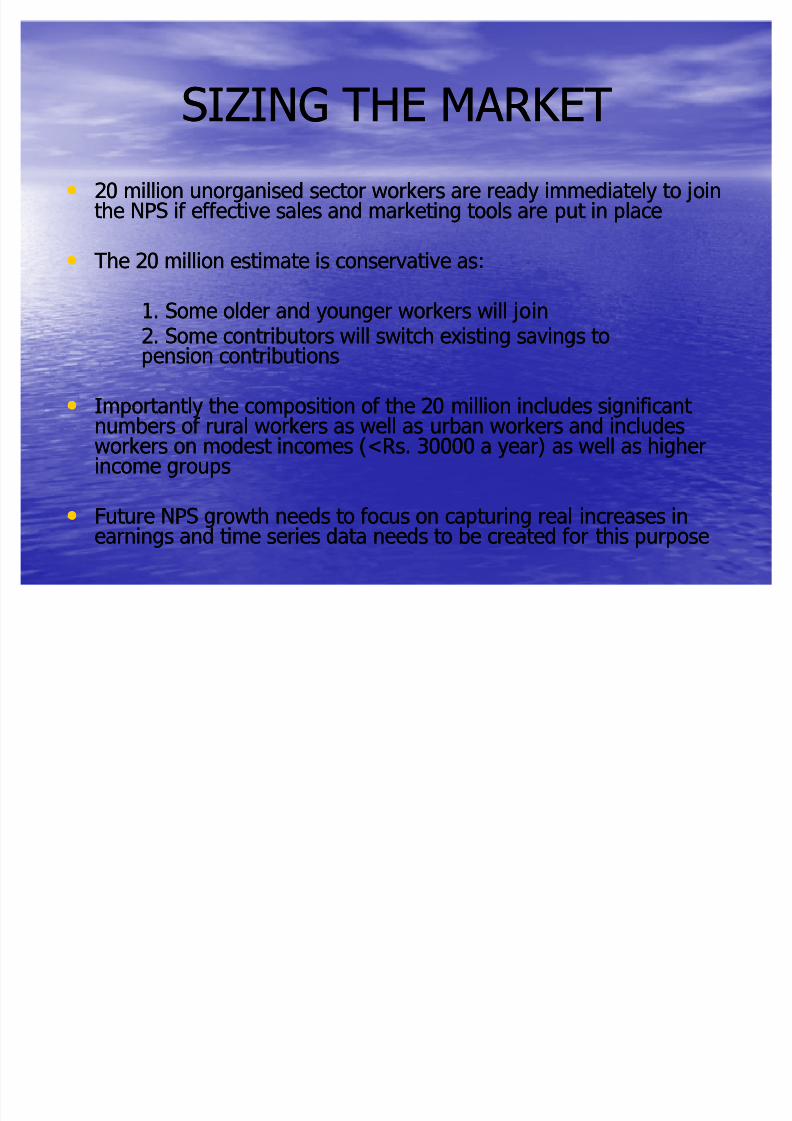

SIZING THE MARKETSIZING THE MARKET

20 million unorganised sector workers are ready immediately to join20 million unorganised sector workers are ready immediately to jointhe NPS if effective sales and marketing tools are put in placethe NPS if effective sales and marketing tools are put in place

The 20 million estimate is conservative as:The 20 million estimate is conservative as:

1. Some older and younger workers will join1. Some older and younger workers will join2. Some contributors will switch existing savings to2. Some contributors will switch existing savings topension contributionspension contributions

Importantly the composition of the 20 million includes significant Importantly the composition of the 20 million includes significant numbers of rural workers as well as urban workers and includesnumbers of rural workers as well as urban workers and includesworkers on modest incomes (<Rs. 30000 a year) as well as higherworkers on modest incomes (<Rs. 30000 a year) as well as higherincome groupsincome groups

Future NPS growth needs to focus on capturing real increases inFuture NPS growth needs to focus on capturing real increases inearnings and time series data needs to be created for this purposeearnings and time series data needs to be created for this purpose

