ALP Presentation Draft 4.20.16

24

1 “Amazon-ing” Trained Solutions

-

Upload

havilah-driver -

Category

Documents

-

view

52 -

download

3

Transcript of ALP Presentation Draft 4.20.16

1

“Amazon-ing”Trained Solutions

P. Geissinger

Add date and may want to add title on "Amazon-ing" since that is how CSX group attending knows project

2

Agenda

I. Overview of Disruptor OrganizationII. 3D PrintingIII. 3rd Party Logistics ProvidersIV. VisibilityV. Driverless TrucksVI.Collapsible Containers

3

• Visibility

• Autonomous Vehicles

• Collapsible Containers

• 3D Printing• 3rd Party Logistics Providers

Disruptors are Organized into Watch and Do

Watch Do

The Internet of Things & Industry 4.0

The Internet of Things Supports all the Disruptors

4

5

Enterprise 3D Printing Grows and Refines

3D Printing software reads a digital file and uses additive manufacturing to make a 3-dimensional solid

67% of Manufacturers already own Tool for prototyping, product development, innovation Accounts for 95% of printed objects by volume

2006

2008

2010

2012

2014

2016

2018

2020

0

200

400

600

800

1000

3D Printing Industry Expected Revenue

Rev

enue

(in

mill

ion

$)

6

3D Printing Increases Time and Cost Expectations

Time and Efficiency

Time to marketDemand response

Lead timeMaterials

Business and Manufacturing PlansCost

InventoryLabor

Materials

FlexibilityDigital Business

Component Assembly

Consumers11%

Manufac-turing

Companies39%

Construc-tion and architec-

ture compa-

nies27%

Medical companies

23%

3-D Printing Industry Market Segmentation

Total Industry: $492.4 million

7

Prepare through Monitoring, Visibility, and Network Adjustments

Cost Sensitivity Monitor the adaption of 3D printing, especially in industries

like footwear, toys, ceramics, and major partners of CSX

Raw Materials for Component Printing

Rebalance customer portfolio to make it easy for smaller manufacturers to partner

Re-shoring and Fragmented

Manufacturing Market

Adjust network to respond to localized production and transportation

More Customer Acquisition

Opportunities Introduce new services such as logistics consulting

Time and Efficiency Introduce new infrastructure to communicate costs and time.

Clearly defined lead times are paramount

8

3PLs offer more service through their value chain

Raw material control, quality control, planning, and scheduling Inbound Logistics

Operations

Outbound Logistics

Marketing and sales

After-sales services

Department Responsibilities

Value Added Service

provided by contract logistics provider

Manufacturing, packaging, quality check, production control,

maintenance

Finishing of goods, material handling, dispatch, deliver, invoicing

Customer support management, order taking, market research, sales

optimization

Maintenance, warranty, training, installation, upgrades of products

9

3PL Consolidations are on the Rise

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

05

1015

3PL Acquisitions over $100M from 1999 - 2015

Number of Acquisitions

Key Takeaways• M&A increasing• Consolidation turns firms into logistics one-stop shops that

service all its clients’ supply chain functions• Highly concentrated

Success Stories• XPO Logistics acquired Conway and Norbert Dentressangle

Result• 157.2% revenue growth in 2015 of $606.3 million up from

$235.7 million in 2014

Success Stories • FedEx acquired French parcel delivery company TNT

Result• Increased market share from 10% to 22% in Europe’s

express delivery market

Impact on CSX• Logistics one stop-shops attract businesses outsourcing

more than one of their logistics functions (ex: intermodal and transportation management)

• Provide visibility from pre-rail to the end user• Likely increase customer’s willingness to pay higher prices

for premium services• Potentially take clientele from CSX

FedEx10%

TNT12%

UPS25%

DHL41%

Others12%

Estimated 2014 Market Share for International Shipments in Europe

10

3PLs affect Service Expectations and Business Volume

Value added services Provide real-time visibility

to customers Shift perception of

ShipCSX app from optional to necessary tool

Provide end-to-end supply chain visibility

Extends customer base

Diversifies service offerings

Expands geographic footprint and access to networks

Horizontal alliances Extends customer base Diversifies product and

service offerings Greater access to

transportation networks Provide end-to-end supply

chain visibility

Acquire a 3PL Partner with 3PLImprove ShipCSX

App

Visibility is an Essential Business Component

11

In a survey conducted by the Aberdeen Group of companies with predominately global supply chains 63% of companies indicated visibility as a high priority for improvement

In CSX’s survey, 94% responded to the question of “over the next 5 years what is the likelihood of supply chain visibility playing a role in your supply chain” with either extremely likely, very likely or moderately likely

Opportunities to Expand Visibility

12

Recommendation: More Visibility and ‘Freemium’ Pricing Model

13

Offer more visibility information through the ShipCSX App

Use a ‘freemium’ price versioning strategy Maintain relationships with customers and

outstanding service Offering the option to have access to visibility

information at a higher price point allows CSX to determine Demand Scalability

14

Driverless trucks hinder economic growth

8.7 Million truck drivers exist, and also create network effects such as motels businesses

Truck driver: the most common occupation by state

15

Driver Shortage Still on the Rise

Source : American Trucking Association. Driver Shortage Analysis 2015

Driverless Trucks will significantly affect the landscape of the trucking industry Driver Shortages will be addressed with more companies going autonomous CSX now has the potential for improved first mile and last mile delivery