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 17/26

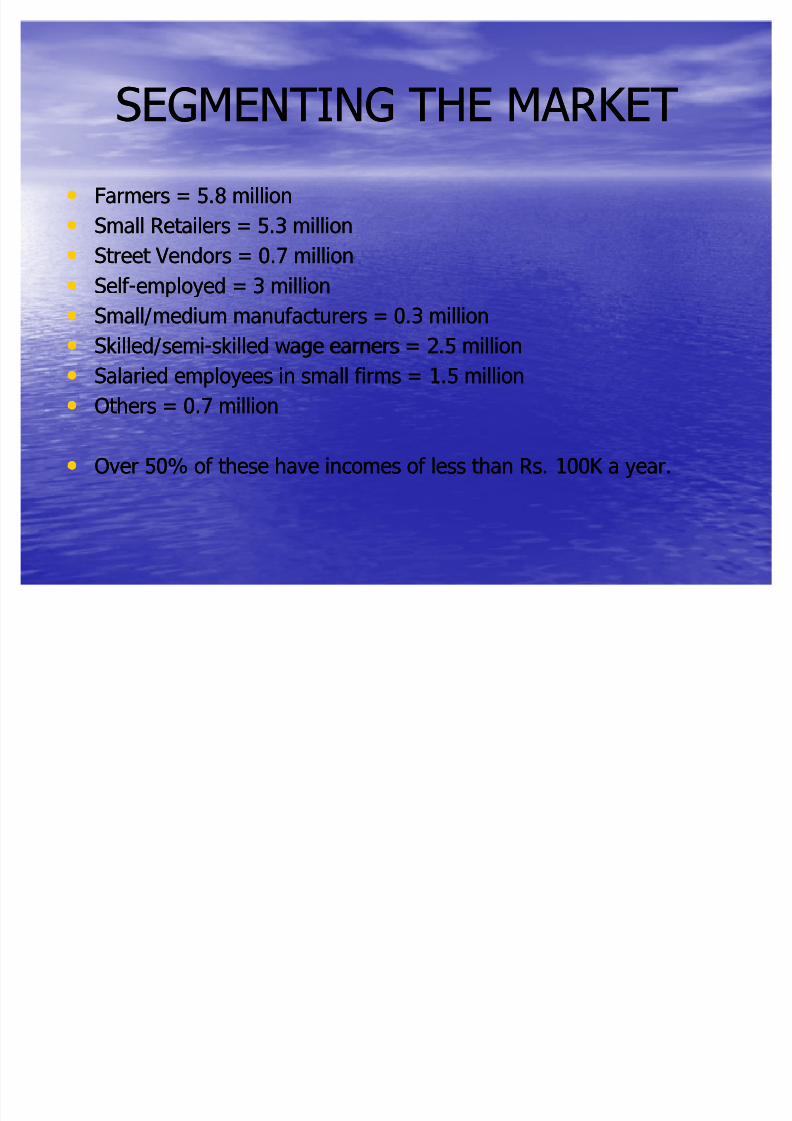

SEGMENTING THE MARKETSEGMENTING THE MARKET

Farmers = 5.8 millionFarmers = 5.8 million

Small Retailers = 5.3 millionSmall Retailers = 5.3 million

Street Vendors = 0.7 millionStreet Vendors = 0.7 million

Self Self--employed = 3 millionemployed = 3 million

Small/medium manufacturers = 0.3 millionSmall/medium manufacturers = 0.3 million

Skilled/semiSkilled/semi--skilled wage earners = 2.5 millionskilled wage earners = 2.5 million

Salaried employees in small firms = 1.5 millionSalaried employees in small firms = 1.5 million

Others = 0.7 millionOthers = 0.7 million

Over 50% of these have incomes of less than Rs. 100K a year.Over 50% of these have incomes of less than Rs. 100K a year.