2008 2011 20140

500010000150002000025000300003500040000

20,000

31,000

38,000

Truck Driver Shortage Growth

16

Driverless Truck timeline is closer than expected

http://www.huffingtonpost.com/scott-santens/self-driving-trucks-are-going-to-hit-us_b_7308874.html

17

Opportunities for CSX to sophisticate operations

Driver Shortage Eliminates the ever lasting problem logistics companies face. CSX now needn’t worry about pre and post freight transportation

Environmental Impact Lesser Carbon gas emissions through driverless trucks by factor of 20%

Line Haul Transportation

Helps to transport goods from offshore warehouses to intermodal terminal

Last Mile Delivery Autonomous ‘drones’ to help delivery to doorstep, as CSX looks to enhance last mile delivery

Safety A founding pillar for CSX. No requirement for drivers to stop after 11 hours, and not prone to human error.

18

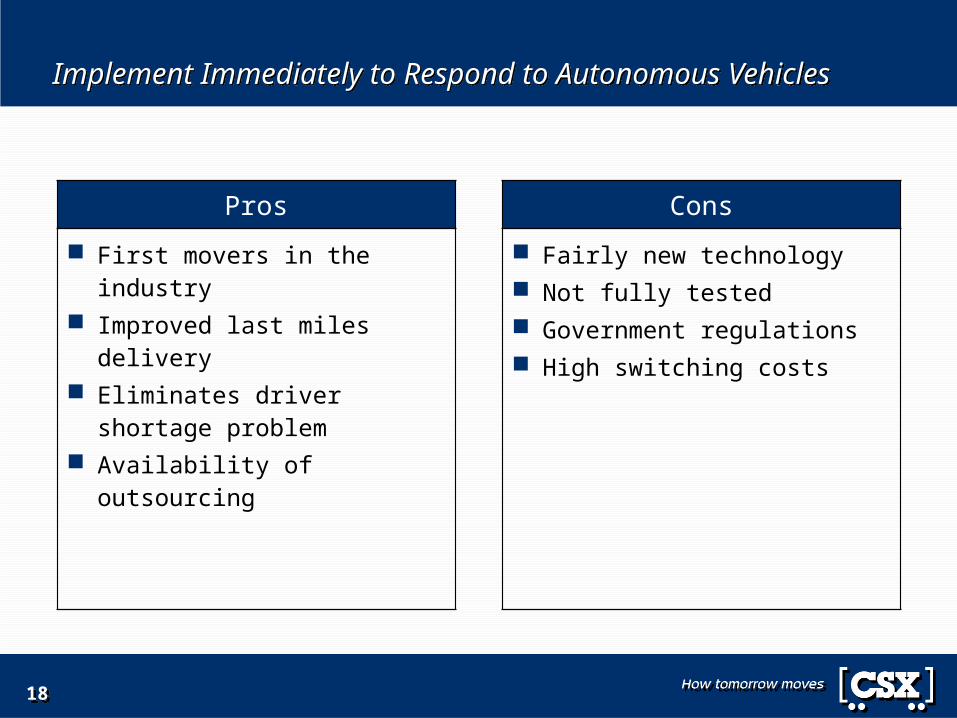

Implement Immediately to Respond to Autonomous Vehicles

Pros Cons

First movers in the industry Improved last miles delivery Eliminates driver shortage

problem Availability of outsourcing

Fairly new technology Not fully tested Government regulations High switching costs

19

Collapsible Containers Reduce Space Requirements for Empty Containers

Folds along hinges Only requires forklift Fits 5 containers in

space of 1 non-collapsed

Takes 30 seconds

20

Empty Containers are Stacking Up

LA NY/NJ0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Number of Containers Shipped From Ports(Expressed as ratio vs. previous year)

2014 2015Source: WSJ Logistics Report – “At U.S. Ports, Exports Are Coming Up Empty”

Growing number of empty containers due to international trade imbalance

Easier to ship containers back to refill quickly for max revenue

Costing shipping lines billions per year

21

Warehouse Fees

Shorter Length

Loading Speed

Fuel Efficiency

Smaller Footprint

Collapsible Containers Improve Efficiency

22

Less Space— Smaller facilities— Shorter trains— Lower fees

Image – ”greener” Reduce LTV cost by 80% Reduced rates possible for

customers with collapsible

Initial Investment poses risk— Who buys first— Benefits others more than CSX— Retrofit or buy new?

Training/learning time Benefits truckers and

international shippers more Exact time to deploy

uncertain

Recommend CSX Invests with customers and competitors

Share risk and cost by investing with other container shippers

Pros Cons

23

Acting earlier saves money

Technology is available now

Could be seen as more innovative and progressive railroad

Competition will benefit from tech more – don’t let them get head start

24

• Visibility

• Autonomous Vehicles

• Collapsible Containers

• 3D Printing• 3rd Party Logistics Providers

Conclusion

Watch Do