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 18/26

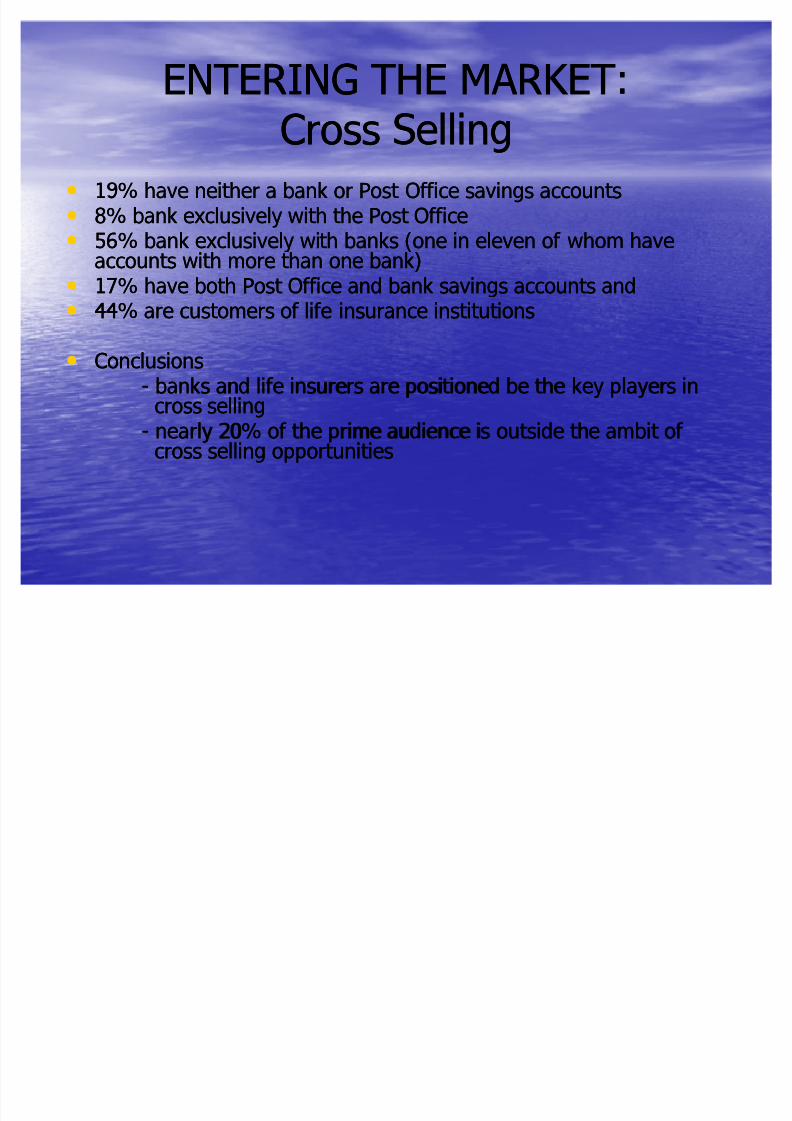

ENTERING THE MARKET:ENTERING THE MARKET:

Cross SellingCross Selling 19% have neither a bank or Post Office savings accounts19% have neither a bank or Post Office savings accounts 8% bank exclusively with the Post Office8% bank exclusively with the Post Office 56% bank exclusively with banks (one in eleven of whom have56% bank exclusively with banks (one in eleven of whom have

accounts with more than one bank)accounts with more than one bank)

17% have both Post Office and bank savings accounts and17% have both Post Office and bank savings accounts and 44% are customers of life insurance institutions44% are customers of life insurance institutions

ConclusionsConclusions-- banks and life insurers are positioned be the key players inbanks and life insurers are positioned be the key players in

cross sellingcross selling-- nearly 20% of the prime audience is outside the ambit of nearly 20% of the prime audience is outside the ambit of cross selling opportunitiescross selling opportunities

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 19/26

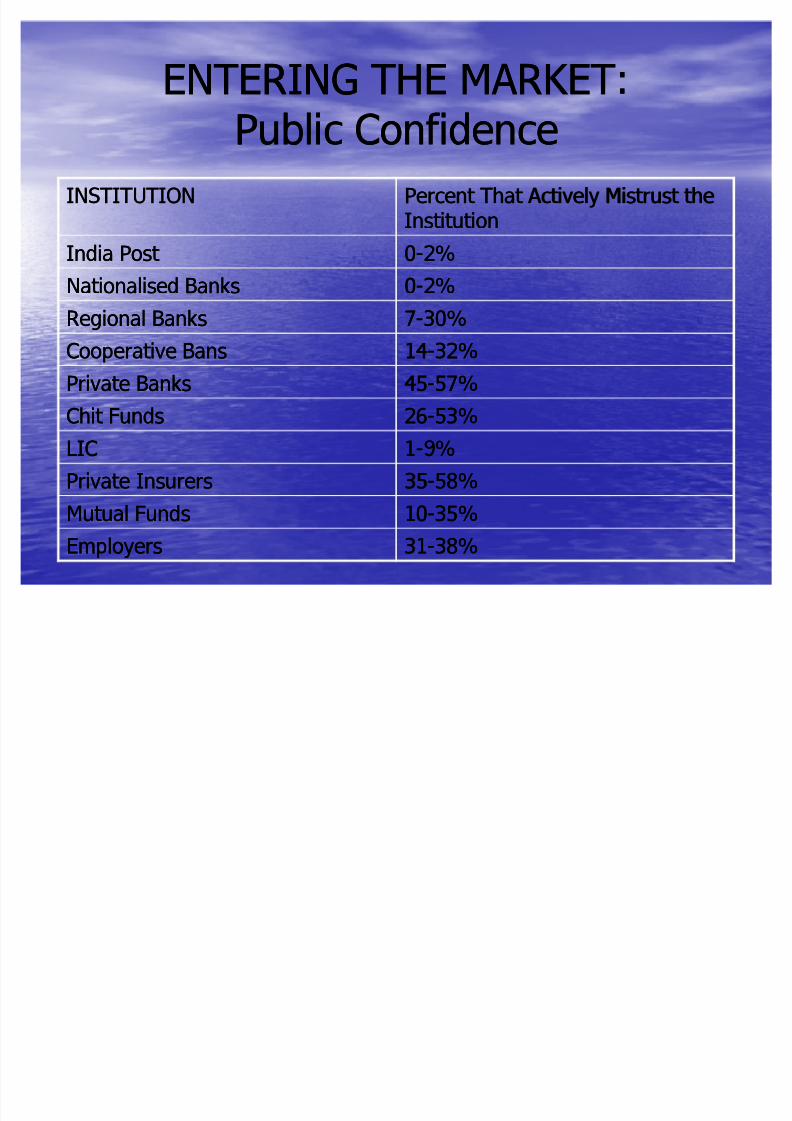

ENTERING THE MARKET:ENTERING THE MARKET:

Public ConfidencePublic ConfidenceINSTITUTIONINSTITUTION Percent That Actively Mistrust thePercent That Actively Mistrust the

InstitutionInstitution

India Post India Post 00--2%2%

Nationalised BanksNationalised Banks 00--2%2%

Regional BanksRegional Banks 77--30%30%

Cooperative BansCooperative Bans 1414--32%32%

Private BanksPrivate Banks 4545--57%57%

Chit FundsChit Funds 2626--53%53%LICLIC 11--9%9%

Private InsurersPrivate Insurers 3535--58%58%

Mutual FundsMutual Funds 1010--35%35%

EmployersEmployers 3131--38%38%

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 20/26

ENTERING THE MARKETENTERING THE MARKET

The Role of Commissioned AgentsThe Role of Commissioned Agents Sales efforts based on agent sales forces are problematicSales efforts based on agent sales forces are problematic

for the NPS that must operate on small margins tofor the NPS that must operate on small margins topromote participation by lower income groupspromote participation by lower income groups

Seeking alternatives to existing practices will beSeeking alternatives to existing practices will beimportant important

For NPS commercial partners there may be opportunitiesFor NPS commercial partners there may be opportunitiesto explore this issue more generally for other financialto explore this issue more generally for other financialproducts where commission taking is causing problemsproducts where commission taking is causing problems

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 21/26

ENTERING THE MARKET:ENTERING THE MARKET:Public information and EducationPublic information and Education

The Thematics of the NPSThe Thematics of the NPS1.1. People may fall into poverty in old age as they are not saving enoughPeople may fall into poverty in old age as they are not saving enough

presently to maintain living standards in retirement (already resonating)presently to maintain living standards in retirement (already resonating)2.2. There will be less joint and extended family support for the aged in theThere will be less joint and extended family support for the aged in the

future (already resonating)future (already resonating)3.3. A comfortable retirement is worth saving for (already resonating) A comfortable retirement is worth saving for (already resonating)4.4. Pensions are a means of providing financial security for wives and otherPensions are a means of providing financial security for wives and other

family members of contributors (not resonating)family members of contributors (not resonating)5.5. Longevity is extending and with it the need to save more for old age (not Longevity is extending and with it the need to save more for old age (not

resonating)resonating)6.6. The financial capacity of Government to financially support the aged willThe financial capacity of Government to financially support the aged will

continue to be limited (not resonating)continue to be limited (not resonating)7.7. Opportunities for extending working life into old age may be more limitedOpportunities for extending working life into old age may be more limited

in the future (not resonating)in the future (not resonating)8.8. Economic restructuring may mean periods of unemployment for those inEconomic restructuring may mean periods of unemployment for those in

traditional occupationstraditional occupations

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 22/26

ENTERING THE MARKET:ENTERING THE MARKET:

Delivering the MessageDelivering the Message The data points clearly to a number of issues that need to be consideredThe data points clearly to a number of issues that need to be considered

carefully and planned in before launch:carefully and planned in before launch:

1.1. Heads of households are the key financial decision makers (90% of Heads of households are the key financial decision makers (90% of

households) so targeting marketing efforts will be important households) so targeting marketing efforts will be important 2.2. 20% of agricultural and wage workers (1.5million) are illiterate and a20% of agricultural and wage workers (1.5million) are illiterate and afurther 20% (4 million) are functionally illiterate so oral messaging will befurther 20% (4 million) are functionally illiterate so oral messaging will beimportant important

3.3. Financial literacy is low generally so supportive financial advising systemsFinancial literacy is low generally so supportive financial advising systemswill be important will be important

4.4. Media access and habits vary greatly between segments with relativelyMedia access and habits vary greatly between segments with relatively

low penetration except for high income groups so media advertising willlow penetration except for high income groups so media advertising willneed to be segmented and targetedneed to be segmented and targeted5.5. Scheduled castes & tribes exceed 10% in most segments and are high inScheduled castes & tribes exceed 10% in most segments and are high in

some (>30% for wage workers) so NPS network access strategies willsome (>30% for wage workers) so NPS network access strategies willneed to be sensitive to these customers access preferencesneed to be sensitive to these customers access preferences

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 23/26

ENTERING THE MARKET:ENTERING THE MARKET:

Test Marketing?Test Marketing? Because of its size and complexity there are obviousBecause of its size and complexity there are obvious

dangers in attempting national implementation of thedangers in attempting national implementation of theNPS from a cold start NPS from a cold start

The experience of unsuccessfully marketing voluntaryThe experience of unsuccessfully marketing voluntarypensions in the past in India should be seen aspensions in the past in India should be seen assalutatory alsosalutatory also

Test marketing offers an opportunity to assess products,Test marketing offers an opportunity to assess products,sales & distribution approaches, financial advisorysales & distribution approaches, financial advisoryservices, monitoring & evaluation tools and management services, monitoring & evaluation tools and management

information systemsinformation systems It is possible from the data to identify optimum test It is possible from the data to identify optimum test

marketing locationsmarketing locations

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 24/26

CONCLUSIONSCONCLUSIONS

1. There is a significant dormant market for1. There is a significant dormant market forvoluntary pensions in India that extends acrossvoluntary pensions in India that extends across

economic sectors and occupational groupingseconomic sectors and occupational groupingsand down the income distributionand down the income distribution

-- Capturing this market will be primarily aCapturing this market will be primarily a

matter of effective marketingmatter of effective marketing

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 25/26

CONCLUSIONSCONCLUSIONS

2.2. The ADB project demonstrates the value of The ADB project demonstrates the value of evidence led planning and the national data set evidence led planning and the national data set created as part of the project provides a soundcreated as part of the project provides a sound

foundation to guide the NPS implementationfoundation to guide the NPS implementationplanplan

For PFRDA continuing in this vein byFor PFRDA continuing in this vein by

extending and supplementing the data overextending and supplementing the data overtime will be important for longtime will be important for long--term growth of term growth of the pension market the pension market

8/8/2019 Conclave Presentation Markets

http://slidepdf.com/reader/full/conclave-presentation-markets 26/26

CONCLUSIONSCONCLUSIONS

3.3. There are lessons also for the Indian financial sectorThere are lessons also for the Indian financial sectorgenerally in respect of other financial productsgenerally in respect of other financial products

-- The data reveal marketing opportunities among lowThe data reveal marketing opportunities among lowand lower middle income earners that to dateand lower middle income earners that to dateappear not have been exploited fully by the Indianappear not have been exploited fully by the Indianfinancial sectorfinancial sector

-- Investing in evidence led decision making to developInvesting in evidence led decision making to developthese markets will be important for growingthese markets will be important for growingbanking, insurance and equity markets generally inbanking, insurance and equity markets generally inIndiaIndia